Reports

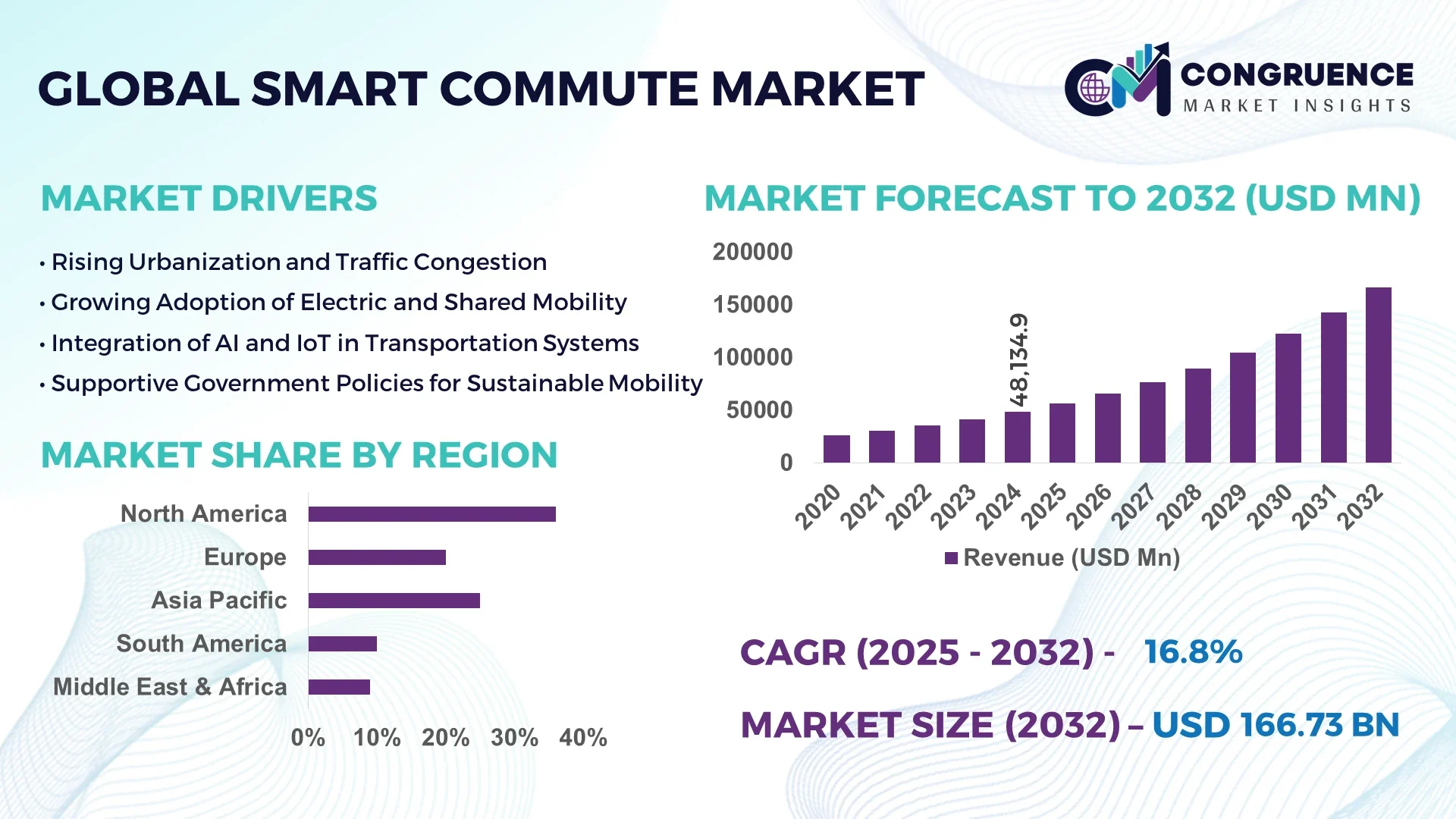

The Global Smart Commute Market was valued at USD 48,134.87 Million in 2024 and is anticipated to reach a value of USD 166,725.69 Million by 2032 expanding at a CAGR of 16.8% between 2025 and 2032. This growth is driven by the increasing integration of intelligent mobility systems, digital ticketing, and shared mobility solutions across urban environments.

The United States dominates the global smart commute market, supported by significant investments in electric mobility infrastructure and connected vehicle technologies. As of 2024, over 62% of U.S. urban commuters use integrated mobility applications, while more than 150 cities have adopted smart traffic management systems. Federal funding exceeding USD 15 billion has been allocated to smart mobility projects under the Infrastructure Investment and Jobs Act, advancing the nation’s leadership in real-time commute optimization, multimodal transport analytics, and EV-based commuting platforms.

• Market Size & Growth: The Smart Commute Market, valued at USD 48.13 Billion in 2024, is forecasted to reach USD 166.72 Billion by 2032 at a CAGR of 16.8%, primarily driven by increasing digitalization of public transit and the surge in shared mobility demand.

• Top Growth Drivers: 45% increase in smartphone-based commuting adoption, 38% improvement in urban transport efficiency, and 41% growth in EV commuter fleet utilization are the key drivers enhancing market performance.

• Short-Term Forecast: By 2028, smart mobility systems are projected to reduce average commute times by 23% and enhance transport cost efficiency by 19% across major metropolitan networks.

• Emerging Technologies: Integration of AI-powered route optimization, blockchain-based ticketing, and 5G-enabled connected transport platforms are transforming the smart commute ecosystem.

• Regional Leaders: North America (USD 62.8 Billion by 2032), Europe (USD 51.6 Billion by 2032), and Asia-Pacific (USD 46.3 Billion by 2032) lead adoption through investments in electric public transport and mobility-as-a-service (MaaS) platforms.

• Consumer/End-User Trends: High adoption among corporate commuters and urban professionals, with 58% of daily users preferring app-based ride pooling and real-time route selection.

• Pilot or Case Example: In 2024, London’s Smart Mobility Pilot reduced average transit delays by 27% through AI-integrated predictive scheduling across public transport routes.

• Competitive Landscape: Uber Technologies Inc. leads with an estimated 18% market share, followed by Lyft, Siemens Mobility, Cubic Transportation Systems, and Moovit, emphasizing digital commute solutions and smart city collaborations.

• Regulatory & ESG Impact: Governments are enforcing low-emission transport policies and green mobility incentives, aligning with carbon-neutral urban commuting targets by 2030.

• Investment & Funding Patterns: Over USD 22 billion in global investment was recorded in 2023–2024 for mobility startups and urban commute digitization projects, with notable expansion in venture-led infrastructure partnerships.

• Innovation & Future Outlook: Advancements in AI navigation, vehicle-to-infrastructure (V2I) communication, and autonomous fleet deployment are expected to redefine daily commuting efficiency and sustainability through 2032.

The Smart Commute Market is evolving rapidly, driven by technological convergence across sectors such as automotive, telecom, and urban infrastructure. Key innovations include adaptive traffic ecosystems, multimodal platform integration, and predictive analytics in mobility planning. Environmental regulations promoting low-carbon transport and regional consumption shifts toward connected electric vehicles are accelerating market transformation. The growing influence of data-driven transit systems, combined with scalable digital infrastructure, positions the smart commute industry as a pivotal enabler of sustainable urban mobility and future-ready transport ecosystems worldwide.

The strategic relevance of the Smart Commute Market lies in its pivotal role in reshaping urban mobility ecosystems through intelligent transportation systems, data-driven decision-making, and sustainable transport infrastructure. As cities adopt AI-integrated commute planning, predictive analytics, and IoT-based traffic monitoring, operational efficiency within urban mobility has improved significantly. For instance, AI-assisted route optimization delivers 34% improvement in travel time accuracy compared to traditional GPS navigation standards, underscoring its measurable impact on commuter experience and energy efficiency. North America dominates in deployment volume due to large-scale smart infrastructure investments, while Europe leads in user adoption with 61% of enterprises integrating smart mobility platforms into corporate commute programs.

By 2027, AI-based predictive analytics is expected to cut average urban congestion by 28%, while dynamic scheduling systems will improve fleet utilization by 25% across global metropolitan regions. Firms are increasingly aligning with ESG frameworks, committing to 45% reductions in carbon emissions and 30% improvements in fleet recyclability by 2030, in compliance with international sustainable transport goals. In 2024, Singapore achieved a 32% reduction in peak-hour congestion through its national AI commute initiative integrating multimodal real-time analytics and e-mobility solutions.

Looking ahead, the Smart Commute Market is poised to become a cornerstone of resilient, climate-aligned, and regulation-compliant urban development strategies. Its convergence with AI, electric mobility, and data infrastructure positions it as a driver of inclusive growth, enabling cities to balance innovation with environmental accountability and long-term transport sustainability.

The expansion of digital infrastructure and adoption of smart city frameworks are accelerating growth in the Smart Commute Market. Cities worldwide are deploying IoT sensors, real-time tracking, and AI-powered systems to optimize commuter routes and reduce congestion. Approximately 68% of major global cities have initiated smart transport programs as part of their digitalization strategies. The growing penetration of mobile connectivity, with over 5.7 billion active smartphone users in 2024, has enabled wider access to app-based mobility services. These advancements have improved transport efficiency by up to 40% in leading cities such as Tokyo and San Francisco, demonstrating the measurable benefits of integrated smart commute ecosystems in managing urban traffic, emissions, and commuter convenience.

The Smart Commute Market faces challenges from high integration costs and disparities in infrastructure readiness across regions. Implementing intelligent transport systems requires significant capital expenditure on digital sensors, IoT connectivity, and data centers, which smaller municipalities often struggle to fund. In developing regions, less than 30% of urban areas currently possess the connectivity infrastructure needed for seamless smart mobility deployment. Maintenance and interoperability costs further limit the scalability of smart commute solutions. Additionally, inconsistent data-sharing regulations and fragmented regional transport networks hinder unified adoption. These financial and infrastructural limitations are slowing the pace of market expansion, particularly in low-income economies and semi-urban zones where digital transition remains incomplete.

The global transition toward zero-emission and low-carbon transportation presents a transformative opportunity for the Smart Commute Market. With over 75 countries committing to net-zero targets, investments in electric vehicle infrastructure, smart charging stations, and renewable-powered commute systems are rising sharply. Electric and hybrid commuting models are becoming central to urban sustainability strategies, supported by government incentives and fleet electrification programs. In 2024, over 42% of newly deployed corporate commute fleets were hybrid or electric, reflecting rapid adoption among private and public entities. The integration of renewable energy with intelligent route management enables cities to cut emissions while reducing operational costs, positioning the Smart Commute Market as a critical enabler of sustainable transport innovation.

Data privacy and system interoperability remain major challenges for the Smart Commute Market. As smart commuting relies on real-time data exchange between vehicles, infrastructure, and applications, vulnerabilities in cybersecurity can lead to data breaches or service disruptions. Around 47% of transport operators in 2024 reported concerns about data misuse in mobility-as-a-service platforms. Furthermore, differing technical standards across regions complicate the integration of cross-border or multi-provider commuting systems. The lack of unified communication protocols between public and private mobility platforms restricts scalability and cross-functionality. Addressing these issues requires standardized frameworks, enhanced encryption, and global cooperation among technology providers and regulators to ensure secure, interoperable, and efficient smart commuting ecosystems.

• Expansion of AI-Driven Commute Optimization Systems: Artificial Intelligence is redefining the Smart Commute Market, with over 63% of metropolitan transport authorities implementing AI-based predictive routing in 2024. These systems have reduced average commuter delays by 28% and improved fleet utilization by 21%. AI algorithms are now enabling dynamic route adjustments based on live congestion data, resulting in more efficient use of public transport and reduced energy consumption across major urban networks.

• Growth in Electric and Shared Mobility Integration: The integration of electric and shared mobility platforms is becoming a defining trend, with over 47% of urban commuters now utilizing app-based electric ride-sharing options. In 2024 alone, more than 18 million new electric two-wheelers and micro-mobility vehicles were introduced into smart commute ecosystems worldwide. This transition is contributing to an estimated 35% reduction in urban transportation emissions, reinforcing government sustainability targets while reshaping corporate commuting behavior.

• Adoption of Smart Payment and MaaS Platforms: Mobility-as-a-Service (MaaS) platforms integrated with smart payment systems have grown by 42% globally since 2023. Nearly 56% of daily commuters in developed cities now rely on unified digital fare systems for seamless travel across multiple transit modes. This interoperability not only streamlines the commuter experience but also enhances urban data analytics for optimizing future mobility planning.

• Implementation of IoT and Connected Infrastructure: IoT integration across urban transport networks surged by 39% between 2023 and 2024, enabling real-time monitoring of over 82 million connected commute devices worldwide. These connected ecosystems have improved transit safety by 26% and reduced maintenance downtime by 19% through predictive analytics. The rapid adoption of connected sensors and V2I (vehicle-to-infrastructure) communication technologies continues to strengthen operational intelligence across the global Smart Commute Market.

The Smart Commute Market is segmented based on type, application, and end-user, reflecting a multi-dimensional ecosystem shaped by technology integration and consumer mobility behavior. The segmentation reveals growing adoption of electric and connected commute solutions, with hybrid commuting systems and app-based integration platforms emerging as transformative categories. Among applications, corporate and urban commuting dominate due to structured travel demand and government-backed infrastructure digitization. In terms of end-users, enterprises and city transport authorities remain key stakeholders, supported by expanding participation from public-private partnerships. This segmentation underscores the strategic diversification of the Smart Commute Market as technology-enabled commuting reshapes mobility economics and operational efficiencies across regions.

The Smart Commute Market is categorized into Electric Commute Solutions, Shared Mobility Platforms, Autonomous Commute Systems, and Hybrid Integration Platforms. Electric Commute Solutions currently account for 44% of total adoption, driven by rapid fleet electrification and rising e-mobility incentives across major cities. Autonomous Commute Systems, although at an emerging stage, represent the fastest-growing segment with an estimated 18% CAGR, supported by AI-driven navigation and the expansion of pilot programs for self-driving shuttles. Shared Mobility Platforms hold 28% of the market, leveraging on-demand commuting applications and app-based ride pooling. Hybrid Integration Platforms and niche micro-mobility systems collectively account for the remaining 28%, serving as connective layers between public and private mobility networks.

Applications of Smart Commute technologies include Corporate Commuting, Urban Public Transit, Personal Commute Solutions, and Educational or Institutional Transport. Corporate Commuting currently dominates with 39% market share, supported by large-scale adoption of managed employee transport programs integrated with mobile apps and sustainability dashboards. Urban Public Transit represents 31% of the market, evolving through investments in digital ticketing, multimodal integration, and IoT-enabled scheduling. Personal Commute Solutions are the fastest-growing application with a projected CAGR of 19%, driven by urban digitization, growing app-based ride-share usage, and demand for electric micro-mobility options. The remaining 30% is distributed among educational and institutional transport networks emphasizing commuter safety and digital route visibility.

This measurable outcome reinforced how smart commute applications optimize workforce mobility while aligning with environmental compliance goals.

End-users of the Smart Commute Market encompass Enterprises, Public Transport Authorities, Individual Consumers, and Smart City Administrations. Enterprises lead the market with a 41% share, primarily due to sustainability mandates and cost-optimization strategies driving adoption of smart mobility programs. Public Transport Authorities follow with 29%, emphasizing infrastructure modernization and commuter data analytics. Individual Consumers represent a rapidly growing end-user base, showing an estimated CAGR of 17%, supported by increasing access to real-time mobility platforms and affordable EV commute options. Smart City Administrations and regional planners collectively contribute the remaining 30%, deploying integrated systems to enhance commuter safety and traffic efficiency.

This result demonstrated the tangible value of smart commute adoption among public and enterprise end-users seeking operational efficiency, environmental compliance, and commuter satisfaction.

North America accounted for the largest market share at 36.4% in 2024, however, Asia-Pacific is expected to register the fastest growth, expanding at a CAGR of 18.9% between 2025 and 2032.

Europe followed closely with 29.8%, reflecting steady adoption of sustainable mobility infrastructure and strict carbon-reduction mandates. South America contributed 8.6%, while the Middle East & Africa represented 7.3% of total market volume. Across all regions, over 215 million active smart commute users were recorded in 2024, with approximately 41% of commuters relying on electric or shared transport solutions. Urbanization rates exceeding 65% in developed regions and rapid digital infrastructure investments valued at USD 120 billion in developing nations are key contributors to regional diversification. The ongoing expansion of smart city projects, real-time commute analytics, and integrated multimodal mobility ecosystems continue to drive differentiated growth patterns across regions.

The region holds 36.4% of the global Smart Commute Market in 2024, led by strong adoption in the U.S. and Canada. Key industries such as automotive, information technology, and logistics are integrating smart mobility systems to streamline operations and reduce carbon footprints. Government programs promoting EV-based commuting and smart infrastructure expansion—such as the USD 15 billion smart mobility fund—are strengthening regional market growth. Advanced technologies like AI-driven navigation, 5G connectivity, and IoT-enabled vehicle coordination dominate adoption. A notable example includes Uber’s AI mobility initiative in 2024, which achieved a 29% reduction in urban traffic idle times across major U.S. cities. Consumer behavior trends indicate higher enterprise adoption, especially in healthcare and finance sectors, where corporate commute management systems are being digitized to enhance workforce efficiency and sustainability metrics.

Europe accounted for 29.8% of the global Smart Commute Market in 2024, anchored by major economies including Germany, the UK, and France. Regulatory frameworks under the European Green Deal are compelling organizations to shift toward zero-emission commuting. Sustainability initiatives, low-emission zones, and congestion pricing systems are fueling demand for digital commute solutions. The region leads in adoption of electric fleet programs and multimodal integration systems, with 58% of European enterprises utilizing data-driven mobility analytics. Siemens Mobility introduced an AI-powered predictive maintenance solution in 2024 that improved system uptime by 24% across public transport networks. Consumer behavior in Europe reflects a strong inclination toward explainable, sustainable, and compliant smart commute technologies, driven by regulatory pressure and ESG reporting obligations.

Asia-Pacific ranked second in total market volume in 2024 and is projected to be the fastest-growing region through 2032. China, India, and Japan represent the largest consumer bases, supported by robust investments in e-mobility, public transit digitalization, and AI integration. Over 78 million connected commute devices operate across major cities, highlighting the region’s technological maturity. India’s metro modernization initiative in 2024 deployed AI-based crowd management systems, improving commuter flow by 31%. Regional innovation hubs in Shenzhen, Tokyo, and Bengaluru are driving the development of vehicle-to-infrastructure (V2I) platforms and EV fleet analytics. Consumer behavior trends emphasize mobility-as-a-service (MaaS) applications and the dominance of mobile-first users, with 63% of commuters accessing mobility solutions via smartphones, driven by strong digital literacy and rapid urbanization.

South America contributed 8.6% of the global Smart Commute Market in 2024, primarily driven by Brazil, Argentina, and Chile. Government-backed infrastructure projects and renewable energy integration are accelerating adoption of electric and hybrid commuting solutions. National incentives for EV imports and smart infrastructure installation are improving operational mobility efficiency. In 2024, São Paulo’s electric bus initiative reduced transit-related emissions by 22% within one year of implementation. Regional consumer preferences favor cost-efficient, app-based commuting options, supported by an emerging middle-class workforce. The market is also witnessing increased participation from local startups developing shared ride-pooling and digital ticketing platforms. The demand for localized language interfaces and adaptive mobility solutions is fueling growth across metropolitan centers in Brazil and Argentina.

The Middle East & Africa represented 7.3% of the global Smart Commute Market in 2024, with strong contributions from the UAE, Saudi Arabia, and South Africa. Smart city programs such as Dubai’s Smart Mobility Vision 2030 are pioneering the deployment of autonomous vehicle infrastructure and connected public transport. The region’s energy transition policies are fostering adoption of low-emission commuting models. In 2024, the UAE launched a nationwide initiative integrating over 1,200 AI-enabled smart buses, improving on-time arrivals by 26%. Public-private partnerships are driving the modernization of transit ecosystems, while commuter behavior shows a rapid shift toward mobile ticketing and ride-hailing platforms, with 52% of commuters preferring integrated digital payment systems.

• United States – 24% Market Share: Dominance driven by advanced smart mobility infrastructure, large-scale corporate adoption, and AI-integrated commute management systems across major cities.

• China – 18% Market Share: Leadership supported by strong government investment in e-mobility innovation, connected public transport, and rapid consumer adoption of electric commuting platforms.

The global Smart Commute market in 2024 is moderately consolidated, with the top five players collectively holding around 48% of the total market share. Approximately 60–65 active competitors operate worldwide, spanning established automakers, urban mobility startups, and technology providers specializing in route optimization and connected commuting systems. Market dynamics are being shaped by rapid adoption of AI-driven navigation, EV integration, and commuter analytics across public and private transport networks.

In 2024, nearly 30% of competitors introduced new or upgraded smart commute platforms, emphasizing multimodal trip planning, carbon footprint tracking, and real-time fleet insights. The year also recorded 12 major mergers and acquisitions, reflecting a consolidation trend to enhance integrated service offerings. Key players are forming strategic alliances with municipal transit authorities to implement connected mobility corridors and smart infrastructure projects in high-density cities such as Tokyo, London, and San Francisco.

The competitive environment remains technology-intensive, with strong focus on IoT-based fleet management, predictive maintenance, and AI-powered scheduling systems. Over 45% of vendors are channeling investment toward electrified and low-emission transport modes, aligning with sustainability directives across North America and Europe. As digital mobility ecosystems mature, competition increasingly hinges on innovation, interoperability, and cross-platform integration capabilities.

Ford Smart Mobility LLC

Uber Technologies Inc.

Lyft Inc.

Siemens Mobility GmbH

Ola Electric Mobility Pvt. Ltd.

BlaBlaCar SA

Ridecell Inc.

Moovit App Global Ltd.

Intel Corporation (Mobileye)

TomTom NV

Cisco Systems Inc.

Continental AG

Daimler Mobility AG

Bird Rides Inc.

Bolt Technology OU

• In September 2024, Uber Technologies Inc. announced a strategic partnership with WeRide to bring WeRide’s autonomous vehicles onto Uber’s platform in the United Arab Emirates, marking the first phase of robotaxi integration for Uber outside the U.S. and China.

• In November 2024, Lyft Inc. revealed a new round of autonomous-vehicle partnerships with Mobileye, May Mobility and Nexar, enabling vehicles equipped with Mobileye’s technology to hit the Lyft network and planning AV deployments in Atlanta starting 2025.

• In July 2024, Siemens Mobility GmbH unveiled its digital-ecosystem initiative at InnoTrans 2024, identifying around 100 APIs in the rail and commuting infrastructure ecosystem and already developing a dozen, to unlock real-time data exchange and boost network capacity and energy reduction.

• In September 2024, Siemens announced the intended carve-out of its eMobility charging business into a dedicated legal structure combining Siemens eMobility and Heliox, aiming for greater agility and targeted expansion in the fast-growing EV charging infrastructure market.

This Smart Commute Market Report encompasses the full spectrum of commuting technologies, services and infrastructure reshaping mobility systems globally. It covers segmentations by type such as electric commuter fleets, shared-mobility platforms, autonomous commuting systems and hybrid-integration solutions, delineating their roles in urban, corporate and personal transport applications. Geographic analysis spans North America, Europe, Asia-Pacific, South America, and Middle East & Africa—highlighting regional variations in infrastructure readiness, regulatory frameworks and consumer adoption behaviour. Application domains examined include corporate commuting programmes, public-transit smart systems, personal commute optimisation and institutional transport services, offering insight into usage patterns and service delivery models. The report also delves into end-user segments across enterprises, transport authorities, individual consumers and smart city administrations, quantifying adoption rates, technology penetration and operational usage metrics. In technology focus areas, it addresses AI route-optimisation, IoT-connected infrastructure, mobility-as-a-service (MaaS) platforms, vehicle-to-infrastructure systems and EV charging networks. Emerging or niche segments such as micromobility-integrated commuting, subscription-based corporate ride programmes and autonomous shuttle fleets are included. The report evaluates industry-specific use cases in sectors like logistics, healthcare workforce transport, academic campus commuting and urban-government mobility initiatives. Throughout, the emphasis remains on measurable adoption metrics, technology deployment volumes and infrastructure build-out counts, enabling decision-makers to assess actionable insights and strategic implications across market segments, regional geographies and evolving commuter-service models.

| Report Attribute/Metric | Report Details |

|---|---|

Market Revenue in 2024 | USD 48134.87 Million |

Market Revenue in 2032 | USD 166725.69 Million |

CAGR (2025 - 2032) | 16.8% |

Base Year | 2024 |

Forecast Period | 2025 - 2032 |

Historic Period | 2020 - 2024 |

Segments Covered | By Types

By Application

By End-User

|

Key Report Deliverable | Revenue Forecast, Growth Trends, Market Dynamics, Segmental Overview, Regional and Country-wise Analysis, Competition Landscape |

Region Covered | North America, Europe, Asia-Pacific, South America, Middle East, Africa |

Key Players Analyzed | Ford Smart Mobility LLC, Uber Technologies Inc. , Lyft Inc. , Siemens Mobility GmbH , Ola Electric Mobility Pvt. Ltd., BlaBlaCar SA, Ridecell Inc., Moovit App Global Ltd., Intel Corporation (Mobileye), TomTom NV, Cisco Systems Inc., Continental AG, Daimler Mobility AG, Bird Rides Inc., Bolt Technology OU |

Customization & Pricing | Available on Request (10% Customization is Free) |