Reports

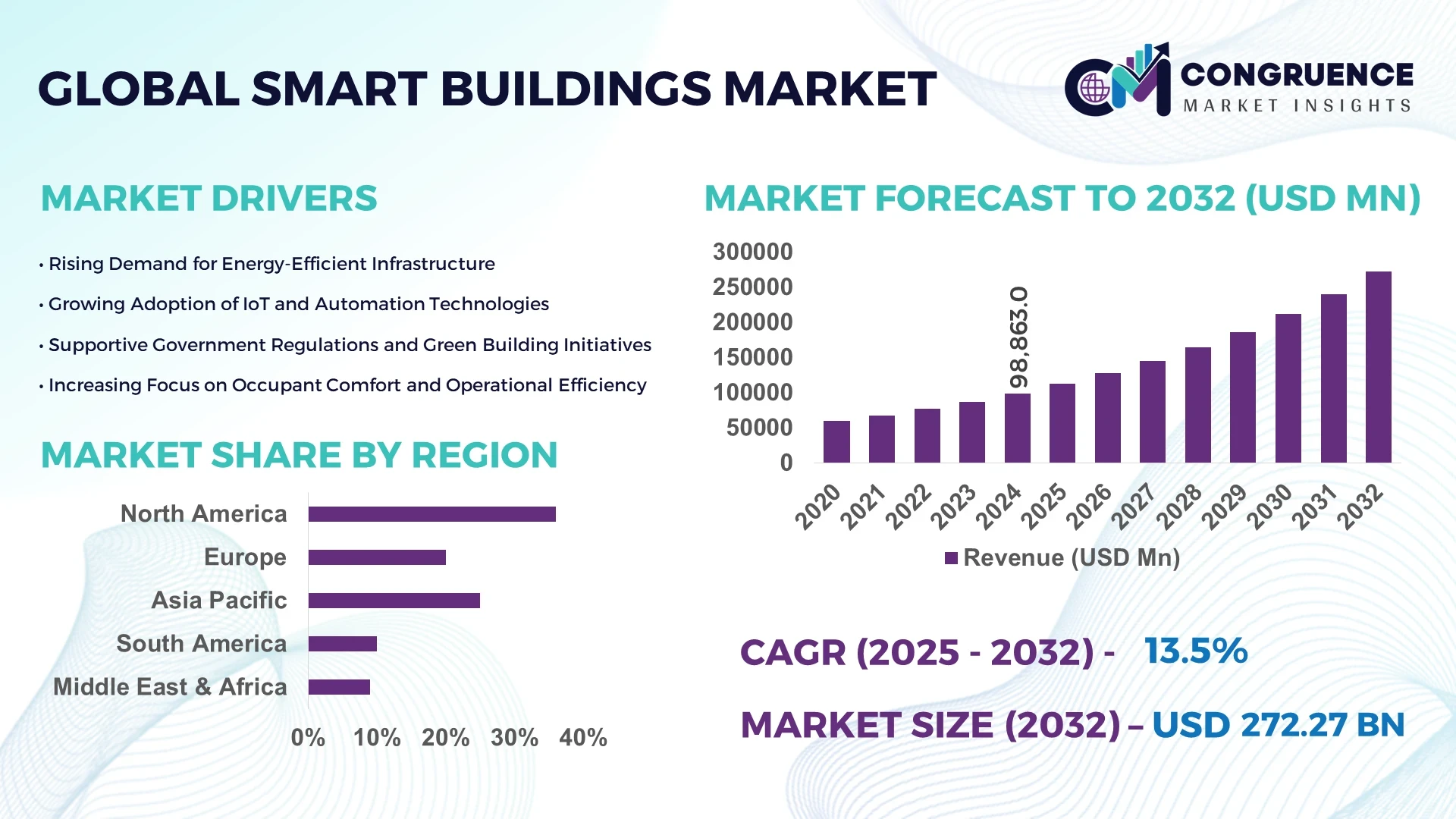

The Global Smart Buildings Market was valued at USD 98863 Million in 2024 and is anticipated to reach a value of USD 272270 Million by 2032 expanding at a CAGR of 13.5% between 2025 and 2032. This growth is driven by rising focus on energy efficiency and digital building infrastructure.

In the United States, major investment in building automation has propelled advanced deployments: over USD 24.66 billion was recorded in the U.S. smart building market in 2024, with projections reaching around USD 68.67 billion by 2034 at a CAGR of 10.78%. Key applications in the U.S. include commercial office parks and institutional buildings equipped with IoT-enabled HVAC, occupancy sensors, and edge-analytics platforms. The government’s Federal Smart Buildings Accelerator (FSBA) under the U.S. Department of Energy provided technical support and assessments for federal facilities to adopt grid-interactive efficient building technologies.

Market Size & Growth: Valued at approx. USD 98.9 billion in 2024, expected to reach USD 272.3 billion by 2032 at a CAGR of 13.5%; driven by smart infrastructure investments.

Top Growth Drivers: Energy management system upgrades ~58 %, IoT sensor adoption ~46 %, retrofit of legacy buildings ~39 %.

Short-Term Forecast: By 2028, smart building installations are expected to reduce operational energy costs by ~22 % and improve occupant-space utilization by ~18 %.

Emerging Technologies: AI-powered predictive maintenance platforms, 5G/edge-connected building control systems, digital twin modelling of building operations.

Regional Leaders: North America – projected USD 95 billion by 2032 with widespread enterprise adoption; Asia-Pacific – projected USD 78 billion by 2032 driven by urban infrastructure roll-out; Europe – projected USD 65 billion by 2032 with strong regulatory push for sustainability.

Consumer/End-User Trends: Commercial (office, retail, hospitality) buildings are leading adopters, with increased demand for occupant comfort, health monitoring, and flexible space management.

Pilot or Case Example: In 2024, a federal building retrofit under the FSBA achieved ~15 % reduction in energy consumption and improved predictive maintenance uptime by ~12 %.

Competitive Landscape: Market leader holds approx. ~18 % share; major competitors include Siemens AG, Johnson Controls International plc, Honeywell International Inc., Schneider Electric SE, ABB Ltd..

Regulatory & ESG Impact: Building codes, green-certification incentives, energy-efficiency mandates and ESG disclosure requirements are accelerating adoption of smart buildings.

Investment & Funding Patterns: Recent investments exceed USD 5.5 billion in venture funding and project finance for building-management and automation platforms, with increased interest in outcome-based financing models.

Innovation & Future Outlook: Integration of renewables, storage, building-to-grid interaction, occupant-behaviour analytics, scalable retrofits of legacy portfolios are shaping next-gen smart building ecosystems.

Smart buildings are now being deployed across commercial, residential and industrial sectors with the commercial segment contributing the largest share. Recent innovations include digital-twin-enabled operations, AI-driven fault detection and cloud-native building management systems. Regulatory frameworks such as energy-performance mandates and sustainability certifications are strongly influencing adoption in developed regions, while emerging markets are experiencing rapid growth due to urbanisation and smart-city initiatives. Future outlook indicates increasing integration of renewable energy and grid-interactive buildings, demand for occupant-centric services and scalable retrofit business models will drive the market expansion.

The Smart Buildings Market has become strategically vital as organizations prioritize digital transformation, operational efficiency, and sustainability goals. Smart infrastructure powered by IoT, AI, and advanced analytics is redefining the built environment by enabling real-time monitoring, predictive maintenance, and optimized energy management. AI-based building automation delivers up to 28% improvement in energy efficiency compared to legacy building management systems, reducing operational costs and carbon emissions simultaneously. In regional comparison, North America dominates in volume, owing to extensive commercial infrastructure, while Europe leads in adoption, with over 61% of enterprises implementing some form of building automation system by 2024. By 2027, the integration of edge computing and digital twins is expected to improve asset lifecycle efficiency by 32% and reduce downtime by 18%.

From a compliance and ESG perspective, firms are committing to carbon-intensity reductions of 40% by 2030, aligning with global net-zero targets and green building certification frameworks such as LEED and BREEAM. In 2024, Siemens AG achieved a 25% operational energy reduction across its global facilities through AI-integrated smart control systems. Future pathways indicate greater interoperability between renewable microgrids, grid-interactive efficient buildings, and circular-economy-based infrastructure. The Smart Buildings Market is thus positioned as a pillar of resilience, compliance, and sustainable growth, bridging the gap between digital intelligence and environmental stewardship.

The surge in IoT and automation adoption is a primary driver of the Smart Buildings Market, transforming traditional infrastructure into responsive, intelligent ecosystems. Over 75 billion IoT-connected devices are projected globally by 2025, with a significant share attributed to smart building applications such as HVAC monitoring, access control, and lighting automation. Automated energy management has shown efficiency improvements of up to 30%, reducing operational expenditures for commercial and industrial users. Integration with cloud-based systems allows centralized control of multisite operations, while data analytics enhances predictive maintenance. This convergence of IoT and automation strengthens the market’s strategic relevance by ensuring cost-effective, scalable, and sustainable building operations.

Despite rapid digitization, cybersecurity vulnerabilities and lack of interoperability standards remain critical restraints for the Smart Buildings Market. Connected devices exchange vast volumes of sensitive data, making them potential targets for cyber threats. Reports indicate that over 40% of smart buildings experienced at least one cybersecurity incident in 2023, disrupting systems and exposing operational risks. Furthermore, varying communication protocols and proprietary ecosystems hinder seamless integration between systems from different vendors. This fragmentation increases implementation complexity and costs while limiting scalability. Addressing these challenges requires standardized frameworks, secure communication layers, and continuous monitoring systems to protect data integrity and ensure system reliability across smart infrastructure.

The growing integration of AI and digital twin technologies offers substantial opportunities for the Smart Buildings Market. Digital twins enable real-time simulation of building performance, allowing proactive maintenance and energy optimization. Studies show that facilities using digital twins can achieve 20–25% improvement in operational efficiency and up to 15% reduction in maintenance costs. The convergence of AI-driven analytics with sensor-based data provides granular insights into energy flow, space utilization, and occupant behavior. These advancements create new business models, including predictive maintenance-as-a-service and adaptive workspace solutions. The opportunity landscape is expanding, with stakeholders focusing on creating self-learning, energy-efficient buildings aligned with sustainability and ESG goals.

The Smart Buildings Market faces challenges related to high initial investment and complex regulatory frameworks. Deploying IoT infrastructure, automation systems, and integrated analytics platforms requires substantial capital outlay, particularly for retrofitting existing buildings. Small and medium enterprises often struggle to justify upfront costs against long-term savings. Additionally, differing regional compliance standards—such as varying green certification requirements and energy codes—create administrative burdens for global developers. In 2024, implementation delays linked to regulatory clearances averaged 9–12 months, affecting project timelines. Overcoming these challenges demands scalable financing models, harmonized standards, and collaborative policy frameworks to ensure broader, faster adoption of smart building technologies worldwide.

• Rise in Modular and Prefabricated Construction: The adoption of modular and prefabricated construction is reshaping demand dynamics in the Smart Buildings Market. Nearly 55% of new smart infrastructure projects in 2024 integrated modular methods, resulting in up to 35% faster project completion and 20% lower material wastage compared to traditional techniques. Automated prefabrication of HVAC ducts, smart panels, and electrical units has also improved installation precision, with error margins reduced by 18%. Europe and North America are leading in this transformation, leveraging prefabricated components to accelerate smart building deployments with minimal on-site disruption.

• Expansion of AI and Machine Learning in Building Management: AI and ML technologies are increasingly driving intelligent automation and performance optimization in smart facilities. Over 62% of large-scale smart buildings implemented AI-driven management systems by 2024 to monitor energy, security, and occupancy in real time. Predictive algorithms have led to 28% improvement in system uptime and 22% energy savings, minimizing unplanned maintenance events. Continuous learning models are now capable of forecasting building usage patterns with over 90% accuracy, enabling adaptive lighting, ventilation, and temperature control based on human behavior and environmental data.

• Surge in Edge and Cloud Integration for Data Analytics: The integration of edge computing and cloud analytics has become a cornerstone of smart infrastructure modernization. Approximately 70% of newly commissioned smart buildings deploy hybrid architectures that process data locally and in the cloud. This model enables real-time decision-making latency under 10 milliseconds while enhancing network reliability by 33%. The combined approach facilitates efficient energy management and fault detection, improving operational transparency. Growing reliance on digital twins and data lakes further enhances predictive insights, empowering enterprises to optimize performance across entire building portfolios.

• Growing Focus on Sustainability and Net-Zero Compliance: Sustainability goals are shaping the evolution of the Smart Buildings Market, with 48% of corporate building owners setting carbon-neutral targets for 2030. Smart energy management systems have reduced electricity consumption by up to 30% through dynamic load balancing and renewable energy integration. Smart water management and waste recycling solutions have achieved 25% improvement in resource utilization across commercial spaces. Moreover, ESG-compliant smart infrastructure is being prioritized by institutional investors, with over USD 120 billion equivalent allocated globally to sustainable building transformation initiatives focused on decarbonization and environmental stewardship.

The Smart Buildings Market is segmented based on type, application, and end-user insights, reflecting a highly diversified ecosystem of technology and functionality integration. The segmentation highlights how building automation, energy management, and intelligent infrastructure systems converge to enhance operational efficiency. Smart building types vary from intelligent security systems to HVAC control, lighting automation, and facility management software. Application areas include commercial complexes, residential structures, industrial plants, and government facilities. End-user segmentation emphasizes adoption across sectors such as corporate offices, manufacturing units, and healthcare institutions. Each segment displays distinct growth patterns influenced by automation intensity, sustainability focus, and digital transformation readiness. Together, these segmentation dynamics reveal an evolving market shaped by the convergence of IoT, AI, and data analytics to achieve intelligent, sustainable, and adaptive infrastructure environments.

Building Management Systems (BMS) currently account for approximately 41% of adoption within the Smart Buildings Market, leading the segment due to their central role in integrating HVAC, lighting, security, and energy subsystems. This dominance is driven by the growing demand for centralized monitoring and predictive control. Energy Management Systems follow with a 28% share, supported by the global transition toward carbon-neutral infrastructure. However, the fastest-growing segment is Smart Security and Access Control Systems, projected to grow at a CAGR of 14.2%, fueled by the rise in connected surveillance and biometric authentication technologies. Intelligent Lighting Systems and Smart HVAC Controls collectively contribute 31% of the remaining segment share, finding increased adoption in large office spaces and industrial facilities due to automation-driven efficiency benefits.

Commercial applications currently dominate the Smart Buildings Market, accounting for approximately 48% of the total installations, as enterprises continue investing in technology-led building automation for cost efficiency and compliance. Residential applications represent about 27% of adoption, driven by growing consumer awareness of smart home ecosystems and increased affordability of connected devices. The fastest-growing application segment is Industrial, projected to expand at a CAGR of 13.8%, supported by IoT-based monitoring systems improving energy efficiency and predictive maintenance in manufacturing facilities. Educational and government buildings make up a combined 25% share, leveraging smart automation to optimize facility operations and improve sustainability credentials.

Corporate enterprises lead the Smart Buildings Market, accounting for about 44% of end-user adoption, driven by large-scale implementation of automation and sustainability programs in office spaces and business parks. The fastest-growing end-user segment is the Healthcare sector, expected to grow at a CAGR of 14.7%, as hospitals and clinics increasingly adopt smart systems for air quality control, energy optimization, and patient comfort. The Industrial and Retail sectors collectively contribute 33% of the remaining share, using connected infrastructure to enhance operational agility and customer experience. Educational institutions and government organizations account for 23%, focusing on smart campus models that align with ESG mandates.

North America accounted for the largest market share at 36% in 2024; however, Asia-Pacific is expected to register the fastest growth, expanding at a CAGR of 14.1% between 2025 and 2032.

Europe followed closely, contributing 29% of global deployment, while the Middle East & Africa and South America collectively represented around 10% and 8%, respectively. The rapid adoption of smart infrastructure technologies is strongly influenced by regional economic conditions, construction activity, and regulatory mandates promoting green and energy-efficient buildings. With over 320 million smart devices integrated across commercial buildings worldwide by 2024, regional disparities in technology integration are becoming evident—developed economies focus on sustainability compliance, whereas emerging economies emphasize large-scale automation and digital infrastructure development.

How are advanced automation and ESG policies reshaping the Smart Buildings ecosystem?

North America holds a dominant position with approximately 36% of the global Smart Buildings Market, supported by robust investments in intelligent commercial and industrial infrastructure. The United States and Canada are at the forefront of digital transformation, with strong regulatory backing through energy efficiency mandates and LEED certifications. Key industries driving demand include healthcare, finance, and information technology, all investing in AI-integrated facility management and predictive energy control systems. Local companies are also contributing; for instance, Johnson Controls expanded its OpenBlue platform to support advanced digital twins across corporate campuses. Consumer behavior reflects high enterprise adoption, particularly in corporate and healthcare segments, where over 64% of new buildings integrate smart automation technologies to enhance efficiency and occupant wellbeing.

Why is sustainability regulation accelerating innovation in Smart Building technologies?

Europe accounts for approximately 29% of the Smart Buildings Market, led by Germany, the UK, and France, where strong environmental policies and stringent energy performance directives drive innovation. Regulatory bodies have enforced sustainability standards requiring measurable reductions in carbon emissions and energy consumption. Smart HVAC systems, energy management software, and intelligent lighting solutions are increasingly adopted across urban centers. Companies such as Siemens AG and Schneider Electric have pioneered building automation platforms that align with EU’s decarbonization objectives. European consumers display preference for explainable, regulatory-compliant technologies, with over 58% of enterprises prioritizing data transparency and sustainability reporting as part of their smart infrastructure strategies.

How is rapid urbanization fueling next-generation Smart Building innovations?

Asia-Pacific ranks as the fastest-growing region in the Smart Buildings Market, accounting for around 27% of total installations in 2024, driven primarily by China, India, and Japan. Urban development programs and industrial automation have spurred demand for intelligent infrastructure and smart city integration. Technological hubs across Japan and South Korea are introducing AI-based HVAC and occupancy management systems. In China, several large-scale smart city projects have integrated over 50 million connected sensors to optimize traffic, lighting, and facility management. Consumer adoption is influenced by digital lifestyles and expanding e-commerce infrastructure, with a significant rise in mobile-based building control applications across residential and commercial sectors.

How are energy transitions and construction modernization shaping Smart Building deployment?

South America accounted for about 8% of the Smart Buildings Market in 2024, with Brazil and Argentina being the principal contributors. The region is witnessing increasing smart adoption in commercial real estate and industrial complexes, supported by renewable energy integration and modernization of construction practices. Governments are offering tax incentives for energy-efficient infrastructure, and several municipalities have launched urban sustainability initiatives. Local developers in Brazil have begun integrating IoT-based lighting and HVAC systems to achieve 15–20% reductions in electricity use. Regional consumers exhibit growing awareness of energy-efficient housing, with smart automation demand expanding across both high-rise apartments and public infrastructure projects.

How is construction diversification driving intelligent infrastructure investments?

The Middle East & Africa region accounted for roughly 10% of the Smart Buildings Market in 2024, driven by large-scale investments in commercial, hospitality, and mixed-use developments across the UAE, Saudi Arabia, and South Africa. Ongoing construction megaprojects, such as sustainable city initiatives and carbon-neutral complexes, are pushing adoption of smart HVAC and lighting control systems. Local governments are implementing green building codes to meet energy efficiency standards, while regional developers are integrating IoT platforms for real-time building analytics. Consumer behavior is increasingly shaped by luxury and sustainability trends, with over 40% of new commercial properties incorporating smart automation and building management systems to enhance occupant comfort and reduce emissions.

United States – 24% market share: Dominance supported by strong digital infrastructure, regulatory energy standards, and enterprise-level adoption across commercial buildings.

China – 18% market share: Driven by extensive smart city programs, large-scale manufacturing capabilities, and rapid implementation of IoT-based building automation technologies.

The Smart Buildings Market is characterized by a moderately consolidated structure, with the top five players collectively accounting for approximately 48% of global market activity. Over 120 active competitors operate globally, ranging from multinational conglomerates to specialized solution providers focused on automation, IoT, and energy efficiency technologies. The competitive dynamics are driven by innovation in building automation software, energy management systems, and cloud-based analytics platforms. Strategic partnerships and acquisitions are common—particularly among major vendors aiming to expand digital capabilities and regional footprints. For instance, multiple alliances formed in 2024 focused on integrating AI-driven predictive maintenance and cybersecurity protocols into smart building ecosystems. Emerging players are concentrating on niche innovations, such as edge computing and real-time occupant analytics, to differentiate from larger competitors. The market reflects an increasing shift toward interoperability and open architecture platforms, enabling seamless integration of HVAC, lighting, and security systems. Continuous R&D investments exceeding USD 12 billion annually underscore the sector’s innovation intensity, while ecosystem collaborations with telecom operators and cloud providers further intensify competition.

Honeywell International Inc.

ABB Ltd.

Cisco Systems Inc.

IBM Corporation

Hitachi Ltd.

Panasonic Holdings Corporation

Delta Electronics Inc.

Legrand SA

United Technologies Corporation

Lutron Electronics Co., Inc.

Emerson Electric Co.

BuildingIQ Pty Ltd.

Technological advancements in the Smart Buildings Market are reshaping operational efficiency, energy management, and occupant comfort. Building automation systems (BAS) have achieved nearly 68% integration across new commercial developments globally, enabling centralized control of HVAC, lighting, and security. IoT-enabled sensors are becoming core infrastructure, with over 2.5 billion devices currently deployed in smart facilities to monitor temperature, occupancy, and energy usage in real time. These systems generate actionable insights that help reduce energy consumption by up to 35% annually, directly contributing to sustainability goals and reduced operational costs.

Artificial Intelligence (AI) and Machine Learning (ML) technologies are emerging as the next transformative layer. Predictive analytics powered by AI algorithms now improve equipment maintenance cycles by 28% and cut downtime by nearly 20%. Edge computing is further accelerating responsiveness by processing data locally, a critical factor in high-traffic smart commercial spaces. Integration of 5G connectivity has enhanced communication speed and reliability by over 40%, facilitating real-time system coordination and advanced automation in multi-building complexes.

Digital twin technology is gaining momentum, with approximately 45% of large-scale infrastructure projects incorporating virtual modeling to simulate performance and optimize resource allocation. Meanwhile, cybersecurity protocols are strengthening—smart building networks with advanced encryption and intrusion detection saw a 32% drop in breach attempts in 2024. Collectively, these technologies are positioning smart buildings as self-learning, adaptive ecosystems that balance energy efficiency, comfort, and compliance in a data-driven urban environment.

In early 2023, Siemens AG introduced a suite of IoT-based smart building solutions at a major industry fair, enabling small and medium-sized buildings to integrate cloud platforms and environmental sensors, thereby improving indoor air quality monitoring and occupant comfort in retrofit applications.

In February 2024, Siemens entered a strategic partnership with Zumtobel Group and Enlighted, Inc. to bundle high-precision smart sensors and premium lighting fixtures into prefabricated IoT lighting systems that target commercial offices, higher-education campuses and smart hospitals worldwide.

On April 10, 2024, Johnson Controls International plc was named “Overall Leader for its Smart Building Management Platform” by an independent industry intelligence firm, following assessment of its OpenBlue ecosystem for implementation capability and comprehensive service-breadth across commercial building verticals.

In September 2024, Johnson Controls released an update of its Metasys 14.0 building automation system, designed to enhance occupant health, safety and sustainability by integrating advanced machine-learning controls, improved sensor analytics and expanded cloud connectivity across commercial portfolios. )

This Smart Buildings Market Report covers global and regional developments across multiple dimensions of infrastructure automation, intelligent controls, and digital ecosystem integration. It addresses segmentation by product type—such as building automation systems, energy management platforms, security/access control devices and lighting/IoT sensor networks—and by application across commercial, residential, industrial and public-sector buildings. Geographic scope spans North America, Europe, Asia-Pacific, South America and Middle East & Africa, offering comparative analysis of installation volumes, technology adoption rates and regional regulatory influences.

The report also details end-user industry verticals including corporate offices, healthcare, education, retail and manufacturing, and examines how each sector deploys smart building technologies in response to operational efficiency, occupant wellness and sustainability imperatives. On the technology front, the study explores traditional building management hardware, cloud and edge computing platforms, AI-driven analytics, digital twin modelling, wireless IoT sensor networks and integrated building-to-grid systems. Emerging market segments such as retrofit-enablement services for legacy buildings, bundled offerings for smart campuses, and service-based models (e.g., building-as-a-service) are also included.

For decision-makers, the report outlines competitive profiles, innovation trends, investment patterns and regulatory frameworks, enabling strategic insight into vendor positioning, partnership opportunities and technology road-maps.

| Report Attribute/Metric | Report Details |

|---|---|

Market Revenue in 2024 | USD 98863 Million |

Market Revenue in 2032 | USD 272270 Million |

CAGR (2025 - 2032) | 13.5% |

Base Year | 2024 |

Forecast Period | 2025 - 2032 |

Historic Period | 2020 - 2024 |

Segments Covered | By Types

By Application

By End-User

|

Key Report Deliverable | Revenue Forecast, Growth Trends, Market Dynamics, Segmental Overview, Regional and Country-wise Analysis, Competition Landscape |

Region Covered | North America, Europe, Asia-Pacific, South America, Middle East, Africa |

Key Players Analyzed | Johnson Controls International plc, Siemens AG, Schneider Electric SE, Honeywell International Inc., ABB Ltd., Cisco Systems Inc., IBM Corporation, Hitachi Ltd., Panasonic Holdings Corporation, Delta Electronics Inc., Legrand SA, United Technologies Corporation, Lutron Electronics Co., Inc., Emerson Electric Co., BuildingIQ Pty Ltd. |

Customization & Pricing | Available on Request (10% Customization is Free) |