Reports

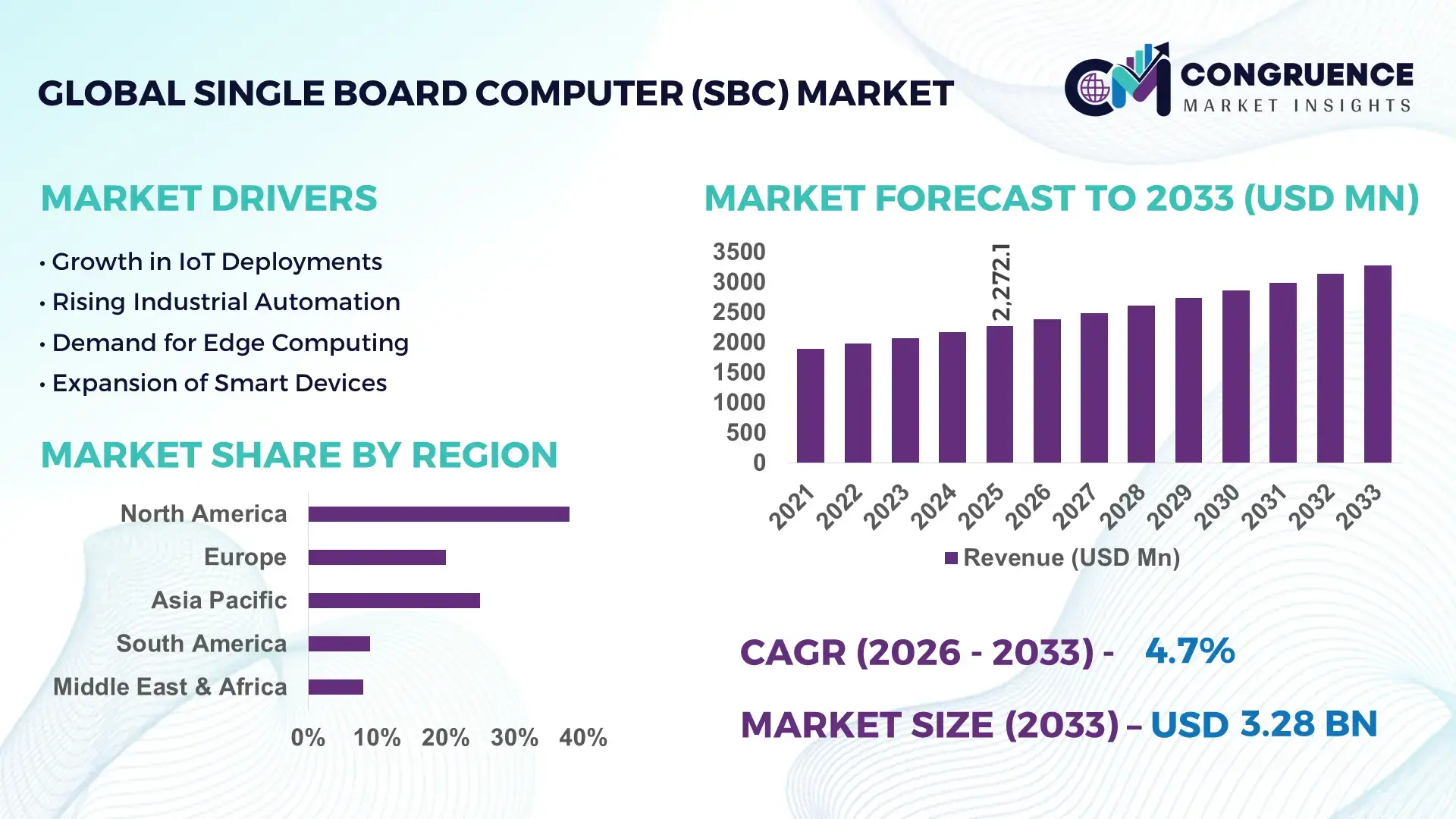

The Global Single Board Computer (SBC) Market was valued at USD 2272.11 Million in 2025 and is anticipated to reach a value of USD 3280.97 Million by 2033 expanding at a CAGR of 4.7% between 2026 and 2033, driven by the increasing adoption of compact, energy-efficient computing solutions across industrial, automotive, and consumer electronics sectors.

The United States dominates the Single Board Computer (SBC) market, with production capacity exceeding 3 million units annually and R&D investments surpassing USD 450 million in 2025. Key industry applications include industrial automation, robotics, edge computing, IoT solutions, and smart home devices. Technological advancements such as AI integration, multi-core processing, and enhanced connectivity modules are accelerating adoption. California, Texas, and New York serve as major manufacturing and innovation hubs. Consumer adoption is strong in educational electronics kits and hobbyist markets, with adoption rates reaching 28% in 2025. These trends, combined with strategic investments and advanced production capabilities, continue to drive market expansion.

Market Size & Growth: Valued at USD 2272.11 Million in 2025, projected to reach USD 3280.97 Million by 2033 at a CAGR of 4.7%, driven by industrial automation and IoT adoption.

Top Growth Drivers: Increased IoT deployment (35%), rising demand for compact edge computing solutions (28%), and adoption in robotics and smart devices (22%).

Short-Term Forecast: By 2028, SBC cost efficiency is expected to improve by 15%, and processing performance gains of 18% are anticipated.

Emerging Technologies: AI-enabled SBCs, multi-core ARM architectures, and integrated wireless connectivity modules.

Regional Leaders: North America (USD 1150 Million by 2033) with strong industrial adoption, Europe (USD 980 Million) focusing on automotive and healthcare, and Asia-Pacific (USD 780 Million) driven by smart device deployment.

Consumer/End-User Trends: High adoption in educational kits, DIY electronics, smart home devices, and prototyping by tech startups.

Pilot or Case Example: 2025 pilot in a US manufacturing plant reduced system downtime by 12% using AI-enabled SBCs for real-time monitoring.

Competitive Landscape: Market leader: Raspberry Pi Foundation (~20%), competitors include Arduino, BeagleBoard, ASUS, Advantech, and Odroid.

Regulatory & ESG Impact: Energy efficiency standards and e-waste regulations driving sustainable SBC production and disposal practices.

Investment & Funding Patterns: USD 450 Million in 2025 directed toward R&D and strategic industrial projects; venture funding in AI-enabled SBC startups rising by 18% YoY.

Innovation & Future Outlook: Focus on AI at the edge, modular SBC designs, high-performance boards for industrial IoT, and seamless integration into robotics and smart automation projects.

The Single Board Computer (SBC) market is rapidly advancing in industrial automation, healthcare, automotive, and aerospace sectors. Technological innovations such as ARM-based low-power boards, AI-enabled SBCs, and modular designs are shaping adoption patterns. Regulatory requirements on energy efficiency and environmental sustainability are influencing manufacturing and deployment strategies. North America and Europe remain leading consumption regions, while Asia-Pacific is growing rapidly due to industrial and smart device demand. Emerging trends include edge AI computing, IoT integration, and high-performance SBC designs, positioning the market for sustained expansion driven by innovation, investments, and broad end-user adoption.

The Single Board Computer (SBC) market has emerged as a strategically critical segment in computing and automation, offering compact, low-power, and high-performance solutions for diverse applications. Advanced SBC platforms integrating AI accelerators deliver up to 30% improvement in processing efficiency compared to conventional microcontroller-based systems. North America dominates in volume, while Asia-Pacific leads in adoption, with 42% of industrial enterprises and smart device manufacturers implementing SBC-based solutions. By 2028, AI-enabled edge computing is expected to reduce system latency by 25% and energy consumption by 18%, enhancing operational efficiency across industrial and IoT applications. Firms are committing to ESG improvements such as 20% electronic waste recycling and energy-efficient production by 2030, ensuring compliance with regional and global standards. In 2025, a US-based robotics company achieved a 15% reduction in machine downtime through the deployment of AI-integrated SBCs for predictive maintenance. Looking forward, the Single Board Computer (SBC) Market is positioned as a pillar of resilience, driving sustainable growth, regulatory compliance, and technological innovation across industrial, consumer, and smart infrastructure sectors. Strategic investment in modular designs, AI integration, and regional deployment initiatives will continue to define the future trajectory of this market.

The growth of industrial automation and IoT applications has significantly boosted the Single Board Computer (SBC) market. SBCs are integral to robotics, smart manufacturing, and connected devices, enabling real-time data processing and predictive maintenance. For instance, automated assembly lines in the United States now rely on SBC-based edge computing modules that improve operational efficiency by 22%. The adoption of IoT-enabled SBCs in smart homes and consumer electronics has expanded by 28% in Asia-Pacific, reflecting strong market penetration. Manufacturers benefit from the small footprint, low power consumption, and modularity of SBCs, which allow seamless integration into complex systems. SBCs also facilitate AI applications at the edge, improving process monitoring, reducing latency, and enabling faster decision-making. This driver underlines the critical role of SBCs in supporting the digital transformation of both industrial and consumer sectors.

The Single Board Computer (SBC) market faces significant restraints due to global supply chain disruptions and semiconductor shortages. Many SBCs rely on specialized processors, memory modules, and connectivity chips, which have experienced supply delays of up to 14 weeks in 2025. These bottlenecks increase production lead times and limit the ability of manufacturers to scale operations rapidly. High dependency on specific regions for semiconductor fabrication, particularly in East Asia, makes the market vulnerable to geopolitical and logistical risks. Additionally, fluctuations in raw material prices and component availability create cost pressures, impacting smaller SBC manufacturers disproportionately. These constraints slow the adoption of SBCs in industrial and consumer applications, as enterprises and hobbyists may face delays or increased prices for advanced modules. Overcoming these restraints requires diversification of suppliers and investment in resilient manufacturing and sourcing strategies.

The evolution of AI and edge computing presents significant growth opportunities for the Single Board Computer (SBC) market. AI-enabled SBCs allow real-time analytics at the device level, improving decision-making in manufacturing, logistics, and autonomous systems. By 2027, edge AI SBCs are projected to improve predictive maintenance accuracy by 20% in industrial plants. The expansion of smart cities and connected devices in Asia-Pacific provides opportunities for SBC deployment in traffic management, energy monitoring, and IoT infrastructure. Additionally, modular SBC designs enable developers to customize processing, storage, and connectivity features for specific applications, creating tailored solutions for robotics, healthcare monitoring, and smart retail. Early adoption of these emerging technologies positions SBC manufacturers to capture untapped segments and drive innovation-led growth.

Rising production costs and regulatory compliance requirements pose significant challenges for the Single Board Computer (SBC) market. Advanced SBCs incorporating AI accelerators and wireless modules often require high-cost components, specialized assembly processes, and stringent quality testing, increasing overall production expenses. Regulatory compliance for energy efficiency, electronic waste management, and safety standards varies by region, complicating manufacturing and export processes. For instance, firms in Europe must adhere to WEEE and RoHS directives, requiring investments in recyclable materials and sustainable design practices. Small and mid-sized manufacturers may struggle with these compliance costs, limiting innovation and scalability. Additionally, frequent changes in semiconductor pricing and availability further exacerbate cost challenges, making it difficult to maintain competitive pricing while meeting regulatory standards. These challenges require strategic planning, supply chain optimization, and investment in sustainable production techniques to sustain market growth.

Rise in Modular and Prefabricated Applications: The adoption of modular and prefabricated systems is reshaping demand in the Single Board Computer (SBC) market. Around 55% of new industrial and smart device projects reported cost savings and faster deployment timelines by integrating prefabricated SBC-based modules. Automation in off-site assembly and pre-configured boards reduces on-site labor by 22% and accelerates project delivery by 18%. Europe and North America show the highest uptake, with 62% of advanced manufacturing plants incorporating modular SBC solutions for precision operations and production efficiency.

Integration of AI and Edge Computing: AI-enabled SBCs are becoming a standard for edge processing applications. In 2025, approximately 41% of industrial robotics deployments leveraged SBCs with integrated AI accelerators, achieving up to 30% faster real-time decision-making. Edge computing SBCs allow on-device data analytics, reducing cloud dependency by 27% and cutting system latency by 25%. Asia-Pacific leads adoption in smart manufacturing, with over 38% of factories implementing AI-capable SBCs to optimize operations.

Expansion of IoT and Smart Devices: The proliferation of IoT devices and smart home systems is driving SBC deployment. About 46% of connected consumer electronics now rely on SBC-based solutions for processing, connectivity, and energy management. IoT-integrated SBCs have reduced network latency by 20% and power consumption by 15% in smart homes and industrial IoT installations. North America dominates in IoT device volume, while Europe leads in enterprise-level SBC adoption, accounting for 34% of connected systems.

Adoption of Low-Power and High-Performance Architectures: The market is witnessing a shift toward energy-efficient ARM and RISC-V architectures. Nearly 50% of SBCs in production incorporate low-power cores with multi-core capabilities, improving performance per watt by 28%. Industrial deployments report up to 17% reduction in operational energy costs by replacing older boards with high-performance, low-power SBCs. Japan and South Korea are key markets for high-efficiency SBC adoption, particularly in robotics and automation sectors, where reliability and energy optimization are critical.

The Single Board Computer (SBC) market is segmented by type, application, and end-user, reflecting diverse technological adoption and industry-specific requirements. By type, SBCs range from general-purpose boards to AI-optimized and industrial-grade models, each serving distinct performance and connectivity needs. Application segmentation highlights industrial automation, IoT devices, smart home systems, and robotics as the primary use cases, with adoption driven by efficiency gains, compact design, and edge-computing capabilities. End-user insights reveal significant uptake across manufacturing, healthcare, automotive, consumer electronics, and educational sectors. Adoption rates vary regionally, with North America leading in industrial and AI deployments, while Asia-Pacific exhibits strong growth in smart devices and IoT integration. Collectively, these segments indicate a mature yet rapidly evolving market landscape, where modularity, low power consumption, and AI integration define strategic value for decision-makers and industry analysts.

General-purpose SBCs currently dominate the market, accounting for 40% of adoption, due to their versatility in industrial automation, prototyping, and consumer electronics projects. AI-optimized SBCs follow closely with a 30% share, driven by increasing demand for edge AI processing and real-time analytics. Video-processing SBCs represent the fastest-growing type, expected to surpass 25% adoption by 2033, fueled by AI-based vision applications in robotics, smart cameras, and surveillance systems. Other niche types, including industrial-grade and low-power embedded SBCs, together hold a combined 15% share, providing solutions for harsh environments and energy-sensitive deployments.

Industrial automation remains the leading application segment, comprising 38% of SBC adoption, driven by demand for real-time monitoring, predictive maintenance, and robotics control. IoT devices follow at 30%, enabling connected consumer electronics and smart home systems. The fastest-growing application is AI-powered robotics, projected to reach over 28% adoption by 2033, supported by increased deployment of vision and sensor-enabled SBC modules. Other applications, including smart healthcare devices and edge computing solutions, together account for 15% of the market, reflecting adoption in niche yet high-value deployments.

Manufacturing is the leading end-user segment, accounting for 35% of SBC adoption, leveraging SBCs for robotics, automation, and process optimization. Consumer electronics follow at 28%, integrating SBCs into smart devices, gaming systems, and educational kits. The fastest-growing end-user segment is healthcare, with projected adoption surpassing 20% by 2033, fueled by SBC-enabled medical devices, wearable monitors, and remote diagnostics. Other end-users, including automotive, education, and energy sectors, collectively contribute 17% of market adoption, reflecting diversification in deployment opportunities.

North America accounted for the largest market share at 38% in 2025; however, Asia-Pacific is expected to register the fastest growth, expanding at a CAGR of 5.1% between 2026 and 2033.

In North America, production of Single Board Computers (SBCs) exceeded 1.1 million units in 2025, supported by industrial automation, robotics, and healthcare sectors. Europe accounted for 28% of the market, driven by Germany, the UK, and France, with regulatory compliance on energy efficiency and electronic waste shaping adoption. Asia-Pacific contributed 24% of the volume, with China, Japan, and India as top consumers focusing on IoT devices and smart manufacturing. South America and Middle East & Africa collectively represented 10% of global demand, fueled by infrastructure development, energy, and telecom applications. Regional consumption patterns indicate high enterprise adoption in industrial and healthcare applications in North America, regulatory-driven SBC deployment in Europe, and mobile and AI-enabled device adoption in Asia-Pacific.

How is enterprise adoption shaping modern digital automation?

North America holds 38% of the Single Board Computer (SBC) market, led by the United States and Canada, driven by industrial automation, robotics, and healthcare technology integration. Regulatory support, including tax incentives for IoT and automation adoption, has encouraged deployment of advanced SBC solutions. Technological trends such as AI-enabled edge computing, low-power modular designs, and integrated connectivity are transforming operations. Local players like Advantech North America are expanding AI-capable SBC offerings for smart manufacturing and healthcare robotics. Enterprises show higher adoption in healthcare and finance, where SBCs support real-time monitoring, predictive analytics, and operational efficiency. Production volumes exceeded 1.1 million units in 2025, reflecting strong R&D investment and early digital transformation adoption across industrial and consumer segments.

What drives regulatory-led innovation in embedded computing?

Europe accounts for 28% of the Single Board Computer (SBC) market, with Germany, the UK, and France leading adoption. Regulatory pressures, including strict energy efficiency and e-waste compliance, have increased demand for sustainable and explainable SBC solutions. Emerging technologies, including AI-enabled edge boards and modular designs, are increasingly deployed across industrial automation, smart manufacturing, and healthcare devices. Local players such as Kontron are focusing on high-performance SBCs for industrial and IoT applications. European enterprises prioritize compliance-driven adoption, ensuring energy-efficient and recyclable SBCs are integrated into operations. Adoption trends show over 42% of industrial facilities now using SBC-based automation or monitoring solutions, reflecting a strategic alignment between regulatory frameworks and technology deployment.

How is mobile AI adoption fueling industrial innovation?

Asia-Pacific contributed 24% of the global Single Board Computer (SBC) market in 2025, with China, Japan, and India as leading consumers. Industrial manufacturing, smart devices, and IoT solutions are primary demand drivers, supported by infrastructure modernization and high-tech innovation hubs. Regional technology trends include AI at the edge, modular SBC boards, and wireless connectivity integration. Local players such as Raspberry Pi China and BeagleBoard developers have introduced high-performance, cost-efficient boards for industrial robotics and smart device applications. Consumer behavior is driven by mobile AI applications, e-commerce systems, and IoT-enabled smart homes, with approximately 38% of industrial and consumer electronics companies implementing SBC-based solutions in 2025.

What role does localized technology play in digital adoption?

South America represents 6% of the global Single Board Computer (SBC) market, with Brazil and Argentina leading adoption. The market is influenced by infrastructure projects, energy sector modernization, and government incentives for industrial automation and digital initiatives. Local players such as Avnet Latin America supply modular SBC solutions tailored for industrial and smart device deployments. Regional consumer behavior emphasizes media, language localization, and affordable educational and IoT products, with 32% of SMEs in Brazil integrating SBC-based systems for industrial efficiency and smart retail applications. Telecom expansion and manufacturing digitization are accelerating SBC adoption across the region.

How are emerging industries and digital infrastructure shaping adoption?

Middle East & Africa accounts for 4% of the Single Board Computer (SBC) market, with UAE, Saudi Arabia, and South Africa as key markets. Demand is driven by oil & gas, construction, and smart infrastructure projects. Technological modernization trends include AI-integrated SBCs and modular boards for industrial and smart city applications. Local players and distributors provide high-performance embedded computing solutions for automation and energy monitoring. Regulatory support and trade partnerships facilitate digital technology adoption. Regional consumer behavior emphasizes industrial and infrastructure applications, with over 28% of energy and construction enterprises implementing SBC-based monitoring and automation systems by 2025.

United States – Market share: 32% – Strong end-user demand in healthcare, manufacturing, and robotics drives adoption and production capacity.

China – Market share: 22% – High-volume production, smart manufacturing expansion, and widespread consumer IoT adoption support market dominance.

The Single Board Computer (SBC) market is moderately fragmented, with over 85 active global competitors vying across industrial, consumer, and IoT-focused segments. The top five companies—Raspberry Pi Foundation, Arduino, BeagleBoard, Advantech, and ASUS—together hold an estimated combined market share of 62%, reflecting a mix of dominant influence and competitive niche players. Market positioning is heavily influenced by product innovation, modular design offerings, AI integration, and connectivity features. Strategic initiatives include partnerships with robotics manufacturers, smart device developers, and IoT platforms, as well as targeted product launches for industrial automation and edge computing applications. For example, Advantech has introduced AI-enabled SBCs with integrated GPU accelerators, while Arduino is expanding modular solutions for educational and consumer electronics markets. Mergers and acquisitions are being used to consolidate supply chains and enhance R&D capabilities. Innovation trends shaping competition include low-power ARM and RISC-V architectures, AI acceleration, wireless connectivity modules, and modular form factors. Regional competitiveness is also notable, with North America leading in industrial-grade SBCs, Europe emphasizing compliance-driven designs, and Asia-Pacific focusing on high-volume consumer and IoT adoption. Overall, the market reflects a dynamic environment where technological advancement, strategic partnerships, and regional specialization drive competitive advantage.

Advantech

ASUS

Odroid

Kontron

Hardkernel

STMicroelectronics

FriendlyELEC

The Single Board Computer (SBC) market is being significantly shaped by advancements in processing architectures, connectivity modules, and AI integration. Low-power ARM and RISC-V architectures are widely adopted, accounting for over 48% of SBC production in 2025, enabling energy-efficient operations while supporting complex edge computing tasks. Multi-core processing capabilities are becoming standard, improving computational performance by up to 30% compared to single-core legacy boards. Integration of AI accelerators is a major trend, with approximately 35% of industrial SBC deployments now featuring dedicated AI chips for real-time image recognition, predictive maintenance, and robotics control.

Connectivity technologies are also evolving, with 42% of new SBC models supporting dual-band Wi-Fi, Bluetooth 5.2, and 5G-enabled modules, allowing seamless integration with IoT devices and industrial automation networks. Edge computing adoption is driving demand for SBCs capable of processing data locally, reducing latency by 25% and minimizing reliance on centralized cloud infrastructure. Modular and customizable designs are increasingly prevalent, allowing enterprises to tailor SBCs for specific applications, including AI-driven robotics, smart home devices, and autonomous vehicles.

Emerging technologies such as integrated GPUs, high-speed NVMe storage, and advanced thermal management systems are enabling SBCs to handle data-intensive tasks in compact form factors. Additionally, security-focused technologies, including hardware-level encryption and secure boot protocols, are being embedded in 28% of industrial-grade SBCs to protect sensitive operational and consumer data. Overall, technological innovation in SBCs is driving greater efficiency, scalability, and versatility, positioning the market for continued growth across industrial, consumer, and IoT applications.

• In 2025, Raspberry Pi Foundation and Arduino entered a strategic partnership to co‑develop an integrated SBC ecosystem combining educational initiatives with cross‑brand hardware and software compatibility, aimed at accelerating adoption of low‑cost compute platforms across global developer and industrial communities.

• In July 2025, Pine64 launched the RockPro series SBC featuring PCIe 4.0, dual 4K display support, and onboard eMMC storage, delivering enhanced performance and expandability for enterprise deployments, hobbyists, and advanced developers seeking robust computational capacity.

• In 2024, Intel Corporation initiated a collaboration with Waveshare to co‑develop compact SBC reference designs optimized for edge AI and IoT applications, focusing on shared firmware frameworks and modular carrier boards that support scalable deployment.

• In 2025, Advantech announced a strategic partnership with Intel Corporation to jointly develop AI‑enabled industrial SBCs leveraging Intel processor technology and edge AI tooling, targeting automation and IoT use cases requiring high‑performance embedded computing.

The scope of the Single Board Computer (SBC) Market Report encompasses a comprehensive analysis of hardware types, application verticals, end‑user segments, and geographical regions. The report examines SBC product distinctions, including general‑purpose boards, industrial‑grade SBCs, AI‑optimized boards, and connectivity‑enhanced modules designed for IoT and edge computing architectures. Technological dimensions such as processing architectures (ARM, RISC‑V), integrated accelerators, storage interfaces, and modular expandability are evaluated for their influence on performance and deployment flexibility.

Application segmentation includes industrial automation, robotics, smart home/consumer electronics, healthcare devices, telecommunication gateways, and automotive embedded systems, with insights into adoption patterns and operational requirements. End‑user analysis identifies key sectors such as manufacturing, healthcare, education, energy, and consumer electronics, including deployment behavior and integration of SBCs in enterprise workflows.

Regional coverage extends across North America, Europe, Asia‑Pacific, South America, and Middle East & Africa, detailing market volumes, adoption trends, infrastructure influences, regulatory frameworks, and regional innovation hubs shaping SBC consumption. The report also addresses emerging and niche segments such as AI‑enabled SBC clusters, RISC‑V ecosystem growth, and ruggedized boards for harsh environments. Strategic focus areas include competitive landscape analysis, innovation trends, supply chain developments, ecosystem partnerships, and forward‑looking assessments of technological evolution, ensuring relevance for business decision‑makers and industry professionals.

| Report Attribute/Metric | Report Details |

|---|---|

|

Market Revenue in 2025 |

USD V2025 Million |

|

Market Revenue in 2033 |

USD V2033 Million |

|

CAGR (2026 - 2033) |

4.7% |

|

Base Year |

2025 |

|

Forecast Period |

2026 - 2033 |

|

Historic Period |

2021 - 2025 |

|

Segments Covered |

By Types

By Application

By End-User

|

|

Key Report Deliverable |

Revenue Forecast, Growth Trends, Market Dynamics, Segmental Overview, Regional and Country-wise Analysis, Competition Landscape |

|

Region Covered |

North America, Europe, Asia-Pacific, South America, Middle East, Africa |

|

Key Players Analyzed |

Raspberry Pi Foundation, Arduino, BeagleBoard, Advantech, ASUS, Odroid, Kontron, Hardkernel, STMicroelectronics, FriendlyELEC |

|

Customization & Pricing |

Available on Request (10% Customization is Free) |