Reports

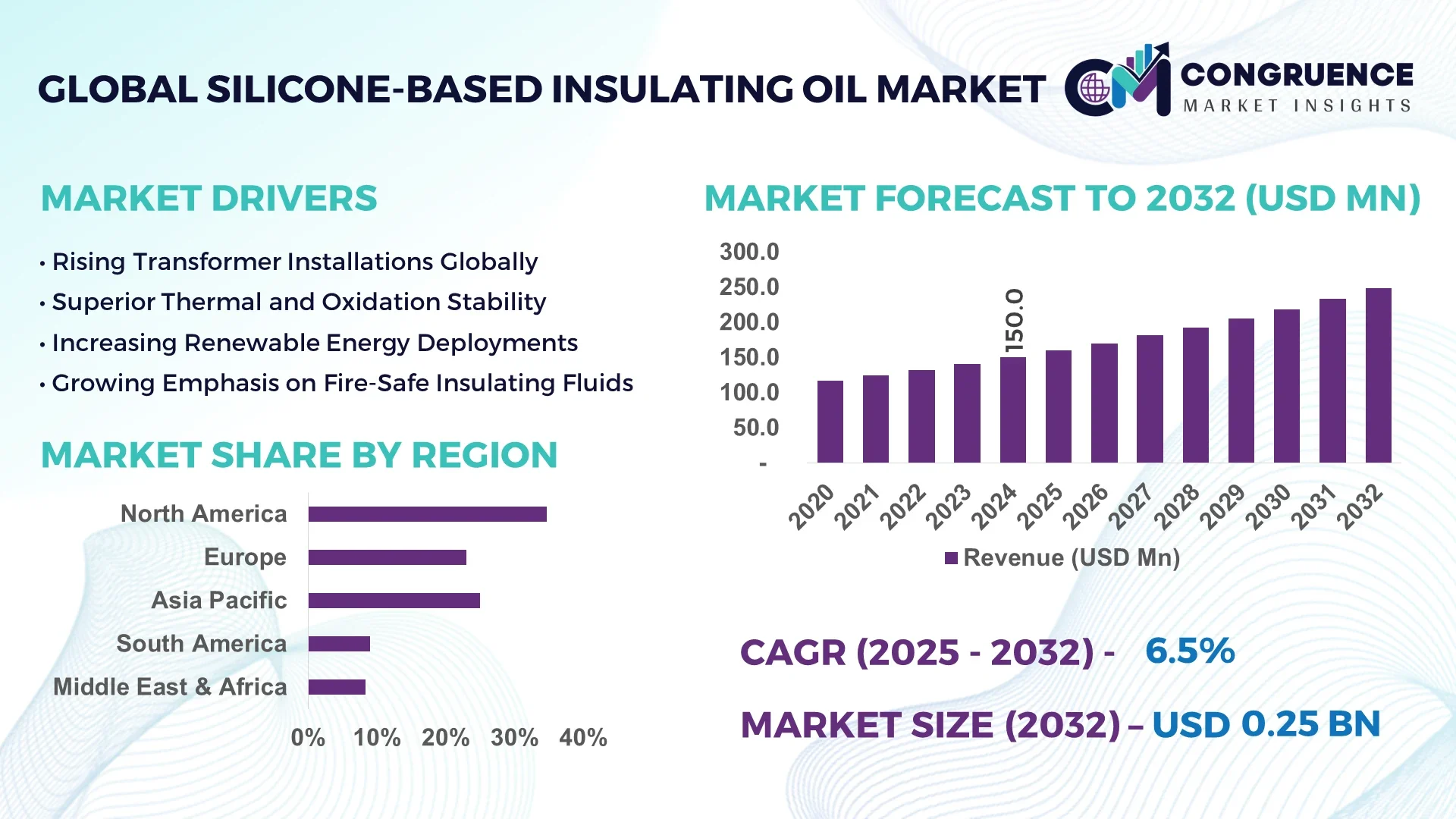

The Global Silicone-based Insulating Oil Market was valued at USD 150.0 Million in 2024 and is anticipated to reach a value of USD 248.2 Million by 2032 expanding at a CAGR of 6.5% between 2025 and 2032.

The United States leads the global silicone-based insulating oil market due to its robust infrastructure for power transmission and distribution, high adoption of smart grid technologies, and increasing refurbishment of aging transformers. The growing emphasis on fire-safe and environmentally friendly transformer fluids also contributes to the rising demand for silicone-based insulating oils across industrial and utility sectors in the country.

Silicone-based insulating oils are gaining traction owing to their excellent thermal stability, oxidation resistance, and superior dielectric properties. These fluids are ideal for high-voltage and high-temperature applications, especially in harsh environments where traditional mineral oils fail. As governments and utilities worldwide move towards more reliable and long-lasting power infrastructure, the demand for silicone-based insulating oils is witnessing consistent growth. The increasing focus on grid modernization, integration of renewable energy systems, and the need for eco-friendly alternatives in transformer applications further drive the market's expansion.

Artificial intelligence is playing a transformative role in the silicone-based insulating oil market, particularly by optimizing asset management and predictive maintenance in power systems. With the integration of AI and machine learning algorithms into transformer monitoring systems, utility providers can now assess the real-time performance and aging of insulating fluids. This significantly reduces the risk of unplanned downtimes and failures, enabling cost-effective maintenance schedules and extending the operational lifespan of power transformers.

Advanced analytics tools powered by AI are also facilitating better quality control during the manufacturing of silicone-based insulating oils. These systems ensure the consistency of chemical formulations and predict potential performance issues before the product reaches the market. Additionally, AI-driven material science is being employed to simulate and design improved formulations that offer enhanced oxidation stability and longer service life, making these oils more reliable for extreme environments.

AI is further contributing to sustainability by enabling data-driven insights into fluid degradation and recycling options. By analyzing sensor data, AI systems can determine the remaining useful life of the insulating oil, guiding decisions on when to recycle or replace the fluid, thus reducing environmental waste.

"In March 2024, a leading U.S.-based utility company deployed an AI-based transformer health monitoring system that uses infrared sensors and real-time analytics to evaluate the performance of silicone-based insulating oils under high-load conditions. The system reportedly reduced fluid-related transformer failures by 28% within the first six months of deployment, leading to significant improvements in grid reliability and maintenance planning."

The increasing emphasis on fire safety standards and environmental regulations has accelerated the demand for fire-resistant transformer fluids, particularly silicone-based insulating oils. These fluids have a much higher fire point than traditional mineral oils, making them ideal for use in densely populated areas, underground substations, and other high-risk environments. Their superior dielectric properties and non-toxicity further support their usage in critical infrastructure where safety is a paramount concern. Utility providers and industrial players are increasingly opting for these oils to meet compliance requirements and enhance the operational safety of their electrical assets.

Despite their superior properties, silicone-based insulating oils face adoption barriers due to their relatively high cost compared to mineral-based transformer oils. The initial investment required for purchasing and retrofitting equipment to handle silicone fluids can be substantial, especially for small- and medium-scale power utilities. This cost sensitivity is particularly evident in developing regions where budget constraints often dictate equipment procurement decisions. Additionally, limited awareness and lack of local manufacturing infrastructure further restrict the accessibility and scalability of these advanced fluids in price-sensitive markets.

Governments and energy providers across the globe are investing heavily in upgrading aging power infrastructure and integrating renewable energy sources. This shift toward modern, resilient, and efficient grids presents a significant opportunity for silicone-based insulating oil manufacturers. These oils are increasingly being specified for use in new-generation transformers and switchgear that require superior thermal and dielectric performance. With the growing deployment of high-voltage substations and offshore wind installations, the demand for high-performance insulating fluids is expected to surge, providing lucrative prospects for manufacturers in this segment.

One of the major challenges facing the silicone-based insulating oil market is the limited compatibility with existing transformer systems designed for mineral oil. Silicone fluids typically require specialized gaskets, seals, and equipment modifications to ensure safe and efficient operation. Additionally, retrofilling old transformers with silicone oil is a complex and costly process that involves thorough cleaning and system adjustments. This not only increases the operational downtime but also adds to the total cost of ownership, making it a less attractive option for utilities looking for straightforward upgrades.

Rise in Grid Resiliency Projects: Governments and utilities are actively pursuing projects to increase the resiliency and reliability of power grids. Silicone-based insulating oils are being increasingly adopted in critical substations and backup systems where long fluid life and minimal maintenance are essential. These oils perform well under temperature extremes, making them suitable for such applications.

Adoption in Renewable Energy Integration: The rise of renewable energy installations, such as offshore wind farms and solar parks, is driving the demand for durable and thermally stable insulating fluids. Silicone-based oils, with their superior dielectric strength and resistance to moisture and oxidation, are preferred in environments where renewable integration places a heavy load on grid assets.

Increased Use in Underground and Enclosed Substations: Urban expansion has led to the proliferation of underground substations that require non-flammable, non-toxic fluids. Silicone-based insulating oils meet these requirements, contributing to their rising popularity in metro cities and high-density areas across Asia and Europe.

Technological Innovations in Fluid Formulation: Manufacturers are investing in R&D to develop silicone insulating oils with enhanced viscosity, thermal conductivity, and bio-degradability. These advancements aim to offer better environmental performance and operational efficiency, aligning with global sustainability goals and regulatory mandates for eco-friendly transformer solutions.

The silicone-based insulating oil market is segmented based on type, application, and end-user. Each of these segments plays a crucial role in shaping the overall demand dynamics and market penetration strategies. Product types differ primarily in composition and viscosity characteristics, while applications are tailored across various equipment types such as transformers, capacitors, and switchgear. End-user analysis includes power utilities, industrial sectors, and commercial infrastructure, each exhibiting distinct purchasing behavior and specification requirements. Understanding these segments helps identify growth opportunities and streamline product development to meet targeted demand.

Silicone-based insulating oils are available in different types including high-viscosity silicone fluids, low-viscosity silicone fluids, and specialty modified silicones. Among these, high-viscosity silicone fluids dominate the market due to their robust dielectric strength and thermal stability, making them ideal for large-scale power transformers and high-voltage applications. However, the fastest-growing segment is low-viscosity silicone fluids, primarily driven by the need for more efficient heat dissipation and improved energy performance in compact and enclosed systems. Low-viscosity variants also offer better compatibility with automated filling systems, which is gaining traction in modern equipment manufacturing facilities. As equipment designers move toward lighter and more compact systems, the demand for these fluid types continues to rise.

The primary applications of silicone-based insulating oil include power transformers, distribution transformers, switchgear, and capacitors. Power transformers remain the leading application segment due to their critical role in high-load transmission systems and substation reliability. The consistent demand from utility-scale transmission infrastructure projects sustains the growth of this segment. On the other hand, switchgear applications are witnessing the fastest growth, particularly in urban areas where compact, enclosed, and safe systems are essential. The excellent fire-retardant and dielectric properties of silicone oils make them suitable for use in such equipment. Capacitor applications are growing modestly but are expected to expand with the development of high-performance, long-life power storage systems.

Key end-users of silicone-based insulating oils include utilities, industrial plants, commercial buildings, and renewable energy installations. Utilities are the dominant end-user group, driven by the continuous upgrades of aging infrastructure and the deployment of grid automation technologies. The industrial segment, encompassing manufacturing and processing facilities, is showing rapid growth as companies seek reliable and safe insulating fluids to minimize equipment downtime. The fastest-growing end-user segment is renewable energy installations, particularly offshore wind and solar energy systems that operate in extreme and variable environments. These installations require fluids that can withstand high moisture levels and temperature fluctuations, where silicone-based insulating oils outperform conventional alternatives.

North America accounted for the largest market share at 34.7% in 2024; however, Asia-Pacific is expected to register the fastest growth, expanding at a CAGR of 8.2% between 2025 and 2032.

The North American market has been driven by robust investments in energy infrastructure and modernization of utility-grade transformers. Meanwhile, Asia-Pacific is rapidly expanding due to increasing demand for reliable and high-temperature electrical insulation solutions in countries like China, India, and South Korea, supported by fast-paced industrialization and renewable energy deployment.

Surging Grid Modernization and Utility Transformer Replacement

North America's dominance in the silicone-based insulating oil market stems from widespread grid modernization projects across the United States and Canada. In 2024, utilities in the region deployed silicone-based insulating oil in over 30% of new high-voltage transformer installations due to its superior thermal stability and low flammability. Replacement of aging transformers in the U.S. alone surpassed USD 5 billion in investment during the year, a sizable portion of which involved silicone-insulated systems to meet fire safety codes in urban settings. Additionally, Canadian hydroelectric infrastructure upgrades have increased silicone fluid usage in large-scale power units.

Growing Emphasis on Environmental Safety and Renewable Integration

Europe remains a critical player in the global silicone-based insulating oil market due to stringent environmental regulations and growing adoption of renewable energy infrastructure. In 2024, over 42% of all newly commissioned offshore wind substations across Germany and the Netherlands adopted silicone oils to mitigate fire risks and ensure higher dielectric reliability under harsh marine conditions. The region’s transition to green energy has propelled the deployment of dry-type and silicone-filled transformers, especially in France, Italy, and Nordic countries. EU-based OEMs are also increasing the integration of biodegradable and low-emission insulating oils in compliance with REACH and RoHS standards.

Infrastructure Boom and Industrial Electrification Surge Demand

The Asia-Pacific region is witnessing the fastest growth driven by rising electricity consumption and infrastructure development across China, India, and Southeast Asia. In 2024, China installed over 12,000 units of silicone-based insulating oil-filled distribution transformers in densely populated cities where fire safety and compact design are critical. India’s rural electrification programs added over 50,000 kilometers of new transmission lines, much of which employed silicone oil-insulated switchgear and transformers in hot-climate zones. Japan and South Korea, with their aging grid systems, are also replacing conventional oils with silicone-based alternatives to comply with stricter fire prevention standards.

Hydropower Modernization and Urban Grid Reliability Push

In South America, Brazil and Argentina lead the silicone-based insulating oil market. In 2024, Brazil alone accounted for 65% of new insulating oil consumption in the region, mainly for hydropower transformer upgrades in states like São Paulo and Paraná. The region is focusing on urban grid reliability, with cities like Buenos Aires adopting silicone-based insulation in high-rise transformer substations due to its low volatility and thermal endurance. Ongoing privatization of electric utilities in countries like Chile is also expanding the use of silicone-based oils in modern substations and smart grid components.

Harsh Climate Applications Driving Silicone Oil Preference

In the Middle East & Africa, extreme environmental conditions are fostering the adoption of silicone-based insulating oils in electrical components. In 2024, over transitioned to silicone-insulated units to cope with ambient temperatures exceeding 50°C. South Africa, on the other hand, has initiated several renewable microgrid projects in off-grid mining regions, integrating silicone-based insulating oil in solar inverter transformers and load centers. Additionally, increased investment in oil and gas electrical systems in Kuwait and Nigeria is stimulating demand for high-performance silicone insulation materials.

United States – values at USD 52.1 Million, dominates due to extensive transformer replacement programs and urban fire safety mandates.

China – values at USD 39.3 Million, leads in volume-driven demand fueled by infrastructure growth and smart grid expansion.

The silicone-based insulating oil market is marked by a highly competitive environment where major chemical and specialty fluid producers vie for dominance. Dow, for instance, holds a leadership position with a global presence and extensive product lines tailored for transformer, switchgear, and capacitor insulation applications. Other significant players include Momentive, Shin‑Etsu Chemical, and Wacker Chemie, each leveraging strong R&D capabilities and strategic partnerships with utilities and OEMs.

In 2023–2024, competition intensified as companies focused on product differentiation and regional expansion. For example, a key player introduced biodegradable silicone oils with enhanced thermal stability, enabling entry into environmentally regulated markets. Another competitor invested in nanotechnology to increase dielectric performance, appealing to high-voltage and harsh climate applications. Moreover, several firms have expanded manufacturing footprints and distribution networks across Asia-Pacific and the Middle East to tap into infrastructure growth. This competitive push is further underscored by increasing alliances between silicone oil manufacturers and power equipment OEMs, aimed at co-developing insulating fluids tailored to specific transformer designs and grid modernization needs. Product innovation, regional presence, and strategic partnerships remain the primary levers for competitive advantage in this market.

Dow

Momentive

Shin‑Etsu Chemical

Wacker Chemie

Elkem Silicones

Evonik

Ferro

Technology innovations are critical drivers in the silicone-based insulating oil sector, with recent advancements focused on enhancing thermal performance, dielectric properties, and environmental safety. One notable development is the integration of nanotechnology, where nanoparticles such as titanium dioxide are dispersed in silicone oil to increase dielectric breakdown voltage and improve electrical insulation—research has shown significant improvement in breakdown strength under high-stress conditions.

Another important trend is the development of biodegradable and low-toxicity silicone formulations. These new grades maintain high fire points and thermal stability while reducing environmental impact, appealing to eco-conscious utilities and regulators.

Additionally, improvements in polymer-modified silicone oils have advanced oxidation resistance and viscosity stability at high temperatures. These enhancements enable long-term performance and reduce maintenance intervals for heavy-duty transformer units.

On the manufacturing side, AI-driven quality control systems are now being used to detect formulation inconsistencies in real time, ensuring compliance with strict industry standards. Sensor-enabled production lines also allow dynamic monitoring of viscosity, moisture content, and dielectric constant, improving batch consistency.

Lastly, compatibility-focused additives are being introduced to ease retrofilling of silicone oil into existing mineral oil-based transformers. These additives reduce seal swelling and eliminate the need for hardware replacement, simplifying adoption in legacy systems.

In June 2024, In Australia’s EnergyConnect transmission project, Ergon Inc. and distributor Molekulis introduced their HyVolt transformer oils—silicone-based fluids designed to enhance performance in large interconnector substations across NSW and Victoria, featuring thermal stability improvements under high-load conditions.

In February 2023, Cargill launched its FR3r natural ester insulating fluid—derived from over 95% rapeseed oil—which includes modified silicone components to extend fluid lifespan and improve eco-profile compared to traditional ester oils.

In June 2023, Antala, an industrial chemicals distributor, expanded its silicone transformer oil offerings, adding high-dielectric-strength silicone fluids targeted at emerging power infrastructure projects in Southeast Asia and Africa.

In March 2023, Nynas AB broadened its bio-based transformer oil line (NYTRO series), incorporating silicone additives to enhance environmental credentials and dielectric performance, catering to North American grid modernization demands.

This report comprehensively covers silicone-based insulating oils used primarily in power transformers, distribution transformers, switchgear, and capacitors. It addresses key areas such as product types (high-/low-viscosity, modified silicones), application contexts (HV, MV, and specialty equipment), and end-user segments (utilities, industrial, renewables, and commercial infrastructure). It analyzes technology trends, including nanofluid formulations, biodegradable grades, AI-enabled quality control, and retrofit compatibility solutions.

Additionally, the report highlights regional market developments—covering North America, Europe, Asia-Pacific, South America, and Middle East & Africa—offering insights into the drivers, pricing variations, and regulatory influences prevalent in each region. Competitive analysis profiles major players, their product portfolios, technological initiatives, and strategic partnerships. Real-world case studies illustrate silicone oil deployment in grid upgrades, renewable integration, and climate-challenging environments. The report also outlines recent market events, such as product launches and project rollouts, to demonstrate innovation momentum and adoption patterns.

Overall, this market report serves as a strategic tool for manufacturers, utilities, OEMs, and investors by detailing product trends, technology advances, competitive positioning, and regional dynamics necessary for informed decision-making within the silicone-based insulating oil sector.

| Report Attribute / Metric | Report Details |

|---|---|

| Market Name | Global Silicone‑based Insulating Oil Market |

| Market Revenue (2024) | USD 150.0 Million |

| Market Revenue (2032) | USD 248.2 Million |

| CAGR (2025–2032) | 6.5 % |

| Base Year | 2024 |

| Forecast Period | 2025 – 2032 |

| Historic Period | 2020 – 2024 |

| Segments Covered |

By Type

By Application

By End-User

|

| Key Report Deliverables | Revenue Forecast, Growth Trends, Market Dynamics, Segmental Overview, Regional & Country‑wise Analysis, Competition Landscape, Technological Insights, Recent Developments |

| Regions Covered | North America, Europe, Asia‑Pacific, South America, Middle East & Africa |

| Key Players Analyzed | Dow, Momentive, Shin‑Etsu Chemical, Wacker Chemie, Elkem Silicones, Evonik, Ferro |

| Customization & Pricing | Available on Request (10 % Customization is Free) |