Reports

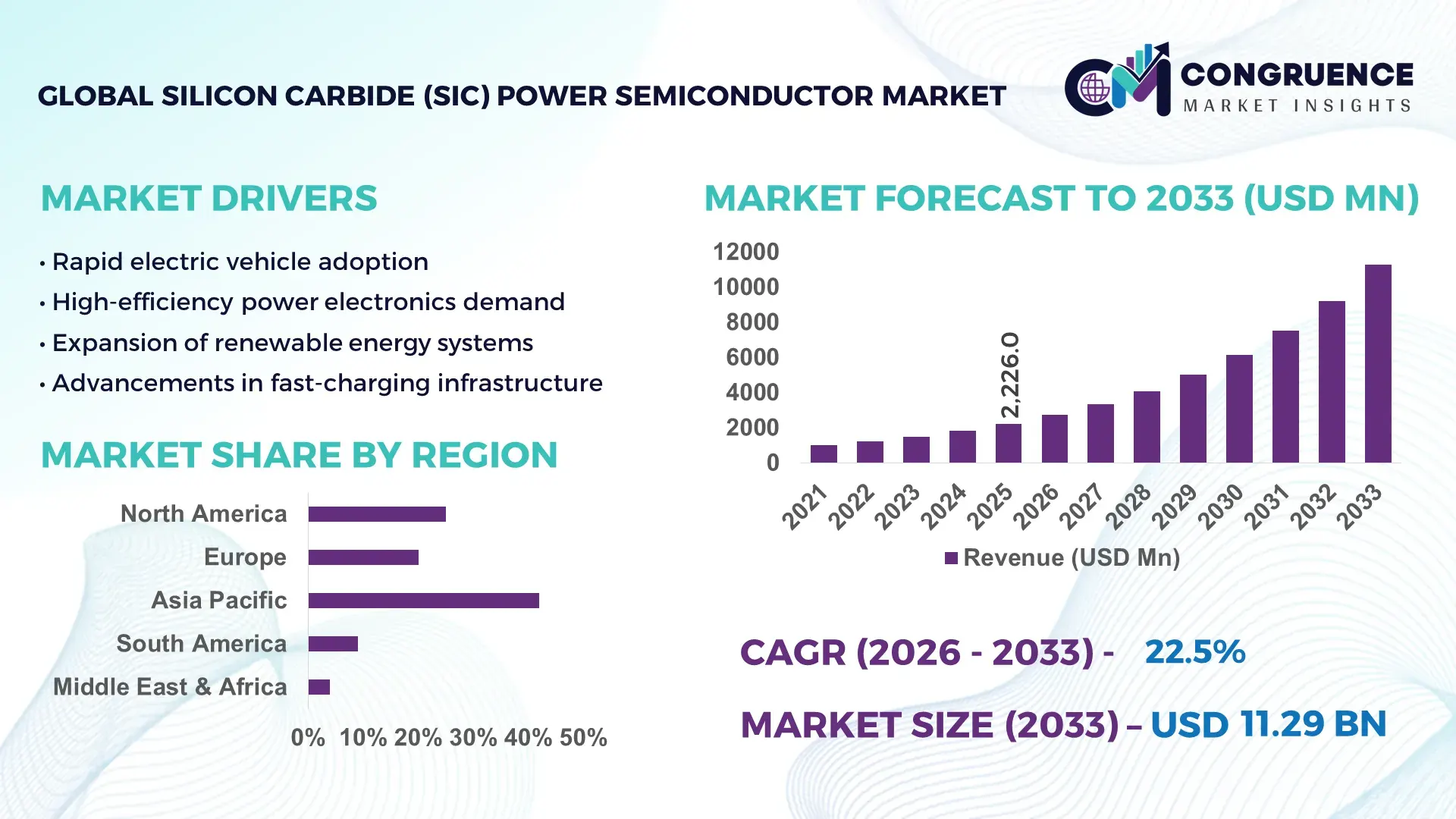

The Global Silicon Carbide (SiC) Power Semiconductor Market was valued at USD 2225.95 Million in 2025 and is anticipated to reach a value of USD 11287.69 Million by 2033 expanding at a CAGR of 22.5% between 2026 and 2033. This expansion is driven by accelerated electrification across automotive, energy, and industrial power systems requiring higher efficiency and thermal performance.

China represents the most influential country in the Silicon Carbide (SiC) power semiconductor landscape, supported by large-scale manufacturing capacity, sustained capital investment, and rapid downstream adoption. By 2025, China operated over 15 active or announced SiC wafer and device fabrication facilities, with cumulative planned investments exceeding USD 12 billion. Domestic SiC wafer production capacity surpassed 1.2 million 6-inch equivalent wafers annually, supporting applications across electric vehicles, fast-charging infrastructure, renewable energy inverters, rail traction, and industrial motor drives. China’s EV sector alone integrated SiC devices in over 35% of newly launched high-voltage platforms in 2024, while SiC-based photovoltaic inverters accounted for approximately 40% of new utility-scale solar installations. Continuous advancements in 8-inch SiC wafer processing, epitaxy yield optimization, and vertical device integration further strengthen China’s technological footprint across the SiC value chain.

Market Size & Growth: USD 2225.95 Million in 2025, projected to reach USD 11287.69 Million by 2033 at a CAGR of 22.5%, driven by high-voltage electrification and efficiency mandates.

Top Growth Drivers: EV powertrain adoption at ~32%, power conversion efficiency improvement of ~45%, system-level energy loss reduction of ~50%.

Short-Term Forecast: By 2028, average SiC device cost per kW is expected to decline by ~28% due to scale-up of 8-inch wafers and yield improvements.

Emerging Technologies: 8-inch SiC wafers, advanced trench MOSFET architectures, high-temperature SiC modules for >800V systems.

Regional Leaders: Asia-Pacific at ~USD 5200 Million by 2033 with EV integration focus; North America at ~USD 3400 Million driven by industrial and data center power; Europe at ~USD 2100 Million led by automotive electrification.

Consumer/End-User Trends: Automotive OEMs, renewable energy developers, and industrial automation users increasingly prefer SiC for compact, high-efficiency designs.

Pilot or Case Example: In 2024, a commercial EV platform deployment achieved ~6% driving range improvement using full SiC inverter architecture.

Competitive Landscape: Wolfspeed holds ~35% share, followed by Infineon Technologies, STMicroelectronics, onsemi, ROHM Semiconductor, and Mitsubishi Electric.

Regulatory & ESG Impact: Stricter vehicle efficiency norms, grid decarbonization targets, and energy-efficiency standards accelerate SiC adoption.

Investment & Funding Patterns: Over USD 18 billion invested globally since 2022 in SiC fabs, wafer expansion, and vertically integrated supply chains.

Innovation & Future Outlook: Integration of SiC with advanced packaging, AI-driven power management, and ultra-fast charging ecosystems will define next-phase growth.

The Silicon Carbide (SiC) power semiconductor market serves critical industry sectors including automotive, which contributes approximately 45% of total demand, followed by industrial power electronics at around 25%, and energy and utilities near 20%. Recent innovations such as 8-inch SiC wafers, next-generation MOSFETs, and high-density power modules are improving performance while reducing system costs. Regulatory pressure to lower emissions, combined with energy-efficiency standards and renewable integration targets, continues to stimulate adoption. Regionally, Asia-Pacific leads consumption due to EV and renewable deployment, while North America and Europe exhibit strong growth in industrial automation and charging infrastructure. Emerging trends include vertical integration, localized wafer supply chains, and increasing use of SiC in data centers and aerospace, positioning the market for sustained long-term expansion.

The strategic relevance of the Silicon Carbide (SiC) Power Semiconductor Market lies in its ability to redefine power efficiency, system density, and long-term sustainability across critical electrification value chains. SiC-based power devices are increasingly embedded in electric vehicles, renewable energy systems, rail traction, data centers, and industrial automation due to their superior electrical and thermal characteristics. For comparative benchmarking, Silicon Carbide (SiC) MOSFET technology delivers approximately 45% higher power conversion efficiency compared to traditional silicon IGBT standards, while also enabling switching frequency improvements of over 60% at high voltages. Regionally, Asia-Pacific dominates in volume-driven manufacturing and device shipments, while Europe leads in adoption intensity, with nearly 42% of automotive OEMs integrating SiC-based inverters across new EV platforms. Over the short term, by 2028, AI-enabled power module design optimization is expected to improve thermal management efficiency by nearly 20%, reducing system-level cooling requirements and total energy loss. From a compliance and ESG perspective, firms across the SiC value chain are committing to carbon-intensity reductions of 25–30% per device through energy-efficient fabs and recycling of silicon carbide substrates by 2030. In a measurable micro-scenario, in 2024, a leading European automotive manufacturer achieved a 6% increase in EV driving range through full SiC inverter deployment combined with AI-based power management. Looking forward, the Silicon Carbide (SiC) Power Semiconductor Market is positioned as a core pillar supporting resilience, regulatory compliance, and sustainable growth across global electrification ecosystems.

The rapid electrification of transportation is a primary driver of growth for the Silicon Carbide (SiC) Power Semiconductor market. SiC devices enable higher switching frequencies, reduced conduction losses, and compact inverter designs, making them ideal for electric vehicles, rail systems, and charging infrastructure. By 2025, over 35% of newly introduced global EV platforms adopted SiC-based inverters, particularly in premium and long-range models. SiC power modules also support operating temperatures exceeding 200°C, reducing cooling system weight by up to 30%. In fast-charging applications, SiC enables charging efficiencies above 98%, significantly lowering energy loss per charging cycle. These performance benefits directly translate into extended vehicle range, reduced system complexity, and improved total cost of ownership, reinforcing sustained adoption across transportation segments.

Despite strong demand, the Silicon Carbide (SiC) Power Semiconductor market faces restraints related to manufacturing complexity and substrate availability. Producing defect-free SiC wafers is significantly more challenging than silicon, with defect densities historically up to ten times higher. As of 2025, global SiC substrate yield rates remained below 70% for advanced power-grade wafers, limiting supply consistency. Capital requirements for a single SiC fabrication line often exceed USD 1 billion, creating high entry barriers. Additionally, long qualification cycles in automotive and aerospace applications, often exceeding 24 months, slow down commercial scalability. These structural limitations constrain rapid capacity expansion and contribute to price volatility across the supply chain.

The expansion of renewable energy infrastructure presents significant opportunities for the Silicon Carbide (SiC) Power Semiconductor market. SiC devices are increasingly used in solar inverters, wind power converters, and energy storage systems due to their high efficiency and ability to operate at elevated voltages. By 2025, SiC-based inverters accounted for approximately 40% of new utility-scale solar installations, driven by their ability to reduce power losses by nearly 50% compared to silicon-based solutions. In energy storage systems, SiC enables faster bidirectional power flow and higher power density, supporting grid stability and peak-load management. As global renewable capacity additions continue to rise, SiC adoption is expected to deepen across both centralized and distributed energy architectures.

Cost pressures and the lack of unified industry standards remain critical challenges for the Silicon Carbide (SiC) Power Semiconductor market. Although device-level costs are declining, SiC components still carry a price premium of 2–3 times compared to conventional silicon alternatives. Variability in packaging standards, gate drive requirements, and reliability testing protocols increases integration complexity for system designers. Additionally, the shortage of skilled engineers with SiC-specific design expertise slows adoption in emerging markets. Regulatory differences across regions further complicate certification and deployment timelines. These challenges require coordinated efforts in standardization, workforce development, and supply chain optimization to ensure long-term market scalability.

• Accelerated Transition to 8-Inch SiC Wafers: The shift from 6-inch to 8-inch Silicon Carbide wafers is a defining trend, directly impacting scalability and unit economics. By 2025, over 30% of newly announced SiC fabrication capacity globally is designed around 8-inch wafer lines. This transition improves die output per wafer by approximately 85% and reduces cost per device by nearly 25%. Yield improvements of 15–20% have been reported in early high-volume runs, enabling faster qualification for automotive and industrial-grade applications.

• Deepening Penetration of 800V+ Electric Vehicle Architectures: Silicon Carbide power semiconductors are increasingly standard in high-voltage EV platforms. In 2024–2025, nearly 40% of newly launched premium and mid-range EV models adopted full SiC-based inverters. Compared to silicon solutions, SiC enables switching loss reductions of around 50% and supports power density improvements of over 60%. These gains translate into 5–7% vehicle range enhancement and up to 10% reduction in inverter weight, strengthening OEM adoption momentum.

• Expansion of SiC in Fast-Charging and Grid Infrastructure: Deployment of SiC devices in DC fast chargers and grid-tied power systems is accelerating. By 2025, more than 45% of new ultra-fast charging stations above 150 kW incorporated SiC-based power modules. These systems achieve charging efficiencies above 98% and reduce thermal losses by nearly 40%. In grid applications, SiC adoption in solid-state transformers and energy storage interfaces has improved power conversion efficiency by approximately 35%.

• Integration of Advanced Packaging and Intelligent Power Modules: Advanced packaging, including double-sided cooling and high-density power modules, is reshaping SiC system design. Around 28% of new SiC power modules introduced in 2024 featured advanced thermal packaging, enabling junction temperature increases of up to 30°C. Additionally, integration of digital monitoring and AI-assisted control within SiC modules has improved fault detection accuracy by nearly 25% and reduced unplanned downtime in industrial applications by about 18%.

The Silicon Carbide (SiC) Power Semiconductor market is segmented by type, application, and end-user, each reflecting distinct adoption patterns driven by performance requirements, voltage levels, and operating environments. Product segmentation highlights strong differentiation between discrete devices and power modules based on integration depth and thermal performance. Application-wise, transportation electrification and energy infrastructure dominate demand due to efficiency and high-voltage needs, while industrial and data center applications show steady expansion. End-user segmentation reflects concentrated adoption among automotive OEMs and power equipment manufacturers, alongside rising uptake from utilities and industrial automation players. Across segments, purchasing decisions are increasingly influenced by lifecycle efficiency, thermal stability above 200°C, and compatibility with next-generation power architectures, shaping how demand is distributed across types, use cases, and customer groups.

The Silicon Carbide (SiC) Power Semiconductor market by type is led by SiC MOSFETs, which account for approximately 48% of total adoption due to their superior switching efficiency, low on-resistance, and suitability for voltages above 650V. SiC MOSFETs are widely deployed in EV inverters, fast chargers, and renewable energy systems where efficiency gains of 40–50% over silicon devices are critical. SiC power modules represent the fastest-growing type, driven by demand for compact, high-power-density solutions in automotive and industrial systems; this segment is expanding at an estimated 26% CAGR as OEMs move toward integrated module architectures to reduce system complexity. SiC diodes, including Schottky barrier diodes, continue to play a supporting role in power factor correction and auxiliary circuits, contributing to roughly 18% of total demand. Other device types, such as hybrid modules and customized multi-chip packages, collectively account for about 8% and serve niche applications requiring tailored thermal or voltage performance.

By application, electric vehicles and transportation systems dominate the Silicon Carbide (SiC) Power Semiconductor market with an estimated 45% share, reflecting widespread adoption in traction inverters, onboard chargers, and DC fast-charging infrastructure. In comparison, renewable energy and power generation applications account for around 28%, while industrial motor drives and automation systems contribute nearly 17%. Although EVs lead in current deployment, renewable energy applications are the fastest-growing, supported by large-scale solar and wind installations adopting SiC-based inverters; this segment is expanding at approximately 24% CAGR as grid operators prioritize efficiency and reduced thermal losses. Data centers and power supply units form a smaller but growing segment, benefiting from SiC’s ability to cut power losses by more than 30% in high-frequency switching environments.

From an end-user perspective, automotive OEMs and tier-1 suppliers represent the largest segment, accounting for approximately 47% of total Silicon Carbide (SiC) Power Semiconductor usage, driven by electrified powertrains and high-voltage vehicle platforms. Utilities and energy companies follow with around 22% share, reflecting adoption in renewable integration and grid modernization projects. Industrial equipment manufacturers contribute close to 18%, particularly in high-efficiency motor drives and automation systems. While automotive remains dominant, energy and utility operators constitute the fastest-growing end-user group, expanding at an estimated 23% CAGR due to rising deployment of SiC-enabled inverters and solid-state transformers. Other end-users, including data center operators, rail operators, and aerospace system integrators, collectively account for about 13%, with adoption rates exceeding 20% in advanced power management applications.

Asia-Pacific accounted for the largest market share at 46% in 2025 however, North America is expected to register the fastest growth, expanding at a CAGR of 24.1% between 2026 and 2033.

Asia-Pacific dominance is supported by high-volume manufacturing, strong EV penetration, and large-scale renewable energy deployments, with over 1.2 million SiC wafers processed annually across the region. North America’s accelerated growth outlook is driven by capacity expansion, with more than USD 8 billion committed to new SiC fabs and over 35% of new EV platforms integrating SiC-based power modules. Europe holds approximately 27% market share, supported by regulatory-driven electrification and sustainability mandates. South America and the Middle East & Africa together account for nearly 12%, reflecting growing investments in grid infrastructure, industrial electrification, and energy transition programs. Regional disparities in adoption intensity, manufacturing depth, and end-use applications continue to shape differentiated growth trajectories across the global Silicon Carbide (SiC) Power Semiconductor market.

How is advanced manufacturing and electrification reshaping demand dynamics?

North America holds approximately 29% of the Silicon Carbide (SiC) Power Semiconductor market, supported by strong demand from electric vehicles, renewable energy systems, aerospace, and data centers. The region has over 40% of global announced SiC fabrication expansions, reflecting policy-backed domestic semiconductor manufacturing initiatives. Government incentives targeting clean energy and EV supply chains have accelerated adoption of SiC devices in fast-charging networks and grid-scale energy storage. Technologically, the region leads in 8-inch SiC wafer transition and AI-assisted power module design. A notable local player is actively expanding vertically integrated SiC manufacturing to support automotive and industrial customers. Regional consumer behavior shows higher enterprise adoption in automotive, energy, and mission-critical infrastructure, with SiC increasingly preferred for long-life, high-reliability power systems.

How do regulatory mandates accelerate next-generation power electronics adoption?

Europe accounts for nearly 27% of the Silicon Carbide (SiC) Power Semiconductor market, with Germany, France, and the UK representing more than 65% of regional demand. Strong regulatory frameworks tied to vehicle emissions, energy efficiency, and industrial decarbonization are accelerating SiC adoption. Over 45% of newly launched European EV platforms utilize SiC-based inverters, reflecting high adoption intensity. Sustainability initiatives promoting energy-efficient power conversion have also driven SiC use in rail traction and renewable energy inverters. Regional players are focusing on advanced automotive-grade SiC modules and localized supply chains. Consumer behavior in the region is shaped by regulatory pressure, resulting in demand for highly efficient, traceable, and standards-compliant Silicon Carbide (SiC) Power Semiconductor solutions.

Why does manufacturing scale and EV penetration define regional leadership?

Asia-Pacific leads the Silicon Carbide (SiC) Power Semiconductor market by volume, accounting for approximately 46% of global demand. China, Japan, and South Korea collectively represent over 70% of regional consumption, driven by EV production, renewable installations, and industrial automation. The region hosts more than 15 active SiC wafer and device fabrication facilities, with rapid scaling of 8-inch wafer lines. China alone integrates SiC devices in over 35% of new high-voltage EV platforms. Regional innovation hubs focus on yield optimization, vertical integration, and cost reduction. Consumer behavior reflects high-volume adoption driven by manufacturing efficiency, EV affordability, and infrastructure expansion.

How is energy infrastructure modernization influencing adoption patterns?

South America accounts for approximately 7% of the global Silicon Carbide (SiC) Power Semiconductor market, with Brazil and Argentina as key contributors. Regional demand is largely driven by renewable energy projects, grid upgrades, and industrial electrification. Solar and wind installations using SiC-based inverters have increased system efficiency by nearly 30% compared to legacy technologies. Government incentives supporting clean energy and localized manufacturing have improved market accessibility. While local production remains limited, regional players are partnering with global suppliers to integrate SiC into power systems. Consumer behavior shows demand closely tied to energy reliability, cost efficiency, and localized application requirements.

How are diversification and digital infrastructure driving power semiconductor demand?

The Middle East & Africa region represents close to 5% of the Silicon Carbide (SiC) Power Semiconductor market, with growth concentrated in the UAE, Saudi Arabia, and South Africa. Demand is supported by oil & gas electrification, renewable energy projects, smart city developments, and data center expansion. SiC devices are increasingly deployed in high-temperature, high-reliability environments, improving power efficiency by over 35% in grid and industrial systems. Regional trade partnerships and technology transfer initiatives support adoption. Consumer behavior reflects preference for durable, high-efficiency power electronics aligned with long-term infrastructure investments.

China – 34% market share: Dominance driven by large-scale SiC manufacturing capacity, high EV production volumes, and extensive renewable energy deployment.

United States – 28% market share: Leadership supported by advanced SiC fabrication, strong automotive and energy demand, and significant government-backed semiconductor investments.

The Silicon Carbide (SiC) Power Semiconductor market exhibits a moderately consolidated competitive structure, characterized by a limited number of vertically integrated leaders and a growing pool of specialized device and module manufacturers. Globally, more than 35 active companies participate across wafer manufacturing, discrete devices, and power module integration. The top five players collectively account for approximately 70–75% of total market presence, reflecting high entry barriers driven by capital intensity, long qualification cycles, and substrate complexity.

Competition is increasingly shaped by capacity expansion strategies, particularly the shift toward 8-inch SiC wafer fabrication, which improves die output by nearly 80–85% per wafer compared to 6-inch formats. Strategic initiatives such as long-term automotive supply agreements, multi-billion-dollar fab expansions, and vertical integration across substrates, epitaxy, and devices are defining competitive positioning. Product innovation focuses on high-voltage MOSFETs above 1200V, advanced trench architectures, and double-sided cooled power modules capable of operating beyond 200°C junction temperatures.

Partnerships between automotive OEMs and SiC suppliers have increased by over 30% since 2023, ensuring supply security and faster platform qualification. Mergers and technology collaborations are also rising as companies seek to shorten development cycles and improve yield rates, which currently average 65–75% for power-grade wafers. Overall, competition is driven by scalability, automotive-grade reliability, and the ability to deliver cost reductions of 20–30% at the system level.

Wolfspeed

Infineon Technologies AG

STMicroelectronics

onsemi

ROHM Semiconductor

Mitsubishi Electric Corporation

Fuji Electric Co., Ltd.

Toshiba Electronic Devices & Storage

Bosch Semiconductor

Renesas Electronics Corporation

The Silicon Carbide (SiC) Power Semiconductor market’s technology landscape is being shaped by innovations that materially improve device performance, manufacturing efficiency, and system-level integration. A major technological shift is the industry-wide transition to 200 mm (8-inch) SiC wafer technology, which increases die output per wafer by up to 85–90% compared to legacy 150 mm wafers and enables more efficient use of expensive SiC substrates. Leading manufacturers have started releasing the first commercial products based on advanced 200 mm SiC wafers, targeting high-voltage applications across EV traction inverters, renewable energy systems, and industrial power converters, a milestone that enhances production scalability and product standardization across multiple end markets.

Device architecture continues to evolve with trench MOSFETs, superjunction structures, and advanced packaging, yielding significantly lower switching and conduction losses—improving energy efficiency by up to 40% over conventional designs. Compact packages, including TO-Leadless (TOLL) formats, are now achieving ~39% thermal performance improvements and reduced device footprints for high-density power applications, which accelerates deployment in space-constrained systems such as AI servers and photovoltaic inverters. (

SiC integration with digital control, sensing, and AI-assisted design tools is reducing design cycles and enabling more precise predictive thermal and reliability modeling. This supports broader adoption in grid infrastructure, aerospace, and defense systems that demand robust, high-temperature performance. Additionally, heterogenous integration of SiC with gallium nitride (GaN) and other wide-bandgap materials is emerging as a pathway to address ultra-high frequency and high power density requirements, further diversifying the technology base. Overall, these advancements drive a more competitive, performance-focused era in which SiC technology is central to next-generation electrified systems requiring superior efficiency, reliability, and compact form factors.

• In Q1 2025, Infineon Technologies AG began releasing its first silicon carbide (SiC) power products built on an advanced 200 mm wafer manufacturing technology from its Villach, Austria facility, enhancing high-voltage capabilities for EV, renewable energy, and rail applications as part of its SiC technology roadmap. (Infineon)

• In December 2025, ROHM Semiconductor initiated full-scale mass production of its SCT40xxDLL series of SiC MOSFETs in a compact TO-Leadless (TOLL) package, delivering about 39% improved thermal performance and a reduced footprint, supporting industrial power supplies, energy storage systems, and PV inverters. (Semiconductor Today)

• In early 2025, Wolfspeed neared completion of its $5 billion specialized SiC wafer fabrication facility in Chatham County, North Carolina, targeting advanced 200 mm SiC wafer production by mid-2025 to support EV, energy, and AI power semiconductor demands. (TrendForce)

• Throughout 2024–2025, multiple major SiC wafer fab expansions progressed globally, including Infineon’s Kulim, Malaysia 8-inch wafer fab commencing operations, and onsemi’s expanded Korean facility transitioning to 8-inch production by 2025, indicating broad industry shifts toward scalable SiC manufacturing. (Semiconductor Today)

The scope of the Silicon Carbide (SiC) Power Semiconductor Market Report encompasses a comprehensive evaluation of the industry across device types, voltage classes, applications, end-user industries, and geographic regions. The report examines key product categories including SiC MOSFETs, diodes, and integrated power modules, covering voltage ranges from below 650V to above 1700V, which together address requirements across transportation, energy, and industrial power systems. It assesses adoption patterns across core applications such as electric vehicle traction inverters, onboard chargers, DC fast-charging stations, renewable energy inverters, industrial motor drives, rail traction, aerospace power systems, and high-efficiency data center power supplies.

Geographically, the report analyzes market dynamics across North America, Europe, Asia-Pacific, South America, and the Middle East & Africa, capturing differences in manufacturing concentration, technology deployment intensity, and regulatory influence. Asia-Pacific is evaluated for high-volume production and supply chain integration, while North America and Europe are examined for advanced device innovation, qualification standards, and high-value system integration. The report also includes emerging regions where grid modernization, clean energy investment, and industrial electrification are expanding SiC adoption.

From a technology perspective, the scope covers advancements in 6-inch and 8-inch wafer processing, epitaxial growth techniques, trench and planar MOSFET architectures, advanced packaging formats, and thermal management innovations. Industry focus areas include automotive OEMs, tier-1 suppliers, utilities, industrial equipment manufacturers, and infrastructure developers. Additionally, the report incorporates niche segments such as solid-state transformers, aerospace electrification, and ultra-fast charging systems, providing decision-makers with a structured view of current coverage and future opportunity areas within the Silicon Carbide (SiC) Power Semiconductor ecosystem.

| Report Attribute/Metric | Report Details |

|---|---|

|

Market Revenue in 2025 |

USD V2025 Million |

|

Market Revenue in 2033 |

USD V2033 Million |

|

CAGR (2026 - 2033) |

22.5% |

|

Base Year |

2025 |

|

Forecast Period |

2026 - 2033 |

|

Historic Period |

2021 - 2025 |

|

Segments Covered |

By Types

By Application

By End-User

|

|

Key Report Deliverable |

Revenue Forecast, Growth Trends, Market Dynamics, Segmental Overview, Regional and Country-wise Analysis, Competition Landscape |

|

Region Covered |

North America, Europe, Asia-Pacific, South America, Middle East, Africa |

|

Key Players Analyzed |

Wolfspeed, Infineon Technologies AG, STMicroelectronics, onsemi, ROHM Semiconductor, Mitsubishi Electric Corporation, Fuji Electric Co., Ltd., Toshiba Electronic Devices & Storage, Bosch Semiconductor, Renesas Electronics Corporation |

|

Customization & Pricing |

Available on Request (10% Customization is Free) |