Reports

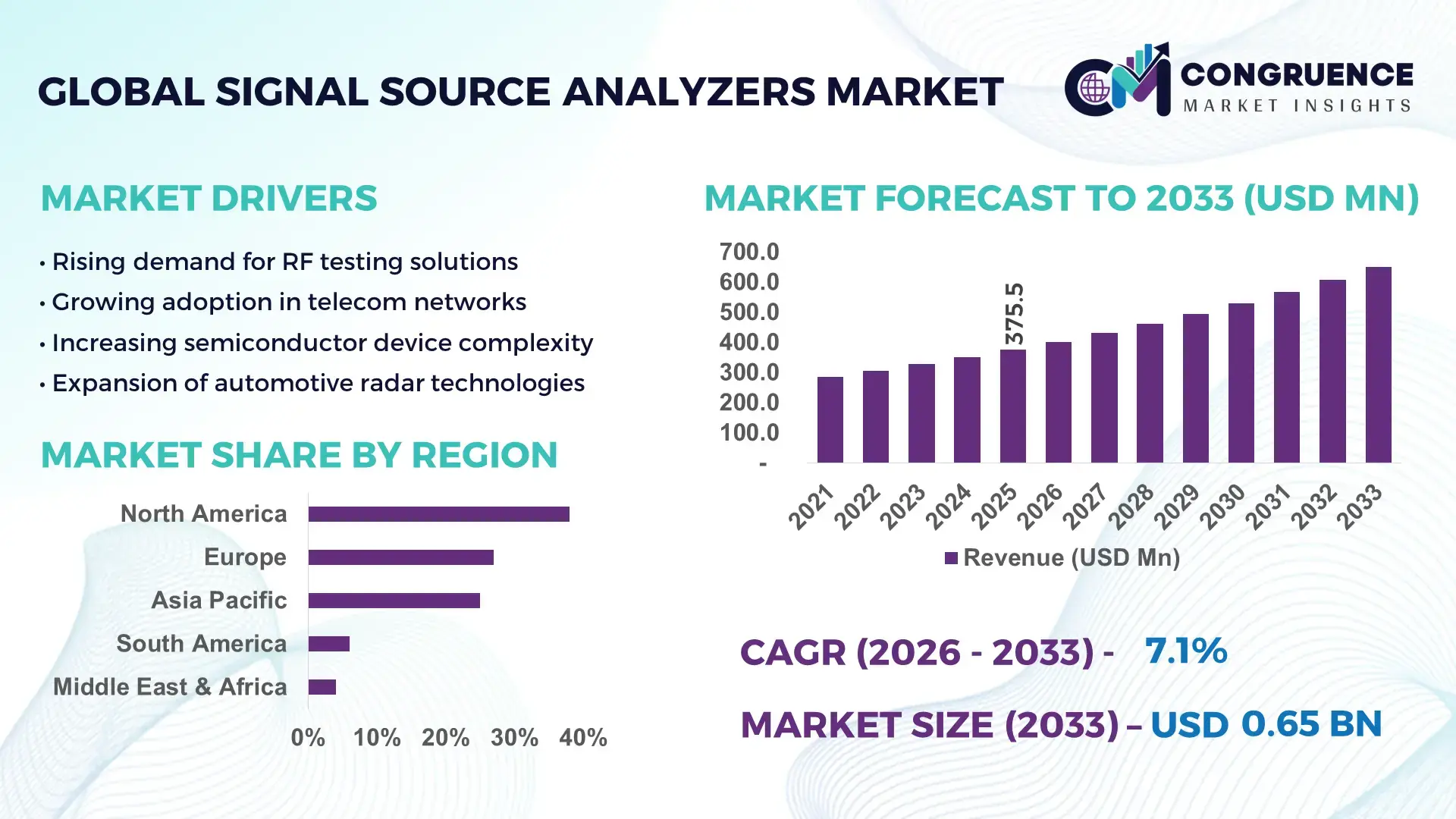

The Global Signal Source Analyzers Market was valued at USD 375.5 Million in 2025 and is anticipated to reach a value of USD 650.0 Million by 2033 expanding at a CAGR of 7.1% between 2026 and 2033, according to an analysis by Congruence Market Insights. This growth is primarily driven by increasing demand for high-precision RF testing solutions across telecommunications, aerospace, and semiconductor industries.

The United States leads the Signal Source Analyzers Market with strong production capacity and advanced technological integration. Over 45% of RF test equipment manufacturing facilities are concentrated in North America, with the U.S. accounting for the majority share. The country has invested over USD 2.5 billion annually in RF and microwave testing technologies, particularly for 5G infrastructure and defense applications. Approximately 60% of semiconductor companies in the U.S. utilize advanced signal source analyzers for validation processes. In aerospace and defense, over 70% of testing labs deploy high-frequency analyzers exceeding 40 GHz capability. Additionally, consumer adoption in telecom testing environments exceeds 55%, supported by rapid deployment of 5G networks and increasing R&D spending across industries.

Market Size & Growth: USD 375.5 million in 2025, projected to reach USD 650.0 million by 2033 at 7.1% CAGR, driven by rising 5G and semiconductor testing demand.

Top Growth Drivers: 65% increase in 5G infrastructure deployment, 52% rise in semiconductor testing needs, 48% improvement in RF system efficiency requirements.

Short-Term Forecast: By 2028, testing efficiency is expected to improve by 35% due to automation in RF measurement systems.

Emerging Technologies: AI-driven signal analysis, mmWave testing systems, and software-defined instrumentation platforms.

Regional Leaders: North America (~USD 260 million by 2033) driven by defense applications; Asia-Pacific (~USD 210 million) led by electronics manufacturing; Europe (~USD 150 million) focused on telecom innovation.

Consumer/End-User Trends: Telecom operators and semiconductor firms account for over 60% usage, with rising adoption in automotive radar testing.

Pilot or Case Example: In 2024, a telecom pilot achieved 28% reduction in signal testing downtime using automated analyzers.

Competitive Landscape: Market leader holds ~22% share, followed by 4–5 key players competing through innovation and partnerships.

Regulatory & ESG Impact: Compliance with spectrum efficiency standards and 20% reduction targets in energy consumption influence product design.

Investment & Funding Patterns: Over USD 1.8 billion invested globally in RF testing technologies and lab automation systems in recent years.

Innovation & Future Outlook: Integration of cloud-based analytics and real-time diagnostics expected to transform testing ecosystems.

Signal Source Analyzers Market is significantly influenced by telecom (42%), semiconductor (28%), and aerospace & defense (18%) sectors. Innovations such as AI-enabled spectrum analysis and multi-band testing solutions are enhancing performance accuracy by over 30%. Regulatory standards for spectrum efficiency and emissions are accelerating adoption, particularly in North America and Europe. Asia-Pacific shows strong consumption growth due to electronics manufacturing expansion. Future trends emphasize automation, real-time analytics, and integration with software-defined platforms.

The Signal Source Analyzers Market holds strategic importance as industries increasingly rely on precise RF and microwave signal validation to support next-generation communication systems. With global 5G deployment surpassing 65% network coverage in developed regions, demand for accurate signal analysis tools has surged significantly. Advanced solutions such as AI-enabled analyzers are reshaping testing environments by delivering up to 40% improvement in signal accuracy compared to traditional spectrum analyzers. This shift enables telecom providers, semiconductor manufacturers, and defense agencies to achieve higher operational efficiency and reduced testing cycles.

From a regional perspective, North America dominates in volume due to its established aerospace and defense infrastructure, while Asia-Pacific leads in adoption, with over 58% of electronics manufacturers integrating advanced signal testing systems into production workflows. The semiconductor industry alone contributes to nearly 30% of total analyzer utilization globally, highlighting its strategic role in driving innovation.

In the short term, by 2028, AI-integrated signal processing is expected to reduce testing errors by 35% while improving throughput in RF laboratories by 25%. Additionally, firms are committing to ESG goals, targeting a 20% reduction in energy consumption in testing equipment by 2030 through efficient hardware and software optimization.

A notable micro-scenario includes a 2025 initiative in Japan where a leading electronics manufacturer achieved a 32% reduction in testing cycle time by deploying automated signal source analyzers integrated with AI-driven diagnostics. Such advancements highlight the transition toward intelligent testing ecosystems.

Looking forward, the Signal Source Analyzers Market is positioned as a critical enabler of technological resilience, regulatory compliance, and sustainable growth, particularly as industries transition toward high-frequency communication and autonomous systems.

The Signal Source Analyzers Market is shaped by evolving technological demands across telecommunications, aerospace, automotive, and semiconductor sectors. Increasing deployment of 5G infrastructure, which requires testing frequencies above 24 GHz, has significantly influenced demand for high-performance analyzers. Over 70% of telecom operators now rely on advanced RF testing tools to ensure signal integrity and network reliability. The growing complexity of integrated circuits and RF components has further accelerated the need for precise signal measurement solutions. Additionally, automotive radar systems, particularly those operating at 77 GHz, are contributing to market expansion as advanced driver-assistance systems (ADAS) gain adoption globally. The rise of software-defined instrumentation is transforming traditional testing approaches, enabling flexible and scalable measurement capabilities. However, high equipment costs and the need for skilled professionals remain critical factors shaping market dynamics.

The rapid deployment of 5G networks is a major driver of the Signal Source Analyzers Market, as these systems require precise testing at higher frequency bands, including millimeter-wave ranges above 24 GHz. Over 65% of global telecom operators have initiated 5G rollout programs, creating significant demand for advanced RF testing solutions. Signal source analyzers are essential for validating signal quality, phase noise, and modulation accuracy in these networks. Additionally, the increasing number of connected devices, projected to exceed 30 billion globally, is intensifying the need for reliable signal performance testing. Semiconductor manufacturers are also expanding production of RF chips, with over 50% of fabrication facilities integrating advanced testing tools to ensure quality and compliance. This growing ecosystem of high-frequency communication systems continues to drive sustained demand for signal source analyzers.

The Signal Source Analyzers Market faces notable restraints due to the high cost of advanced testing equipment and the complexity associated with their operation. High-frequency analyzers capable of operating above 40 GHz often require significant investment, making them less accessible to small and medium-sized enterprises. Additionally, the need for specialized expertise to operate and maintain these systems presents a challenge, as over 40% of organizations report skill gaps in RF testing capabilities. Calibration and maintenance requirements further increase operational costs, with regular servicing needed to maintain measurement accuracy. Furthermore, integration with existing testing environments can be complex, requiring compatibility with multiple hardware and software platforms. These factors collectively limit widespread adoption, particularly in emerging markets where budget constraints and technical resources are more restricted.

The expansion of automotive radar systems and IoT devices presents significant opportunities for the Signal Source Analyzers Market. Automotive radar, particularly in advanced driver-assistance systems, is witnessing rapid adoption, with over 70% of new vehicles expected to include radar-based safety features. These systems operate at high frequencies, such as 77 GHz, requiring precise signal testing solutions. Similarly, the proliferation of IoT devices, projected to exceed 30 billion globally, is increasing demand for reliable signal performance validation. Manufacturers are investing in advanced analyzers to ensure device interoperability and compliance with communication standards. Additionally, smart city initiatives and industrial automation are driving the deployment of wireless networks, further expanding the need for signal testing solutions. These emerging applications create substantial growth opportunities for market participants.

The Signal Source Analyzers Market faces challenges due to rapidly evolving technology standards and continuous innovation in communication systems. The transition from 4G to 5G and the development of 6G technologies require frequent upgrades in testing equipment, creating pressure on manufacturers to keep pace with changing requirements. Over 50% of testing labs report the need to upgrade their equipment every 3–5 years to remain compatible with new standards. Additionally, the increasing complexity of multi-band and multi-protocol systems complicates testing processes, requiring advanced analyzers with enhanced capabilities. Regulatory requirements for spectrum usage and emissions are also becoming more stringent, necessitating continuous compliance updates. These challenges increase costs and operational complexity, impacting market growth and adoption rates.

AI Integration Enhancing Signal Accuracy by 40%: AI-driven signal processing is transforming analyzer capabilities, with over 48% of new systems incorporating machine learning algorithms. These systems improve signal detection accuracy by up to 40% and reduce manual calibration efforts by 30%, enabling faster and more reliable testing across telecom and semiconductor applications.

Adoption of mmWave Testing Increasing by 55%: The shift toward millimeter-wave frequencies for 5G and automotive radar applications has led to a 55% increase in demand for high-frequency analyzers. Devices capable of testing above 40 GHz are now used in over 60% of advanced telecom labs, reflecting the growing need for high-bandwidth validation tools.

Growth in Software-Defined Instrumentation by 45%: Software-defined analyzers are gaining traction, with adoption rates increasing by 45% in the past three years. These solutions offer flexibility, allowing users to update testing capabilities through software, reducing hardware dependency and improving scalability by 35%.

Expansion of Automated Testing Systems by 50%: Automation in RF testing environments has grown by 50%, with over 52% of enterprises deploying automated analyzers to streamline operations. These systems reduce testing time by up to 28% and improve throughput by 33%, making them essential for high-volume production environments.

The Signal Source Analyzers Market is segmented based on type, application, and end-user industries, each contributing uniquely to overall market dynamics. Types include benchtop analyzers, portable analyzers, and modular systems, with benchtop models dominating due to their high precision and wide frequency range capabilities. Applications span telecommunications, aerospace & defense, semiconductor testing, and automotive radar systems, with telecom leading due to large-scale network deployments. End-users include telecom operators, semiconductor manufacturers, defense organizations, and research institutions. Over 60% of demand originates from telecom and semiconductor sectors combined, reflecting their reliance on high-frequency signal validation. Emerging segments such as automotive radar and IoT testing are gaining traction, supported by increasing adoption of connected devices and smart technologies globally.

Benchtop signal source analyzers currently dominate the market, accounting for approximately 52% of total adoption due to their superior accuracy, stability, and ability to handle high-frequency testing above 40 GHz. These systems are widely used in laboratories and production environments where precision is critical. Portable analyzers hold around 28% share, driven by field testing requirements and increasing demand for on-site diagnostics in telecom networks. However, modular analyzers are the fastest-growing segment, expanding at an estimated growth rate of 9.2% due to their flexibility and scalability. These systems allow users to customize testing configurations, making them ideal for evolving testing needs. Other types, including handheld and hybrid analyzers, collectively account for nearly 20% of the market, serving niche applications such as maintenance and low-frequency testing.

• In 2025, a leading semiconductor testing facility implemented modular analyzers to enhance testing efficiency, reducing validation time for RF components by over 25%.

Telecommunications remains the leading application segment, accounting for approximately 45% of total usage due to extensive deployment of 5G networks and increasing demand for high-frequency testing. Semiconductor testing follows with around 27% share, driven by the need for precise validation of RF chips and integrated circuits. Automotive radar applications are the fastest-growing segment, expanding at an estimated rate of 10.5% due to the rapid adoption of ADAS technologies. Other applications, including aerospace & defense and research, collectively contribute about 28% of the market.

In 2025, more than 42% of telecom operators globally reported increased reliance on advanced signal analyzers for network optimization. Additionally, over 58% of semiconductor manufacturers have integrated automated testing systems into their workflows.

• In 2024, a global telecom operator deployed advanced analyzers across 150+ testing sites, improving network performance validation efficiency by 30%.

Telecom operators represent the leading end-user segment, accounting for approximately 40% of total market adoption due to extensive network testing requirements. Semiconductor manufacturers follow with around 30% share, leveraging analyzers for chip validation and quality assurance. Automotive companies are the fastest-growing end-user segment, expanding at an estimated rate of 11.2% as radar and connectivity systems become standard in vehicles. Other end-users, including defense organizations and research institutions, collectively contribute about 30% of the market.

In 2025, over 50% of telecom enterprises reported adopting automated signal testing systems to improve operational efficiency. Additionally, around 45% of research institutions are investing in high-frequency analyzers for advanced experimentation.

• In 2025, a major automotive manufacturer integrated signal analyzers into its radar testing systems, achieving a 27% improvement in detection accuracy.

North America accounted for the largest market share at 38% in 2025 however, Asia-Pacific is expected to register the fastest growth, expanding at a CAGR of 8.5% between 2026 and 2033.

North America’s dominance is supported by strong aerospace and defense investments, with over 70% of testing labs utilizing high-frequency analyzers. Europe follows with approximately 27% share, driven by telecom modernization and regulatory compliance requirements. Asia-Pacific holds around 25% share, with China, Japan, and India leading in electronics manufacturing and telecom expansion. South America and the Middle East & Africa collectively account for nearly 10% of the market, with growing adoption in telecom and infrastructure projects. Increasing investments in 5G networks, semiconductor production, and automotive technologies across regions continue to shape market dynamics and drive demand for advanced signal testing solutions.

North America holds approximately 38% market share, driven by strong demand from aerospace, defense, and telecommunications sectors. The United States leads regional consumption, with over 65% of enterprises in telecom and semiconductor industries utilizing advanced signal analyzers. Government support for 5G deployment and defense modernization programs has accelerated adoption. Technological advancements, including AI-driven testing and mmWave capabilities, are widely integrated across testing environments. A key player in the region focuses on developing high-frequency analyzers exceeding 50 GHz capabilities, supporting next-generation communication systems. Consumer behavior indicates higher enterprise adoption in healthcare and finance sectors, where secure and reliable communication systems are critical.

Europe accounts for approximately 27% market share, with Germany, the UK, and France as key contributors. Regulatory bodies emphasize spectrum efficiency and emissions control, driving demand for advanced testing solutions. Over 55% of telecom operators in Europe have adopted high-frequency analyzers to comply with regulatory standards. The region is also witnessing increased adoption of software-defined instrumentation, improving testing flexibility by 30%. A leading European company is investing in sustainable testing solutions to reduce energy consumption in RF labs. Consumer behavior reflects strong demand for explainable and compliant testing technologies due to stringent regulatory requirements.

Asia-Pacific ranks among the fastest-growing regions, contributing approximately 25% of global demand. China, Japan, and India are the largest consumers, driven by expanding electronics manufacturing and telecom infrastructure. Over 60% of semiconductor production facilities in the region utilize advanced signal analyzers for quality assurance. The region is also a hub for innovation, with increasing investments in 5G and IoT technologies. A regional player is focusing on cost-effective modular analyzers to cater to growing demand. Consumer behavior shows strong adoption driven by mobile applications and e-commerce growth, supporting widespread deployment of wireless technologies.

South America accounts for approximately 6% of the global market, with Brazil and Argentina leading regional adoption. Telecom expansion projects and infrastructure development are key drivers, with over 40% of telecom operators investing in advanced testing solutions. Government initiatives to improve connectivity have increased demand for signal analyzers. A local player is focusing on affordable testing solutions to support small and medium enterprises. Consumer behavior indicates demand tied to media localization and communication services, driving gradual adoption across the region.

The Middle East & Africa region holds around 4% market share, with UAE and South Africa as key growth countries. Demand is driven by oil & gas, telecom, and construction sectors, with over 35% of enterprises investing in digital infrastructure. Technological modernization initiatives are promoting adoption of advanced testing tools. A regional company is focusing on integrating analyzers with smart infrastructure projects. Consumer behavior reflects increasing demand for reliable communication systems, supporting gradual market expansion.

United States – 32% Market share: Signal Source Analyzers Market growth driven by strong aerospace, defense, and semiconductor production capacity.

China – 21% Market share: Signal Source Analyzers Market expansion supported by large-scale electronics manufacturing and telecom infrastructure development.

The Signal Source Analyzers Market is moderately consolidated, with the top five companies collectively holding approximately 58% of the global market share. The competitive environment includes around 20–25 active global and regional players focusing on innovation, product differentiation, and strategic partnerships. Leading companies are investing heavily in research and development, with over 15% of their annual budgets allocated to advanced RF testing technologies. Product innovation, particularly in AI-driven analyzers and software-defined instrumentation, is a key competitive factor. Companies are also forming partnerships with telecom operators and semiconductor manufacturers to expand their market presence. Mergers and acquisitions are increasing, with at least 6 major deals recorded between 2023 and 2025, aimed at strengthening technological capabilities and geographic reach.

Additionally, players are focusing on sustainability, targeting reductions in energy consumption of testing equipment by up to 20%. The market is characterized by high entry barriers due to technological complexity and capital requirements, limiting new entrants while intensifying competition among established players.

Rohde & Schwarz

Anritsu Corporation

Tektronix, Inc.

National Instruments Corporation

Advantest Corporation

Viavi Solutions Inc.

Yokogawa Electric Corporation

Teledyne Technologies Incorporated

B&K Precision Corporation

Rigol Technologies

GW Instek

Stanford Research Systems

Aaronia AG

Technological advancements are significantly shaping the Signal Source Analyzers Market, with a strong focus on improving accuracy, efficiency, and scalability. AI and machine learning integration is enabling advanced signal processing capabilities, improving measurement accuracy by up to 40% and reducing manual intervention by 30%. These technologies allow real-time analysis of complex RF signals, making them essential for 5G and emerging 6G applications.

Another key innovation is the adoption of millimeter-wave (mmWave) testing capabilities, with analyzers now supporting frequencies above 50 GHz. Over 60% of advanced telecom labs have integrated mmWave testing systems to validate high-frequency signals required for next-generation communication networks. Additionally, software-defined instrumentation is gaining traction, offering flexibility and scalability. These systems allow users to upgrade functionalities through software, reducing hardware dependency and improving operational efficiency by 35%.

Automation is also transforming testing environments, with over 50% of enterprises deploying automated analyzers to streamline operations. Automated systems reduce testing time by up to 28% and improve throughput by 33%, making them ideal for high-volume production environments. Cloud-based analytics and remote monitoring are further enhancing capabilities, enabling real-time data access and collaboration across global teams. These technological advancements are positioning signal source analyzers as critical tools in modern communication and electronics industries.

• In December 2025, Keysight Technologies introduced a new FieldFox D-Series handheld analyzer enabling 120 MHz IQ streaming for gap-free signal capture, allowing engineers to capture, stream, and replay RF signals for deeper analysis and faster troubleshooting in complex wireless environments. Source: www.keysight.com

• In February 2025, Keysight Technologies expanded its RF and microwave portfolio by launching compact signal generators, synthesizers, and signal source analyzers, enhancing high-frequency testing capabilities and enabling improved validation across telecom, aerospace, and semiconductor applications.

• In 2025, Rohde & Schwarz launched the FSWX multichannel signal and spectrum analyzer, featuring a novel multi-path architecture with cross-correlation capability and 8 GHz internal bandwidth, enabling advanced RF testing for 5G, satellite, and automotive radar systems.

• In August 2024, Anritsu Corporation’s MP1900A signal integrity analyzer was selected as a Thunderbolt™ 5 receiver verification device, improving receiver measurement flexibility and speed, supporting next-generation high-speed interface validation for advanced computing and connectivity systems.

The Signal Source Analyzers Market Report provides a comprehensive analysis of the industry, covering key segments, technologies, applications, and regional dynamics. The report evaluates multiple product types, including benchtop, portable, and modular analyzers, each with distinct operational capabilities and application areas. It also examines diverse applications such as telecommunications, semiconductor testing, aerospace & defense, automotive radar systems, and research laboratories, highlighting their respective contributions to market demand.

Geographically, the report spans North America, Europe, Asia-Pacific, South America, and the Middle East & Africa, offering detailed insights into regional adoption patterns, infrastructure development, and industry-specific demand drivers. The analysis includes over 20 countries, focusing on key markets such as the United States, China, Germany, Japan, and India.

Technological coverage includes AI-driven signal processing, software-defined instrumentation, mmWave testing, and automated testing systems. The report also explores emerging trends such as cloud-based analytics and real-time monitoring, which are transforming testing environments. Additionally, it addresses industry-specific requirements, including regulatory compliance, spectrum efficiency, and energy optimization.

The report further evaluates end-user industries, including telecom operators, semiconductor manufacturers, automotive companies, and defense organizations, providing insights into adoption rates and usage patterns. It highlights innovation trends, strategic initiatives, and competitive dynamics shaping the market. Overall, the report offers a detailed and structured view of the Signal Source Analyzers Market, enabling decision-makers to identify growth opportunities, assess risks, and develop informed business strategies.

| Report Attribute / Metric | Details |

|---|---|

| Market Revenue (2025) | USD 375.5 Million |

| Market Revenue (2033) | USD 650.0 Million |

| CAGR (2026–2033) | 7.1% |

| Base Year | 2025 |

| Forecast Period | 2026–2033 |

| Historic Period | 2021–2025 |

| Segments Covered |

By Type

By Application

By End-User Insights

|

| Key Report Deliverables | Revenue Forecast; Market Trends; Growth Drivers & Restraints; Technology Insights; Segmentation Analysis; Regional Insights; Competitive Landscape; Regulatory & ESG Overview; Recent Developments |

| Regions Covered | North America; Europe; Asia-Pacific; South America; Middle East & Africa |

| Key Players Analyzed | Keysight Technologies; Rohde & Schwarz; Anritsu Corporation; Tektronix, Inc.; National Instruments Corporation; Advantest Corporation; Viavi Solutions Inc.; Yokogawa Electric Corporation; Teledyne Technologies Incorporated; B&K Precision Corporation; Rigol Technologies; GW Instek; Stanford Research Systems; Aaronia AG |

| Customization & Pricing | Available on Request (10% Customization Free) |