Reports

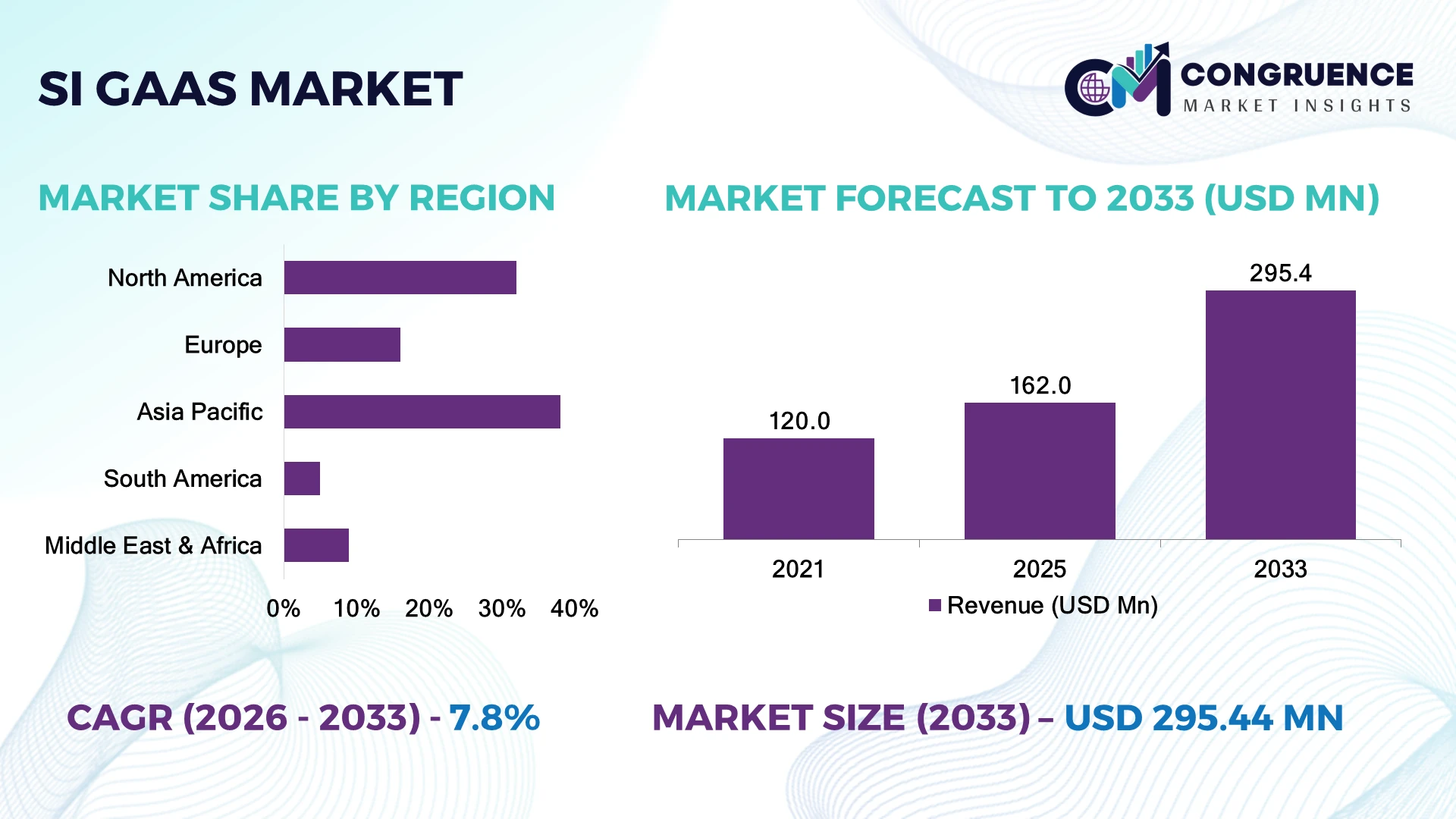

The Global SI GaAs Market was valued at USD 162 Million in 2025 and is anticipated to reach a value of USD 295.4 Million by 2033 expanding at a CAGR of 7.8% between 2026 and 2033. Growth is driven by rising adoption of semi-insulating gallium arsenide substrates in 5G RF components, satellite communications, defense electronics, and high-frequency semiconductor applications requiring superior electron mobility and signal stability.

China dominates the SI GaAs market with an estimated 35%+ share of global production capacity, supported by semiconductor localization programs, expanding RF component manufacturing, and investments exceeding USD 10 billion in compound semiconductor infrastructure. The United States maintains strong leadership in defense, aerospace, and advanced communication applications, while Japan contributes over 20% of high-quality GaAs substrate expertise through precision semiconductor manufacturing. Compared with Europe’s specialized research-driven ecosystem, China’s large-scale fabrication capacity enables faster commercial deployment.

Strategic expansion of domestic supply chains and advanced substrate production capabilities will determine future competitive advantage.

Market Size & Growth: USD 162 Million (2025) to USD 295.4 Million (2033) at 7.8% CAGR, driven by 5G infrastructure and advanced RF semiconductor demand.

Top Growth Drivers: 5G adoption (35%), defense electronics expansion (25%), satellite communication growth (20%).

Short-Term Forecast: By 2028, automated substrate manufacturing improves production efficiency by 15% and reduces defect rates by 10%.

Emerging Technologies: AI-enabled semiconductor design, advanced RF modules, and next-generation compound semiconductor materials accelerate innovation.

Regional Leaders: Asia-Pacific reaches USD 175 Million by 2033 with semiconductor expansion; North America reaches USD 75 Million through defense modernization; Europe reaches USD 45 Million through specialty applications.

Consumer/End-User Trends: More than 60% of new high-frequency communication systems integrate compound semiconductor components for improved performance.

Pilot/Case Example: 2024 semiconductor fabrication upgrades achieved approximately 20% yield improvement through automated inspection and precision processing.

Competitive Landscape: Leading suppliers include Sumitomo Electric, Freiberger Compound Materials, IQE, AXT, and WIN Semiconductors, with top players controlling nearly 50% of specialized substrate supply.

Regulatory & ESG Impact: Semiconductor localization policies reduce supply-chain dependency by 30% while encouraging regional manufacturing resilience.

Investment & Funding: More than USD 15 billion committed globally toward compound semiconductor facilities, partnerships, and capacity expansion programs.

Innovation & Future Outlook: Next-generation SI GaAs platforms are shifting toward integrated RF systems, defense-grade electronics, and advanced connectivity solutions.

SI GaAs materials are gaining importance across 5G base stations, aerospace communication systems, radar technologies, and high-frequency electronic devices due to their superior insulation properties and thermal stability. Recent substrate innovations have improved manufacturing precision, with defect reduction exceeding 15% in advanced production environments. Supply-chain diversification after semiconductor disruptions and increased regional fabrication investments are creating new opportunities for SI GaAs suppliers and technology partners.

The SI GaAs market is becoming strategically important as industries prioritize high-performance semiconductor materials for communication infrastructure, defense systems, and next-generation electronic platforms. Global semiconductor supply-chain restructuring, driven by regional manufacturing policies and technology security initiatives, is accelerating investments in compound semiconductor capacity and localized production networks.

SI GaAs technology provides measurable advantages over traditional silicon solutions in high-frequency applications, delivering approximately 5–10 times higher electron mobility and improved signal performance for RF systems. While Asia-Pacific leads in manufacturing scale and commercial deployment, North America maintains stronger demand from aerospace, defense, and satellite communication sectors, supported by advanced research ecosystems.

Over the next few years, companies are increasing investments in automated fabrication, precision wafer processing, and strategic partnerships to secure supply reliability. For example, RF component manufacturers are integrating SI GaAs substrates into 5G infrastructure equipment to improve transmission efficiency and reduce performance losses in dense networks. The strategic focus is shifting from volume production alone toward quality control, technological differentiation, and resilient semiconductor ecosystems. Companies that strengthen advanced manufacturing capabilities and regional supply partnerships will gain a stronger position in the evolving global compound semiconductor landscape.

The rising deployment of 5G infrastructure, satellite communication, and defense electronics is accelerating SI GaAs adoption due to its superior RF performance and electrical isolation capabilities. More than 60% of advanced RF systems increasingly utilize compound semiconductor materials, while defense and aerospace applications account for a significant share of high-reliability demand. The United States is expanding domestic semiconductor programs to strengthen compound material supply chains, reducing reliance on Asian wafer sources. Companies are responding through wafer fabrication upgrades, strategic partnerships, and process innovation to improve substrate quality, increase production consistency, and secure positions in high-frequency communication markets.

High production costs, limited fabrication infrastructure, and dependence on specialized wafer suppliers restrict SI GaAs market scalability. Manufacturing SI GaAs substrates requires advanced crystal growth capabilities, with fewer than 10 major global suppliers controlling a substantial portion of premium-grade wafer availability. Japan and Germany maintain strong technical capabilities, but supply concentration creates procurement risks during semiconductor shortages. Raw material price fluctuations and specialized equipment requirements can increase production expenses by 15–20% compared with conventional semiconductor materials. Companies are reducing exposure through supplier diversification, long-term procurement agreements, and localized manufacturing investments to improve operational stability and cost control.

Increasing demand for high-frequency connectivity, satellite broadband, and next-generation defense systems is creating new opportunities for SI GaAs suppliers. Satellite communication deployments are expanding rapidly, with commercial space programs increasing investments in RF components by more than 25% in recent years. Emerging applications such as autonomous systems, aerospace electronics, and advanced radar platforms require materials capable of operating at higher frequencies with lower signal loss. Companies are investing in larger wafer formats, automated manufacturing, and R&D partnerships to improve efficiency. The integration of SI GaAs with advanced packaging technologies presents a strategic opportunity to capture demand from high-performance electronic systems.

Scaling SI GaAs manufacturing remains challenging due to complex crystal growth processes, skilled workforce shortages, and integration requirements across semiconductor ecosystems. Production yields for advanced compound semiconductor wafers remain lower than silicon-based alternatives, creating efficiency pressures for manufacturers. More than 30% of semiconductor companies identify supply-chain resilience and technical expertise as key operational priorities. The growing complexity of RF modules and multi-material semiconductor designs requires stronger collaboration between wafer producers, device manufacturers, and system integrators. Companies must address process automation, workforce development, and technology standardization to maintain competitiveness and ensure consistent deployment across communication and defense applications.

RF Communication Expansion SI GaAs adoption is accelerating in 5G base stations, satellite communication, and defense RF systems, with high-frequency applications accounting for more than 60% of new compound semiconductor deployments. The transition toward higher-frequency networks is increasing demand for substrates with superior electron mobility and signal stability. Companies are scaling wafer production, improving fabrication automation, and forming supply partnerships to support faster deployment cycles and advanced communication infrastructure requirements.

Compound Semiconductor Localization Semiconductor supply-chain restructuring is driving investment in domestic SI GaAs production capabilities, particularly across the United States and Japan. More than 25% of recent compound semiconductor expansion initiatives focus on improving regional manufacturing resilience and reducing dependency on concentrated suppliers. Companies are establishing local partnerships, expanding fabrication capacity, and securing long-term material agreements to strengthen operational continuity amid global semiconductor supply pressures.

Wafer Technology Advancement SI GaAs manufacturers are improving substrate performance through larger wafer formats, advanced crystal growth techniques, and automated defect monitoring systems. Production upgrades are targeting 15–20% improvements in manufacturing efficiency while reducing quality variations across high-value applications. Companies are prioritizing process innovation and precision manufacturing to meet increasing requirements from aerospace electronics, radar systems, and high-speed communication devices.

Space And Defense Modernization Aerospace and defense modernization programs are increasing demand for reliable SI GaAs-based RF components, with more than 30% of advanced military communication systems emphasizing high-performance semiconductor materials. Commercial satellite networks are also expanding the need for lightweight, efficient RF solutions. Companies are strengthening aerospace partnerships, developing specialized product portfolios, and increasing investments in radiation-resistant and high-reliability semiconductor technologies.

Semi-insulating SI GaAs wafers represent the leading type segment, accounting for approximately 85% of the market due to their extensive use in RF integrated circuits, microwave devices, and high-frequency communication systems. Their superior electrical isolation, low parasitic capacitance, and stable performance at high frequencies make them essential for telecom infrastructure and defense electronics. Conductive GaAs materials maintain relevance in specialized applications, but their adoption remains limited compared with semi-insulating substrates. High-purity SI GaAs wafers are gaining momentum as manufacturers demand improved device reliability and lower signal losses. The fastest-growing shift is toward advanced-grade SI GaAs substrates with enhanced uniformity and larger wafer dimensions, supported by increasing semiconductor miniaturization trends. More than 20% of new compound semiconductor manufacturing upgrades focus on improving wafer quality and production efficiency. Companies are expanding crystal growth capabilities, investing in automated inspection technologies, and developing customized substrate solutions to strengthen positions in aerospace, satellite, and next-generation communication markets.

RF devices represent the dominant application segment, contributing approximately 70% of SI GaAs demand due to widespread usage in wireless communication infrastructure, radar systems, and satellite electronics. The segment benefits from increasing requirements for high-frequency performance, signal integrity, and thermal stability. Microwave components and optoelectronic applications also contribute to market demand, particularly in specialized industrial and aerospace systems. RF applications remain concentrated among telecom equipment manufacturers and defense technology providers. Satellite communication and advanced radar systems are emerging as the fastest-growing application areas, driven by expanding connectivity requirements and defense modernization programs. More than 30% of new satellite communication platforms incorporate advanced compound semiconductor components to improve transmission efficiency. Companies are adapting through application-specific product development, strategic collaborations, and expanded manufacturing capabilities to address rising demand from commercial space operators and defense contractors.

Telecommunication companies represent the leading end-user segment, accounting for approximately 45% of SI GaAs consumption due to extensive deployment in wireless infrastructure, RF modules, and communication equipment. Defense and aerospace organizations follow closely with around 30% share, supported by demand for reliable high-frequency systems, radar platforms, and secure communication networks. Industrial electronics and research institutions contribute additional demand through specialized applications requiring advanced semiconductor performance. The defense and aerospace segment is emerging as the fastest-growing end-user category as governments increase investments in communication security, satellite capabilities, and advanced electronic warfare systems. Defense technology programs are expanding compound semiconductor usage by more than 20% as performance requirements rise. Companies are responding through customized product development, government partnerships, and dedicated supply agreements to address mission-critical semiconductor requirements.

Asia-Pacific accounted for the largest market share at 38% in 2025 however, North America is expected to register the fastest growth, expanding at a CAGR of 8.4% between 2026 and 2033.

North America holds approximately 32% of the global SI GaAs market, supported by strong demand from aerospace, defense, satellite communication, and advanced wireless infrastructure industries. The United States represents the primary contributor due to its established compound semiconductor ecosystem and government-backed semiconductor localization initiatives. Defense communication programs, radar systems, and commercial satellite networks account for a significant portion of regional deployment. More than 40% of North American SI GaAs demand is linked to high-frequency RF applications, driving manufacturers to expand fabrication capabilities and strengthen domestic supply chains. Companies are increasing investments in specialized wafer production, automation, and strategic partnerships to improve supply security and support next-generation communication systems.

United States Market Outlook: The United States dominates North America's SI GaAs landscape through advanced semiconductor research, defense electronics manufacturing, and aerospace technology leadership. The country contributes nearly 30% of global compound semiconductor innovation activity, with major investments focused on domestic wafer production and secure semiconductor supply chains. Increasing deployment of satellite communication systems and military RF technologies continues to strengthen demand for high-performance SI GaAs substrates.

Europe accounts for approximately 16% of the global SI GaAs market, driven by aerospace electronics, automotive radar systems, and specialized industrial applications. Countries including Germany, France, and the United Kingdom maintain strong compound semiconductor capabilities through research institutions and advanced manufacturing facilities. European semiconductor strategies are encouraging localized production and reducing dependency on external suppliers. More than 20% of regional demand originates from aerospace, defense, and scientific applications requiring reliable high-frequency performance. Companies are expanding partnerships with research organizations and improving wafer processing capabilities to support advanced RF applications while aligning with European technology sovereignty initiatives.

Germany Market Outlook: Germany leads Europe's SI GaAs adoption through advanced industrial electronics, automotive radar development, and precision semiconductor manufacturing expertise. The country has a strong compound semiconductor ecosystem supported by research-driven innovation and industrial automation capabilities. Increasing adoption of radar-based vehicle technologies and high-frequency communication systems is creating additional demand for reliable GaAs-based components.

Asia-Pacific represents the largest SI GaAs market with approximately 38% share, supported by extensive semiconductor manufacturing infrastructure, electronics production capacity, and established wafer fabrication ecosystems. Japan, China, South Korea, and Taiwan contribute significantly to regional production and consumption. Japan maintains strong expertise in high-quality GaAs substrate manufacturing, while Taiwan and South Korea leverage advanced semiconductor supply chains for device integration. More than 50% of global semiconductor manufacturing capacity is concentrated in Asia-Pacific, strengthening the region’s position in compound semiconductor production. Companies are expanding fabrication partnerships, improving wafer output, and investing in advanced material technologies to serve telecom, consumer electronics, and defense-related applications.

Japan Market Outlook: Japan remains a strategically important SI GaAs market due to its advanced material science capabilities and strong wafer manufacturing base. The country contributes a significant portion of global high-purity GaAs substrate production, with more than 25% of its compound semiconductor activity focused on RF and communication applications. Japanese manufacturers are increasing automation and precision processing investments to maintain leadership in premium semiconductor materials.

South America accounts for approximately 5% of the global SI GaAs market, with demand concentrated in telecommunications infrastructure, satellite connectivity, and defense communication applications. Brazil represents the largest contributor due to its expanding digital infrastructure programs and aerospace capabilities. Regional adoption remains limited by semiconductor manufacturing constraints and dependence on imported advanced materials. However, satellite connectivity initiatives and modernization of communication networks are increasing interest in high-performance RF components. More than 15% of new regional telecom investments involve advanced connectivity upgrades, creating opportunities for SI GaAs suppliers. Companies are focusing on distribution partnerships and technology collaborations to improve market access and support deployment growth.

Brazil Market Outlook: Brazil leads South America's SI GaAs demand through telecommunications expansion, satellite communication programs, and aerospace technology development. The country’s growing connectivity initiatives are increasing demand for advanced RF components, particularly in remote communication networks. Local partnerships with international semiconductor suppliers are helping improve access to specialized compound semiconductor technologies.

The Middle East & Africa region contributes approximately 9% of the global SI GaAs market, supported by defense modernization, satellite communication investments, and advanced connectivity infrastructure development. Gulf countries are increasing spending on secure communication systems, aerospace technologies, and smart infrastructure projects. The United Arab Emirates and Saudi Arabia are key markets due to their investments in satellite programs and digital transformation initiatives. More than 20% of regional technology investments are directed toward advanced communication and security infrastructure. Companies are strengthening partnerships with defense contractors, telecom operators, and satellite providers to expand SI GaAs adoption across specialized applications.

United Arab Emirates Market Outlook: The United Arab Emirates is emerging as a strategic SI GaAs market through satellite technology investments, aerospace initiatives, and advanced communication infrastructure development. The country’s space programs and defense modernization efforts are increasing demand for reliable RF semiconductor components. Growing collaboration with global technology companies is supporting adoption of advanced compound semiconductor solutions across critical applications.

The SI GaAs market features competition between global wafer suppliers such as Sumitomo Electric, Freiberger Compound Materials, IQE, and AXT against specialized regional producers and compound semiconductor innovators. Top five players collectively control approximately 55% of supply, creating a moderately consolidated structure. Competition is driven by substrate quality, manufacturing consistency, pricing, and supply reliability, with premium wafer producers achieving 15–20% performance advantages through advanced crystal growth technologies. Companies compete through fabrication expansion, strategic partnerships, process automation, and vertical integration of material production. Japanese and U.S. suppliers lead high-quality substrate development, while cost-focused Asian manufacturers strengthen volume capabilities. The market is shifting toward supply-chain control and customized wafer solutions as telecom, aerospace, and defense customers demand higher reliability. High capital requirements, technical expertise, and limited manufacturing infrastructure create strong entry barriers. Winning requires superior wafer performance, dependable supply networks, and application-specific innovation.

Freiberger Compound Materials

IQE plc

AXT Inc.

Wafer Technology Ltd.

China Crystal Technologies

Vital Materials Co., Ltd.

Yunnan Germanium Co., Ltd.

Semiconductor Wafer Inc.

MTI Corporation

Galaxy Compound Semiconductors

IntelliEPI Inc.

SI GaAs technology is advancing through improved wafer manufacturing, automated inspection, and high-purity substrate processing. Advanced crystal growth techniques are improving wafer uniformity by approximately 15%, enabling stronger performance in RF devices and satellite systems. Automation adoption across semiconductor facilities is increasing process efficiency by nearly 20%, giving manufacturers better yield control and production consistency.

The shift from traditional semiconductor materials toward compound semiconductor platforms is accelerating as high-frequency applications demand superior mobility and thermal performance. Compared with conventional silicon-based RF solutions, SI GaAs delivers approximately 30% higher efficiency in selected high-frequency applications. Telecom equipment providers, defense manufacturers, and satellite companies benefit from improved signal integrity and reduced power losses.

Between 2026 and 2028, integration of AI-driven manufacturing analytics, advanced packaging, and larger wafer formats will reshape competitive positioning. Companies investing in smart fabrication systems and customized substrate solutions will gain advantages through faster production cycles, improved reliability, and stronger partnerships across aerospace, communication, and defense ecosystems.

January 2025 IQE plc secured $5.8 million in customer commitments for compound semiconductor wafer products, including advanced epitaxial wafers and substrates for sensing applications. The agreements support aerospace, industrial, and security markets while strengthening IQE’s position in specialized compound semiconductor supply chains. Source: www.iqep.com

April 2025 IQE plc partnered with X-FAB to develop a scalable GaN power device platform using advanced compound semiconductor expertise. The two-year collaboration targets 650V GaN technology for automotive, data center, and consumer applications, improving access to optimized semiconductor manufacturing solutions. Source: www.iqep.com

July 2025 AXT Inc. reported improved operational efficiency while addressing supply-chain constraints affecting gallium arsenide export processing. The company highlighted recovery in manufacturing performance and continued development of compound semiconductor substrates supporting 5G infrastructure, wireless devices, and satellite applications. Source: www.investors.axt.com

October 2025 Sumitomo Electric Industries showcased GaAs substrates among its advanced semiconductor and optical technology portfolio at the China International Import Expo, highlighting continued global commercialization efforts for compound semiconductor materials. The company presented GaAs substrate technologies alongside data-center and communication solutions.

The SI GaAs market report provides comprehensive coverage of semi-insulating gallium arsenide technologies across wafer types, RF devices, satellite communication systems, aerospace applications, defense electronics, and industrial semiconductor uses. The analysis evaluates leading market segments, adoption patterns, manufacturing capabilities, and competitive positioning across North America, Europe, Asia-Pacific, South America, and Middle East & Africa.

The report examines technology advancements, supply-chain developments, production strategies, and investment priorities shaping the market from 2026 to 2033. It covers established suppliers, emerging manufacturers, and niche application opportunities while highlighting deployment trends, customization requirements, and strategic expansion opportunities. The study supports companies and investors in identifying growth areas, evaluating competitive advantages, and developing informed strategies for semiconductor ecosystem participation.

| Report Attribute / Metric | Details |

|---|---|

| Market Revenue (2025) | USD 162.0 Million |

| Market Revenue (2033) | USD 295.4 Million |

| CAGR (2026–2033) | 7.8% |

| Base Year | 2025 |

| Forecast Period | 2026–2033 |

| Historic Period | 2021–2025 |

| Segments Covered |

By Type

By Application

By End-User

|

| Key Deliverables | Revenue Forecast; Market Trends; Growth Drivers & Restraints; Technology Insights; Segmentation Analysis; Regional Insights; Competitive Landscape; Regulatory & ESG Overview; Recent Developments |

| Regions Covered | North America; Europe; Asia-Pacific; South America; Middle East & Africa |

| Companies Profiled | Sumitomo Electric Industries; Freiberger Compound Materials; IQE plc; AXT Inc.; Wafer Technology Ltd.; China Crystal Technologies; Vital Materials Co., Ltd.; Yunnan Germanium Co., Ltd.; Semiconductor Wafer Inc.; MTI Corporation; Galaxy Compound Semiconductors; IntelliEPI Inc. |

| Customization & Pricing | Available on Request (10% Customization Free) |