Reports

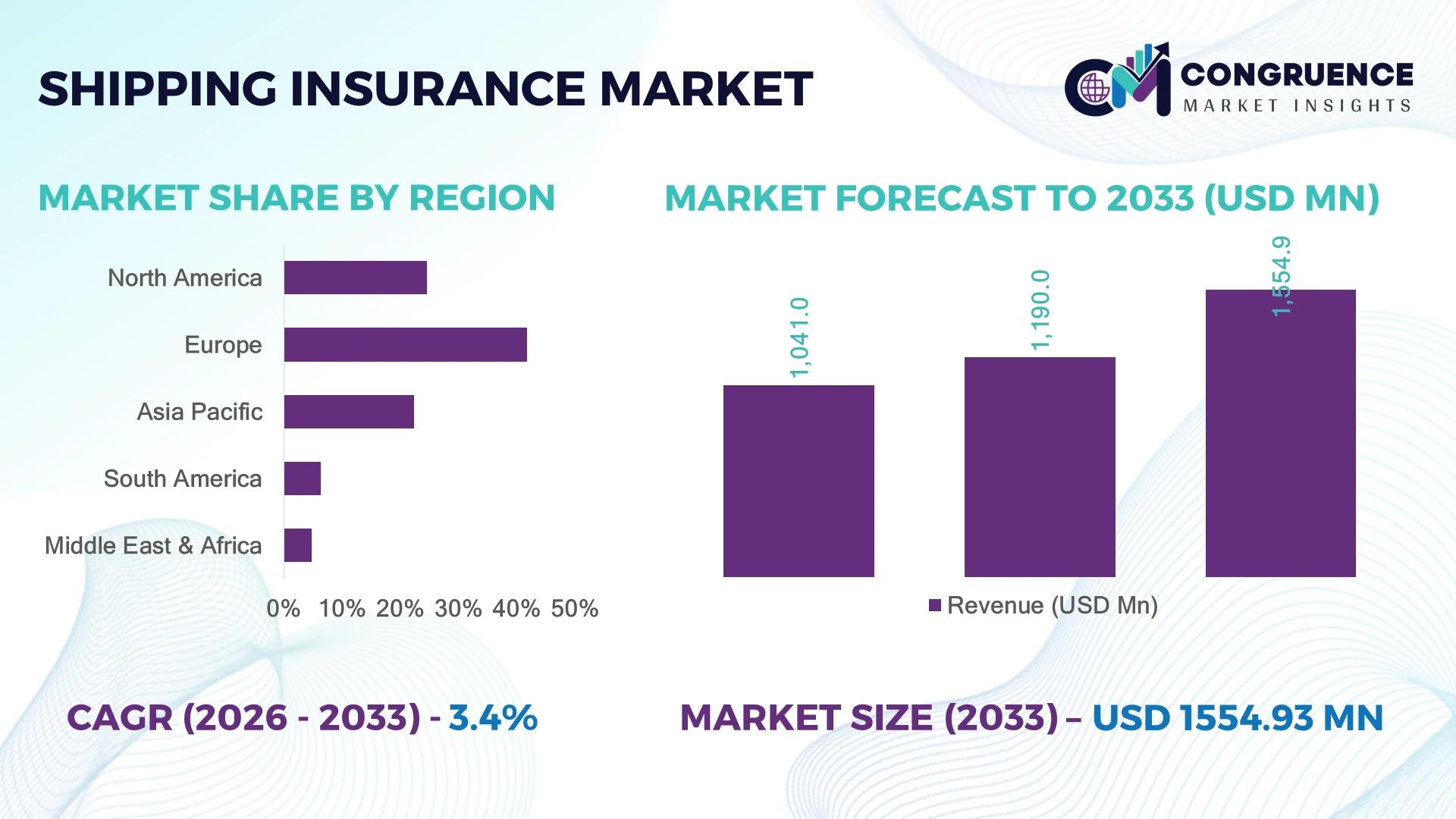

The Global Shipping Insurance Market was valued at USD 1,190.0 Million in 2025 and is anticipated to reach a value of USD 1,554.9 Million by 2033 expanding at a CAGR of 3.4% between 2026 and 2033. Growth is driven by rising maritime trade volumes, increasing cargo-value exposure, digital underwriting platforms, and stricter international marine risk compliance requirements.

The United Kingdom remains a dominant force, accounting for approximately 35% of the global marine insurance market through London's established underwriting ecosystem, while Singapore has expanded its regional marine insurance capacity by over 20% through maritime finance initiatives and digital claims processing. The continued implementation of IMO decarbonization regulations is accelerating specialized insurance products for alternative-fuel vessels, reinforcing the UK's leadership while Asia strengthens regional risk management capabilities.

This market landscape encourages insurers to prioritize digital risk analytics, regional underwriting expansion, and specialized maritime coverage portfolios.

Market Size & Growth: USD 1,190.0 Million (2025) expected to reach USD 1,554.9 Million (2033) at 3.4% CAGR, supported by advanced digital underwriting and expanding global shipping activity.

Top Growth Drivers: Cargo trade expansion (+6%), digital claims automation (40% faster processing), and cyber-risk coverage adoption (30% increase).

Short-Term Forecast: By 2028, AI-enabled underwriting is projected to reduce policy processing time by nearly 35%, improving operational efficiency.

Emerging Technologies: AI-powered risk assessment, satellite vessel monitoring, and blockchain documentation are reducing fraud while improving underwriting accuracy by over 25%.

Regional Leaders: Europe (~USD 500 Million), Asia-Pacific (~USD 370 Million), and North America (~USD 220 Million) lead through digital marine insurance adoption and expanding maritime trade corridors.

Consumer/End-User Trends: More than 55% of large shipping operators now prefer integrated cargo, cyber, and liability insurance packages under unified digital platforms.

Pilot/Case Example: In 2024, digital marine claims automation initiatives reduced average claims settlement time by approximately 40% across selected commercial fleets.

Competitive Landscape: The leading insurer holds roughly 12% market share, with Allianz Commercial, AXA XL, Chubb, Zurich Insurance Group, and Gard remaining major global participants.

Regulatory & ESG Impact: IMO environmental regulations have increased demand for specialized vessel compliance insurance by nearly 22%, particularly across international shipping routes.

Investment & Funding: More than USD 1.3 Billion has been directed toward InsurTech partnerships, AI underwriting platforms, and maritime digitalization supporting resilient global supply chains.

Innovation & Future Outlook: Predictive analytics, embedded marine insurance, and automated risk intelligence are strengthening underwriting precision while supporting regional expansion strategies.

The Shipping Insurance Market is evolving through increasing demand for cyber-risk protection, environmental liability coverage, and AI-driven underwriting platforms that improve policy accuracy and claims management. Digital documentation and predictive vessel analytics have improved underwriting efficiency by nearly 25%, while expanding cross-border shipping operations and evolving maritime compliance requirements continue to reshape insurer product portfolios and create opportunities for specialized risk solutions, setting the stage for broader strategic transformation.

Shipping insurance has become increasingly strategic as maritime trade networks expand and cargo values continue to rise across global logistics corridors. Digital transformation, supply-chain restructuring, and evolving international maritime regulations are encouraging insurers to redesign underwriting models while improving operational resilience. Companies are shifting from conventional policy administration toward data-driven risk assessment to strengthen competitiveness and improve portfolio performance.

Modern AI-enabled underwriting platforms evaluate vessel performance, weather exposure, and cargo risks significantly faster than traditional manual assessment, reducing policy processing times by approximately 35% while improving underwriting consistency. Europe continues to lead through mature marine insurance expertise and established regulatory frameworks, whereas Asia-Pacific is advancing through rapid port modernization, digital shipping ecosystems, and expanding international trade routes. Over the next two to three years, automated claims management and predictive maritime analytics are expected to become standard capabilities across major commercial insurers.

Leading insurers are deploying cloud-based marine insurance platforms, expanding regional partnerships, and integrating satellite-based vessel monitoring into risk evaluation workflows. For example, insurers supporting container shipping operators increasingly combine real-time voyage intelligence with automated claims validation to improve customer response and operational transparency. Organizations that strengthen digital capabilities, specialized underwriting expertise, and global partnership networks will establish stronger competitive positioning and long-term relevance within the evolving shipping insurance ecosystem.

The increasing complexity of global shipping operations is accelerating demand for advanced marine insurance supported by AI-driven underwriting, predictive analytics, and real-time vessel monitoring. More than 60% of leading commercial insurers now integrate digital risk assessment into underwriting workflows, while automated claims platforms have reduced settlement times by nearly 40%. The implementation of IMO environmental regulations has also expanded demand for specialized coverage for alternative-fuel vessels and environmental liabilities. This combination of regulatory evolution and operational digitalization enables insurers to improve pricing accuracy and reduce fraud. In response, insurers in the United Kingdom and Singapore are investing in InsurTech partnerships, satellite-data integration, and digital policy platforms to strengthen underwriting precision and differentiate high-value commercial marine offerings.

Rising climate-related losses, geopolitical disruptions, and volatile reinsurance costs continue to pressure underwriting profitability across shipping insurance portfolios. Marine catastrophe claims have increased by approximately 20% over recent years, while reinsurance premiums for high-risk shipping routes have risen by nearly 15%. Ongoing security concerns affecting the Red Sea shipping corridor have further elevated war-risk premiums and operational uncertainty for cargo operators. These structural pressures reduce pricing stability, complicate policy renewals, and increase capital requirements for insurers. To mitigate exposure, companies are expanding geographic diversification, strengthening catastrophe modeling capabilities, negotiating long-term reinsurance agreements, and refining vessel-specific underwriting standards to maintain portfolio resilience.

Digital ecosystems are creating new opportunities beyond traditional marine coverage through embedded insurance, predictive voyage analytics, and automated cargo-risk assessment. AI-supported underwriting has improved risk prediction accuracy by nearly 30%, while blockchain-enabled documentation can reduce claims verification time by over 35%. Singapore's Smart Port initiatives are encouraging wider adoption of connected maritime platforms capable of integrating insurance services directly into shipping operations. Insurers are responding by expanding digital partnerships with logistics providers, investing in cloud-native policy administration systems, and developing parametric marine insurance products for weather and supply-chain disruptions. These innovations create operational efficiencies while opening previously underserved customer segments across international maritime trade networks.

Long-term competitiveness depends on integrating fragmented shipping, logistics, weather, and vessel-performance data into unified underwriting environments. Nearly 45% of marine insurers continue to operate on legacy policy administration platforms, while cyber incidents targeting maritime infrastructure have increased by approximately 25% as vessel connectivity expands. The growing digitization of global fleets creates additional cybersecurity and interoperability challenges, particularly for multinational insurers managing cross-border regulatory requirements. Organizations must modernize core insurance platforms, strengthen cyber resilience, and develop standardized data-sharing frameworks through technology partnerships and infrastructure investments. Firms that successfully integrate real-time operational intelligence into underwriting processes will achieve superior risk selection, faster decision-making, and stronger long-term competitive positioning.

AI-Driven Underwriting Expansion Commercial marine insurers are rapidly deploying AI-enabled underwriting engines, with digital risk assessment adoption exceeding 60% among large international insurers and policy processing times declining by nearly 35%. Continuous vessel telemetry, weather intelligence, and cargo analytics now support dynamic premium calculations instead of periodic evaluations. Following increased maritime disruption after Red Sea shipping rerouting, insurers are expanding partnerships with maritime data providers and InsurTech firms to improve underwriting precision while reducing manual intervention.

Cyber Risk Coverage Evolution Growing digitalization across vessels and port infrastructure has increased demand for dedicated marine cyber insurance, with cyber-related endorsements rising by approximately 30% since 2023 and connected vessel deployments surpassing 55% among major fleets. As autonomous navigation and smart shipping platforms expand, insurers are restructuring policy frameworks to include cyber resilience, operational technology protection, and digital incident response through specialized underwriting teams and technology collaborations.

Parametric Insurance Adoption Parametric marine insurance is gaining traction as shipping operators seek faster claim settlements for weather-related disruptions. Trigger-based policies reduce claim processing time by nearly 40%, while satellite monitoring improves event verification accuracy by over 25%. The growing frequency of climate-related shipping disruptions is encouraging insurers in the United Kingdom and Singapore to scale automated payout models, strengthening customer retention and improving operational efficiency across global trade corridors.

Integrated Digital Claims Platforms Marine insurers are replacing fragmented claims administration with cloud-native digital ecosystems that combine blockchain documentation, electronic bills of lading, and automated verification. Digital claim submissions now account for approximately 65% of commercial marine policies, reducing administrative costs by nearly 20%. Shipping companies increasingly expect end-to-end digital servicing, prompting insurers to modernize legacy platforms, integrate logistics partners, and standardize claims workflows to enhance customer experience and portfolio scalability.

Cargo Insurance remains the leading segment, accounting for approximately 42% of total market demand owing to its broad applicability across international trade, containerized freight, and multimodal logistics. Rising cargo values, increasing cross-border commerce, and expanding e-commerce exports continue to strengthen demand for comprehensive cargo protection. Liability Insurance is emerging as the fastest-growing segment as environmental compliance, cyber exposure, and contractual obligations become more complex for global shipping operators. Insurers are responding by expanding integrated policies that combine cargo, liability, and digital risk coverage within unified commercial packages. Hull Insurance continues to represent a mature segment due to the large installed base of commercial vessels requiring annual protection against physical damage. Freight Insurance is witnessing stable adoption among exporters seeking protection against financial losses resulting from cargo delays or transport interruptions, while Other Marine Insurance products—including offshore energy and specialty marine risks—are expanding through customized underwriting solutions. Approximately 58% of insurers now offer modular marine insurance products, while nearly 35% have introduced AI-supported underwriting capabilities to improve pricing accuracy and portfolio diversification.

Fleet Managers and Shipping Operators represent the largest application segment, accounting for approximately 48% of overall policy demand due to continuous vessel operations, regulatory compliance obligations, and enterprise-wide risk management requirements. Large commercial fleets increasingly purchase integrated marine insurance programs covering hull, cargo, liability, and cyber risks under unified contracts, reducing administrative complexity and improving policy consistency. Consignee insurance is emerging as the fastest-growing application as importers seek greater protection against supply-chain disruptions, cargo delays, and geopolitical shipping risks. More than 45% of multinational importers now require enhanced marine coverage within procurement contracts, encouraging insurers to introduce flexible and digital-first policy structures. Consignor applications remain strategically important, particularly for exporters of high-value manufactured goods, pharmaceuticals, and electronics requiring comprehensive transit protection. Companies are deploying automated policy issuance, electronic documentation, and AI-assisted claims processing to improve operational efficiency and customer experience. Nearly 38% of commercial marine insurers have expanded digital application platforms, while approximately 30% have integrated logistics visibility tools into underwriting workflows. This evolution is shifting marine insurance from a transactional service toward an embedded risk-management solution across global supply chains.

Shipping Companies remain the dominant end-user segment, representing nearly 46% of total insurance demand due to extensive vessel ownership, international operations, and continuous exposure to operational, environmental, and contractual risks. Fleet modernization, digital navigation systems, and expanding compliance requirements have increased demand for comprehensive insurance portfolios covering multiple risk categories. Freight Forwarders and Logistics Providers are the fastest-growing end-user group as integrated logistics services expand and businesses seek end-to-end cargo protection. Around 34% of logistics companies have strengthened insurance partnerships to improve shipment visibility and reduce claims-related disruptions. Cargo Owners continue to increase insurance adoption for high-value commodities, temperature-sensitive products, and cross-border manufacturing supply chains, particularly in countries such as China and Germany, where export-oriented industries require robust marine risk protection. Port Operators are also investing in specialized liability and infrastructure-related insurance as automation and smart-port technologies become more widespread. Insurers are responding with customized pricing models, ecosystem partnerships, and digital policy management platforms that support enterprise customers with scalable, data-driven marine risk solutions while improving customer retention and underwriting performance.

Europe accounted for the largest market share at 41.8% in 2025 however, Asia-Pacific is expected to register the fastest growth, expanding at a CAGR of 4.3% between 2026 and 2033.

North America accounted for approximately 24.6% of the global Shipping Insurance Market in 2025, supported by extensive maritime trade, sophisticated insurance infrastructure, and rapid adoption of digital underwriting technologies. Large commercial insurers continue integrating AI-driven risk assessment, satellite vessel monitoring, and automated claims management to improve underwriting efficiency. More than 65% of marine insurance policies for large fleets are now processed through digital platforms. Increased investment in cyber-risk protection and supply-chain resilience following disruptions across global shipping routes has accelerated product innovation. Strategic collaborations between insurers, logistics companies, and maritime technology providers are further enhancing operational transparency and portfolio diversification.

United States Market Outlook: The United States remains the regional leader due to its extensive commercial shipping activity, established insurance ecosystem, and advanced maritime technology adoption. Major ports including Los Angeles, Houston, and New York continue driving demand for cargo, liability, and hull insurance. More than 70% of leading marine insurers operating in the country have expanded AI-supported underwriting capabilities while increasing investments in cyber-risk protection and digital claims automation, enabling stronger operational resilience for commercial shipping enterprises.

Europe leads the global Shipping Insurance Market with approximately 41.8% market share, supported by London's established marine insurance ecosystem, mature maritime legal frameworks, and advanced underwriting expertise. The implementation of IMO environmental standards and stricter sustainability regulations is increasing demand for specialized insurance covering alternative-fuel vessels, environmental liabilities, and operational compliance. More than 60% of large European marine insurers have adopted predictive analytics within underwriting operations. Ongoing investment in digital documentation, electronic bills of lading, and automated claims platforms is improving operational efficiency while strengthening Europe's position as the global center for marine insurance innovation.

United Kingdom Market Outlook: The United Kingdom remains the most influential national market owing to London's concentration of marine insurers, brokers, reinsurers, and maritime legal specialists. The country accounts for roughly 35% of global marine insurance premium placement through the London market. Continuous investment in AI-based underwriting, marine cyber insurance, and international reinsurance partnerships enables insurers to manage increasingly complex global shipping risks while maintaining leadership in specialty marine insurance products.

Asia-Pacific represents approximately 22.4% of the global Shipping Insurance Market and continues strengthening its position through expanding maritime trade, large-scale port modernization, and rapid digital transformation. Growing container throughput, increasing regional exports, and government-backed smart-port initiatives are encouraging insurers to introduce integrated marine insurance platforms. Nearly 58% of newly issued commercial shipping policies across major regional markets now incorporate digital documentation and automated claims workflows. Investment in logistics infrastructure and connected shipping ecosystems continues improving underwriting accuracy while expanding insurance penetration among regional shipping operators.

Singapore Market Outlook: Singapore serves as the region's leading marine insurance hub due to its world-class port infrastructure, maritime financial services, and favorable regulatory environment. The country has expanded maritime digitalization initiatives by more than 20% over recent years through Smart Port programs and integrated shipping platforms. Insurers continue partnering with logistics technology firms and maritime analytics providers to deliver faster underwriting decisions, advanced voyage risk assessment, and highly efficient digital claims management.

South America accounts for approximately 6.4% of the global Shipping Insurance Market, with demand supported by expanding agricultural exports, mining shipments, and containerized trade. Marine insurers are increasing policy customization for commodity exporters facing growing weather-related and geopolitical transportation risks. Infrastructure modernization across key ports has improved cargo handling efficiency by nearly 15%, although uneven logistics networks continue affecting operational consistency. Companies are strengthening regional partnerships, introducing digital policy management systems, and expanding cargo insurance offerings to improve service accessibility while supporting export-oriented industries.

Brazil Market Outlook: Brazil dominates the regional market through its extensive agricultural exports, mining industry, and large commercial port network. Santos Port and other major logistics hubs continue generating substantial demand for cargo and liability insurance. Commercial insurers are expanding digital underwriting capabilities while introducing specialized insurance products for grain, mineral, and energy exports, supporting improved risk management across international shipping operations and strengthening insurer participation within Brazil's export economy.

The Middle East & Africa contributes approximately 4.8% of the global Shipping Insurance Market, supported by strategic shipping corridors, expanding port infrastructure, and growing maritime investment. Modernization projects across major logistics hubs are increasing demand for specialized marine insurance covering energy cargoes, container shipping, and offshore operations. More than 30% of new marine infrastructure developments in Gulf countries now incorporate digital logistics and vessel management systems, encouraging insurers to deploy technology-enabled underwriting and automated claims capabilities. Cross-border trade diversification is also creating new opportunities for specialized commercial marine insurance solutions.

United Arab Emirates Market Outlook: The United Arab Emirates remains the region's leading market owing to Jebel Ali Port, its advanced logistics ecosystem, and strong maritime financial services sector. Continuous investment in free zones, smart-port technologies, and international shipping connectivity has strengthened demand for integrated marine insurance products. Insurers are increasingly establishing regional underwriting centers and technology partnerships in the UAE to support high-value cargo movements, offshore energy operations, and expanding global trade connectivity.

The Shipping Insurance Market is led by Allianz Commercial, AXA XL, Chubb, Zurich Insurance Group, and Gard, competing directly with regional mutual insurers, Protection & Indemnity (P&I) clubs, and specialist marine underwriters such as Skuld and NorthStandard. The top five players collectively control approximately 48% of the global market, reflecting moderate concentration with strong specialist competition. Rivalry increasingly centers on digital underwriting, cyber-risk coverage, claims speed, and global service capability rather than price alone. AI-enabled underwriting reduces policy processing time by nearly 35%, while automated claims platforms improve settlement efficiency by around 40%. Large insurers are expanding through InsurTech partnerships, embedded marine insurance offerings, and satellite-data integration, whereas regional players compete through customized policies and local regulatory expertise. Consolidation continues as climate risk, geopolitical exposures, and cyber threats reshape underwriting priorities. High capital requirements, regulatory compliance, and global reinsurance access remain significant entry barriers. Sustained success depends on superior risk analytics, digital servicing, global networks, and specialized marine expertise.

AXA XL

Chubb

Zurich Insurance Group

Gard

Tokio Marine Holdings

Sompo Holdings

HDI Global

The American Club

Skuld

NorthStandard

The Swedish Club

Swiss Re

Munich Re

Digital underwriting platforms powered by artificial intelligence, machine learning, and predictive analytics are transforming marine insurance operations. More than 60% of leading marine insurers have integrated AI into underwriting workflows, reducing policy processing times by approximately 35% while improving risk selection accuracy. Real-time vessel tracking through AIS, satellite imagery, and weather intelligence enables continuous risk assessment rather than static annual evaluations, allowing insurers to optimize pricing and portfolio management.

Blockchain-enabled electronic bills of lading, cloud-based claims platforms, and IoT-connected vessel monitoring are replacing paper-intensive legacy processes. Compared with conventional manual claims administration, digital claims ecosystems shorten settlement cycles by nearly 40% while reducing administrative costs by about 20%. Large multinational insurers benefit most because integrated technology platforms improve scalability, compliance management, and cross-border policy servicing. Around 55% of commercial fleet customers now prefer insurers offering digital policy administration and automated claims capabilities.

Between 2026 and 2028, generative AI, digital twins for voyage risk modelling, and embedded marine insurance integrated into logistics platforms will become major competitive differentiators. Companies investing early in predictive risk intelligence, cyber-risk analytics, and automated underwriting ecosystems will strengthen customer retention, improve capital efficiency, and respond faster to increasingly complex geopolitical, climate, and supply-chain risks.

May 2025 – Allianz Commercial: Published its Safety and Shipping Review 2025, reporting that global large-vessel losses declined to 27 ships in 2024, over 20% lower than the previous year, while highlighting rising geopolitical risks reshaping marine underwriting priorities. Business impact: stronger focus on war-risk and cyber-risk solutions. Source: www.commercial.allianz.com

January 2024 – AXA XL: Entered an underwriting agreement with U.S. Marine Insurance Group to expand its Inland Marine insurance offering, broadening delegated underwriting capabilities and strengthening distribution across commercial specialty markets. Business impact: improved market reach and product availability.

May 2025 – Government of India: Approved three additional Russian insurers, increasing the total to eight authorized providers of marine P&I cover for vessels entering Indian ports through February 2026. Business impact: maintained insurance continuity for energy imports amid sanctions.

July 2025 – AXA XL: Expanded industry engagement around next-generation marine insurance by promoting risk solutions supporting decarbonization, alternative-fuel vessels, and sustainable shipping operations. Business impact: accelerated development of insurance products aligned with maritime energy transition initiatives.

This report provides comprehensive analysis of the Shipping Insurance Market across Cargo Insurance, Hull Insurance, Freight Insurance, Liability Insurance, and Other Marine Insurance segments while evaluating applications including Fleet Managers & Operators, Consignors, and Consignees. It further assesses demand across Shipping Companies, Cargo Owners, Freight Forwarders & Logistics Providers, Port Operators, and other commercial end users throughout North America, Europe, Asia-Pacific, South America, and the Middle East & Africa. The study also examines digital underwriting, AI-enabled risk analytics, blockchain documentation, cyber-risk coverage, and predictive claims technologies influencing operational transformation.

The report evaluates competitive positioning of major global insurers, deployment trends, technology adoption patterns, and regional market dynamics between 2026 and 2033. It highlights segment leadership, enterprise adoption trends, digital insurance penetration, and strategic investment priorities while supporting expansion planning, partnership evaluation, portfolio optimization, risk management, and long-term competitive decision-making for insurers, investors, logistics providers, and maritime stakeholders operating across global shipping ecosystems.

| Report Attribute / Metric | Details |

|---|---|

| Market Revenue (2025) | USD 1,190.0 Million |

| Market Revenue (2033) | USD 1,554.9 Million |

| CAGR (2026–2033) | 3.4% |

| Base Year | 2025 |

| Forecast Period | 2026–2033 |

| Historic Period | 2021–2025 |

| Segments Covered |

By Type

By Application

By End-User

|

| Key Deliverables | Revenue Forecast; Market Trends; Growth Drivers & Restraints; Technology Insights; Segmentation Analysis; Regional Insights; Competitive Landscape; Regulatory & ESG Overview; Recent Developments |

| Regions Covered | North America; Europe; Asia-Pacific; South America; Middle East & Africa |

| Key Players Analyzed | Allianz Commercial; AXA XL; Chubb; Zurich Insurance Group; Gard; Tokio Marine Holdings; Sompo Holdings; HDI Global; The American Club; Skuld; NorthStandard; The Swedish Club; Swiss Re; Munich Re |

| Customization & Pricing | Available on Request (10% Customization Free) |