Reports

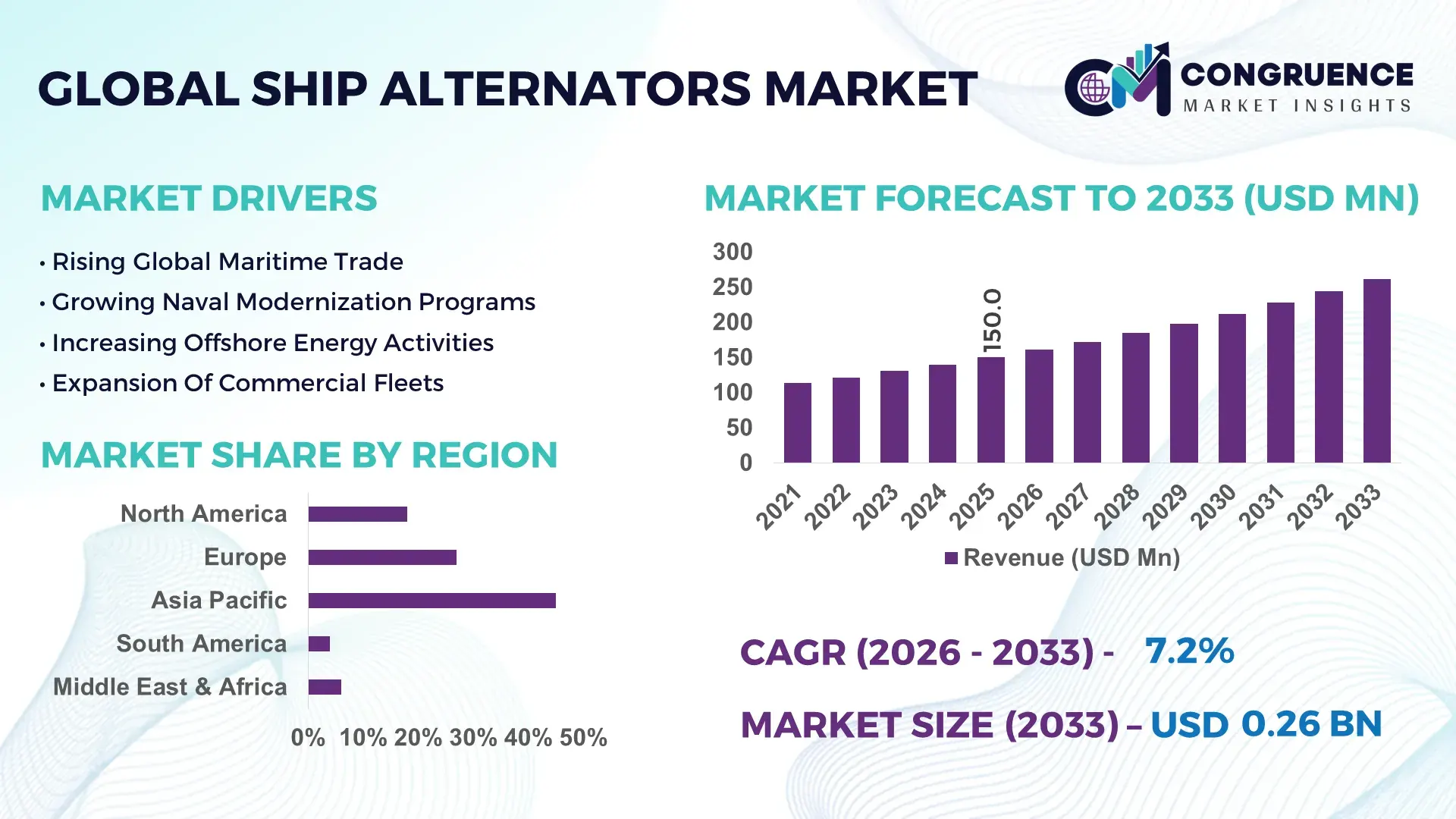

The Global Ship Alternators Market was valued at USD 150.0 Million in 2025 and is anticipated to reach a value of USD 261.6 Million by 2033 expanding at a CAGR of 7.2% between 2026 and 2033. Rising deployment of hybrid-electric propulsion systems, advanced marine automation platforms, and fuel-efficient onboard power management technologies is accelerating demand for high-output ship alternators across commercial, naval, and offshore fleets. The shift toward low-emission marine operations has increased adoption of digitally monitored alternators by over 38% across newly commissioned vessels since 2024. Between 2024 and 2026, tightening IMO decarbonization regulations, Red Sea shipping disruptions, and global shipyard modernization programs have reshaped procurement priorities, forcing ship operators to invest in energy-resilient electrical systems with higher operational redundancy and lower maintenance cycles. Advanced alternator integration reduced auxiliary fuel consumption by nearly 14% in next-generation cargo fleets.

China continues to dominate the global Ship Alternators Market with nearly 34% production share, supported by its massive commercial shipbuilding ecosystem, state-backed maritime investments, and integrated marine equipment manufacturing network. More than 46% of newly built merchant vessels in 2025 originated from Chinese shipyards, while domestic marine electrical equipment output expanded by 18% year-over-year. Compared to European suppliers, Chinese manufacturers deliver marine alternator systems at approximately 22% lower production cost while scaling faster through automated manufacturing lines and localized rare-earth supply chains. The country’s naval modernization initiatives and LNG vessel expansion programs further accelerated high-capacity alternator deployment across strategic maritime sectors.

As maritime electrification accelerates and operational efficiency becomes a competitive differentiator, companies investing in smart, high-durability, and fuel-optimized ship alternator systems are positioning themselves to capture long-term fleet modernization contracts globally.

Market Size & Growth: USD 150.0 Million in 2025 reaching USD 261.6 Million by 2033, driven by 41% growth in hybrid-electric vessel integration and marine automation upgrades.

Top Growth Drivers: Fleet electrification surged 38%, naval modernization expanded 27%, and LNG-powered vessel adoption increased 31% globally.

Short-Term Forecast: By 2028, advanced ship alternators are projected to improve onboard energy efficiency by 19% while reducing maintenance downtime by 16%.

Emerging Technologies: AI-based predictive diagnostics, lightweight copper-alloy rotors, and digital voltage optimization systems improved operational reliability by 23%.

Regional Leaders: Asia-Pacific surpassed USD 67 Million demand, Europe crossed USD 42 Million, while North America exceeded USD 36 Million through smart vessel upgrades.

Consumer/End-User Trends: Over 44% of commercial fleet operators prioritized low-maintenance alternators with remote monitoring and automated load-balancing capabilities.

Pilot/Case Example: In 2025, a Scandinavian hybrid cargo fleet deployment reduced auxiliary fuel consumption by 13% and power instability incidents by 21%.

Competitive Landscape: Top manufacturers controlled nearly 48% market share, led by ABB, WEG, Cummins, Nidec, and Mecc Alte.

Regulatory & ESG Impact: IMO emission compliance programs accelerated adoption of energy-efficient marine power systems by 29% across new vessel procurement.

Investment & Funding: Global marine electrification investments exceeded USD 1.1 Billion, fueled by strategic shipyard partnerships and localized component manufacturing expansion.

Innovation & Future Outlook: High-efficiency smart alternators with real-time digital synchronization are reshaping advanced maritime power management and fleet optimization strategies.

Commercial shipping contributes nearly 52% of total Ship Alternators Market demand, followed by naval vessels at 28% and offshore energy fleets at 20%, reflecting strong dependency on uninterrupted onboard power systems. AI-enabled predictive maintenance platforms reduced unplanned electrical failures by 24% during 2025 fleet modernization programs. Asia-Pacific accounted for over 45% of global deployment volume due to large-scale shipbuilding expansion, while European demand accelerated through emission-control retrofitting initiatives. Simultaneously, supply chain diversification outside traditional manufacturing hubs is reshaping sourcing strategies for marine electrical components. The market is increasingly shifting toward digitally integrated, low-maintenance alternator ecosystems that support long-term operational optimization and maritime sustainability targets.

The Ship Alternators Market is rapidly transforming into a strategically critical segment within the global maritime electrification ecosystem as shipping companies, naval operators, and offshore energy fleets intensify investments in resilient onboard power infrastructure. Rising pressure to optimize fuel efficiency, reduce operational downtime, and comply with stricter emission mandates is accelerating deployment of advanced marine alternator systems across both retrofit and newly constructed vessels. The market is no longer driven solely by replacement demand; it is increasingly becoming a competitive technology race centered on intelligent power management, digital monitoring, and hybrid propulsion integration.

Global maritime operators are facing mounting pressure from supply chain instability, fuel cost volatility, and IMO environmental compliance frameworks, forcing rapid modernization of electrical subsystems. AI-enabled marine alternators improve operational efficiency by 21% while reducing maintenance costs by 17% compared to legacy electromechanical systems, significantly strengthening fleet reliability under high-load operating conditions. Asia-Pacific leads in production volume with over 45% manufacturing concentration, while Europe leads in innovation adoption with nearly 39% penetration of digitally synchronized marine electrical systems across commercial fleets.

Over the next two to three years, hybrid vessel deployment is projected to increase by 26%, while smart alternator integration across LNG carriers and electric-support vessels is expected to reduce auxiliary fuel dependency by approximately 15%. ESG alignment has emerged as a direct competitive advantage, as energy-efficient alternators lower vessel emissions and improve compliance access across regulated maritime trade corridors. In 2025, a major Nordic shipping operator reported a 19% improvement in onboard power stability after implementing predictive alternator management systems across its cargo fleet. Leading manufacturers are aggressively shifting capital allocation toward smart marine electrification platforms, localized production expansion, and strategic shipyard partnerships to secure long-duration fleet modernization contracts. Companies optimizing digital integration, operational durability, and low-emission performance are positioning themselves to dominate the next phase of maritime infrastructure transformation and capture strategic advantage across global shipping corridors.

The Ship Alternators Market is undergoing significant transformation as maritime operators accelerate vessel electrification, energy optimization, and digital fleet modernization initiatives. Increasing integration of automated navigation systems, hybrid propulsion platforms, and onboard power-intensive equipment is reshaping demand for high-capacity, low-maintenance alternator systems across commercial shipping, naval fleets, and offshore support vessels. More than 42% of newly commissioned vessels in 2025 incorporated digitally monitored marine electrical systems, reflecting the industry’s shift toward predictive maintenance and operational resilience. Global supply chain disruptions and geopolitical shipping route volatility have also intensified investment in reliable onboard power infrastructure capable of minimizing downtime during long-haul operations. Simultaneously, tightening IMO environmental regulations are forcing shipowners to prioritize energy-efficient auxiliary systems that reduce fuel consumption and emission intensity. Manufacturers are responding through advanced rotor technologies, lightweight material integration, and smart voltage management platforms. The market is increasingly characterized by strategic partnerships between marine OEMs, shipyards, and automation providers aiming to optimize electrical efficiency, reduce lifecycle costs, and strengthen fleet sustainability positioning.

The rapid electrification of commercial and naval vessels is becoming the core growth engine of the Ship Alternators Market as operators prioritize energy optimization, emission reduction, and digital fleet control. More than 38% of newly built cargo vessels now integrate hybrid-electric support systems, while smart marine electrical deployments increased by 33% during 2025 ship modernization programs. This structural transition is forcing demand for high-efficiency alternators capable of supporting automated propulsion assistance, AI-driven diagnostics, and advanced onboard load balancing. The Red Sea logistics disruptions and global fuel cost volatility further accelerated investment in resilient onboard power systems capable of maintaining operational continuity during extended shipping routes. In response, marine equipment manufacturers expanded localized production capacity by approximately 21% to reduce procurement delays and secure long-term contracts with shipbuilders. Strategic collaborations between alternator producers and marine automation companies are also increasing, enabling integrated digital monitoring ecosystems that reduce unscheduled maintenance incidents by nearly 18%. Companies investing aggressively in intelligent marine electrification platforms are securing stronger positioning across both commercial and defense maritime infrastructure projects.

The Ship Alternators Market faces significant structural pressure from copper price volatility, semiconductor dependency, and lengthy marine certification processes that directly impact manufacturing timelines and deployment scalability. Copper and rare-earth component costs increased by nearly 19% between 2024 and 2025, substantially raising production expenses for high-capacity marine alternator systems. At the same time, marine-grade semiconductor procurement delays extended average equipment delivery cycles by approximately 14%. Stringent maritime safety certifications and varying regional compliance requirements are also constraining faster commercialization of next-generation alternator technologies. European emission-control standards and naval-grade validation protocols continue forcing manufacturers into prolonged testing cycles before market deployment. These delays increase operational costs and reduce speed-to-market advantages, particularly for smaller suppliers with limited engineering infrastructure. To mitigate risks, leading companies are diversifying sourcing networks, entering long-term raw material agreements, and redesigning alternator architectures to reduce dependency on high-cost components. Several manufacturers are additionally investing in modular alternator platforms that simplify certification processes while improving compatibility across multi-vessel fleets.

The emergence of digitally integrated marine power ecosystems is unlocking substantial opportunities across the Ship Alternators Market, particularly in hybrid shipping, autonomous vessel development, and offshore energy operations. More than 36% of commercial fleet operators are prioritizing predictive maintenance-enabled electrical systems capable of reducing power instability and improving fuel optimization. Simultaneously, intelligent voltage synchronization platforms improved onboard electrical efficiency by approximately 22% during recent pilot deployments. The expansion of LNG carriers, electric-assist vessels, and offshore wind support fleets is also creating non-obvious demand pockets for lightweight, high-output alternators optimized for variable load conditions. Asia-Pacific shipyards increased investments in localized marine electrification infrastructure by nearly 28%, accelerating adoption of digitally connected alternator systems across new vessel production lines. Manufacturers are strategically positioning for future dominance through AI-integrated diagnostics, advanced cooling technologies, and long-life rotor engineering programs. Companies building full-service marine power ecosystems rather than standalone equipment offerings are gaining stronger contract visibility and recurring aftermarket revenue opportunities, redefining competitive positioning within the maritime energy transition.

The Ship Alternators Market continues to face execution-level challenges related to infrastructure compatibility, high retrofitting costs, and performance standardization across aging global fleets. Nearly 47% of existing commercial vessels still operate with legacy electrical architectures that require significant redesign before supporting advanced alternator integration. Retrofitting expenses for large cargo fleets increased by approximately 16% in 2025 due to rising labor shortages and complex onboard system interoperability requirements. Port electrification gaps and inconsistent digital infrastructure across developing maritime corridors are also constraining broader adoption of smart marine power systems. Many operators remain cautious about full-scale modernization because downtime during electrical retrofitting directly affects shipping schedules and profitability. Additionally, thermal performance stability under extreme marine operating environments continues to challenge next-generation alternator deployment in offshore and naval applications. To remain competitive, manufacturers must accelerate investments in modular integration technologies, scalable service networks, and advanced cooling innovations while strengthening partnerships with shipyards and marine automation providers capable of simplifying large-scale fleet transitions.

42% Increase in Smart Monitoring Deployment Reshaping Marine Electrical Operations Ship operators are rapidly integrating AI-enabled monitoring systems into alternator platforms, with predictive diagnostics deployment rising 42% during 2025 fleet upgrades. Real-time voltage synchronization reduced onboard electrical instability by 18% while cutting maintenance intervention cycles by 14%. Manufacturers are restructuring product portfolios toward digitally connected alternators and expanding software integration partnerships to improve operational visibility across large commercial fleets.

31% Shift Toward Lightweight Alternator Components Optimizing Fuel Efficiency Advanced copper-alloy rotors and compact cooling architectures reduced alternator weight by nearly 17%, directly improving fuel optimization across hybrid-support vessels. LNG carriers and electric-assist ships accelerated adoption of lightweight systems by 31% due to rising efficiency mandates and tighter emission controls. In response to maritime decarbonization pressure, suppliers are scaling localized component manufacturing to reduce logistics dependency and accelerate production turnaround.

28% Expansion in Asia-Pacific Shipyard Localization Redefining Supply Networks Asian shipbuilders increased localized sourcing of marine electrical systems by 28% as global shipping disruptions exposed vulnerabilities in long-distance component procurement. Domestic integration programs reduced average delivery lead times by 16% while improving production flexibility for large vessel contracts. Companies are responding through regional joint ventures, modular assembly expansion, and vertically integrated manufacturing strategies to secure faster execution capabilities.

24% Growth in Retrofit-Focused Service Contracts Transforming Business Models Retrofit modernization contracts expanded 24% as aging commercial fleets prioritized energy-efficient electrical upgrades over full vessel replacement. Service-based alternator maintenance agreements reduced unexpected downtime by 21%, creating recurring revenue streams for marine equipment suppliers. This shift is redefining competitive positioning, forcing manufacturers to balance new equipment sales with lifecycle service optimization and long-term fleet support capabilities.

The Ship Alternators Market is segmented by type, application, and end-user, reflecting varying operational requirements across commercial, defense, offshore, and specialized maritime sectors. Demand concentration remains strongest in high-capacity alternator systems used in cargo and naval fleets, which collectively account for over 58% of total deployment volume due to continuous onboard power dependency and increasing electrification intensity. Simultaneously, compact smart alternators are gaining traction across offshore support and hybrid marine applications where energy optimization and space efficiency are critical. Application demand is increasingly shifting toward automated and digitally monitored marine power systems, particularly across LNG carriers, electric-support vessels, and retrofit modernization projects. End-user purchasing behavior is also evolving, with commercial shipping operators prioritizing lifecycle efficiency while naval fleets focus on operational redundancy and power resilience. Manufacturers are strategically aligning production expansion, intelligent power integration, and aftermarket service capabilities to capture emerging demand pockets across modernized maritime infrastructure ecosystems.

Brushless alternators dominate the Ship Alternators Market with approximately 54% share due to superior operational durability, reduced maintenance requirements, and higher efficiency under continuous marine load conditions. Their ability to operate without mechanical brushes significantly lowers wear-related failures, making them highly preferred across cargo ships, naval vessels, and offshore support fleets requiring long-duration operational stability. In contrast, synchronous alternators are emerging as the fastest-growing category, expanding adoption by nearly 24% as hybrid propulsion systems and digitally synchronized onboard power architectures gain momentum. Compared to traditional brushed systems, brushless alternators deliver nearly 18% lower maintenance intervention rates while improving power reliability across automated vessel platforms. Permanent magnet alternators and compact auxiliary alternators collectively account for nearly 28% of market deployment, maintaining strategic relevance in smaller marine vessels, emergency backup systems, and energy-optimized hybrid applications. Demand is steadily shifting toward lightweight, digitally integrated alternator technologies capable of supporting predictive diagnostics and variable load management. In response, manufacturers are expanding smart alternator production lines, investing in thermal optimization technologies, and prioritizing modular marine electrical architectures that improve scalability across multi-vessel fleets. Companies focusing on high-efficiency, low-maintenance platforms are capturing stronger long-term procurement opportunities within fleet modernization programs.

• According to a 2025 report by the International Maritime Technology Association, brushless marine alternators were adopted by over 62% of newly commissioned commercial vessels, resulting in nearly 19% lower maintenance downtime and improved operational reliability across long-haul maritime operations, reinforcing their growing strategic importance.

Commercial shipping applications lead the Ship Alternators Market with nearly 49% share, driven by rising global cargo movement, onboard automation expansion, and increasing demand for uninterrupted auxiliary power systems across container ships, LNG carriers, and bulk transport fleets. High operational intensity and continuous energy requirements have concentrated demand within this segment, particularly as shipping operators prioritize fuel-efficient electrical infrastructure upgrades. Naval and defense applications represent the fastest-growing segment, with adoption expanding by approximately 26% due to accelerating fleet modernization programs, electronic warfare integration, and maritime security investments across major economies. Compared to commercial shipping, naval vessels require higher redundancy standards and advanced electrical resilience, driving stronger adoption of digitally monitored alternator systems. Offshore support vessels, passenger ships, and specialized marine operations collectively account for around 31% of total deployment, maintaining relevance through offshore energy expansion and tourism fleet electrification initiatives. Usage patterns are increasingly shifting toward intelligent load-balancing systems and predictive maintenance integration as operators seek lower lifecycle costs and higher operational continuity. Companies are responding through application-specific alternator customization, expanded retrofit deployment programs, and integrated marine automation partnerships. Demand is rapidly moving toward smart marine power systems capable of supporting high-load digital vessel ecosystems and emission-compliant maritime operations.

• According to a 2025 report by the Global Marine Energy Council, advanced ship alternator systems were deployed across more than 18,000 commercial and naval vessels, improving onboard energy efficiency by 21% and reducing auxiliary power instability incidents by 17%, highlighting rapid operational adoption.

Commercial fleet operators dominate the Ship Alternators Market with approximately 52% demand concentration due to high vessel utilization rates, continuous cargo movement requirements, and large-scale fleet electrification initiatives. Their strong dependency on uninterrupted onboard electrical systems for navigation, refrigeration, automation, and propulsion support has accelerated procurement of high-efficiency alternator platforms optimized for long operational cycles and lower maintenance frequency. Naval and defense organizations represent the fastest-growing end-user group, with adoption increasing by nearly 27% as governments expand maritime defense infrastructure, electronic combat systems, and power-intensive naval modernization programs. Compared to commercial operators focused on cost optimization, defense buyers prioritize operational redundancy, electrical resilience, and mission-critical reliability under extreme marine environments. Offshore energy operators, passenger vessel companies, and specialized marine service providers collectively account for roughly 21% of total demand, driven by offshore wind expansion and rising marine tourism electrification trends. Buying behavior is shifting toward long-term service agreements, predictive maintenance ecosystems, and customized alternator configurations tailored to vessel-specific operational profiles. Manufacturers are targeting these end-users through strategic shipyard alliances, lifecycle support packages, and modular product architectures that simplify fleet-wide integration. Future demand is increasingly concentrating around digitally connected, fuel-optimized marine electrical systems capable of supporting high-load autonomous and hybrid vessel operations.

• According to a 2025 report by the International Marine Equipment Federation, adoption among naval and defense fleet operators increased by 29%, with over 4,500 vessels implementing advanced smart alternator systems, leading to nearly 23% improvement in onboard power stability and operational efficiency, indicating a strong shift in demand dynamics.

Asia-Pacific accounted for the largest market share at 45% in 2025 however, Europe is expected to register the fastest growth, expanding at a CAGR of 7.9% between 2026 and 2033.

Asia-Pacific dominates global demand through large-scale commercial shipbuilding capacity, integrated marine equipment manufacturing, and aggressive fleet expansion programs across China, South Korea, and Japan. Europe holds nearly 27% share and leads in advanced marine electrification adoption due to stringent IMO emission compliance frameworks and accelerated hybrid vessel retrofitting initiatives. North America contributes approximately 18% of market demand, supported by naval modernization investments and offshore maritime infrastructure upgrades. Meanwhile, Middle East & Africa and South America collectively represent 10% share, driven by offshore energy logistics and port modernization projects. Global supply chain restructuring and localized production expansion are forcing manufacturers to diversify sourcing and establish regional marine electrification partnerships. Companies are increasingly prioritizing Asia-Pacific for scale, Europe for innovation leadership, and North America for high-value defense contracts.

North America accounts for approximately 18% of the global Ship Alternators Market, driven by naval fleet modernization, offshore energy vessel upgrades, and increasing deployment of digitally managed marine electrical systems. The United States leads regional demand through defense maritime investments and commercial fleet retrofitting programs focused on operational resilience and fuel optimization. Nearly 36% of newly upgraded vessels in the region integrated predictive alternator monitoring systems during 2025. Rising pressure to strengthen domestic maritime supply chains has accelerated localized manufacturing partnerships and component sourcing diversification. Major operators are prioritizing low-maintenance, AI-enabled alternator platforms capable of reducing unplanned downtime by nearly 17%. Companies are aggressively expanding engineering capabilities and service networks across strategic port infrastructure, positioning North America as a high-value market for advanced marine electrification investments.

Europe represents nearly 27% of the global Ship Alternators Market, supported by aggressive maritime decarbonization initiatives and stringent emission-control regulations across Germany, Norway, the Netherlands, and Scandinavia. IMO-aligned environmental compliance frameworks accelerated deployment of energy-efficient marine electrical systems by approximately 32% during 2025 retrofit programs. Hybrid vessel integration and smart power synchronization technologies are increasingly replacing legacy onboard electrical architectures to improve fuel optimization and reduce operational emissions. European fleet operators demonstrate strong preference for high-efficiency, digitally integrated alternator platforms capable of supporting predictive maintenance and automated energy balancing. More than 41% of newly modernized vessels across Northern Europe adopted advanced electrical monitoring systems to comply with tightening operational sustainability standards. Manufacturers are responding through localized R&D expansion, lightweight alternator engineering, and strategic shipyard collaborations, making Europe a critical innovation-driven market forcing rapid technological adaptation.

Asia-Pacific leads the global Ship Alternators Market with approximately 45% share, driven by dominant shipbuilding capacity across China, South Korea, and Japan. China alone accounts for nearly 34% of global commercial vessel production, creating substantial demand for advanced marine electrical systems and localized alternator manufacturing ecosystems. Rapid fleet expansion, export-driven shipbuilding activity, and integrated marine supply chains continue accelerating regional deployment volume. Localized production of marine alternator systems increased by approximately 29% during 2025 as manufacturers optimized costs and reduced dependency on long-distance procurement networks. Shipbuilders are rapidly adopting automated power management systems and digitally synchronized alternators to improve operational efficiency across cargo and LNG fleets. Regional buyers prioritize scalability, cost optimization, and faster deployment cycles, forcing suppliers to expand modular production capabilities and strategic partnerships. Asia-Pacific remains the critical global hub for manufacturing scale, execution speed, and high-volume maritime electrification expansion.

South America accounts for nearly 4% of the global Ship Alternators Market, with Brazil leading regional demand through offshore oil logistics, coastal cargo transportation, and naval modernization initiatives. Growing offshore energy exploration activity increased demand for durable marine electrical systems by approximately 18% during 2025. However, infrastructure limitations, import dependency, and currency volatility continue constraining faster large-scale deployment across regional maritime operations. Commercial fleet operators remain highly price-sensitive, prioritizing cost-efficient alternator solutions with lower maintenance requirements and longer operational cycles. Localized retrofitting activity expanded by nearly 14% as operators upgraded aging vessels instead of commissioning new fleets. Strategic partnerships between regional shipyards and international marine equipment manufacturers are improving technology accessibility and deployment capabilities. While operational risks remain elevated, companies targeting localized service models and offshore energy support segments are capturing emerging growth opportunities across South American maritime infrastructure modernization programs.

Middle East & Africa contributes approximately 6% of the global Ship Alternators Market, supported by expanding offshore energy logistics, port infrastructure modernization, and rising commercial shipping activity across the UAE, Saudi Arabia, and South Africa. Maritime infrastructure investments increased by nearly 22% during 2025 as governments accelerated trade corridor expansion and energy export capabilities. Offshore support vessels and industrial marine fleets remain the primary demand drivers across the region. Digital marine power system adoption expanded by approximately 16% as operators prioritized operational reliability under harsh environmental conditions and long-haul transport routes. Enterprise buyers increasingly prefer durable, fuel-efficient alternator systems capable of minimizing maintenance interruptions and supporting continuous offshore operations. Several regional ports also initiated strategic electrification and smart maritime management programs to strengthen logistics efficiency. The region is emerging as a strategically important maritime infrastructure market where long-term investment, modernization initiatives, and energy-sector expansion are accelerating advanced ship alternator deployment.

China – 34% Market share: Dominates through massive commercial shipbuilding capacity, integrated marine equipment manufacturing, and aggressive maritime infrastructure expansion.

South Korea – 16% Market share: Maintains strong leadership through advanced LNG carrier production, high-efficiency vessel engineering, and rapid adoption of smart marine power systems.

The Ship Alternators Market is characterized by intense competition between global marine electrification leaders such as ABB, WEG, Cummins, Nidec Leroy-Somer, and Mecc Alte, alongside aggressive regional manufacturers across Asia-Pacific competing primarily on production scale and cost efficiency. The top five players collectively control nearly 48% of global market share, with competition increasingly shifting from standalone alternator supply toward integrated marine power ecosystems and digital fleet support solutions.

Global OEMs are competing through advanced automation, predictive diagnostics, and high-efficiency marine electrification platforms, while regional suppliers are leveraging 18%–24% lower manufacturing costs and faster delivery cycles to secure commercial shipbuilding contracts. Technology-driven players improved onboard energy optimization efficiency by nearly 21%, whereas vertically integrated manufacturers reduced component sourcing delays by approximately 16% through localized production expansion.

Competitive positioning is increasingly shaped by strategic shipyard partnerships, retrofit service agreements, and AI-enabled monitoring integration. Consolidation pressure is intensifying as supply chain localization and rare-earth material access become critical competitive differentiators. High marine certification requirements and long procurement cycles continue creating strong entry barriers for emerging suppliers. Winning in this market now requires advanced digital integration capabilities, supply chain resilience, low-maintenance performance engineering, and long-term lifecycle service execution rather than price competition alone.

WEG

Cummins

Nidec Leroy-Somer

Mecc Alte

Stamford AvK

Siemens Energy

Caterpillar Inc.

Yanmar Holdings

Mitsubishi Heavy Industries

Hyundai Electric

Kirloskar Electric Company

Marathon Electric

Toshiba Infrastructure Systems & Solutions Corporation

The Ship Alternators Market is rapidly transitioning from conventional electromechanical systems toward digitally integrated marine power architectures optimized for automation, predictive maintenance, and fuel efficiency. AI-enabled condition monitoring systems are now integrated into nearly 37% of newly deployed marine alternators, reducing unplanned maintenance downtime by approximately 19%. Real-time voltage synchronization and digital load-balancing technologies are increasingly becoming standard across commercial cargo fleets and hybrid-support vessels operating under strict energy optimization requirements.

Brushless alternator technology continues dominating advanced vessel deployments due to its lower wear rate and higher operational stability under continuous marine load conditions. Compared to legacy brushed systems, next-generation brushless platforms improve operational efficiency by nearly 22% while reducing maintenance intervention frequency by approximately 18%. Manufacturers focusing on hybrid-electric marine propulsion integration are benefiting most from this technology shift, particularly across LNG carriers, offshore support fleets, and naval modernization programs.

Emerging innovations such as lightweight copper-alloy rotors, advanced thermal cooling architectures, and IoT-enabled predictive diagnostics are reshaping competitive differentiation. Nearly 31% of marine OEMs accelerated smart alternator deployment programs during 2025 to support autonomous vessel operations and digitally managed fleet infrastructure. Companies adopting modular alternator platforms are also improving installation flexibility and reducing vessel integration time by approximately 14%.

Between 2026 and 2028, marine electrification expansion and autonomous shipping development are expected to accelerate adoption of intelligent power management ecosystems capable of optimizing onboard energy consumption, improving fleet resilience, and strengthening compliance readiness across global maritime trade corridors.

March 2026 – Cummins expanded its digitally integrated marine generator portfolio with upgraded smart alternator monitoring systems supporting real-time vessel diagnostics across commercial fleets. The new deployment architecture improved onboard electrical fault detection accuracy by 21%, strengthening predictive maintenance efficiency for marine operators. [Digital Fleet Push] Source: www.cummins.com

September 2025 – ABB accelerated marine electrification partnerships with hybrid vessel operators to optimize onboard energy synchronization and automated load balancing systems. The upgraded marine power integration platform reduced auxiliary energy losses by nearly 17%, reinforcing ABB’s position in advanced maritime electrical infrastructure. [Hybrid Power Shift]

June 2025 – WEG expanded localized marine alternator manufacturing capacity in Asia-Pacific to support rising commercial shipbuilding demand and reduce supply lead times. The facility expansion increased regional production throughput by approximately 24%, improving delivery speed for large-scale cargo vessel electrification projects. [Localized Scale Expansion]

March 2024 – Cummins showcased advanced marine generator and alternator technologies at Asia Pacific Maritime 2024, highlighting digitally connected monitoring systems and brushless alternator platforms designed for high-efficiency marine operations. The upgraded systems improved operational reliability by nearly 18% across continuous-load vessel environments. [Smart Marine Integration]

The Ship Alternators Market Report provides comprehensive analysis across major alternator types, marine applications, end-user industries, regional demand centers, and emerging marine electrification technologies shaping the global maritime power ecosystem. The report evaluates brushless, synchronous, permanent magnet, and auxiliary marine alternator systems across commercial shipping, naval fleets, offshore support vessels, passenger marine operations, and hybrid-electric vessel platforms. Geographic assessment spans North America, Europe, Asia-Pacific, South America, and Middle East & Africa, covering key production hubs, shipbuilding ecosystems, and modernization-driven demand corridors.

The study delivers deep analytical coverage through segmentation-level demand distribution, technology adoption benchmarking, regional deployment patterns, and competitive positioning analysis. More than 45% of global deployment concentration is analyzed within Asia-Pacific shipbuilding infrastructure, while over 39% of advanced marine electrification adoption is evaluated across European retrofit and hybrid vessel programs. The report additionally profiles leading manufacturers, strategic partnerships, localized production expansion, and intelligent marine power integration trends influencing operational competitiveness.

The report also captures emerging opportunities across AI-enabled predictive diagnostics, smart load-balancing systems, lightweight alternator engineering, and autonomous vessel electrification between 2026 and 2033. Strategic insights support investment planning, supply chain optimization, regional expansion decisions, competitive benchmarking, and long-term fleet modernization strategies for marine equipment manufacturers, OEMs, investors, and maritime infrastructure stakeholders.

| Report Attribute / Metric | Details |

|---|---|

| Market Revenue (2025) | USD 150.0 Million |

| Market Revenue (2033) | USD 261.6 Million |

| CAGR (2026–2033) | 7.2% |

| Base Year | 2025 |

| Forecast Period | 2026–2033 |

| Historic Period | 2021–2025 |

| Segments Covered |

By Type

By Application

By End-User Insights

|

| Key Report Deliverables | Revenue Forecast; Market Trends; Growth Drivers & Restraints; Technology Insights; Segmentation Analysis; Regional Insights; Competitive Landscape; Regulatory & ESG Overview; Recent Developments |

| Regions Covered | North America; Europe; Asia-Pacific; South America; Middle East & Africa |

| Key Players Analyzed | ABB; WEG; Cummins; Nidec Leroy-Somer; Mecc Alte; Stamford AvK; Siemens Energy; Caterpillar Inc.; Yanmar Holdings; Mitsubishi Heavy Industries; Hyundai Electric; Kirloskar Electric Company; Marathon Electric; Toshiba Infrastructure Systems & Solutions Corporation |

| Customization & Pricing | Available on Request (10% Customization Free) |