Reports

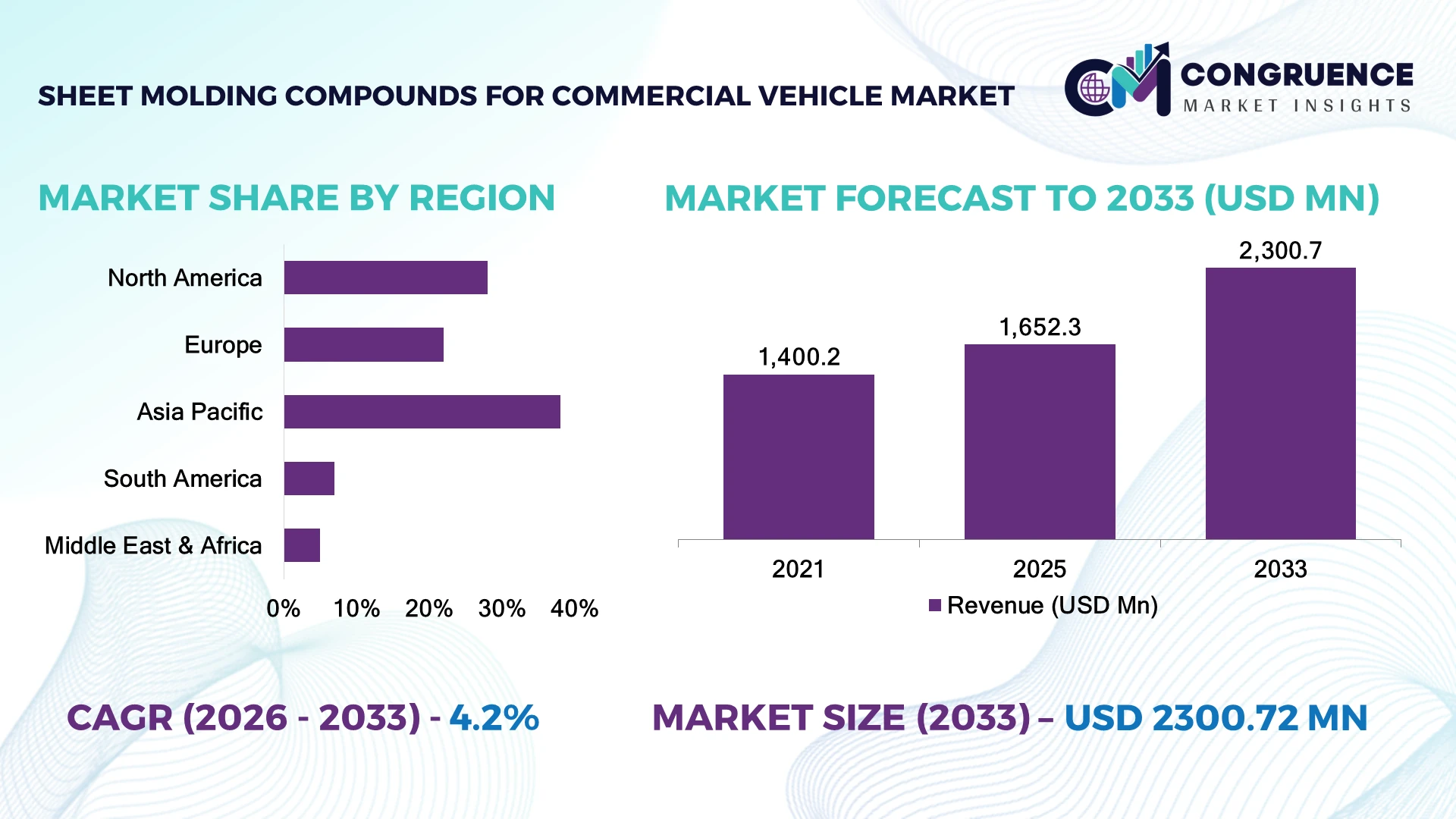

The Global Sheet Molding Compounds For Commercial Vehicle Market was valued at USD 1,652.3 Million in 2025 and is anticipated to reach a value of USD 2,300.7 Million by 2033 expanding at a CAGR of 4.225% between 2026 and 2033. Growth is driven by lightweight composite adoption in commercial vehicles, rising demand for corrosion-resistant body components, and OEM efforts to improve fuel efficiency and electric vehicle range.

China dominates the market with nearly 35% share, supported by large-scale commercial vehicle production, composite manufacturing capacity expansion, and investments under advanced automotive supply-chain programs. The country produces over 3 million commercial vehicles annually, while the U.S. focuses on high-performance composites for fleet electrification and accounts for approximately 25% adoption in advanced vehicle platforms. European manufacturers are accelerating SMC integration due to stringent EU emissions regulations.

Strategic material localization and composite innovation will define future competitive advantage.

Market Size & Growth: USD 1,652.3 Million (2025) to USD 2,300.7 Million (2033) at 4.225% CAGR, driven by lightweight vehicle architecture and composite material substitution.

Top Growth Drivers: Weight reduction demand (35%), electric commercial vehicle adoption (28%), corrosion resistance requirements (22%).

Short-Term Forecast: By 2028, SMC adoption in commercial vehicle body panels increases by 15%, reducing component weight by up to 20%.

Emerging Technologies: Advanced SMC formulations, automated compression molding, AI-based material optimization, and recycled composite development accelerate innovation.

Regional Leaders: Asia Pacific reaches USD 1.1 Billion by 2033 with EV manufacturing expansion; North America reaches USD 650 Million with fleet modernization; Europe reaches USD 450 Million through emissions compliance initiatives.

Consumer/End-User Trends: Over 40% of commercial vehicle manufacturers prioritize lightweight materials to improve operating efficiency and reduce lifecycle costs.

Pilot/Case Example: 2024 composite vehicle programs achieved approximately 18% weight reduction using SMC-based structural components in commercial platforms.

Competitive Landscape: Major suppliers include IDI Composites International, Menzolit, Polynt Group, Core Molding Technologies, and Continental Structural Plastics, with leading players controlling significant regional supply capacity.

Regulatory & ESG Impact: Global vehicle emission policies are increasing composite adoption, with lightweight materials contributing up to 10%–15% efficiency improvement in selected applications.

Investment & Funding: Automotive composite producers are directing billions of dollars toward material innovation, regional manufacturing expansion, and sustainable production processes.

Innovation & Future Outlook: Next-generation SMC solutions focus on recyclable fibers, faster molding cycles, and integrated battery-electric commercial vehicle structures.

Sheet molding compounds for commercial vehicles are gaining importance as manufacturers seek durable, lightweight, and scalable alternatives to conventional metals. Increasing use of carbon and glass fiber-reinforced composites has improved component performance, with advanced formulations supporting more than 30% higher design flexibility compared with traditional materials. Supply-chain localization in Asia and North America is strengthening production reliability, while regulatory pressure on vehicle efficiency continues encouraging composite adoption across fleets.

The Sheet Molding Compounds For Commercial Vehicle Market is becoming strategically important as vehicle manufacturers balance lightweight engineering, operational efficiency, and evolving sustainability targets. Commercial vehicle producers are restructuring supply chains after global disruptions and increasing regional sourcing of composite materials to secure consistent availability and reduce manufacturing risks.

Advanced SMC technologies are replacing traditional metal components through faster production cycles and improved design flexibility. Compared with conventional steel parts, SMC components reduce weight by approximately 15%–25% while lowering corrosion-related maintenance requirements. Automated compression molding systems further improve production efficiency by reducing cycle times by nearly 20%.

Asia Pacific leads in large-scale manufacturing capacity, while North America emphasizes fleet electrification and high-performance composite applications. Europe is advancing adoption through stricter emissions regulations and circular-material initiatives. Companies are expanding partnerships with composite suppliers and investing in localized production facilities to support next-generation commercial vehicles.

Over the next 2–3 years, manufacturers will prioritize recyclable SMC materials, digital manufacturing controls, and integrated lightweight structures. Strategic investments in advanced composites will strengthen competitive positioning by improving vehicle efficiency, reducing lifecycle costs, and supporting long-term transportation transformation.

Commercial vehicle manufacturers are increasing SMC adoption as lightweight engineering becomes central to fuel savings and electric vehicle range optimization. SMC components reduce vehicle part weight by 15%–25% compared with conventional metal alternatives, while improving corrosion resistance by more than 30% in demanding operating environments. In China, expanding electric commercial vehicle production is accelerating composite integration across buses and delivery fleets. Companies are responding through localized manufacturing investments, advanced compression molding partnerships, and development of recyclable SMC formulations. The strategic advantage lies in reducing lifecycle costs while meeting stricter efficiency standards without compromising structural performance.

High dependency on glass fibers, resins, and specialized additives creates cost pressure for SMC manufacturers, particularly during periods of supply-chain instability. Resin and reinforcement material fluctuations can increase production costs by 10%–20%, affecting pricing strategies for commercial vehicle suppliers. European manufacturers face additional pressure from energy-intensive composite processing and evolving environmental compliance requirements. Companies are reducing exposure through supplier diversification, regional sourcing agreements, and long-term material contracts. A key operational limitation remains that smaller suppliers lack the purchasing power and technical infrastructure required to absorb material price swings, slowing broader adoption among cost-sensitive commercial vehicle producers.

Growing demand for recyclable and high-performance composites is creating new opportunities for SMC suppliers across electric trucks, buses, and specialty commercial vehicles. Next-generation SMC materials incorporating recycled fibers and low-emission resins are improving sustainability performance, with manufacturers targeting 20%–30% reductions in material waste through optimized production processes. Japan and Germany are advancing composite innovation through automotive research collaborations focused on circular materials. Companies are increasing R&D spending, forming technology partnerships, and expanding automated molding capabilities to capture emerging applications. A significant opportunity exists in battery-electric commercial vehicles, where lightweight SMC structures support improved payload efficiency and extended operating range.

Scaling SMC production for diverse commercial vehicle platforms requires advanced tooling, process control, and skilled workforce capabilities. Complex component designs can increase tooling investments by 15%–25%, creating barriers for manufacturers serving multiple vehicle segments. In the United States and Germany, suppliers are upgrading digital manufacturing systems to improve consistency and reduce production variation. Companies must solve challenges related to automated quality inspection, material recycling, and platform-specific engineering requirements through technology investments and strategic collaborations. The long-term competitive differentiator will be the ability to integrate smart manufacturing with sustainable composite production while maintaining consistent performance across high-volume commercial vehicle applications.

Recyclable Composite Integration Commercial vehicle manufacturers are increasing the use of recyclable SMC formulations, with recycled fiber adoption rising by nearly 20% in selected automotive applications. Germany and Japan are advancing circular composite programs to reduce material waste by 15%–25%. Companies are restructuring material strategies through partnerships with resin suppliers and investing in low-emission composite technologies to meet sustainability targets.

Automated Molding Expansion Automated compression molding systems are transforming SMC production by improving manufacturing speed by 15%–30% and reducing manual intervention requirements. U.S. and Chinese suppliers are deploying digital process monitoring to enhance quality consistency across high-volume vehicle programs. Companies are expanding smart factory capabilities to reduce defects, optimize tooling utilization, and strengthen supply reliability.

Electric Fleet Material Shift The growth of electric commercial vehicles is accelerating demand for lightweight SMC structures, with manufacturers targeting 10%–20% vehicle weight reductions to improve battery efficiency. Fleet operators in China and Europe are prioritizing composite components for buses and delivery vehicles. Companies are redesigning product portfolios toward EV-compatible body panels, battery covers, and structural components.

Localized Composite Supply Chains Global supply-chain restructuring is encouraging regional SMC production investments, with manufacturers increasing local sourcing by 25%–40% to reduce logistics risks. North American and European suppliers are expanding domestic composite capacity following raw material disruptions. Companies are adopting multi-supplier strategies, regional partnerships, and integrated production networks to improve operational resilience.

Glass Fiber Sheet Molding Compounds represent the leading type segment, accounting for approximately 70%–75% of commercial vehicle SMC applications due to their cost efficiency, high strength-to-weight ratio, and compatibility with large-scale compression molding. The segment remains dominant in truck body panels, exterior components, and structural applications where manufacturers prioritize durability and production scalability. Carbon Fiber SMC, although representing a smaller share of nearly 10%–15%, is the fastest-growing segment as premium commercial vehicle platforms adopt advanced lightweight materials for improved efficiency and performance. Traditional polyester-based SMC continues supporting high-volume applications, while vinyl ester and hybrid SMC materials are gaining attention for improved mechanical properties and chemical resistance. Companies are increasing investment in hybrid formulations and automated processing technologies to balance performance with manufacturing economics. The shift toward electric commercial vehicles is redirecting development priorities toward lighter, stronger composite solutions.

Exterior body components represent the leading application segment, capturing approximately 45%–50% of commercial vehicle SMC usage due to strong demand for lightweight, corrosion-resistant panels, hoods, roofs, and covers. These applications provide significant operational advantages by reducing maintenance requirements and improving vehicle lifecycle performance. Structural components are the fastest-growing application area, expanding at a stronger pace as manufacturers integrate composites into electric trucks, buses, and specialized fleet vehicles. Interior components, electrical housings, and other applications continue maintaining steady adoption, particularly where manufacturers require flame resistance, durability, and design flexibility. Approximately 25%–30% of new commercial vehicle platforms incorporate advanced composite components to improve efficiency and manufacturing flexibility. Companies are responding through application-specific SMC development, automated production expansion, and partnerships with vehicle OEMs to accelerate integration.

Commercial vehicle manufacturers (OEMs) represent the dominant end-user segment, accounting for nearly 60%–65% of SMC demand due to direct integration of composite components into vehicle platforms. OEMs rely on SMC materials for weight optimization, improved styling flexibility, and reduced assembly complexity across trucks, buses, and specialty vehicles. Fleet operators and aftermarket suppliers represent emerging demand groups, with adoption increasing as maintenance efficiency and vehicle lifecycle optimization become stronger priorities. Tier-1 automotive suppliers are also expanding their role by developing customized composite solutions and supporting OEM production programs. Fleet modernization initiatives in China, the United States, and Europe are increasing demand for durable lightweight components, with more than 30% of commercial vehicle operators prioritizing efficiency-focused upgrades. Companies are strengthening partnerships with OEMs, expanding regional manufacturing capabilities, and developing application-specific materials to secure long-term contracts.

Asia-Pacific accounted for the largest market share at 38% in 2025 however, North America is expected to register the fastest growth, expanding at a CAGR of 5.1% between 2026 and 2033.

North America holds approximately 28% of the global Sheet Molding Compounds For Commercial Vehicle Market, supported by strong commercial vehicle manufacturing capabilities in the United States, Mexico, and Canada. The region’s adoption is concentrated in truck body panels, structural components, and electric commercial vehicle platforms. Increasing fleet electrification programs and emission reduction targets are accelerating SMC integration, with manufacturers targeting 15%–20% vehicle weight reductions through composite materials. Automotive suppliers are expanding localized production facilities and forming OEM partnerships to improve supply reliability. Advanced molding automation and recycled composite development are becoming key priorities across major manufacturing hubs.

United States Market Outlook: The United States represents the largest North American market due to its established commercial vehicle manufacturing ecosystem and growing electric fleet transition. More than 30% of new commercial vehicle development programs prioritize lightweight materials to improve efficiency. Companies are investing in domestic composite production, automated manufacturing systems, and advanced material partnerships to support next-generation trucks and specialty vehicles.

Europe contributes nearly 22% of global SMC demand for commercial vehicles, supported by Germany, France, and Italy’s strong automotive manufacturing base. The region’s market direction is shaped by strict emission regulations, sustainability targets, and increased use of lightweight materials in transportation. Germany remains a major hub for composite innovation, with manufacturers integrating SMC components into commercial vehicles to reduce weight and improve durability. Around 25% of European vehicle material development initiatives focus on improving recyclability and reducing lifecycle emissions. Companies are strengthening supplier networks, investing in circular composite technologies, and expanding production capabilities to meet changing automotive requirements.

Germany Market Outlook: Germany leads European SMC adoption due to its advanced automotive engineering capabilities and strong supplier ecosystem. The country’s commercial vehicle manufacturers are increasing composite usage in electric mobility platforms and high-performance applications. More than 40% of automotive suppliers in Germany are evaluating sustainable composite solutions to support future vehicle production and regulatory compliance.

Asia-Pacific dominates the global Sheet Molding Compounds For Commercial Vehicle Market with approximately 38% share, driven by large-scale commercial vehicle production in China, Japan, South Korea, and India. China’s expanding electric truck and bus manufacturing ecosystem is creating strong demand for lightweight composite components. The region benefits from integrated supply chains, high-volume production capabilities, and increasing investment in advanced materials. China produces millions of commercial vehicles annually, creating significant opportunities for SMC adoption across exterior and structural applications. Companies are expanding local manufacturing capacity, developing cost-efficient composite formulations, and strengthening partnerships with automotive OEMs.

China Market Outlook: China remains the leading Asia-Pacific market due to its extensive commercial vehicle manufacturing base and rapid electric mobility deployment. More than 35% of new energy commercial vehicle programs incorporate lightweight material strategies to improve operating efficiency. Domestic composite manufacturers are increasing automation investment and developing localized supply networks to support large-scale production.

South America represents a developing market for SMC adoption, supported by commercial vehicle manufacturing activities in Brazil and Argentina. The region accounts for nearly 7% of global demand, with applications concentrated in truck body components, agricultural vehicles, and transportation fleets. Brazil’s automotive industry modernization initiatives are encouraging manufacturers to adopt lightweight materials for improved fuel efficiency and durability. However, limited composite production infrastructure and dependence on imported raw materials continue affecting adoption speed. Companies are improving supply resilience through regional partnerships, localized processing facilities, and collaboration with automotive manufacturers to address material availability challenges.

Brazil Market Outlook: Brazil is the largest South American market due to its established vehicle manufacturing sector and agricultural transportation demand. The country produces over 2 million vehicles annually across commercial and passenger categories, creating opportunities for composite component integration. Manufacturers are focusing on cost-effective SMC solutions for trucks, buses, and specialty vehicles.

Middle East & Africa accounts for approximately 5% of global SMC demand, with adoption supported by transportation infrastructure development, fleet modernization, and industrial diversification programs. Countries such as the United Arab Emirates and Saudi Arabia are increasing investment in logistics fleets and advanced manufacturing capabilities. The region’s commercial vehicle sector is gradually adopting lightweight composite components to improve operational efficiency in demanding environments. More than 20% of new industrial mobility initiatives emphasize efficiency improvements and material optimization. Companies are developing regional partnerships, expanding distribution networks, and introducing durable composite solutions suitable for high-temperature operating conditions.

Saudi Arabia Market Outlook: Saudi Arabia is emerging as a strategically important market due to infrastructure expansion and industrial localization programs. The country’s logistics and transportation sectors are undergoing modernization, increasing demand for efficient commercial vehicles. Manufacturers are exploring composite material partnerships and technology investments to support local production capabilities and future mobility initiatives.

The Sheet Molding Compounds For Commercial Vehicle Market features competition between global composite suppliers such as IDI Composites International, Menzolit, Polynt, and Core Molding Technologies, alongside regional manufacturers competing on cost and localized supply. The top five players account for approximately 45% of market share, creating a moderately consolidated structure. Competition is driven by material performance, customization, production speed, and supply reliability, with advanced formulations improving component strength by 15%–25% and automated processing reducing cycle times by nearly 20%. Global leaders are expanding manufacturing footprints, while regional suppliers focus on pricing flexibility and faster delivery. Companies are investing in recyclable composites, OEM partnerships, and vertical integration to secure supply chains. The competitive landscape is shifting toward sustainable materials and EV-focused lightweight solutions. High tooling investment and technical expertise remain entry barriers. Winning requires superior innovation, reliable capacity, and strong OEM collaboration.

Menzolit

Polynt Group

Core Molding Technologies

Continental Structural Plastics

Premix Inc.

DIC Corporation

Lorenz Kunststofftechnik

Molymer SSP

ASTAR S.A.

Changzhou Rixin Composite Materials

Tianma Group

Jiangsu Jiuding New Material

Huamei New Material

Advanced SMC formulations are transforming commercial vehicle component manufacturing through improved fiber reinforcement, low-density materials, and recyclable resin systems. Hybrid glass-carbon fiber SMC solutions deliver approximately 20% higher strength-to-weight performance than conventional composites, enabling lighter truck panels and structural parts. Adoption is increasing among OEMs developing electric commercial vehicles, where weight optimization directly improves operating efficiency and battery utilization.

Automation and digital manufacturing are becoming critical technology differentiators. Automated compression molding systems improve production consistency by 15%–30% compared with traditional manual processes while reducing material waste. Manufacturers are integrating AI-based process monitoring, digital twins, and predictive quality systems to optimize tooling performance and reduce production variation.

Between 2026 and 2028, recyclable SMC materials, smart manufacturing platforms, and EV-specific composite architectures will influence competitive positioning. Companies with advanced material engineering capabilities and localized automated production will gain advantages through faster development cycles, improved cost control, and stronger OEM partnerships. The transition from conventional SMC production toward intelligent composite manufacturing is reshaping supplier strategies across commercial vehicle markets.

October 2024 IDI Composites International opened its new 120,000-square-foot global headquarters and manufacturing technology center in Noblesville, Indiana. The facility includes three SMC production lines and doubles SMC/BMC production capacity, strengthening automotive and transportation composite supply. Source: www.idicomposites.com

April 2025 IDI Composites International expanded its manufacturing network through a joint venture with SMC Composites in Mexico City, creating IDI Composites International Mexico. The facility increased global manufacturing locations to seven and improved supply access for transportation customers. Source: www.idicomposites.com

April 2025 Menzolit advanced its sustainability strategy by participating in the CICLO R&D project focused on improving composite circularity. The initiative supports recyclable material development and strengthens sustainable SMC solutions for automotive applications and industrial markets. Source: www.menzolit.com

2025 IDI Composites International continued development of advanced Structural Thermoset Composites, including carbon-fiber reinforced SMC solutions designed for lightweight transportation applications. The technology combines high strength, corrosion resistance, and reduced weight for demanding commercial vehicle components.

The Sheet Molding Compounds For Commercial Vehicle Market Report covers detailed analysis across material types, including glass fiber SMC, carbon fiber SMC, and advanced hybrid formulations. The report evaluates applications such as exterior components, structural parts, interior components, and electrical systems, along with end-users including OEMs, suppliers, and fleet operators. Regional coverage includes North America, Europe, Asia-Pacific, South America, and Middle East & Africa with country-level industrial insights.

The report examines technology adoption, manufacturing trends, supply-chain developments, competitive strategies, and emerging opportunities in electric commercial vehicles. Analysis highlights automation adoption, recyclable composite development, supplier expansion, and OEM partnerships. The study supports investment planning, market entry strategies, product positioning, and long-term competitive decisions from 2026 to 2033.

| Report Attribute / Metric | Details |

|---|---|

| Market Revenue (2025) | USD 1,652.3 Million |

| Market Revenue (2033) | USD 2,300.7 Million |

| CAGR (2026–2033) | 4.225% |

| Base Year | 2025 |

| Forecast Period | 2026–2033 |

| Historic Period | 2021–2025 |

| Segments Covered |

By Type

By Application

By End-User

|

| Key Deliverables | Revenue Forecast; Market Trends; Growth Drivers & Restraints; Technology Insights; Segmentation Analysis; Regional Insights; Competitive Landscape; Regulatory & ESG Overview; Recent Developments |

| Regions Covered | North America; Europe; Asia-Pacific; South America; Middle East & Africa |

| Companies Profiled | IDI Composites International; Menzolit; Polynt Group; Core Molding Technologies; Continental Structural Plastics; Premix Inc.; DIC Corporation; Lorenz Kunststofftechnik; Molymer SSP; ASTAR S.A.; Changzhou Rixin Composite Materials; Tianma Group; Jiangsu Jiuding New Material; Huamei New Material |

| Customization & Pricing | Available on Request (10% Customization Free) |