Reports

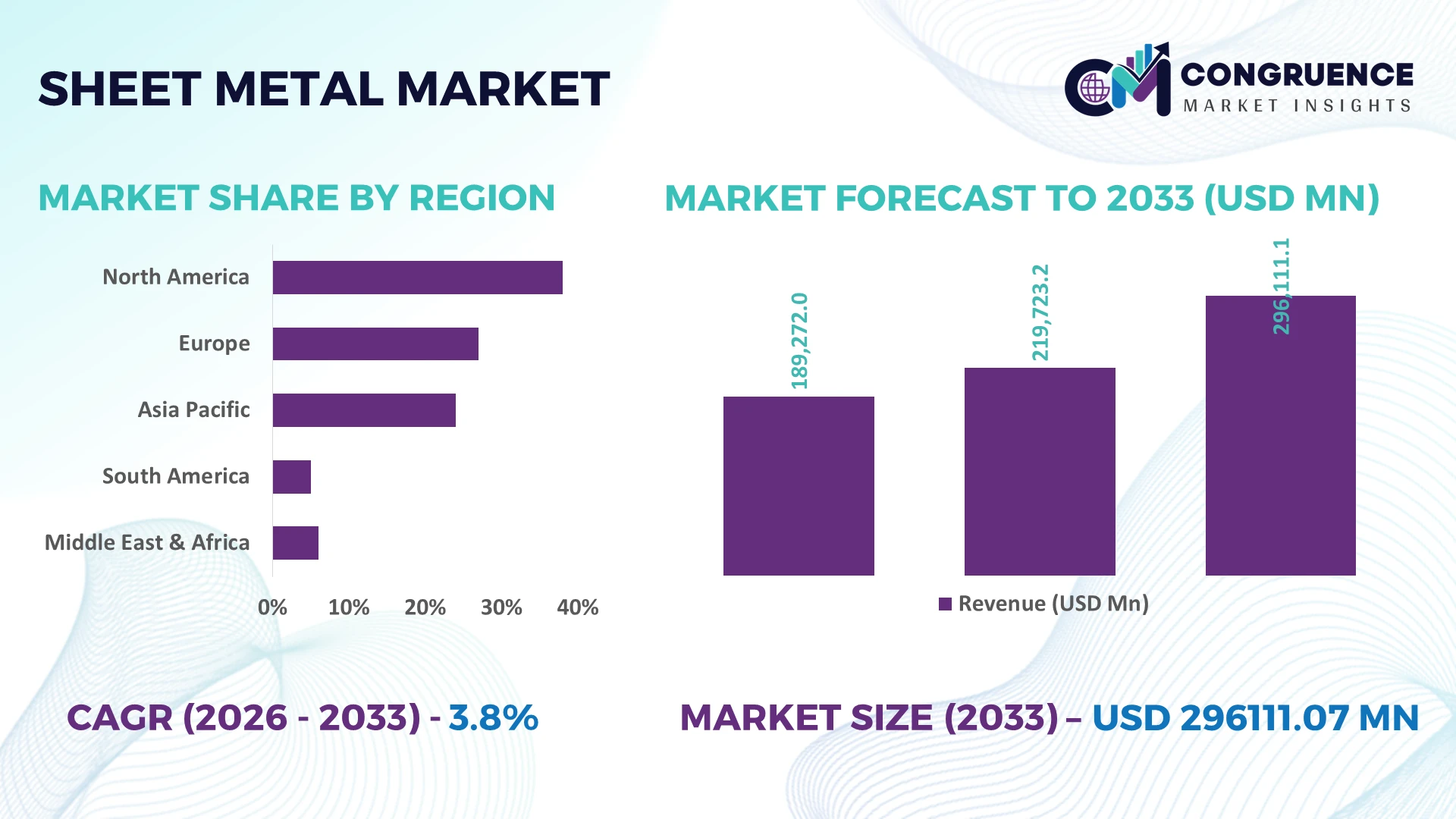

The Global Sheet Metal Market was valued at USD 219723.15 Million in 2025 and is anticipated to reach a value of USD 296111.07 Million by 2033 expanding at a CAGR of 3.8% between 2026 and 2033. Growth is being driven by automated fabrication systems, electric vehicle manufacturing, aerospace component production, and precision metal processing supported by digital factory modernization.

China remains the dominant country, accounting for approximately 35% of global sheet metal production capacity, supported by large-scale automotive, construction, consumer electronics, and industrial equipment manufacturing. More than 60% of major fabrication facilities have integrated CNC and robotic processing technologies, while India continues expanding faster through manufacturing investments and production-linked industrial policies. Ongoing global supply-chain diversification following Red Sea shipping disruptions has further reinforced regional manufacturing resilience and localized sourcing strategies.

Manufacturers should prioritize automation investments, regional production networks, and advanced forming capabilities to strengthen competitiveness across high-value industrial applications.

Market Size & Growth: USD 219723.15 Million (2025) to USD 296111.07 Million (2033) at 3.8% CAGR, supported by automated fabrication, EV production, and industrial modernization.

Top Growth Drivers: EV manufacturing (+22%), industrial automation (+18%), and aerospace component demand (+15%) continue accelerating global production.

Short-Term Forecast: By 2028, fabrication efficiency improves over 16% while material waste declines approximately 12% through digital manufacturing.

Emerging Technologies: AI-driven quality inspection, robotic bending systems, and digital twin production increase throughput by nearly 20%.

Regional Leaders: Asia-Pacific exceeds USD 145 Billion, Europe surpasses USD 62 Billion, North America approaches USD 54 Billion, driven by localized manufacturing expansion.

Consumer/End-User Trends: More than 58% of industrial buyers prioritize precision-engineered lightweight sheet metal components for energy-efficient equipment.

Pilot/Case Example: 2026 smart fabrication deployment reduced production defects by 24% and shortened production cycles by 18%.

Competitive Landscape: Top manufacturers control approximately 32% market share alongside leaders including ArcelorMittal, Nippon Steel, POSCO, Tata Steel, and SSAB.

Regulatory & ESG Impact: Low-carbon manufacturing initiatives reduce production emissions by roughly 14% while strengthening export competitiveness.

Investment & Funding: More than USD 11 Billion supports plant expansion, automation upgrades, and regional supply-chain diversification projects.

Innovation & Future Outlook: Advanced high-strength steel, laser processing, and intelligent manufacturing platforms accelerate premium product development and operational resilience.

Growing demand from automotive, aerospace, electrical equipment, renewable energy, and construction sectors continues reshaping the Sheet Metal Market. Intelligent laser cutting, AI-enabled quality monitoring, and high-strength lightweight alloys are improving production precision and reducing processing time. Around 27% of new fabrication investments target smart manufacturing capabilities, while regional supply-chain localization and evolving industrial compliance requirements continue influencing procurement strategies, setting the foundation for the strategic discussion ahead.

Sheet metal manufacturing has become a strategic industrial capability as governments and manufacturers strengthen domestic production, modernize infrastructure, and reduce dependence on extended global supply chains. Rising investment in electric mobility, industrial machinery, energy infrastructure, and advanced manufacturing is increasing demand for precision-engineered fabricated components. Digital factory deployment and localized sourcing strategies are transforming procurement decisions, while stricter quality standards are accelerating adoption of automated fabrication technologies across high-value manufacturing sectors.

Advanced fiber laser cutting combined with AI-enabled process control delivers approximately 25% faster processing and reduces material scrap by nearly 18% compared with conventional mechanical cutting systems. China continues leading large-scale production through integrated manufacturing clusters, while Germany differentiates through highly automated precision fabrication supporting automotive and industrial engineering. Over the next two to three years, robotic forming and digital production monitoring are expected to exceed 65% adoption among newly commissioned fabrication facilities, improving operational consistency and reducing production downtime.

Leading manufacturers are deploying smart fabrication cells, expanding regional processing facilities, and partnering with automation providers to strengthen production flexibility. For example, automotive suppliers are integrating automated bending and laser welding systems to shorten production cycles while supporting lightweight component manufacturing. Companies securing digital manufacturing capabilities, resilient supply networks, and high-precision fabrication expertise will strengthen competitive positioning as industrial customers increasingly prioritize quality, responsiveness, and manufacturing resilience.

The primary growth driver is the rapid integration of intelligent manufacturing technologies across sheet metal fabrication. More than 62% of newly commissioned fabrication facilities now incorporate CNC automation, while robotic welding improves production consistency by nearly 30% and reduces rework rates by approximately 20%. India's manufacturing expansion initiatives and China's continued investment in smart factories are accelerating deployment of advanced forming and cutting technologies. In response, manufacturers are expanding automated production lines, investing in AI-enabled quality inspection, and forming technology partnerships to increase throughput while lowering operational costs. The strategic advantage increasingly lies in combining digital process control with flexible manufacturing systems capable of supporting high-mix, low-volume production requirements.

Fluctuating steel and aluminum prices remain a structural constraint for sheet metal producers, particularly those operating under long-term supply contracts. Raw materials typically account for over 55% of fabrication costs, while price swings exceeding 15% within a year directly compress margins and complicate production planning. Shipping disruptions and energy cost fluctuations continue affecting procurement reliability in several manufacturing hubs. Companies are responding by diversifying supplier networks, increasing localized sourcing, and negotiating multi-year procurement agreements to improve cost predictability. Businesses with stronger inventory optimization and digital procurement capabilities are maintaining greater operational stability despite ongoing commodity market volatility.

Advanced automation, digital twins, and AI-driven production optimization are opening new opportunities beyond conventional sheet metal processing. Automated process monitoring improves equipment utilization by nearly 20%, while predictive maintenance reduces unexpected downtime by approximately 25%. Japan and South Korea are expanding investment in intelligent manufacturing platforms supporting high-precision industrial applications and lightweight component production. Companies are increasing R&D spending, establishing automation partnerships, and developing integrated fabrication ecosystems capable of delivering customized production with shorter lead times. A significant strategic opportunity exists in combining digital engineering with flexible manufacturing to serve rapidly evolving electric mobility and industrial equipment markets.

Long-term competitiveness depends on successfully integrating advanced manufacturing technologies while addressing persistent workforce shortages. More than 40% of fabrication companies report difficulty recruiting skilled CNC programmers and automation specialists, while digital system integration can extend implementation timelines by nearly 20%. Complex interoperability between legacy equipment and modern manufacturing execution systems further limits operational consistency. Manufacturers are investing in workforce development, industrial training partnerships, and standardized digital architectures to improve implementation success. Organizations that effectively combine technical talent, interoperable production infrastructure, and cybersecurity-ready manufacturing systems will achieve stronger operational resilience and sustain competitive differentiation over the coming decade.

Smart Factories Expand Rapidly: AI-enabled production scheduling, robotic bending, and machine vision inspection are becoming standard across modern fabrication plants. More than 65% of newly commissioned high-volume facilities now integrate automated workflow control, while production defects decline by nearly 22% and setup times improve by around 18%. Labor shortages in Germany and Japan are accelerating digital deployment, prompting manufacturers to restructure operations through integrated software platforms, automation partnerships, and centralized production management for greater throughput consistency.

Localized Supply Networks Strengthen: Manufacturers are shifting procurement toward regional suppliers to reduce logistics risks and improve delivery reliability following continued global shipping disruptions. Local sourcing has increased by approximately 20% among major industrial fabricators, while average component lead times have fallen by nearly 15%. Companies are expanding secondary processing facilities and establishing long-term supplier agreements across India and Mexico, creating more resilient manufacturing ecosystems while reducing inventory exposure and transportation uncertainty.

Precision Laser Processing Advances: Fiber laser cutting and automated welding technologies are replacing conventional fabrication methods for high-tolerance industrial applications. Laser-equipped production lines improve material utilization by approximately 17% while shortening processing cycles by nearly 25%. Automotive and electronics manufacturers are increasing deployment of digitally controlled fabrication systems, encouraging equipment suppliers to scale modular production solutions that support flexible batch manufacturing without sacrificing dimensional accuracy.

Lightweight Material Mix Evolves: Product engineering priorities increasingly favor optimized material selection rather than maximum material thickness, particularly in transportation and electronics manufacturing. Advanced aluminum and high-strength steel usage has expanded by roughly 19%, while hybrid fabrication processes reduce assembly weight by nearly 14%. Manufacturers are strengthening partnerships with material producers and investing in multi-material forming technologies as industrial decarbonization policies and energy-efficiency requirements reshape component design strategies.

Steel remains the dominant sheet metal type because of its cost efficiency, structural strength, and broad compatibility with automotive, construction, and industrial manufacturing. It accounts for approximately 52% of fabricated sheet metal demand, supported by mature supply chains and established processing infrastructure. Stainless steel continues expanding in food processing, healthcare equipment, and chemical applications where corrosion resistance is critical. Copper and brass retain strategic importance in electrical systems, precision engineering, and decorative architectural applications despite representing comparatively smaller production volumes.

Aluminum is the fastest-growing type as lightweight engineering becomes a priority across transportation and electronics manufacturing. Aluminum sheet demand has increased by nearly 18% in advanced mobility applications, while manufacturers report weight reductions approaching 30% compared with conventional steel assemblies. Companies are expanding aluminum processing capacity, developing advanced forming technologies, and strengthening partnerships with alloy producers to improve production flexibility. Investment priorities increasingly balance steel's production scale with aluminum's performance advantages, while stainless steel, copper, and brass continue supporting specialized high-value industrial applications.

Automotive remains the leading application, representing approximately 41% of total sheet metal consumption due to extensive use in body structures, chassis systems, and structural reinforcements. Automated stamping, laser cutting, and robotic welding continue improving production efficiency by nearly 20% across vehicle manufacturing facilities. Construction follows with consistent demand for roofing, structural panels, and building components, while industrial equipment maintains stable consumption through machinery and production infrastructure modernization.

Aerospace is the fastest-growing application as aircraft manufacturers increase production of lightweight precision components manufactured from advanced alloys. Aerospace fabrication activity has expanded by approximately 16%, supported by greater adoption of high-precision forming technologies and tighter dimensional requirements. Electronics manufacturers continue increasing demand for compact enclosures and thermal management components, while industrial equipment suppliers invest in flexible fabrication systems capable of serving multiple sectors. Companies are scaling automated production, expanding precision machining capabilities, and integrating digital quality assurance to support increasingly specialized application requirements.

Manufacturing remains the largest end-user because of continuous demand for machinery, factory equipment, production systems, and fabricated industrial components. Nearly 38% of fabricated sheet metal output supports manufacturing operations, while automated fabrication reduces production cycle times by approximately 18%. Construction and automotive continue generating substantial purchasing volumes through infrastructure development and vehicle production, whereas electronics manufacturers increasingly require precision-fabricated lightweight assemblies supporting miniaturized product designs.

Energy is emerging as the fastest-growing end-user as renewable power infrastructure, battery manufacturing, and grid modernization projects increase demand for durable fabricated metal components. Demand from the energy sector has expanded by roughly 17%, encouraging manufacturers to develop application-specific products and strengthen engineering partnerships. Aerospace & defense buyers continue emphasizing precision fabrication and certified manufacturing processes, while companies increasingly customize production, optimize pricing strategies, and establish long-term industrial supply agreements to strengthen competitive positioning across diverse end-user markets.

Asia-Pacific accounted for the largest market share at 47.8% in 2025 however, Middle East & Africa is expected to register the fastest growth, expanding at a 5.2% between 2026 and 2033.

Advanced Manufacturing and Nearshoring Strengthen Regional Competitiveness

North America maintains a strong position through highly automated fabrication facilities serving automotive, aerospace, defense, and industrial equipment manufacturers. The region contributes approximately 22% of global sheet metal production, supported by widespread deployment of robotic forming, fiber laser cutting, and digital quality management systems. More than 68% of large fabrication facilities have integrated smart manufacturing technologies, improving production flexibility and reducing operational downtime. Nearshoring initiatives continue driving investment in regional processing capacity, while manufacturers expand partnerships with OEMs to shorten supply chains and improve delivery reliability for high-value engineered components.

United States Market Outlook: The United States leads the regional market through its extensive aerospace, defense, automotive, and industrial manufacturing base supported by advanced fabrication technologies. More than 70% of high-volume production facilities utilize automated laser processing and CNC manufacturing platforms, enabling consistent high-precision output. Domestic investments in semiconductor facilities, electric vehicle production, and industrial reshoring continue strengthening demand for fabricated sheet metal components, while manufacturers prioritize digital production systems and strategic supplier partnerships to improve operational resilience.

Precision Engineering and Low-Carbon Manufacturing Drive Modernization

Europe represents approximately 21% of global sheet metal demand, supported by advanced automotive engineering, industrial machinery production, and strict manufacturing quality standards. Manufacturers are accelerating investment in energy-efficient fabrication equipment, automated forming technologies, and digitally integrated production systems. More than 60% of newly upgraded fabrication plants incorporate intelligent process monitoring to improve productivity and material utilization. Sustainability regulations continue encouraging deployment of lower-emission manufacturing technologies, while engineering-focused enterprises expand production capabilities for lightweight industrial and transportation components.

Germany Market Outlook: Germany remains Europe's strategic manufacturing hub due to its leadership in automotive engineering, industrial machinery, and precision fabrication technologies. Industrial automation deployment exceeds 72% across major fabrication facilities, supporting high-quality sheet metal processing for export-oriented industries. Manufacturers continue investing in digital production platforms, AI-assisted inspection systems, and advanced laser processing while strengthening supplier collaboration to maintain technological leadership in precision-engineered components.

Large-Scale Manufacturing Ecosystems Sustain Global Leadership

Asia-Pacific dominates global sheet metal production through integrated industrial clusters, strong export capabilities, and rapidly expanding manufacturing infrastructure. The region accounts for nearly 48% of market activity, supported by extensive automotive, electronics, construction, and heavy equipment manufacturing. Factory automation adoption has surpassed 63% among newly established large-scale fabrication plants, while continuous investment in smart manufacturing improves productivity and production consistency. Strong domestic demand combined with export-oriented manufacturing enables companies to expand fabrication capacity and strengthen vertically integrated supply networks.

China Market Outlook: China remains the largest national market because of its comprehensive manufacturing ecosystem, advanced steel processing capacity, and extensive industrial infrastructure. Approximately 35% of global sheet metal production capacity is concentrated in China, supported by continuous investment in intelligent manufacturing and industrial automation. Domestic manufacturers are expanding precision fabrication capabilities, integrating AI-enabled quality systems, and strengthening supply-chain localization to support electric vehicles, renewable energy equipment, consumer electronics, and industrial machinery production.

Industrial Expansion Supports Manufacturing Diversification

South America continues strengthening its sheet metal industry through expanding automotive assembly, mining equipment manufacturing, and infrastructure development. The region contributes approximately 5% of global market activity, with industrial modernization gradually increasing fabrication efficiency. Investments in automated cutting systems have improved production productivity by nearly 14%, while manufacturers increasingly localize selected component manufacturing to reduce import dependence. Infrastructure limitations remain a constraint, yet industrial partnerships and equipment modernization continue improving operational competitiveness across priority manufacturing sectors.

Brazil Market Outlook: Brazil leads regional demand through its established automotive manufacturing, construction materials industry, and expanding industrial equipment sector. Major fabrication companies continue modernizing production facilities with automated forming and laser cutting technologies, improving operational efficiency across domestic manufacturing. Industrial investment programs and increasing localization of metal component production are strengthening supply security while supporting higher-value fabricated products for transportation and infrastructure applications.

Industrial Investment Accelerates Manufacturing Transformation

The Middle East & Africa is experiencing rapid industrial transformation driven by infrastructure megaprojects, manufacturing diversification, and localized production initiatives. The region represents approximately 4% of global sheet metal demand while recording accelerating deployment of advanced fabrication technologies. More than 18% of recently announced industrial investments include modern metal processing and fabrication facilities supporting construction, energy, and transportation projects. Governments continue promoting industrial localization, encouraging manufacturers to establish regional production capacity and advanced processing operations.

Saudi Arabia Market Outlook: Saudi Arabia leads regional market development through large-scale industrial diversification programs, infrastructure expansion, and downstream metal manufacturing investments. New industrial zones continue attracting fabrication companies serving energy, construction, and transportation sectors, while automated manufacturing deployment improves production quality and efficiency. Domestic manufacturing initiatives and integrated steel processing investments are strengthening local supply capabilities, enabling companies to reduce import dependence and support long-term industrial expansion.

The Sheet Metal Market is led by ArcelorMittal, Nippon Steel, POSCO, Tata Steel, and SSAB, competing against regional fabricators, specialized processors, and precision engineering firms. Global leaders compete through integrated production and advanced metallurgy, while regional manufacturers challenge on lead time, localized supply, and application-specific customization. The top five players collectively control approximately 34% of the market, creating a moderately consolidated structure. Competition increasingly depends on technology adoption, production flexibility, and supply resilience rather than price alone. Automated fabrication improves productivity by nearly 22%, digital quality systems reduce defects by around 18%, and localized sourcing cuts delivery cycles by approximately 15%. Companies are expanding processing facilities, securing long-term raw material agreements, investing in AI-enabled manufacturing, and strengthening downstream fabrication capabilities through vertical integration and strategic partnerships. Consolidation is shifting competitive advantage toward digitally connected manufacturing ecosystems. High capital investment, automation expertise, and qualified technical talent remain major entry barriers. Winning requires precision manufacturing, resilient supply chains, intelligent automation, and faster customer responsiveness.

ArcelorMittal

Nippon Steel Corporation

POSCO

Tata Steel Limited

SSAB AB

thyssenkrupp AG

Nucor Corporation

United States Steel Corporation

JFE Steel Corporation

Hyundai Steel Company

Baosteel Co., Ltd.

Voestalpine AG

Current technology investment is centered on intelligent fabrication, combining fiber laser cutting, robotic bending, AI-based inspection, and connected manufacturing execution systems. More than 65% of newly modernized fabrication facilities deploy automated production monitoring, while AI-assisted quality control reduces inspection time by approximately 30% and lowers defect rates by nearly 20%. These technologies improve production consistency, shorten changeover periods, and enable manufacturers to process increasingly complex component designs with greater operational reliability.

Emerging technologies include digital twins, predictive maintenance, adaptive robotics, and cloud-connected production analytics. Compared with conventional mechanical fabrication workflows, integrated digital manufacturing improves overall equipment effectiveness by approximately 25% while reducing material waste by nearly 18%. Large automotive, aerospace, and industrial equipment manufacturers benefit most because digital integration supports higher production flexibility, faster engineering revisions, and improved traceability across multi-site manufacturing networks. Around 40% of advanced fabrication facilities are actively expanding connected manufacturing capabilities.

Between 2026 and 2028, autonomous process optimization, AI-driven scheduling, and collaborative robotics will reshape fabrication economics. Companies adopting interoperable digital platforms, simulation-driven process engineering, and real-time production intelligence will strengthen cost competitiveness, improve capacity utilization, and accelerate customer responsiveness. Manufacturers delaying technology modernization risk higher operating costs, longer production cycles, and weaker positioning as intelligent manufacturing becomes the operational benchmark across global sheet metal fabrication.

October 2024: ArcelorMittal advanced its New Energy Magnetic Material (NEMM) collaboration to strengthen electrical steel production for high-efficiency motors, supporting downstream sheet metal applications. The program forms part of a USD 4.4 billion annual capital investment strategy, reinforcing advanced manufacturing competitiveness. Source: ArcelorMittal

June 2025: SSAB signed a technology agreement with Danieli to build its new Luleå mini-mill featuring two electric arc furnaces and a 2.5 million-ton annual capacity, accelerating fossil-free specialty steel production for automotive and industrial sheet metal manufacturing while significantly lowering carbon emissions. Source: SSAB

July 2025: Bystronic and SSAB expanded their strategic partnership to optimize laser cutting and bending for recycled and fossil-free steels through collaborative material testing and process development, improving productivity and manufacturing efficiency for advanced sheet metal fabrication across industrial customers. Source: Bystronic

April 2026: POSCO and JSW Steel established a 50:50 joint venture to construct a 6 million-ton-per-year integrated steel mill in Odisha, India, strengthening localized steel supply, expanding downstream sheet metal manufacturing capacity, and enhancing long-term supply-chain resilience. Source: POSCO Newsroom

This report delivers a comprehensive assessment of the global Sheet Metal Market across the 2026–2033 outlook, examining competitive positioning, manufacturing trends, technology adoption, and evolving procurement strategies. It evaluates five major material types, five core application segments, and six end-user industries while providing detailed regional analysis across North America, Europe, Asia-Pacific, South America, and the Middle East & Africa. More than 60% of the assessment emphasizes operational transformation, automation deployment, and manufacturing modernization influencing industrial competitiveness.

The report analyzes adoption of AI-enabled fabrication, fiber laser processing, robotic forming, digital quality inspection, and smart factory integration alongside supply-chain localization and sustainability initiatives. It benchmarks leading manufacturers, investment priorities, partnership strategies, and product innovation across established and emerging industrial markets. Strategic insights support expansion planning, technology investment, supplier selection, competitive benchmarking, and long-term manufacturing decisions by identifying high-priority demand segments, deployment trends, and evolving enterprise procurement patterns throughout the forecast period.

| Report Attribute/Metric | Report Details |

|---|---|

|

Market Revenue in 2025 |

USD V2025 Million |

|

Market Revenue in 2033 |

USD V2033 Million |

|

CAGR (2026 - 2033) |

C111% |

|

Base Year |

2025 |

|

Forecast Period |

2026 - 2033 |

|

Historic Period |

2021 - 2025 |

|

Segments Covered |

T1 |

|

Key Report Deliverable |

Revenue Forecast, Growth Trends, Market Dynamics, Segmental Overview, Regional and Country-wise Analysis, Competition Landscape |

|

Region Covered |

North America, Europe, Asia-Pacific, South America, Middle East, Africa |

|

Key Players Analyzed |

mplayers |

|

Customization & Pricing |

Available on Request (10% Customization is Free) |