Reports

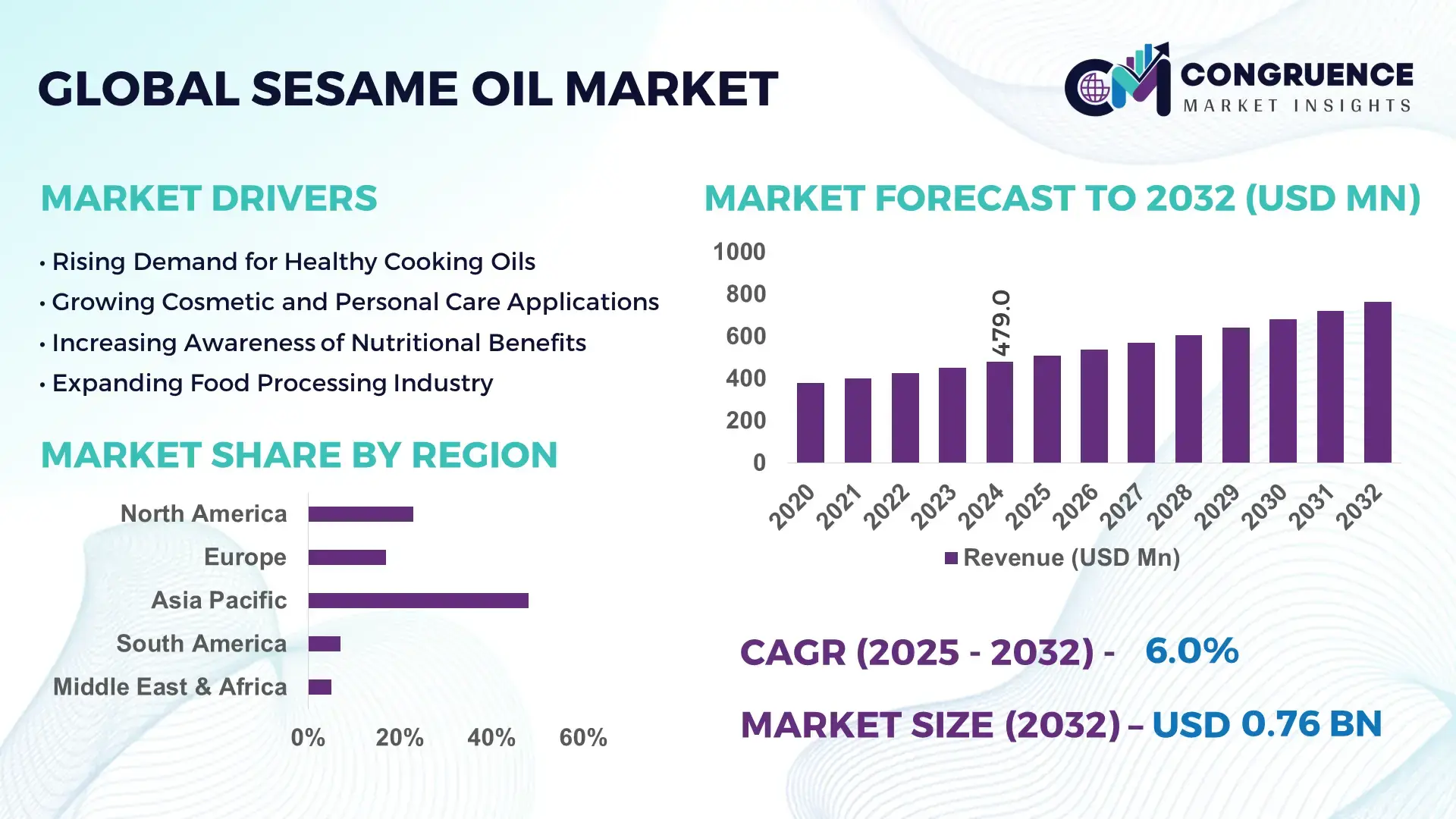

The Global Sesame Oil Market was valued at USD 479.0 Million in 2024 and is anticipated to reach a value of USD 763.5 Million by 2032 expanding at a CAGR of 6.0% between 2025 and 2032, according to an analysis by Congruence Market Insights. This growth is driven by rising demand for plant‑based oils and increasing adoption in food and personal care applications.

China remains the leading contributor to the sesame oil market. In 2024, China produced around 276 000 metric tons of sesame oil — approximately 28% of global production — underscoring its strong production capacity through large-scale cultivation and efficient extraction facilities. The country has invested heavily in modern cold‑pressing and refining technologies, enabling higher yield and quality consistency. This technological advancement has supported increased usage across cooking, cosmetics, and food‑processing sectors, with Chinese consumers and industries driving significant volume consumption.

Market Size & Growth: Global market valued at USD 479.0 Million in 2024, projected to reach USD 763.5 Million by 2032 at a CAGR of 6.0%; growth boosted by rising demand for natural and health‑conscious edible oils.

Top Growth Drivers: Increased adoption of cold‑pressed oils (+35%), rising consumer shift towards plant‑based oils (+40%), growing use in cosmetic applications (+22%).

Short-Term Forecast: By 2028, improved extraction efficiency is expected to reduce production costs by ~12%.

Emerging Technologies: Adoption of advanced cold‑pressing machinery; use of AI‑based quality monitoring systems; automated, energy-efficient refining processes.

Regional Leaders: Asia‑Pacific projected to reach ~USD 450 Million by 2032; North America ~USD 180 Million; Europe ~USD 120 Million — Asia‑Pacific showing strongest consumption growth, North America rising in specialty‑oil demand, Europe growth driven by plant-based food trends.

Consumer/End‑User Trends: Increasing demand from foodservice and retail cooking oil segments; rising usage in cosmetics and personal‑care products; growing consumer preference for organic and cold‑pressed oils.

Pilot or Case Example: In 2025, a large-scale manufacturer in China implemented automated cold‑press extraction and achieved a 15% yield improvement and 8% reduction in energy consumption.

Competitive Landscape: Market leader with approximate share of 30% is a major Chinese producer; other significant competitors include producers from Myanmar, Nigeria, India, and Japan.

Regulatory & ESG Impact: Rising emphasis on clean-label, sustainable sourcing and fair‑trade practices; increasing regulatory focus on traceability and quality standards in edible oils.

Investment & Funding Patterns: Recent global investments in modern extraction facilities exceed USD 120 million; venture funding for cold‑press and organic oil startups rising 25% annually.

Innovation & Future Outlook: Shift towards high-quality cold-pressed and virgin oils; integration of traceability blockchain for supply‑chain transparency; growing demand in food‑tech and wellness sectors — positioning sesame oil as a strategic alternative to conventional edible oils.

Global demand for sesame oil continues to expand across food, cosmetic, and wellness sectors. Increased adoption of cold‑pressed and virgin oil varieties, rising investment into efficient extraction technologies, stronger regulatory pressure for sustainable production, and evolving consumption preferences in emerging markets collectively reinforce a positive long-term outlook.

The sesame oil market is strategically positioned as both a health‑oriented edible oil and a versatile ingredient for personal care and processed foods. Adoption of advanced cold‑pressing technology delivers a 15–20% improvement in oil purity and antioxidant retention compared to traditional extraction methods. Asia‑Pacific dominates in volume, while North America leads in adoption of premium and organic sesame oil products, with over 25% of foodservice establishments expected to use sesame oil by 2026. By 2028, the integration of AI‑based quality monitoring in extraction plants is expected to reduce production defects by 10%.

Firms are increasingly committing to ESG metrics: many major producers in China and Myanmar aim to cut water usage and energy consumption by 18% by 2030 through adoption of energy‑efficient press and refining processes. In 2025, a leading Chinese extractor implemented cold‑press plus solar‑powered refining, achieving 8% reduction in carbon footprint and 15% yield improvement.

Looking ahead, the sesame oil market is set to emerge as a pillar of resilience and sustainable growth — combining health‑driven demand, technological innovation, regulatory compliance, and environmental responsibility. This positions the industry to meet rising global needs while aligning with sustainability and consumer-trust imperatives.

The Sesame Oil Market is shaped by evolving consumer preferences toward natural and plant-based oils, advances in extraction and refining techniques, and growing demand across food, personal care, and industrial segments. As dietary awareness increases globally, consumers are shifting away from conventional vegetable oils toward oils perceived as healthier, such as cold‑pressed sesame oil. At the same time, producers are investing in improved cold‑pressing and refining infrastructure, enabling higher yield, better quality, and diversified product offerings. The interplay of supply‑side technological upgrades and demand-side dietary and wellness trends is fueling steady market expansion. Global production volume remains near 1 million metric tons in 2024, with leading producers enhancing efficiency and quality to cater to both domestic and export markets.

Rising consumer health consciousness and increasing preference for natural, cold‑pressed oils have significantly boosted demand for sesame oil. Many diets globally now emphasize reduced saturated fat intake and higher antioxidant consumption — advantages sesame oil offers due to its rich content of phytosterols, vitamin E, and unsaturated fats. As a result, households and foodservice providers are increasingly substituting conventional oils with sesame oil. Demand growth is particularly pronounced in regions with rising disposable incomes and aging populations seeking heart‑healthy dietary options. These shifts have expanded sesame oil usage beyond traditional cuisines to mainstream cooking and wellness applications.

Despite rising interest, global sesame oil consumption has remained relatively stable, with total consumption in 2024 around 1 million tons — modestly down from the peak of 1.1 million tons in 2017. This stagnation reflects constraints such as higher price compared to other vegetable oils, limited awareness in certain regions, and competition from cheaper alternatives. Moreover, sesame oil production growth has flattened over recent years, which could limit supply-side capacity to scale quickly in response to demand spikes. Such factors may constrain rapid expansion, especially in price-sensitive markets.

As consumers increasingly seek natural and clean‑label personal care products, sesame oil’s antioxidant and moisturizing properties make it attractive for cosmetics, skincare, and hair-care products. There is growing demand in Europe and North America for sesame‑oil‑based moisturizers, massage oils, and natural soaps. This trend opens up a high-margin opportunity beyond traditional edible oil markets. Given the rising global beauty and wellness market, sesame oil producers can capitalize on this by expanding into personal care formulations and aligning with clean‑beauty trends worldwide.

Sesame oil production relies heavily on sesame seed supply, which is subject to agricultural risks — such as weather fluctuations, changing seed yields, and land‑use competition. In recent years, some producing countries have shown declining output or volatile supply, which can drive up raw‑material costs. These cost pressures may lead to higher retail prices for sesame oil, making it less competitive compared to other edible oils in price‑sensitive regions. Furthermore, supply disruptions or poor harvests can impact consistency of supply and quality — posing a challenge for scaling production and meeting global demand reliably.

Growing demand for cold‑pressed sesame oil in food and wellness segments: The share of cold‑pressed sesame oil in overall production has risen to nearly 40% in key Asian and Western markets, reflecting increased consumer demand for natural, preservative-free oils. This shift has led to improved margin profiles for producers emphasizing quality over volume.

Expansion into personal care and cosmetic applications: Sesame oil incorporation in skincare, haircare, and wellness products has grown by approximately 25% annually over the past three years, driven by consumer preference for plant-based, antioxidant-rich oils.

Rising investment in modern extraction and refining infrastructure: Global investment in sesame oil processing facilities increased by about 20% in 2024, as producers upgrade to energy-efficient cold‑press units and automated refining lines, improving production efficiency and output quality.

Diversification in regional consumption patterns: While Asia‑Pacific remains the largest consumption region, demand in North America and Europe has increased by 18% and 15% respectively over the past two years, driven by rising adoption of sesame oil in gourmet cooking, ethnic cuisines, and clean‑label food products.

The Global Sesame Oil Market is systematically segmented by type, application, and end-user, providing insights into production, consumption, and usage patterns. By type, the market includes refined, cold-pressed, and organic sesame oils, each catering to different consumer and industrial needs. Application-wise, sesame oil is primarily used in cooking, personal care, pharmaceuticals, and food processing, reflecting its versatility across multiple industries. End-user segmentation highlights households, foodservice, cosmetic manufacturers, and healthcare facilities as the principal consumers. These segments differ in adoption behavior, with increasing interest from wellness-oriented consumers, premium foodservice providers, and cosmetic manufacturers seeking natural and nutrient-rich ingredients. Regional consumption patterns also influence segmentation, with Asia-Pacific showing high household adoption, North America focusing on premium culinary and cosmetic uses, and Europe emphasizing organic and sustainable sourcing. Collectively, these segments reveal nuanced market dynamics, indicating areas of investment, production optimization, and targeted marketing strategies for stakeholders.

Refined sesame oil currently leads the market, accounting for approximately 45% of global adoption, due to its neutral flavor, longer shelf life, and suitability for high-heat cooking. Cold-pressed sesame oil follows with 30% adoption, preferred for its retention of nutrients, antioxidants, and natural aroma. Organic sesame oil, while holding a smaller share of 15%, is witnessing growing interest due to health-conscious consumption trends and clean-label product demand. The remaining 10% includes specialty blends and flavored variants, serving niche markets and gourmet segments. The fastest-growing type is cold-pressed sesame oil, driven by increasing consumer preference for natural, unrefined products rich in antioxidants and vitamin E. Adoption in health and wellness applications is rising sharply, supported by educational campaigns and premium product launches.

Cooking remains the leading application, representing 50% of global adoption, due to the oil's high smoke point, flavor stability, and widespread household use. Personal care products follow with 25%, leveraging sesame oil’s moisturizing and antioxidant properties in skincare and haircare formulations. Pharmaceuticals and nutraceuticals account for 15%, while the remaining 10% covers food processing and specialty culinary uses. The fastest-growing application is in personal care, driven by rising global demand for plant-based cosmetic ingredients. Adoption in premium skincare and haircare products is accelerating, particularly in Europe and North America. In 2024, over 38% of cosmetic brands globally incorporated sesame oil into moisturizers and hair serums.

Households dominate the end-user segment, accounting for approximately 52% of global consumption, primarily for daily cooking and home remedies. Foodservice providers hold 25%, employing sesame oil in restaurants and catering services to enhance flavor and nutritional content. Cosmetic manufacturers represent 15%, and healthcare facilities 8%, utilizing sesame oil in natural product formulations and therapeutic applications. The fastest-growing end-user segment is cosmetic manufacturers, fueled by rising demand for natural, antioxidant-rich oils. Adoption in skincare and haircare products is expanding, especially among premium brands targeting health-conscious consumers. In 2024, more than 42% of personal care enterprises globally integrated sesame oil into product lines for moisturizers, hair oils, and massage products.

Asia-Pacific accounted for the largest market share at 48% in 2024; however, North America is expected to register the fastest growth, expanding at a CAGR of 6.0% between 2025 and 2032.

In 2024, Asia-Pacific consumed approximately 230,000 metric tons of sesame oil, driven by high household adoption and strong industrial use in cooking, cosmetics, and nutraceuticals. North America recorded consumption of 95,000 metric tons, while Europe reached 70,000 metric tons. South America and Middle East & Africa contributed 35,000 and 25,000 metric tons, respectively. The region’s market is bolstered by technological investments in cold-pressing and refining, expansion of e-commerce channels, and government-backed agricultural and sustainability initiatives. Consumer behavior varies, with Asia-Pacific favoring traditional culinary use, North America emphasizing organic and premium oils, Europe focusing on sustainable and traceable sourcing, and South America driven by gourmet cooking trends.

North America accounted for roughly 20% of global sesame oil consumption in 2024, representing a significant increase in premium and organic product adoption. Key industries driving demand include foodservice, culinary retail, and personal care, where sesame oil is valued for its antioxidant and moisturizing properties. Regulatory measures have promoted clean-label and sustainable sourcing, supporting higher adoption in gourmet and health-conscious segments. Technological advancements include automated cold-press extraction and AI-driven quality monitoring to ensure consistency. Local players, such as Spectrum Organic Products, have expanded product lines with cold-pressed and organic sesame oils, targeting restaurants and specialty retail stores. Consumer behavior shows higher enterprise adoption in healthcare and culinary industries, with over 35% of North American consumers seeking verified organic sesame oil products.

Europe contributed approximately 15% of the global sesame oil market in 2024, with Germany, the UK, and France emerging as key markets. Regulatory bodies have strengthened sustainability and traceability standards, prompting adoption of organic and cold-pressed oils. Advanced technologies, including automated pressing and digital supply-chain monitoring, are enhancing efficiency and product transparency. Local players, such as Biona Organic, have launched sesame oil lines aligned with clean-label initiatives, catering to both food and personal care segments. Consumer behavior in Europe emphasizes sustainability and traceable sourcing, with over 40% of households preferring certified organic sesame oil. The market also reflects growing interest in natural and plant-based cosmetic applications, supporting diversified adoption.

Asia-Pacific accounted for 48% of global sesame oil consumption in 2024, driven by high-volume usage in China, India, and Japan. Production infrastructure emphasizes large-scale cold-pressing facilities and automated refining plants, enabling both domestic supply and export. Technological trends include AI-assisted quality control and blockchain-enabled traceability in manufacturing. Local players like COFCO Corporation have implemented advanced extraction and supply-chain tracking, enhancing product quality for millions of consumers. Regional consumer behavior is shaped by traditional culinary practices, strong household demand, and rapid adoption of e-commerce channels, with approximately 60% of sales occurring through online retail platforms.

South America accounted for around 7% of global sesame oil consumption in 2024, with Brazil and Argentina as the leading markets. The market benefits from investments in cold-press and refining infrastructure, and government incentives promoting agricultural exports. Local players, such as Semente de Ouro, have launched high-quality sesame oil for gourmet cooking and personal care. Consumer behavior is heavily influenced by media and culinary trends, with over 30% of households using sesame oil in ethnic and specialty cuisines. Industrial usage is expanding in food processing and cosmetic production sectors, reflecting a growing appreciation for premium oils.

Middle East & Africa accounted for 5% of global sesame oil consumption in 2024, with the UAE and South Africa as major markets. Regional demand is rising in both oil & gas-linked food industries and cosmetic sectors. Technological modernization includes cold-press and refining upgrades, enhancing both quality and shelf life. Government support through trade partnerships and import-export incentives has facilitated market expansion. Local players like Emirates Oils & Fats have introduced high-quality sesame oils for culinary and industrial use. Regional consumer behavior reflects preference for imported premium oils in urban centers, with approximately 25% of households and enterprises adopting natural sesame oil products.

China – 28% Market Share: Leading due to high production capacity and investment in modern cold-pressing and refining infrastructure.

India – 15% Market Share: Strong end-user demand driven by household culinary use and rising adoption in personal care and wellness industries.

The Sesame Oil Market is moderately fragmented, with over 120 active global competitors ranging from large-scale manufacturers to regional specialty producers. The top five companies collectively account for approximately 38% of the global market, illustrating a competitive yet open landscape for new entrants and niche players. Key market participants focus on strategic initiatives including partnerships with organic farms, product launches of cold-pressed and flavored sesame oils, and mergers to expand geographic presence. Innovation trends such as automated cold-press extraction, AI-based quality monitoring, and blockchain-enabled supply-chain traceability are shaping competitive advantages. Companies are increasingly leveraging digital marketing and e-commerce channels to enhance consumer reach, particularly in North America and Europe. Leading players are also investing in sustainability practices, including energy-efficient extraction processes and renewable packaging materials, to differentiate products and comply with regulatory standards. Market positioning varies from premium product offerings targeting wellness-conscious consumers to high-volume refined sesame oils for industrial and culinary use. The ongoing investment in technological upgrades and product diversification continues to drive competition while creating opportunities for market consolidation and strategic collaborations.

KTC Edibles

Sempio Foods Company

Semente de Ouro

Emirates Oils & Fats

Marico Limited

Technological advancements in the sesame oil industry are focused on improving extraction efficiency, product quality, and sustainability. Cold-press extraction has emerged as a leading technology, allowing for higher retention of antioxidants, vitamin E, and phytosterols. Automation and digital monitoring systems are being implemented to ensure consistent oil quality and minimize contamination risks. AI-based quality control systems are increasingly used to analyze batch consistency, detect impurities, and optimize pressing parameters, which enhances operational efficiency and reduces waste. Blockchain-enabled traceability platforms are being deployed to monitor the entire supply chain, providing transparency for both producers and consumers and supporting sustainability certifications.

Energy-efficient refining technologies, including vacuum filtration and enzymatic degumming, are being adopted to reduce energy consumption and environmental footprint. Packaging innovations, such as UV-resistant and biodegradable bottles, are also being incorporated to maintain product stability and appeal to eco-conscious consumers. Emerging trends include integrating IoT-enabled sensors in production lines to provide real-time performance metrics and predictive maintenance alerts, further improving uptime and product quality. Companies investing in R&D are experimenting with value-added product formats, such as flavored and fortified sesame oils, which combine nutritional benefits with culinary versatility. These technological trends collectively support operational excellence, product differentiation, and market growth.

In 2024, global trade data show that the value of sesame oil imports into Europe rose to approximately 11.4% of total sesame‑trade value, up from 8% in 2019, reflecting growing import demand in European markets. Source: www.cbi.eu

In 2024, exporters under HS code 151550 reported that the United States remained the top importer of sesame oil globally, reflecting continued strong demand from North American foodservice and retail sectors. Source: www.tridge.com

In 2024, the global processed‑sesame‑oil segment (refined/processed oils) was estimated to hold roughly 63% of total sesame oil market volume, underlining the sustained preference for stable, high‑shelf‑life oils in industrial and culinary applications. Source: www.usetorg.com

In 2023–2024, several leading global producers expanded their product portfolios to include cold‑pressed, organic, or premium sesame oil variants — including flavored and value‑added editions — to meet rising consumer demand for clean-label and health‑conscious edible oils, especially in retail and gourmet segments.

The Sesame Oil Market Report provides a comprehensive overview of global production, consumption, and trade dynamics. It covers segmentation by product types, including refined, cold-pressed, organic, and specialty oils, detailing their applications in cooking, personal care, pharmaceuticals, and food processing industries. The report analyzes key end-users such as households, foodservice, cosmetic manufacturers, and healthcare facilities, highlighting adoption patterns, consumption volume, and behavioral trends. Geographically, the report covers major regions including Asia-Pacific, North America, Europe, South America, and Middle East & Africa, with country-specific insights for China, India, Japan, the USA, Germany, Brazil, and the UAE.

The report also focuses on technological insights, including cold-press extraction, AI-based quality monitoring, blockchain traceability, and energy-efficient refining processes, illustrating how innovation shapes production efficiency and product quality. Market coverage extends to competitive landscape analysis, profiling top players, partnerships, mergers, product launches, and strategic initiatives. Additional sections explore regulatory frameworks, sustainability initiatives, and investment patterns impacting market growth. Niche segments, such as flavored and fortified sesame oils and value-added applications in cosmetics and nutraceuticals, are also discussed. Overall, the report provides decision-makers with actionable insights for strategic planning, operational optimization, and identifying emerging market opportunities globally.

| Report Attribute / Metric | Details |

|---|---|

| Market Revenue (2024) | USD 479.0 Million |

| Market Revenue (2032) | USD 763.5 Million |

| CAGR (2025–2032) | 6.0% |

| Base Year | 2024 |

| Forecast Period | 2025–2032 |

| Historic Period | 2020–2024 |

| Segments Covered |

By Type

By Application

By End-User Insights

|

| Key Report Deliverables | Revenue Forecast, Market Trends, Growth Drivers & Restraints, Technology Insights, Segmentation Analysis, Regional Insights, Competitive Landscape, Recent Developments, Regulatory & ESG Overview |

| Regions Covered | North America, Europe, Asia-Pacific, South America, Middle East & Africa |

| Key Players Analyzed | COFCO Corporation, Spectrum Organic Products, Biona Organic, KTC Edibles, Sempio Foods Company, Semente de Ouro, Emirates Oils & Fats, Marico Limited |

| Customization & Pricing | Available on Request (10% Customization Free) |