Reports

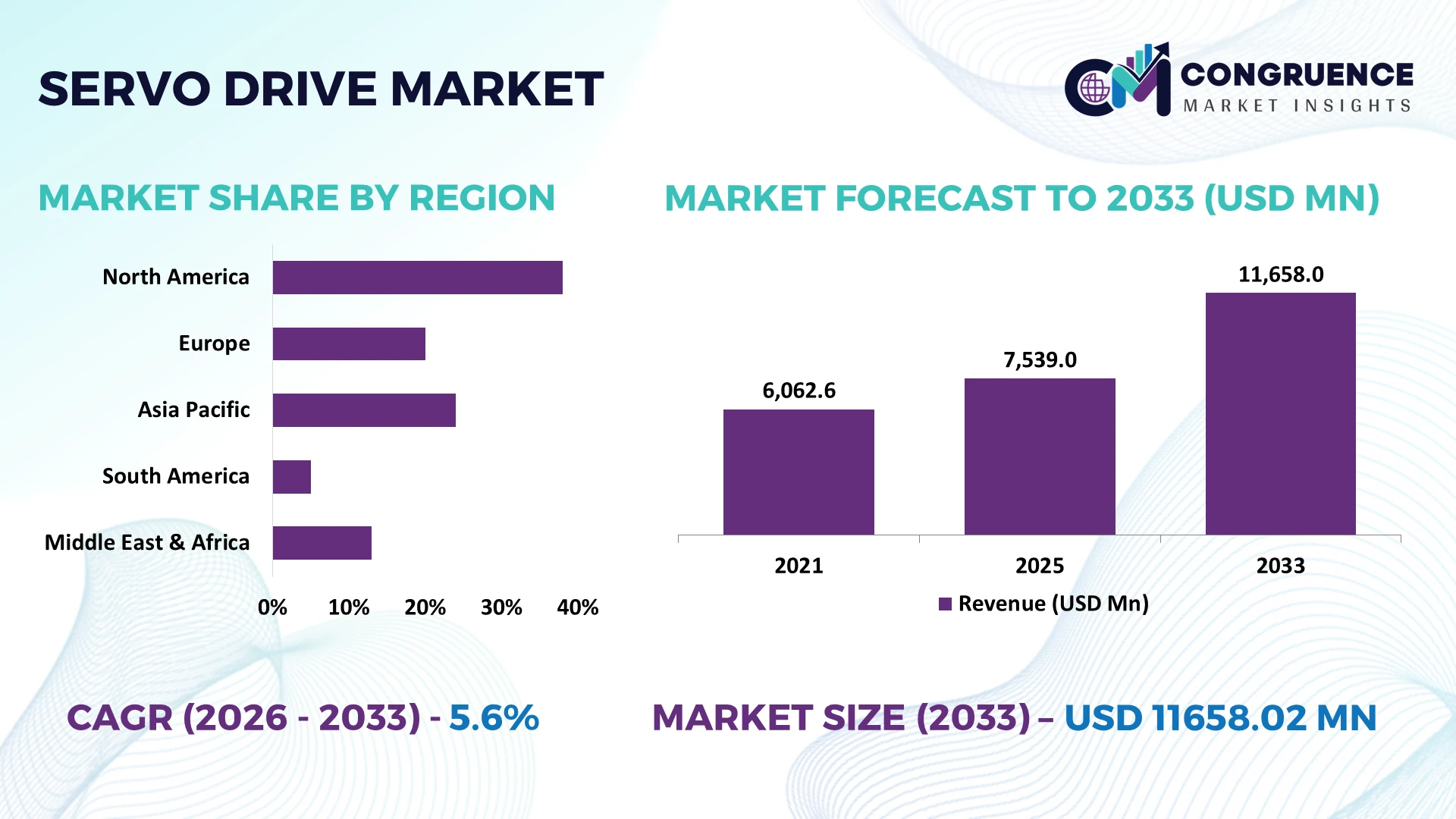

The Global Servo Drive Market was valued at USD 7539 Million in 2025 and is anticipated to reach a value of USD 11658.02 Million by 2033 expanding at a CAGR of 5.6% between 2026 and 2033. Rapid deployment of industrial robotics, AI-enabled motion control, high-speed manufacturing equipment, and precision automation across automotive, semiconductor, electronics, and packaging industries continues to strengthen the global servo drive market.

China remains the leading market, representing approximately 34% of global industrial robot installations while expanding investments in smart manufacturing and semiconductor production. Japan maintains leadership in precision servo technologies, with over 60% of advanced machine tools integrating digital motion control systems, whereas Germany continues accelerating Industry 4.0 modernization despite evolving European industrial policy and supply-chain realignment in 2026.

Manufacturers prioritizing intelligent, energy-efficient, and digitally connected servo drive solutions are strengthening production flexibility, operational resilience, and long-term competitive positioning.

Market Size & Growth: USD 7,539 million (2025) to USD 11,658.02 million (2033) at a CAGR of 5.6%, driven by expanding industrial automation and intelligent motion-control deployment.

Top Growth Drivers: Industrial robotics adoption +18%, smart factory investments +15%, and semiconductor automation demand +12% worldwide.

Short-Term Forecast: By 2027, predictive maintenance reduces unplanned downtime by nearly 20% while improving production efficiency by approximately 16%.

Emerging Technologies: AI-driven tuning, digital twins, edge diagnostics, and industrial Ethernet connectivity are enhancing precision, responsiveness, and system reliability.

Regional Leaders: Asia-Pacific exceeds USD 5.6 billion, Europe approaches USD 2.8 billion, and North America surpasses USD 2.2 billion, supported by continued manufacturing expansion.

Consumer & End-User Trends: More than 68% of newly commissioned automated production lines integrate intelligent servo drive systems to improve precision and energy efficiency.

Pilot/Case Example: A 2026 smart automotive assembly deployment improved positioning accuracy by 25% while reducing commissioning time by 18%.

Competitive Landscape: Leading manufacturers collectively hold approximately 45% of global shipments, with Siemens, Mitsubishi Electric, Yaskawa, Schneider Electric, and Delta Electronics maintaining strong market positions.

Regulatory & ESG Impact: High-efficiency servo drive platforms reduce industrial electricity consumption by approximately 15%, supporting stricter sustainability and carbon-reduction objectives.

Investment & Funding: More than USD 2 billion is supporting automation expansion, regional manufacturing partnerships, and localized production amid global supply-chain diversification.

Innovation & Future Outlook: AI-enabled motion control, integrated functional safety, and software-defined automation are accelerating the next generation of flexible, high-performance manufacturing systems.

Servo Drive Market demand is expanding across robotics, semiconductor fabrication, electric vehicle manufacturing, packaging machinery, and high-precision machine tools as industries pursue faster production cycles and greater accuracy. AI-assisted auto-tuning, integrated safety functions, and real-time condition monitoring improve operational efficiency, while next-generation energy-efficient platforms reduce power consumption by nearly 15%. Ongoing industrial localization initiatives and evolving global supply-chain strategies continue shaping future market opportunities, setting the foundation for the strategic discussion.

Servo drive systems have become a strategic component of modern manufacturing because precision motion control directly influences productivity, product quality, and operational flexibility. Manufacturers are replacing conventional variable-speed architectures with intelligent digital motion platforms to support autonomous production, high-mix manufacturing, and predictive maintenance. Supply-chain restructuring since 2026 has accelerated localized automation investments, encouraging manufacturers to reduce dependence on labor-intensive processes while strengthening production resilience across automotive, electronics, battery, and semiconductor industries.

Modern servo drives equipped with AI-assisted tuning and real-time diagnostics deliver up to 20% lower energy consumption and approximately 30% faster commissioning than legacy analog motion-control systems, reducing lifecycle operating costs while improving equipment utilization. China continues leading large-scale deployment through extensive factory automation, whereas Japan focuses on ultra-precision motion technologies for advanced manufacturing equipment. Germany emphasizes digitally connected production environments, creating a differentiated innovation model centered on industrial interoperability and machine intelligence.

Over the next two to three years, more than 45% of newly commissioned automated production cells are expected to integrate networked servo platforms with edge-based monitoring capabilities. Automotive manufacturers increasingly deploy servo-driven assembly lines to improve positioning accuracy while reducing maintenance intervals. Equipment suppliers are expanding software partnerships, localized production, and integrated automation portfolios, positioning intelligent servo ecosystems as a long-term competitive advantage for industrial manufacturers.

Industrial modernization is increasing demand for intelligent servo drive systems capable of supporting high-speed, precision manufacturing. More than 68% of newly installed automated production lines now integrate digital servo motion control, while predictive maintenance applications reduce unplanned downtime by nearly 20% and improve equipment utilization by approximately 16%. China's continued investment in semiconductor fabrication and advanced manufacturing has reinforced demand for high-performance motion systems. In response, manufacturers are expanding localized production, integrating AI-based drive optimization, and forming automation partnerships to deliver complete motion-control solutions. The strategic shift from standalone hardware toward software-enabled automation platforms strengthens recurring service opportunities while improving long-term customer retention.

Servo drive production continues to face pressure from semiconductor dependency, specialized electronic components, and interoperability challenges across heterogeneous industrial equipment. Lead times for selected industrial control components remain 15–20% above pre-disruption levels, while system integration costs account for nearly 25% of total automation project expenditure. Japan and Germany continue experiencing elevated engineering requirements for legacy equipment upgrades, extending deployment schedules. To reduce operational risk, manufacturers are localizing critical component sourcing, negotiating long-term supply agreements, and developing modular servo architectures compatible with multiple industrial communication protocols. These measures improve deployment consistency while protecting production schedules from supply-chain volatility.

The next phase of servo drive innovation is shifting toward AI-powered optimization, edge computing, and software-defined automation platforms. AI-assisted parameter tuning shortens commissioning time by approximately 30%, while intelligent energy management reduces electricity consumption by nearly 15% across automated production environments. India is emerging as a strategic manufacturing destination through expanding electronics production and industrial automation initiatives, creating demand for scalable motion-control solutions. Equipment suppliers are increasing investment in digital engineering platforms, collaborative robotics integration, and cloud-connected diagnostics. This evolution creates recurring software and lifecycle service opportunities beyond traditional hardware sales, strengthening long-term competitive differentiation.

Successful deployment increasingly depends on digital engineering expertise rather than hardware availability alone. Nearly 40% of industrial facilities report shortages of skilled automation engineers, while integration and software validation activities represent around 30% of total implementation timelines. The transition toward connected manufacturing environments also increases cybersecurity requirements for networked motion-control infrastructure. Manufacturers in the United States and Japan are responding by expanding engineering training programs, strengthening industrial cybersecurity frameworks, and collaborating with automation software providers to simplify commissioning. Companies that successfully combine workforce development, secure connectivity, and interoperable automation platforms will achieve more consistent deployment performance and stronger long-term operational competitiveness.

AI-Based Motion Optimization Intelligent auto-tuning and adaptive control algorithms are becoming standard across industrial motion systems, reducing commissioning time by nearly 30% while improving positioning accuracy by approximately 25%. Japan and Germany are accelerating software-centric automation upgrades as manufacturers integrate predictive diagnostics into production workflows. Servo drive suppliers are expanding AI-enabled portfolios and collaborating with industrial software vendors to shorten deployment cycles and reduce lifecycle maintenance costs.

Localized Manufacturing Expansion Supply-chain restructuring has encouraged manufacturers to regionalize production of servo drives and critical electronic components. Local sourcing has increased by nearly 18% across several industrial automation programs, while component lead times have fallen by approximately 12% through localized assembly. China and India continue attracting automation investments, prompting companies to establish new production facilities, diversify supplier networks, and strengthen strategic partnerships to improve delivery reliability.

Industrial Ethernet Standardization More than 65% of newly deployed servo systems now utilize high-speed industrial Ethernet protocols, improving machine communication efficiency by approximately 20%. The transition toward connected factories is reducing integration complexity while supporting centralized equipment monitoring. Equipment manufacturers are redesigning servo platforms with open communication architectures, enabling faster interoperability across robotics, CNC machines, and automated production cells.

Energy-Efficient Drive Platforms Stricter industrial efficiency requirements and rising electricity costs are accelerating adoption of high-efficiency servo drives capable of lowering power consumption by nearly 15% and reducing heat generation by approximately 18%. A less visible trend is the growing integration of regenerative braking technology, allowing manufacturers to recover operational energy during repetitive motion cycles. Companies are prioritizing modular product development and digital energy management capabilities to strengthen long-term operational sustainability.

Digital Servo Drives dominate the market with an estimated 43% share, supported by superior communication capability, intelligent diagnostics, and seamless integration with Industry 4.0 environments. Their ability to enable predictive maintenance, adaptive tuning, and real-time monitoring makes them the preferred choice for advanced manufacturing. AC Servo Drives remain the second-largest segment because of high efficiency and dependable performance across CNC equipment, robotics, and automated production lines. Together, Digital and AC Servo Drives account for more than 70% of new industrial automation deployments. Manufacturers continue expanding software-enabled product portfolios and strengthening partnerships with industrial automation providers to improve system interoperability.

Multi-Axis Servo Drives represent the fastest-growing segment as demand increases for synchronized motion control in robotics and semiconductor manufacturing, with adoption rising by nearly 19% across high-precision production facilities. DC Servo Drives retain relevance in legacy industrial equipment and specialized applications, while Analog Servo Drives continue serving cost-sensitive installations where modernization remains limited. Investment priorities are increasingly shifting toward intelligent, network-connected motion platforms capable of supporting flexible manufacturing and digital production ecosystems.

Robotics represents the largest application segment with an estimated 36% market share, supported by increasing deployment in automotive assembly, electronics manufacturing, and warehouse automation. Precision positioning, repeatability, and high-speed motion requirements make servo drives essential for robotic systems. CNC Machines continue representing a mature, high-volume application due to continuous modernization of metalworking and precision engineering industries. Combined, Robotics and CNC Machines contribute more than 60% of industrial servo drive installations. Manufacturers are strengthening robotics partnerships and integrating intelligent motion software to improve operational flexibility.

Semiconductor Equipment is emerging as the fastest-growing application as chip manufacturing facilities demand ultra-precise motion control with positioning accuracy improvements exceeding 20%. Packaging Machinery is expanding rapidly through high-speed consumer goods production, while Material Handling continues benefiting from warehouse automation and logistics modernization. Equipment suppliers are introducing modular servo architectures, integrated diagnostics, and scalable motion platforms to address increasingly diverse industrial requirements while improving deployment efficiency.

Automotive remains the largest end-user segment with approximately 34% market share, supported by extensive automation across body assembly, welding, painting, and electric vehicle production. High production volumes and strict quality requirements continue driving investment in intelligent servo motion systems. Industrial Manufacturing follows closely through widespread adoption in machine tools, metal fabrication, and factory automation. Together, these sectors account for more than 60% of large-scale servo drive deployments. Leading suppliers continue developing industry-specific automation packages and expanding localized engineering support for major manufacturing customers.

Electronics is the fastest-growing end-user segment, with automation deployment increasing by approximately 18% as manufacturers expand semiconductor, PCB, and consumer electronics production. Packaging continues strengthening demand through flexible manufacturing and high-speed production lines, while Food & Beverage manufacturers increasingly adopt servo-controlled equipment to improve hygiene, precision, and packaging efficiency. Companies are responding through customized motion-control solutions, strategic OEM partnerships, and integrated digital service offerings that strengthen long-term customer retention and operational performance.

Asia-Pacific accounted for the largest market share at 46.8% in 2025 however, Middle East & Africa is expected to register the fastest growth, expanding at a 6.9% between 2026 and 2033.

Advanced Manufacturing Modernization Accelerates Deployment

North America represents a mature servo drive market, supported by widespread industrial automation across automotive, aerospace, logistics, semiconductor, and food processing industries. The region accounts for approximately 24% of global demand, with the United States driving large-scale deployment of intelligent motion control systems across digitally connected factories. More than 65% of newly commissioned manufacturing facilities integrate Ethernet-enabled servo architectures to improve production flexibility and predictive maintenance capabilities. Continued investments in semiconductor fabrication and warehouse automation are expanding deployment across high-precision production environments. Manufacturers are strengthening partnerships with automation software providers while increasing localized engineering support, allowing faster commissioning, reduced downtime, and greater interoperability across complex manufacturing ecosystems.

United States Market Outlook: The United States remains the region's largest market due to its advanced industrial infrastructure, extensive robotics adoption, and expanding semiconductor manufacturing capacity. More than 70% of large industrial automation projects incorporate intelligent servo motion platforms for precision assembly and material handling applications. Equipment suppliers continue investing in digital engineering services, AI-enabled diagnostics, and integrated automation ecosystems, strengthening domestic manufacturing competitiveness while supporting production modernization initiatives.

Industry 4.0 and Energy Efficiency Reshape Industrial Automation

Europe continues strengthening its position through digitally connected manufacturing, industrial modernization, and stringent energy-efficiency objectives. The region contributes nearly 22% of global servo drive deployment, with demand concentrated across automotive, machine tools, packaging, and industrial equipment manufacturing. Approximately 60% of newly upgraded production facilities now deploy networked servo systems supporting predictive maintenance and real-time operational monitoring. Industrial decarbonization initiatives are encouraging adoption of high-efficiency motion platforms that reduce energy consumption while improving manufacturing precision. Equipment suppliers are expanding software integration capabilities and collaborative automation partnerships to support increasingly flexible production environments.

Germany Market Outlook: Germany leads the European market through its strong machine-building sector, industrial automation expertise, and advanced manufacturing ecosystem. More than 55% of precision machine-tool installations utilize intelligent servo drive platforms integrated with Industry 4.0 communication standards. Manufacturers continue prioritizing modular automation architectures, digital engineering capabilities, and high-performance motion solutions to strengthen production efficiency and export competitiveness.

Manufacturing Scale Sustains Global Leadership

Asia-Pacific remains the world's largest servo drive market, supported by extensive manufacturing capacity, rapid industrial automation, and large-scale electronics and semiconductor production. The region accounts for approximately 46.8% of global demand, with China, Japan, South Korea, and India serving as major deployment centers. More than 72% of new industrial robot installations occur within Asia-Pacific manufacturing facilities, reinforcing demand for precision motion-control technologies. Ongoing factory modernization, expanding battery production, and automation investments continue increasing deployment across automotive, semiconductor, and electronics industries. Companies are expanding regional production facilities, strengthening supplier ecosystems, and introducing software-enabled motion platforms tailored for high-volume manufacturing operations.

China Market Outlook: China remains the largest national market due to its unmatched manufacturing scale, smart factory expansion, and industrial automation investment. The country accounts for roughly 34% of global industrial robot installations, driving continuous demand for advanced servo drive systems across automotive, electronics, and semiconductor manufacturing. Domestic and international suppliers are expanding localized production, intelligent motion-control software, and integrated automation solutions to support increasingly sophisticated manufacturing requirements.

Industrial Automation Expands Across Manufacturing

South America is steadily increasing servo drive adoption through manufacturing modernization, food processing automation, mining operations, and packaging industries. The region contributes approximately 5% of global demand, with Brazil accounting for the majority of industrial deployments. Automation investment across manufacturing facilities has increased by nearly 14% as companies seek higher production consistency and lower operating costs. Infrastructure constraints and dependence on imported automation components continue affecting deployment timelines, encouraging manufacturers to establish regional distribution partnerships and localized technical support. The market increasingly favors modular servo platforms capable of supporting phased industrial upgrades without extensive infrastructure replacement.

Brazil Market Outlook: Brazil leads the regional market through its diversified industrial base, automotive production, and expanding food and beverage manufacturing sector. More than 45% of large automation projects are concentrated within major industrial corridors, where manufacturers continue upgrading production equipment with intelligent motion-control systems. Suppliers are expanding engineering support, training programs, and localized service networks to improve deployment efficiency and long-term equipment performance.

Industrial Diversification Supports Automation Investment

The Middle East & Africa market is gaining momentum through industrial diversification, infrastructure expansion, logistics modernization, and advanced manufacturing initiatives. The region contributes approximately 2.8% of global demand while recording increasing deployment across packaging, food processing, warehousing, and industrial equipment sectors. More than 20% of new industrial projects within major economic zones now incorporate automated motion-control technologies to improve operational efficiency and production quality. Companies are strengthening regional partnerships, expanding technical service capabilities, and investing in localized automation support to address growing industrial demand and workforce modernization initiatives.

Saudi Arabia Market Outlook: Saudi Arabia represents the region's most strategically important market, supported by industrial diversification programs, manufacturing expansion, and smart factory initiatives. Large industrial developments continue integrating advanced automation technologies, with automated production capacity increasing by approximately 18% across selected manufacturing sectors. Automation providers are expanding regional partnerships, engineering capabilities, and technical training programs to support long-term industrial transformation and strengthen domestic production competitiveness.

The competitive landscape is led by Siemens, Mitsubishi Electric, Yaskawa Electric, Schneider Electric, and Delta Electronics, competing directly against regional automation manufacturers and specialized motion-control suppliers for high-value industrial automation projects. The top five players collectively control approximately 45% of the global market, while regional suppliers compete through localized engineering support and cost-efficient product portfolios. Competition is primarily driven by motion accuracy, software integration, lifecycle service capability, and delivery speed rather than hardware pricing alone. AI-enabled servo platforms improve commissioning efficiency by nearly 30%, while energy-efficient designs reduce power consumption by approximately 15%, creating measurable operational advantages. Leading manufacturers are expanding localized production, strengthening OEM partnerships, integrating digital engineering software, and increasing vertical integration to secure critical electronic components amid supply-chain realignment. Software-defined automation and intelligent diagnostics are reshaping purchasing priorities, raising technical entry barriers through interoperability, cybersecurity, and application expertise. Winning requires differentiated digital capabilities, reliable supply networks, rapid deployment, and strong lifecycle support.

Siemens AG

Mitsubishi Electric Corporation

Yaskawa Electric Corporation

Schneider Electric SE

Delta Electronics, Inc.

ABB Ltd.

Rockwell Automation, Inc.

Fuji Electric Co., Ltd.

Bosch Rexroth AG

Beckhoff Automation GmbH & Co. KG

Omron Corporation

Panasonic Industry Co., Ltd.

Nidec Corporation

Inovance Technology Co., Ltd.

Digital servo drives integrated with AI-based motion control, edge diagnostics, and industrial Ethernet have become the core technology for precision manufacturing. More than 68% of newly deployed automation systems now utilize network-enabled servo platforms, enabling predictive maintenance and centralized equipment monitoring. AI-assisted auto-tuning reduces commissioning time by nearly 30% while improving positioning accuracy by approximately 25%, allowing manufacturers to increase throughput with lower engineering effort. Machine builders benefit through faster project delivery, while end users gain higher equipment availability and reduced maintenance costs.

Legacy analog servo systems are steadily being replaced by intelligent digital architectures capable of real-time communication and adaptive control. Compared with conventional analog platforms, modern digital servo drives deliver approximately 20% lower energy consumption and 35% faster response during complex multi-axis motion applications. Semiconductor, robotics, and packaging manufacturers are accelerating adoption because integrated safety, remote diagnostics, and software-defined configuration simplify production expansion while reducing lifecycle operating expenses. This technology transition increasingly favors automation suppliers offering complete digital motion ecosystems rather than standalone hardware.

Between 2026 and 2028, AI-enabled predictive control, digital twins, regenerative energy management, and software-defined automation will reshape industrial motion systems. Adoption of cloud-connected motion analytics is expected to exceed 50% among newly commissioned smart manufacturing facilities. Companies investing now in interoperable servo platforms, cybersecurity-ready communication, and scalable software capabilities will strengthen operational resilience, accelerate automation deployment, and establish durable competitive advantages as intelligent manufacturing becomes the global industrial standard.

January 2024 Siemens introduced the upgraded SINAMICS S210 servo drive system with new V6 software, EtherNet/IP connectivity, and DriveSim Advanced virtual commissioning for applications from 50 W to 7 kW, improving deployment flexibility and engineering efficiency. Source: Siemens Press

January 2025 Yaskawa launched functional safety-compliant products for its Σ-X AC Servo Drive Series, adding Advanced Safety Modules and safety-enabled servo motors to support CE machinery requirements, strengthening machine safety and accelerating adoption across European manufacturing.

May 2025 Mitsubishi Electric partnered with Tramec to deliver integrated gearmotor drive systems combining IE5+ ultra-high-efficiency motors with industrial gearboxes, expanding complete drive solution offerings and improving energy-efficient automation for manufacturing customers.

April 2026 Yaskawa introduced the compact GA501 Ethernet-integrated AC drive, improving connectivity with AC servo drives and robotic systems through native industrial networking, strengthening digital factory integration and simplifying intelligent automation deployment. S

The report provides comprehensive analysis of servo drive technologies across AC Servo Drives, DC Servo Drives, Digital Servo Drives, Analog Servo Drives, and Multi-Axis Servo Drives while evaluating demand across CNC machines, robotics, packaging machinery, material handling, semiconductor equipment, and major industrial end-users. It assesses competitive positioning across North America, Europe, Asia-Pacific, South America, and the Middle East & Africa, covering more than 10 leading manufacturers alongside emerging technology participants. The study also examines deployment trends, digital automation adoption, energy-efficient motion control, and intelligent manufacturing developments.

The report supports strategic decision-making by identifying evolving technology priorities, industrial deployment patterns, supply-chain developments, and competitive differentiation expected between 2026 and 2033. It highlights AI-enabled motion control, Industrial Ethernet integration, predictive maintenance, digital twins, and software-defined automation while evaluating investment priorities, expansion opportunities, localization strategies, partnership activity, and emerging application areas that influence long-term business positioning and industrial automation competitiveness.

| Report Attribute/Metric | Report Details |

|---|---|

Market Revenue in 2025 | USD 7539 Million |

Market Revenue in 2033 | USD 11658.02 Million |

CAGR (2026 - 2033) | 5.6% |

Base Year | 2025 |

Forecast Period | 2026 - 2033 |

Historic Period | 2021 - 2025 |

Segments Covered | By Type

By Application

By End-User

|

Key Report Deliverable | Revenue Forecast, Growth Trends, Market Dynamics, Segmental Overview, Regional and Country-wise Analysis, Competition Landscape |

Region Covered | North America, Europe, Asia-Pacific, South America, Middle East, Africa |

Key Players Analyzed | Siemens AG, Mitsubishi Electric Corporation, Yaskawa Electric Corporation, Schneider Electric SE, Delta Electronics, Inc., ABB Ltd., Rockwell Automation, Inc., Fuji Electric Co., Ltd., Bosch Rexroth AG, Beckhoff Automation GmbH & Co. KG, Omron Corporation, Panasonic Industry Co., Ltd., Nidec Corporation, Inovance Technology Co., Ltd. |

Customization & Pricing | Available on Request (10% Customization is Free) |