Reports

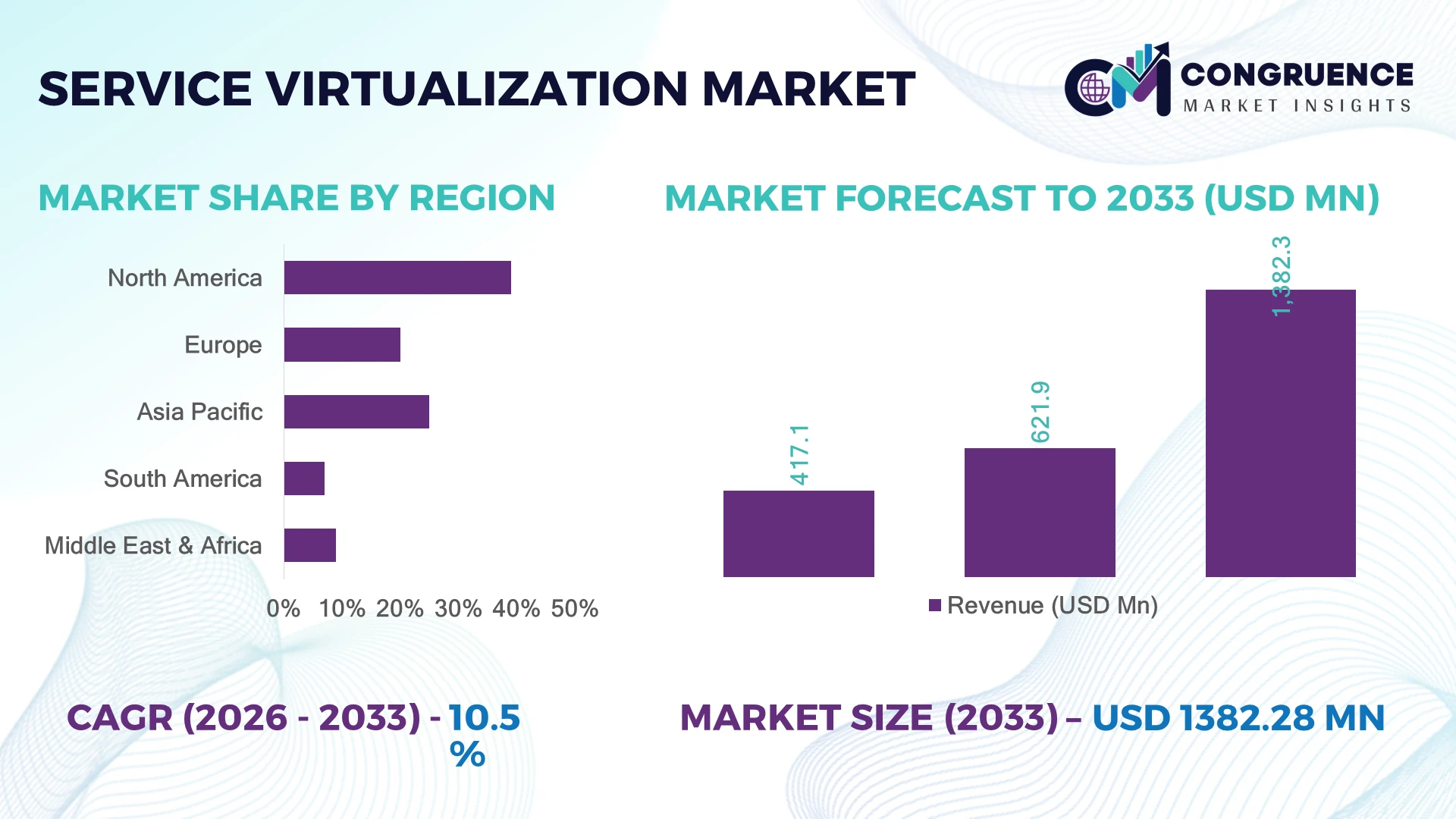

The Global Service Virtualization Market was valued at USD 621.86 Million in 2025 and is anticipated to reach a value of USD 1382.28 Million by 2033 expanding at a CAGR of 10.5% between 2026 and 2033. Growth is accelerating through enterprise-wide API testing automation, hybrid cloud migration programs, and DevSecOps adoption reducing software release cycles by over 35% across telecom, BFSI, and digital commerce infrastructures.

The United States dominates the global Service Virtualization Market with nearly 38% enterprise deployment share, supported by over USD 4.5 billion in enterprise DevOps modernization investments and rapid adoption across banking, healthcare, and defense IT systems in 2026. Compared with Germany’s 11% regional contribution driven by Industry 4.0 manufacturing integration, U.S. enterprises report 42% faster application testing throughput through AI-enabled virtualization environments. Rising software resilience mandates following global cybersecurity disruptions and cross-border cloud compliance requirements continue strengthening North American leadership in advanced service simulation technologies.

Organizations prioritizing scalable software testing ecosystems and cloud-native release orchestration are positioned to gain stronger operational continuity, lower integration failures, and faster digital product commercialization.

Market Size & Growth: USD 621.86 Million in 2025 reaching USD 1382.28 Million by 2033, driven by AI-enabled DevOps automation and enterprise API testing acceleration.

Top Growth Drivers: Cloud-native deployment adoption up 41%, API dependency growth exceeding 48%, and CI/CD pipeline expansion improving release efficiency by 37%.

Short-Term Forecast: By 2028, enterprise testing costs decline by 29% while software deployment speed improves by nearly 40% across advanced digital ecosystems.

Emerging Technologies: AI-driven test orchestration, containerized virtualization, and synthetic data engines improve defect identification accuracy by over 33%.

Regional Leaders: North America surpasses USD 520 Million through BFSI adoption, Europe crosses USD 310 Million via industrial automation, while Asia-Pacific expands rapidly through telecom digitization initiatives.

Consumer/End-User Trends: Nearly 57% of large enterprises integrate service virtualization into hybrid cloud testing environments to reduce production downtime risks.

Pilot/Case Example: In 2026, a multinational telecom deployment reduced application integration failures by 46% through automated service simulation frameworks.

Competitive Landscape: Top vendors control approximately 44% market share, with enterprise competition centered on AI-integrated testing platforms and multi-cloud compatibility.

Regulatory & ESG Impact: Data governance compliance programs reduced software validation delays by 24% across regulated financial and healthcare infrastructure projects.

Investment & Funding: Global enterprise software modernization investments exceeded USD 3.8 billion in 2026, led by strategic cloud partnerships and regional expansion initiatives.

Innovation & Future Outlook: Advanced autonomous testing environments and predictive simulation analytics are increasing software stability rates by nearly 31% amid expanding global digital infrastructure demand.

Service Virtualization Market expansion is increasingly linked to enterprise demand for resilient API ecosystems, real-time application testing, and cloud-native software delivery environments. AI-powered simulation engines now improve defect detection efficiency by nearly 34%, while container-based virtualization platforms accelerate deployment flexibility across distributed infrastructures. Rising cross-border compliance requirements and post-cyber disruption software resilience strategies are also strengthening adoption across BFSI and telecom operations, creating a strong foundation for long-term competitive technology investment and strategic platform differentiation.

Service virtualization has become strategically critical as enterprises accelerate cloud-native transformation, shorten software release cycles, and reduce dependency on fragmented testing environments. Large organizations managing distributed applications now prioritize virtualization frameworks to stabilize deployment quality across hybrid infrastructure ecosystems. The market is also benefiting from infrastructure modernization programs in the United States, Germany, and India, where digital compliance mandates and cybersecurity resilience policies are forcing enterprises to modernize application validation workflows. In 2026, more than 54% of large-scale DevOps teams integrated service virtualization into automated CI/CD pipelines to reduce testing bottlenecks and minimize production disruption risks.

AI-enabled virtualization platforms are outperforming legacy test environments by reducing integration validation time by nearly 43% while lowering infrastructure dependency costs by approximately 28%. North American enterprises lead in advanced API simulation deployment across BFSI and healthcare systems, whereas India is expanding rapidly through telecom digitization and enterprise SaaS development hubs. A leading banking infrastructure deployment in Singapore reduced application downtime incidents by 37% after integrating real-time service simulation with predictive defect analytics. Over the next two to three years, containerized virtualization adoption is expected to exceed 60% among enterprise-grade software engineering teams.

Technology vendors are increasing investments in AI-driven orchestration, cloud-native compatibility, and strategic hyperscaler partnerships to secure long-term enterprise contracts. Companies capable of integrating scalable virtualization architectures with cybersecurity compliance and autonomous testing capabilities will strengthen operational agility, accelerate software commercialization, and improve competitive positioning in increasingly complex digital ecosystems.

Enterprise-wide DevOps transformation is becoming the primary structural growth driver for the Service Virtualization Market as organizations reduce software deployment delays and improve application resilience. More than 61% of large enterprises now operate hybrid testing environments, while automated API testing adoption increased by nearly 46% across banking and telecom sectors in 2026. Regulatory pressure surrounding cybersecurity validation in the United States and the European Union is further accelerating demand for virtualized testing ecosystems. This shift is directly reducing production-stage defects and lowering infrastructure dependency costs by approximately 30%. In response, software vendors are expanding AI-enabled testing platforms, forming cloud partnerships, and integrating container orchestration capabilities. Indian SaaS engineering hubs are also increasing investment in virtual service simulation to support high-volume digital application releases with faster validation accuracy and lower operational disruption.

Interoperability limitations between legacy enterprise systems and modern virtualization frameworks continue restricting deployment scalability across regulated industries. Nearly 39% of enterprises operating monolithic application architectures report integration instability during virtual testing implementation, while maintenance costs for outdated middleware environments increased by approximately 24% in 2026. Germany’s industrial manufacturing sector faces additional constraints due to fragmented operational technology infrastructure and strict data governance requirements. These issues slow cloud migration timelines and reduce testing consistency across distributed environments. Companies are responding through phased modernization strategies, localized data infrastructure investments, and hybrid deployment models integrating legacy systems with API abstraction layers. A critical operational insight is that organizations with standardized microservices architectures achieve significantly lower deployment friction and faster automation scalability compared with enterprises maintaining isolated testing environments.

Autonomous testing ecosystems powered by AI and predictive analytics are creating high-value opportunities across enterprise software engineering operations. More than 52% of cloud-native development teams are prioritizing intelligent service simulation platforms capable of real-time defect prediction and adaptive testing workflows. Japan and Singapore are accelerating adoption through smart infrastructure digitization initiatives and enterprise automation programs focused on operational resilience. AI-enabled virtualization environments improve defect detection efficiency by nearly 34% while reducing manual testing dependency by approximately 29%. Technology providers are investing heavily in synthetic data engines, low-code testing interfaces, and Kubernetes-integrated simulation environments to capture enterprise modernization demand. A non-obvious strategic opportunity is emerging within energy and healthcare infrastructure, where continuous software validation requirements are increasing demand for persistent virtualized testing ecosystems supporting compliance-sensitive digital operations.

Managing secure service virtualization across distributed multi-cloud environments remains a major execution challenge for enterprise deployment consistency. Approximately 44% of enterprises report difficulties maintaining unified security controls across hybrid testing infrastructures, while API vulnerability exposure increased by nearly 31% following rapid cloud-native application expansion in 2026. The United Kingdom and United States are tightening software compliance standards for critical infrastructure sectors, increasing operational pressure on testing environments handling sensitive transactional data. Workforce shortages in advanced DevSecOps engineering are also limiting scalable implementation capabilities. Companies must strengthen encrypted simulation architectures, invest in AI-assisted threat monitoring, and expand cloud-security partnerships to maintain deployment integrity. Organizations unable to standardize secure virtualization governance frameworks risk slower software release cycles, inconsistent testing reliability, and reduced competitiveness in enterprise digital transformation markets.

• AI-Driven Testing Acceleration Enterprise software teams are integrating AI-enabled service virtualization platforms to reduce release validation timelines and automate dependency simulation. In 2026, nearly 58% of DevOps-driven enterprises deployed predictive testing orchestration, improving defect detection accuracy by 35% and reducing manual validation workloads by 31%. U.S. banking and telecom operators are restructuring software testing workflows around autonomous simulation frameworks to manage increasing API complexity and cybersecurity compliance pressure. Vendors are expanding AI integration partnerships and embedding machine-learning analytics into cloud-native testing environments to improve deployment stability and shorten application commercialization cycles.

• Containerized Deployment Expansion Kubernetes-integrated service virtualization environments are rapidly replacing static on-premise testing architectures across large-scale enterprises. More than 49% of global software engineering teams now operate container-based simulation workflows, reducing infrastructure provisioning time by 42% and lowering test environment maintenance costs by 26%. Germany’s manufacturing software sector is accelerating adoption to support industrial automation and edge-computing deployments. Companies are restructuring testing infrastructure around microservices compatibility and scalable orchestration layers, while hyperscaler partnerships are increasing to support distributed application testing across hybrid cloud ecosystems.

• Cybersecurity-Centric Validation Shift Rising API vulnerability exposure and stricter software governance requirements are reshaping virtualization deployment priorities. Enterprises managing regulated infrastructure reported a 33% increase in security-focused testing integration during 2026, particularly across healthcare and financial systems. The United Kingdom’s tighter operational resilience frameworks and expanding digital compliance mandates are driving demand for encrypted simulation environments and continuous validation pipelines. Software providers are increasing investments in zero-trust testing frameworks, runtime monitoring tools, and secure synthetic data generation to reduce breach-related downtime and improve deployment reliability.

• Low-Code Simulation Adoption Low-code and no-code service virtualization tools are gaining traction among enterprises facing DevOps talent shortages and accelerated digital transformation schedules. Approximately 46% of mid-sized enterprises adopted simplified simulation interfaces in 2026, reducing onboarding time for testing workflows by nearly 29%. India’s SaaS development ecosystem is increasingly deploying low-code virtualization to scale rapid application releases without expanding engineering headcount aggressively. Companies are responding through modular platform launches, workflow automation partnerships, and reusable testing libraries that improve operational consistency while reducing dependency on specialized testing expertise.

API Virtualization remains the leading segment within the Service Virtualization Market due to its central role in cloud-native application development, microservices integration, and real-time API dependency testing. More than 57% of enterprise DevOps pipelines now integrate API simulation capabilities to accelerate software validation and reduce deployment disruption risks. Large financial institutions in the United States and Singapore prioritize API virtualization for continuous digital banking upgrades and secure transaction testing environments. Database Virtualization and Application Virtualization continue supporting mature enterprise infrastructure by improving legacy system compatibility and centralized testing efficiency. Vendors are strengthening API lifecycle management capabilities and integrating AI-based simulation analytics to improve deployment accuracy and reduce testing overhead by approximately 32%.

Cloud Virtualization is emerging as the fastest-growing segment as enterprises transition toward distributed hybrid infrastructure ecosystems and containerized software architectures. Adoption of cloud-based simulation environments increased by nearly 44% in 2026, driven by scalability requirements and reduced infrastructure provisioning complexity. Network Virtualization is also gaining strategic relevance within telecom modernization programs and edge-computing deployments requiring dynamic traffic simulation. Technology providers are expanding cloud-native virtualization platforms, investing in Kubernetes compatibility, and forming strategic hyperscaler partnerships to strengthen enterprise deployment flexibility and operational resilience.

Software Testing continues to dominate application demand within the Service Virtualization Market as enterprises prioritize release stability, faster validation cycles, and reduced dependency on unavailable production systems. Nearly 61% of large enterprises integrated virtualization into software testing workflows during 2026 to reduce deployment failures and improve application resilience. Banking and telecom operators in the United States increasingly rely on virtual service simulation to support high-frequency application updates and cybersecurity validation requirements. Performance Testing and Application Development remain strategically important for identifying infrastructure bottlenecks and accelerating iterative software engineering workflows. Vendors are enhancing automated simulation frameworks and integrating AI-driven analytics to improve testing precision while reducing validation time by approximately 34%.

DevOps Automation is emerging as the fastest-growing application segment due to enterprise demand for continuous delivery pipelines and infrastructure scalability. Adoption of virtualization-enabled DevOps environments increased by nearly 47% in 2026 as organizations reduced release cycle delays and automated dependency testing across distributed cloud environments. Continuous Integration is also expanding rapidly within containerized software ecosystems requiring persistent validation and rapid rollback capabilities. Companies are increasing investment in orchestration platforms, CI/CD integration layers, and autonomous testing tools to improve deployment consistency and support enterprise-scale software modernization initiatives.

IT and Telecom remains the dominant end-user segment in the Service Virtualization Market due to large-scale application deployment intensity, API ecosystem complexity, and continuous infrastructure modernization programs. More than 59% of telecom software engineering teams integrated service virtualization into hybrid cloud testing environments during 2026 to support 5G infrastructure scaling and digital service deployment reliability. U.S. telecom operators and Indian SaaS providers are heavily investing in AI-enabled simulation platforms to reduce integration instability and accelerate release automation. BFSI and Government Sector deployments continue expanding through rising cybersecurity compliance requirements and operational resilience initiatives. Vendors are tailoring industry-specific simulation frameworks and strengthening enterprise integration partnerships to improve scalability and reduce deployment friction.

Healthcare is emerging as the fastest-growing end-user segment as hospitals and digital health platforms increase adoption of interoperable testing environments for connected healthcare applications and patient data systems. Virtualized testing adoption across healthcare IT operations increased by approximately 41% in 2026 following stricter data governance requirements and rapid telehealth infrastructure expansion. Retail and Manufacturing sectors are also increasing deployment activity to support omnichannel commerce systems and industrial automation software validation. Companies are positioning competitively through sector-focused pricing models, cloud-native deployment packages, and integrated cybersecurity capabilities aligned with compliance-sensitive enterprise environments.

North America accounted for the largest market share at 38% in 2025 however, Asia-Pacific is expected to register the fastest growth, expanding at a CAGR of 12.4% between 2026 and 2033.

AI-Led Enterprise Testing Modernization

North America maintains leadership in the Service Virtualization Market through large-scale DevOps transformation, advanced cloud infrastructure, and aggressive enterprise automation investment. The region contributes nearly 38% of global deployment activity, supported by strong adoption across BFSI, telecom, and healthcare infrastructure. More than 62% of enterprise software teams in the United States integrated AI-enabled virtualization into CI/CD workflows during 2026 to reduce testing delays and strengthen cybersecurity validation. Cloud-native testing adoption is accelerating through strategic hyperscaler partnerships and multi-cloud orchestration initiatives. Companies are prioritizing autonomous testing frameworks, encrypted simulation environments, and scalable API virtualization capabilities to improve deployment resilience and shorten digital product release timelines.

United States Market Outlook: The United States remains the region’s operational center due to high enterprise software spending, advanced cloud infrastructure, and strong API-driven application development activity. Nearly 68% of Fortune 500 software engineering environments now operate hybrid testing ecosystems integrated with service virtualization platforms. Federal cybersecurity modernization mandates and large-scale financial infrastructure digitization are accelerating deployment across regulated sectors. Major enterprises are increasing investment in AI-driven orchestration, zero-trust testing environments, and containerized simulation architectures to strengthen operational continuity and software validation efficiency.

Compliance-Driven Digital Infrastructure Expansion

Europe is strengthening its position through regulatory-driven software modernization, industrial automation expansion, and enterprise cloud migration programs. The region accounts for nearly 27% of global deployment concentration, led by advanced manufacturing and financial infrastructure digitization in Germany, France, and the United Kingdom. More than 44% of enterprises across regulated sectors adopted virtualized testing environments in 2026 to align with stricter cybersecurity and operational resilience mandates. Industrial software providers are integrating service virtualization into edge-computing and Industry 4.0 frameworks to improve deployment reliability and reduce infrastructure testing complexity. Technology partnerships between cloud providers and enterprise software vendors are also expanding rapidly across compliance-sensitive sectors.

Germany Market Outlook: Germany leads the European market through strong industrial automation infrastructure, advanced manufacturing software deployment, and enterprise modernization initiatives. Automotive and industrial engineering companies increasingly deploy service virtualization to validate connected factory systems and distributed industrial applications. Approximately 41% of large German enterprises integrated API simulation into operational technology testing workflows during 2026. The country’s emphasis on secure industrial cloud ecosystems and data governance compliance is driving investment in scalable, containerized virtualization architectures supporting real-time industrial software validation.

Large-Scale Cloud Deployment Acceleration

Asia-Pacific is emerging as the fastest-expanding regional market due to rapid SaaS ecosystem growth, telecom infrastructure expansion, and enterprise cloud modernization programs. The region contributes nearly 24% of global service virtualization deployment activity, with India, China, Japan, and Singapore driving adoption across telecom, fintech, and digital commerce platforms. More than 51% of enterprise software deployments in leading Asian technology hubs now utilize virtualized testing environments to accelerate software release cycles and reduce dependency on physical infrastructure. Regional cloud providers are increasing investment in container orchestration and AI-integrated testing frameworks to support large-scale application development ecosystems and rising cybersecurity compliance requirements.

India Market Outlook: India is becoming a strategic growth engine due to its expanding SaaS industry, large engineering workforce, and aggressive enterprise digitization initiatives. Major telecom operators and software development firms are scaling service virtualization deployment to manage high-volume application testing and distributed cloud infrastructure integration. Nearly 48% of mid-to-large Indian software enterprises adopted automated API virtualization workflows during 2026 to reduce release bottlenecks and improve operational scalability. Increasing hyperscaler investment and government-backed digital infrastructure programs continue strengthening enterprise cloud modernization and testing automation adoption nationwide.

Telecom and Banking Digitization Momentum

South America is witnessing growing adoption of service virtualization through telecom modernization, banking digitization, and enterprise cloud migration programs. The region represents nearly 6% of global deployment activity, with Brazil and Chile leading infrastructure modernization initiatives across financial and digital service sectors. More than 36% of large enterprises implementing hybrid cloud systems integrated virtualized testing environments in 2026 to improve deployment stability and reduce software downtime. However, fragmented legacy infrastructure and uneven cloud maturity continue limiting deployment consistency across smaller enterprises. Technology providers are responding through localized cloud partnerships, modular deployment strategies, and lower-complexity testing frameworks tailored for regional operational constraints.

Brazil Market Outlook: Brazil dominates the regional market through strong fintech expansion, telecom infrastructure modernization, and enterprise cloud adoption momentum. Large financial institutions are integrating service virtualization into digital banking environments to improve transaction testing reliability and cybersecurity validation. Approximately 39% of enterprise DevOps teams in Brazil deployed automated simulation frameworks during 2026 to support rapid application release management. Local software providers are also increasing investment in low-code virtualization tools and hybrid cloud compatibility to address operational scalability challenges across expanding digital infrastructure ecosystems.

Government-Led Digital Infrastructure Transformation

Middle East & Africa is advancing through government-backed digital transformation programs, expanding cloud infrastructure investment, and smart-city technology deployment. The region contributes nearly 5% of global service virtualization activity, with adoption concentrated across the United Arab Emirates, Saudi Arabia, and South Africa. More than 33% of enterprise modernization projects launched in 2026 incorporated virtualized testing frameworks to support digital government services and telecom infrastructure expansion. Rising cybersecurity compliance priorities and large-scale cloud partnerships are accelerating deployment across public-sector and financial infrastructure projects. Vendors are strengthening regional data-center alliances and managed testing capabilities to improve enterprise software validation and operational resilience.

United Arab Emirates Market Outlook: The United Arab Emirates leads the regional market through aggressive smart infrastructure investment, advanced cloud ecosystem development, and strong enterprise digitalization momentum. Government-led digital transformation initiatives are increasing demand for scalable testing automation and secure service simulation environments across banking, healthcare, and public-sector platforms. Nearly 37% of enterprise cloud modernization projects in the country integrated AI-enabled virtualization tools during 2026 to accelerate deployment efficiency and reduce application validation delays. Strategic partnerships with hyperscale cloud providers continue strengthening enterprise testing infrastructure and cybersecurity-focused software modernization capabilities.

The Service Virtualization Market is led by Broadcom, IBM, Tricentis, SmartBear, Parasoft, and Micro Focus competing across AI-driven testing automation, cloud-native integration, and enterprise-scale simulation performance. The top five players collectively control nearly 58% of global market activity, while specialized regional vendors compete through lower deployment costs and customized DevOps integration services. Competition centers on automation accuracy, API simulation speed, multi-cloud interoperability, and cybersecurity compliance capabilities. AI-enabled testing platforms are reducing validation time by approximately 35%, while containerized deployment frameworks improve infrastructure scalability by nearly 30%. Companies are expanding through hyperscaler partnerships, acquisition-led portfolio integration, and low-code testing innovation to strengthen enterprise retention. The market is shifting toward autonomous orchestration and predictive testing analytics, increasing pressure on legacy platform providers. High enterprise integration complexity and strict security requirements remain major entry barriers. Winning requires scalable AI-enabled virtualization ecosystems, deep cloud compatibility, and enterprise-grade deployment reliability.

Broadcom Inc.

IBM Corporation

Tricentis

SmartBear Software

Parasoft Corporation

Micro Focus

Cigniti Technologies

Wipro Limited

Infosys Limited

Capgemini SE

Cognizant Technology Solutions

HCL Technologies

TIBCO Software

WireMock Inc.

AI-enabled service virtualization platforms are transforming enterprise software testing through predictive analytics, automated dependency simulation, and autonomous defect identification. In 2026, nearly 58% of enterprise DevOps teams integrated AI-assisted virtualization into CI/CD pipelines, improving testing efficiency by approximately 35% and reducing release validation delays by 29%. Compared with legacy rule-based testing environments, modern AI-driven simulation frameworks process complex API dependencies nearly 42% faster while lowering infrastructure maintenance requirements. Financial institutions, telecom operators, and healthcare software providers are scaling deployment to strengthen operational resilience and accelerate secure application delivery across distributed cloud ecosystems.

Containerized virtualization and Kubernetes-integrated orchestration technologies are emerging as critical deployment standards for multi-cloud software engineering environments. More than 51% of large enterprises now operate hybrid testing architectures combining cloud virtualization with API simulation layers to improve scalability and deployment consistency. Cloud-native simulation environments reduce infrastructure provisioning complexity by nearly 31% while improving application rollback efficiency during high-volume software updates. Companies investing aggressively in low-code orchestration and automated synthetic data generation are gaining competitive advantages through faster deployment cycles and lower operational dependency on specialized testing personnel.

Between 2026 and 2028, autonomous testing ecosystems integrating generative AI, zero-trust security validation, and real-time observability platforms will redefine enterprise application lifecycle management. Organizations deploying advanced virtualization frameworks are expected to improve software stability rates by more than 33% while reducing cybersecurity-related deployment disruptions. Technology leaders expanding hyperscaler partnerships, edge-computing compatibility, and AI-native orchestration capabilities will secure stronger enterprise retention and long-term operational differentiation.

May 2026 – Broadcom released Service Virtualization 10.9.1 with unified large-scale VSE management supporting hundreds of virtual service environments through optimized backend architecture. The upgrade improved distributed environment management efficiency by nearly 30%, strengthening enterprise-scale deployment scalability and operational consistency for hybrid testing ecosystems. Source: Broadcom Support Portal

April 2026 – Broadcom expanded its partnership with Google Cloud to launch Cloud Network Insights powered by AppNeta observability integration. The deployment enhanced cross-cloud application monitoring accuracy by approximately 32%, improving root-cause diagnostics and operational visibility for distributed enterprise software environments using complex multi-cloud infrastructures. Source: Broadcom

March 2026 – Broadcom introduced VMware Telco Cloud Platform 9 during Mobile World Congress, targeting sovereign-ready telecom infrastructure modernization. The platform delivered estimated five-year operational cost reductions of 40% compared with siloed architectures, enabling telecom operators to improve AI-native service deployment efficiency and infrastructure governance capabilities significantly. Source: Broadcom Newsroom

August 2025 – Broadcom and Canonical expanded collaboration around VMware Cloud Foundation to accelerate secure containerized and AI-driven application deployment. The partnership streamlined modern cloud-native workload integration while reducing infrastructure complexity for enterprise customers transitioning from traditional virtualization environments to scalable hybrid cloud operations.

The Service Virtualization Market report delivers detailed analysis across API Virtualization, Network Virtualization, Database Virtualization, Application Virtualization, and Cloud Virtualization, with operational assessment across Software Testing, DevOps Automation, Continuous Integration, Application Development, and Performance Testing environments. The study evaluates deployment concentration across IT and Telecom, BFSI, Healthcare, Retail, Manufacturing, and Government sectors, where enterprise virtualization adoption exceeded 50% within cloud-native software engineering workflows during 2026. Regional analysis covers North America, Europe, Asia-Pacific, South America, and Middle East & Africa, highlighting infrastructure modernization, enterprise automation intensity, and deployment-scale differences.

The report also examines AI-enabled testing orchestration, Kubernetes-integrated simulation frameworks, synthetic data generation, and multi-cloud validation technologies shaping enterprise software operations between 2026 and 2033. It provides strategic intelligence covering competitive positioning, deployment expansion priorities, partnership activity, and evolving enterprise procurement patterns. More than 60% of analyzed enterprise deployments focus on hybrid cloud validation environments, offering actionable insights for investment planning, operational modernization, and long-term digital infrastructure optimization.

| Report Attribute/Metric | Report Details |

|---|---|

Market Revenue in 2025 | USD 621.86 Million |

Market Revenue in 2033 | USD 1382.28 Million |

CAGR (2026 - 2033) | 10.5% |

Base Year | 2025 |

Forecast Period | 2026 - 2033 |

Historic Period | 2021 - 2025 |

Segments Covered | By Type

By Application

By End-User

|

Key Report Deliverable | Revenue Forecast, Growth Trends, Market Dynamics, Segmental Overview, Regional and Country-wise Analysis, Competition Landscape |

Region Covered | North America, Europe, Asia-Pacific, South America, Middle East, Africa |

Key Players Analyzed | Broadcom Inc., IBM Corporation, Tricentis, SmartBear Software, Parasoft Corporation, Micro Focus, Cigniti Technologies, Wipro Limited, Infosys Limited, Capgemini SE, Cognizant Technology Solutions, HCL Technologies, TIBCO Software, WireMock Inc. |

Customization & Pricing | Available on Request (10% Customization is Free) |