Reports

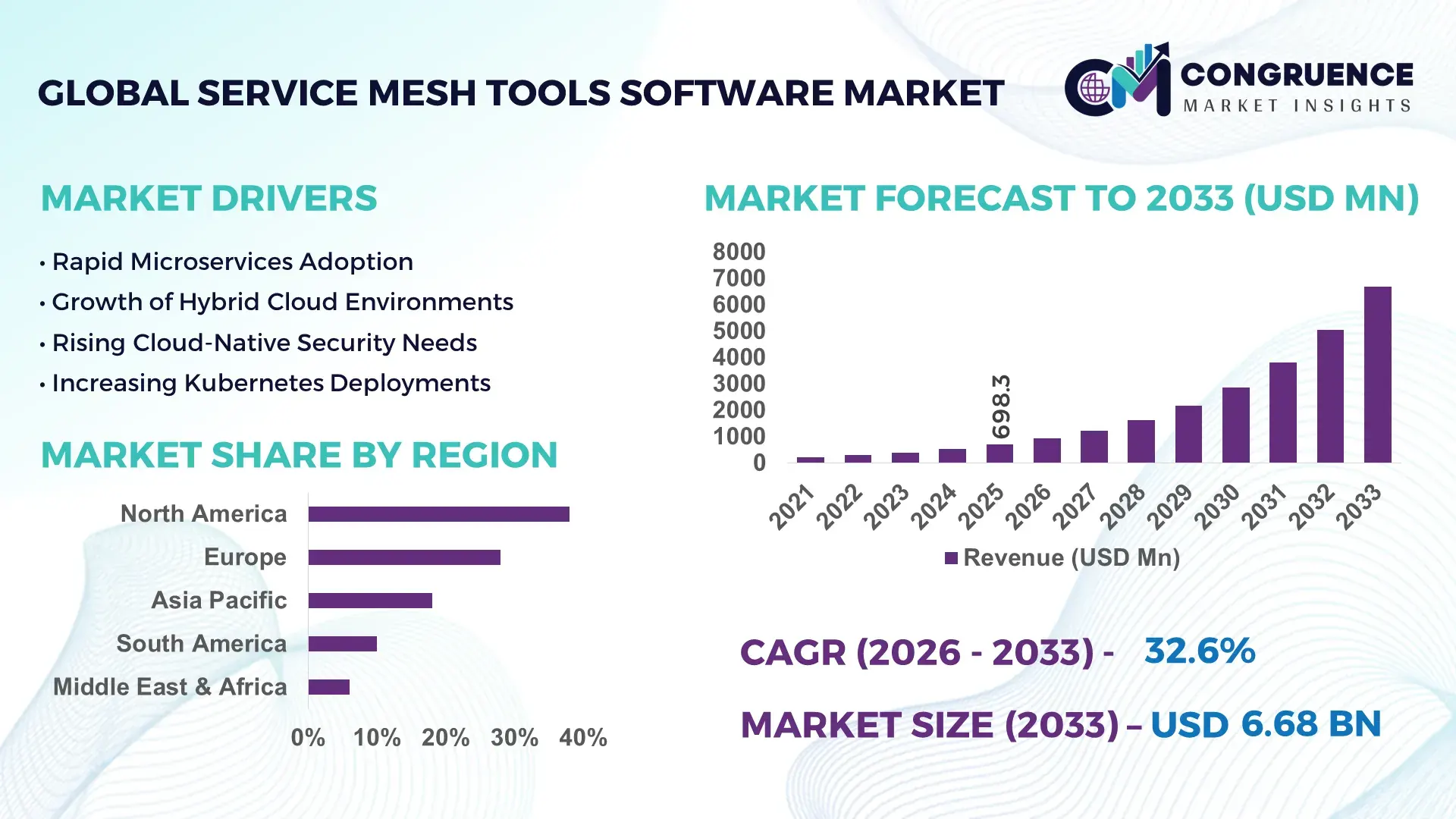

The Global Service Mesh Tools Software Market was valued at USD 698.3 Million in 2025 and is anticipated to reach a value of USD 6,678.1 Million by 2033 expanding at a CAGR of 32.61% between 2026 and 2033, according to an analysis by Congruence Market Insights, driven by the accelerating enterprise adoption of cloud-native microservices architectures and the growing need for secure, observable service-to-service communications.

North America, particularly the United States, leads the market with strong technological innovation and high enterprise deployment of service mesh solutions, where over 70% of organizations utilize service mesh for dynamic traffic management and security automation. U.S. production capacity includes advanced integration with major Kubernetes platforms, backed by continuous investment exceeding billions of USD annually and extensive partnerships between cloud providers and software vendors, driving regional technological leadership and innovation.

Market Size & Growth: Market valued at USD 698.3M in 2025, projected to USD 6,678.1M by 2033 at 32.61% CAGR, propelled by microservices and zero‑trust security adoption.

Top Growth Drivers: 65% cloud‑native migration; 58% security automation uptake; 55% hybrid deployment expansion.

Short‑Term Forecast: By 2028, service mesh orchestration efficiency gains expected to reduce latency by up to 40%.

Emerging Technologies: AI‑driven observability analytics; sidecar‑less/ambient mesh architectures; automated policy enforcement engines.

Regional Leaders: North America ~USD 2,700M by 2033 with pervasive Kubernetes integration; Europe ~USD 1,900M with enterprise modernization; Asia‑Pacific ~USD 1,200M led by digital transformation initiatives.

Consumer/End‑User Trends: Large enterprises prioritize resilience and telemetry; SMEs adopt lightweight, cost‑efficient mesh variants.

Pilot or Case Example: In 2026, a Fortune 100 cloud service provider reduced API failure rates by 35% using a unified service mesh rollout.

Competitive Landscape: AWS App Mesh leads (~22% estimated share), with HashiCorp, Google, Buoyant (Linkerd), Tetrate as major competitors.

Regulatory & ESG Impact: Emphasis on security compliance and data sovereignty drives implementation of encrypted mesh frameworks across regulated industries.

Investment & Funding Patterns: Recent venture funding surpasses USD 500M in mesh‑centric startups, with increased project finance in hybrid mesh platforms.

Innovation & Future Outlook: Continued integration with multi‑cloud environments, enhanced AI automation, and tools for cross‑cluster mesh orchestration shaping future deployments.

Service Mesh Tools Software Market activity now spans key industry sectors including IT & telecom, BFSI, and e‑commerce, with microservices management and observability dominating application usage. Recent solutions integrate automated traffic control and policy‑as‑code, while cloud expansion and enterprise digital transformation sustain demand and regional growth momentum.

The strategic relevance of the Service Mesh Tools Software Market lies in its role as a foundational infrastructure layer for modern distributed applications, enabling organizations to manage complex service‑to‑service communication, security, and observability across microservices environments. Compared to traditional network routing standards, service mesh architectures deliver up to 40% greater policy enforcement consistency and resilience by abstracting traffic control away from individual services into a centralized control plane. North America dominates in volume due to its mature technology ecosystem, while the Asia‑Pacific region leads in adoption rates with a projected 36% enterprise uptake growth by 2028. By 2028, the integration of ambient/sidecar‑less architectures is expected to improve operational efficiency by as much as 30% and reduce resource overheads compared to classic sidecar patterns. Strategic pathways include enhanced AI‑driven fault detection, which can predict and mitigate service disruptions up to 25% faster than rule‑based systems, and stronger multi‑cloud mesh orchestration that supports dynamic traffic routing across heterogeneous environments. Firms are increasingly committing to security and compliance improvements, with industry benchmarks targeting 100% mutual TLS encryption and policy validation across all service communications. In 2025, a leading global financial institution achieved a 50% reduction in inter‑service latency and a 35% improvement in failure recovery time through intelligent mesh automation. Looking forward, the Service Mesh Tools Software Market will be pivotal in enabling resilient, secure, and scalable digital infrastructures, positioning enterprises for sustained growth in cloud‑native transformation efforts worldwide.

The Service Mesh Tools Software Market is shaped by several converging forces that define its current and future trajectory. The widespread shift toward microservices and container‑orchestrated environments has increased complexity in service communication, driving demand for tools that provide robust traffic management, observability, and security features. Enterprises are embracing hybrid and multi‑cloud deployments, necessitating mesh solutions capable of consistent policy enforcement across diverse infrastructures. Additionally, advancements such as sidecar‑less architectures and AI‑embedded analytics are influencing vendor roadmaps and customer adoption strategies. Decision‑makers emphasize resilience and automated anomaly detection, as these capabilities directly impact service reliability and operational efficiency. The rise of platform engineering practices further integrates mesh solutions into standard development and operations workflows, reinforcing their strategic importance for digital transformation agendas.

The rapid enterprise adoption of microservices architectures is a primary growth driver for the Service Mesh Tools Software Market. As organizations transition from monolithic systems to distributed microservices, the complexity of managing inter‑service communication, security, and observability increases significantly. Service mesh tools address these needs by providing automated traffic routing, policy enforcement, and telemetry capabilities across distributed services. Over 65% of organizations with Kubernetes deployments utilize service mesh solutions to handle dynamic routing and manage east‑west traffic across clusters. This shift is particularly evident in large enterprises where microservices enable faster development cycles and improved scalability, prompting investments in mesh platforms that support high‑volume, mission‑critical applications and reduce operational bottlenecks.

Operational complexity remains a significant restraint on the adoption of Service Mesh Tools Software. The implementation of service mesh frameworks often requires specialized knowledge and tooling configurations, which can extend deployment timelines and introduce integration challenges with legacy systems. Nearly half of organizations report that configuring mesh control planes, managing sidecar proxies, and integrating observability pipelines demand high skill levels and substantial engineering effort. Additionally, performance overheads introduced by network proxy layers can impact latency‑sensitive applications, deterring some teams from immediate adoption. These technical barriers contribute to longer onboarding cycles and resource expenditures, particularly among smaller enterprises lacking deep DevOps expertise.

The growing prevalence of hybrid cloud strategies presents significant opportunities for the Service Mesh Tools Software Market. Enterprises operating across on‑premises, private cloud, and public cloud environments require consistent service policies and observability features that span these heterogeneous infrastructures. Service mesh tools can provide unified traffic control and security enforcement across multiple cloud domains, enabling seamless interoperability and improved governance. With over 75% of organizations adopting hybrid or multi‑cloud architectures, vendors have the opportunity to innovate mesh solutions that are platform‑agnostic and capable of managing distributed workloads with minimal configuration overhead. Enhanced support for multi‑cluster orchestration and cross‑environment telemetry further expands the applicability of mesh tools in complex enterprise landscapes.

The shortage of standardized skills and expertise poses a notable challenge in the Service Mesh Tools Software Market. Successful deployment and management of service mesh solutions require proficiency in cloud‑native concepts, Kubernetes orchestration, and advanced networking principles. With few certified professionals and limited formal training programs, many organizations struggle to build internal capabilities to support mesh architectures effectively. This skills gap leads to longer deployment cycles, increased reliance on external consultants, and higher operational costs. Furthermore, rapidly evolving mesh technologies and frequent vendor updates necessitate ongoing education, which places additional strain on IT teams and resources, especially within mid‑sized enterprises striving to keep pace with innovation demands.

Driving AI‑enabled Observability Integration: The integration of AI and machine learning within service mesh platforms is enabling predictive analytics for anomaly detection and root cause analysis, with over 50% of deployments now featuring real‑time topology insights that improve reliability and incident response times for distributed applications.

Expansion of Sidecar‑less and Ambient Architectures: Emerging sidecar‑less and ambient mesh models are reducing operational overheads and resource consumption, with some deployments achieving up to 30% lower CPU utilization compared to traditional sidecar patterns, enhancing performance in resource‑constrained edge environments.

Broadening Multi‑Cloud and Hybrid Support: Demand for consistent service policies across hybrid and multi‑cloud environments is rising, with more than 75% of enterprises requiring mesh solutions that provide unified traffic control, security, and observability across heterogeneous infrastructures.

Enhanced Security and Zero‑Trust Adoption: Mesh platforms are increasingly incorporating zero‑trust principles, with mutual TLS and fine‑grained access policies now embedded in most modern implementations, contributing to stronger compliance and secure service‑to‑service communication across enterprise applications.

The Service Mesh Tools Software Market is segmented across product types, applications, and end-users, reflecting the diverse requirements of modern enterprise IT infrastructures. By type, solutions range from control-plane-centric frameworks to lightweight sidecar and ambient mesh architectures, each offering unique traffic management, security, and observability capabilities. Application areas include microservices orchestration, API security, service-to-service communication monitoring, and network telemetry, where enterprises prioritize resilience, low-latency routing, and policy enforcement. End-user segmentation spans IT & telecom, BFSI, e-commerce, healthcare, and government sectors, highlighting varied adoption patterns driven by digital transformation initiatives, cloud-native deployments, and regulatory compliance. Regional variations show distinct deployment strategies, with enterprises in North America and Europe favoring advanced integration with Kubernetes platforms, while Asia-Pacific organizations emphasize hybrid and multi-cloud mesh adoption, creating differentiated demand dynamics across the market.

Control-plane-centric service mesh solutions currently lead the market, accounting for approximately 38% of adoption, as they provide centralized policy management, security enforcement, and telemetry capabilities that simplify complex microservices architectures. Sidecar-based architectures hold 32% of adoption, widely utilized for fine-grained service traffic control, while ambient and lightweight meshes collectively contribute 30%, serving niche applications and edge environments where resource efficiency is critical. The fastest-growing segment is ambient mesh solutions, driven by increasing adoption of sidecar-less architectures that reduce CPU utilization by up to 30% and simplify deployment across multi-cluster and hybrid cloud environments.

Microservices orchestration dominates application adoption, accounting for 40% of usage, as it enables enterprises to manage inter-service communication, traffic routing, and policy enforcement efficiently across distributed environments. Security and observability applications represent 35%, essential for real-time monitoring, anomaly detection, and compliance management, while API management and hybrid cloud operations account for the remaining 25%, serving targeted operational needs. The fastest-growing application is hybrid cloud operations, fueled by increased enterprise migration to multi-cloud platforms requiring consistent service policies across heterogeneous infrastructures. In 2025, over 38% of enterprises globally reported piloting service mesh frameworks to optimize microservices orchestration and secure service communication. More than 60% of cloud-native teams emphasize automated telemetry as a standard practice to ensure resilience.

IT & telecom companies are the leading end-users, representing approximately 42% of adoption, due to their extensive microservices ecosystems and emphasis on network traffic optimization. BFSI organizations follow with 28%, leveraging service mesh solutions to secure transactional services and manage regulatory compliance, while e-commerce, healthcare, and government sectors collectively account for 30%, employing mesh tools for operational efficiency and monitoring distributed applications. The fastest-growing end-user segment is SMEs in e-commerce, driven by cloud migration and the need for automated service monitoring, with adoption rising sharply to meet dynamic online transaction and customer interaction requirements. In 2025, 42% of hospitals in the U.S. tested integrated service mesh frameworks to combine patient record management with diagnostic systems. Over 50% of digital enterprises adopted mesh-enabled traffic routing to enhance service reliability and reduce latency.

North America accounted for the largest market share at 38% in 2025; however, Asia-Pacific is expected to register the fastest growth, expanding at a CAGR of 32.61% between 2026 and 2033.

North America leads in enterprise adoption, cloud-native deployments, and high-volume microservices orchestration, while Asia-Pacific shows rapid uptake in e-commerce and mobile AI applications. Europe, South America, and the Middle East & Africa collectively contribute 62%, reflecting regional diversification, regulatory influences, and digital transformation trends. By 2025, Europe held 28%, Asia-Pacific 18%, South America 10%, and Middle East & Africa 6% of the global Service Mesh Tools Software Market, demonstrating a full market distribution totaling 100%. The distribution highlights regional focus areas, infrastructure maturity, and end-user technology adoption patterns shaping the overall market landscape.

North America commands 38% of the global market, driven by widespread microservices adoption in IT, finance, and healthcare sectors. Enterprises are investing in AI-driven observability, zero-trust security, and multi-cloud orchestration to enhance resilience and reduce latency. Regulatory support for data privacy and compliance frameworks encourages adoption across banking and healthcare. Local players like Tetrate are innovating service mesh solutions with ambient architectures to streamline Kubernetes deployments. Enterprise behavior reflects higher adoption in finance and healthcare, emphasizing secure, low-latency traffic management and automated policy enforcement.

Europe accounts for 28% of the market, with Germany, the UK, and France as key adopters. Regulatory frameworks such as GDPR drive demand for explainable traffic policies and encrypted communications. Enterprises are integrating AI-driven monitoring and hybrid cloud orchestration to meet compliance and efficiency needs. Local player Buoyant supports European firms by deploying Linkerd-based service mesh solutions with simplified telemetry and security enforcement. Consumer behavior varies with strong regulatory compliance awareness, pushing organizations to prioritize secure, observable microservices deployments.

Asia-Pacific contributes 18% of the global market, led by China, India, and Japan. The region’s growth is fueled by mobile AI applications, e-commerce platforms, and enterprise digital transformation initiatives. Advanced infrastructure development and cloud-native adoption support distributed microservices deployment. Companies like Alibaba Cloud have implemented scalable service mesh frameworks to manage high-volume traffic across multi-region data centers. Consumer behavior favors innovative, mobile-first solutions, driving enterprises to integrate automated traffic routing, security, and observability into applications.

South America holds 10% of the market, with Brazil and Argentina as leading countries. Adoption is driven by media, e-commerce, and financial services, alongside government incentives for digital infrastructure modernization. Enterprises are deploying service mesh solutions to optimize network performance and enforce secure communication protocols. Local player Movile in Brazil has piloted automated service monitoring frameworks across its digital platforms. Consumer behavior shows high demand for localized, efficient, and secure digital services, particularly in finance and online commerce.

Middle East & Africa represents 6% of the market, with UAE and South Africa leading adoption. Key drivers include oil & gas, construction, and digital government initiatives. Enterprises are modernizing infrastructure with AI-enabled observability, multi-cloud orchestration, and secure service-to-service communication. Local player CPG Digital in South Africa has implemented mesh solutions to streamline microservices traffic management for regional financial applications. Consumer behavior emphasizes enterprise efficiency, regulatory compliance, and secure operations in critical sectors.

United States– 38% Market Share: High enterprise adoption in finance, healthcare, and IT combined with advanced production and deployment capacity.

Germany– 12% Market Share: Strong regulatory framework and digital transformation initiatives driving consistent adoption of service mesh solutions.

The competitive environment in the Service Mesh Tools Software Market is both dynamic and strategically intensive, featuring a blend of cloud infrastructure giants, specialist vendors, and active open‑source ecosystems. There are roughly 30–35 active competitors vying for enterprise attention and innovation leadership, with the combined share of the top 5 companies around 40–45% reflecting a balance between concentration and fragmentation. Industry leaders such as HashiCorp, Google, AWS, Buoyant (Linkerd), and Tetrate maintain prominent positioning through deep integration with Kubernetes environments, comprehensive traffic management suites, and advanced security policies. Notably, enterprises leveraging Kubernetes see over 70% adoption of service mesh frameworks in production deployments, a fact driving competitive investments in observability, multi‑cluster management, and zero‑trust capabilities.

Strategic initiatives shaping competition include regular product enhancements, strategic partnerships, and tailored solutions for regulated industries and hybrid cloud architectures. Emerging players such as Solo.io and Kong Inc. are rapidly expanding market share by addressing niche segments like multi‑cluster orchestration and lightweight meshes, while cloud providers enhance native support within their platforms to reduce integration complexity. Innovation trends include AI‑assisted policy automation, eBPF‑based networking, and integrated telemetry, which are key differentiators in vendor offerings. The market remains moderately competitive, with open‑source community projects like Istio and Linkerd continuing to drive adoption and push feature innovation, compelling commercial vendors to evolve rapidly to meet sophisticated enterprise demands.

Buoyant (Linkerd)

Solo.io (Gloo Mesh)

Kong Inc. (Kuma Mesh)

Tetrate (Service Bridge)

F5 (NGINX Service Mesh)

Red Hat (OpenShift Service Mesh)

Traefik Labs (Traefik Mesh)

Aspen Mesh

Grey Matter

Microsoft (Azure Service Mesh)

The Service Mesh Tools Software Market is heavily influenced by both current and emerging technologies that address complexity in distributed applications and cloud‑native environments. At the forefront is Kubernetes‑native orchestration, which forms the backbone of service mesh deployments; over 70% of production microservices workloads now run on Kubernetes platforms, showcasing the essential role of service mesh layers in managing east‑west traffic and resilience. Service mesh solutions are integrating AI and ML capabilities to enable predictive analytics, automated policy orchestration, and anomaly detection, significantly reducing manual configuration overhead and enhancing operational efficiency.

Zero‑trust security models are becoming standard within mesh platforms, embedding technologies such as mutual TLS encryption, SPIFFE identity frameworks, and dynamic access policies for stronger microservices protection. These features are increasingly expected in regulated industries like finance and healthcare, where secure service‑to‑service communication is imperative. eBPF (Extended Berkeley Packet Filter) based networking is another notable innovation, allowing high‑performance and kernel‑level network security without traditional proxy overhead, thus improving data plane performance and security awareness.

Emerging trends also include sidecar‑less or ambient mesh architectures, which reduce resource consumption and simplify deployment lifecycles by splitting control and data plane responsibilities. These novel architectures can lower CPU utilization by significant margins compared to classical sidecar models, making them attractive for edge computing and resource‑constrained environments. Additionally, federated and multi‑cluster mesh solutions are gaining traction, driven by enterprises operating across hybrid cloud environments needing unified policy enforcement and observability. Collectively, these technologies shape a future where adaptive, secure, and intelligent mesh platforms form a foundational layer of distributed application infrastructures.

• In November 2025, Solo.io announced major Gloo Mesh support for Amazon ECS workloads, enabling enterprise‑grade service mesh capabilities on ECS with unified security, policy enforcement, and telemetry across containers and tasks — helping teams transition from legacy tools to modern service mesh architectures. Source: www.solo.io

• In October 2025, Google Cloud updated Cloud Service Mesh, rolling out version 1.21.6‑asm.4 across managed channels with multiple security CVE fixes and enhanced stability for Envoy proxies and control plane components to improve runtime robustness. Source: www.cloud.google.com

• In June 2025, Google Cloud Service Mesh added cluster‑local traffic enforcement and a DNS Proxy feature, offering sidecar users improved traffic control and preview isolation support to avoid cross‑region overflow for managed traffic director implementations. Source: www.cloud.google.com

• In May–June 2025, Solo.io released Gloo Mesh 2.8, enhancing multi‑cluster operations with automated peering, waypoint insights, and an updated unified UI — boosting observability and operational simplicity in complex mesh environments. Source: www.solo.io

The Service Mesh Tools Software Market Report encompasses a comprehensive examination of the technologies, segments, and geographic dynamics driving modern service mesh adoption. It covers a wide range of deployment types, including Kubernetes‑native meshes, sidecar‑based architectures, ambient/sidecar‑less models, and hybrid cloud configurations, reflecting their varied use cases in cloud‑centric ecosystems. Application segments explored include microservices orchestration, API security, network telemetry, observability, and policy governance, providing decision‑makers with insights into operational priorities shaping enterprise demand.

Geographically, the report analyzes market behavior across North America, Europe, Asia‑Pacific, South America, and Middle East & Africa, highlighting distinct regional trends such as regulatory compliance demands in Europe, hybrid infrastructure expansion in Asia‑Pacific, and enterprise efficiency drives in the Middle East & Africa. It also delves into industry verticals such as IT & telecom, BFSI, e‑commerce, healthcare, and government sectors, outlining how service mesh tools address unique challenges like low‑latency traffic control, secure communication, and scalable microservices management.

Furthermore, the report evaluates technological innovations — from AI/ML‑powered observability and automated policy orchestration to advanced security frameworks and eBPF‑enabled networking — that differentiate vendor strategies and influence competitive positioning. By assessing competitive landscapes, strategic initiatives, and recent market developments, the report equips industry professionals with actionable insights to make informed decisions on technology investments, product selection, and strategic partnerships within the evolving infrastructure software domain.

| Report Attribute / Metric | Details |

|---|---|

| Market Revenue (2025) | USD 698.3 Million |

| Market Revenue (2033) | USD 6,678.1 Million |

| CAGR (2026–2033) | 32.61% |

| Base Year | 2025 |

| Forecast Period | 2026–2033 |

| Historic Period | 2021–2025 |

| Segments Covered |

By Type

By Application

By End-User Insights

|

| Key Report Deliverables | Revenue Forecast; Market Trends; Growth Drivers & Restraints; Technology Insights; Segmentation Analysis; Regional Insights; Competitive Landscape; Regulatory & ESG Overview; Recent Developments |

| Regions Covered | North America; Europe; Asia-Pacific; South America; Middle East & Africa |

| Key Players Analyzed | HashiCorp; Google; AWS; Buoyant (Linkerd); Solo.io; Kong Inc.; Tetrate; F5 (NGINX Service Mesh); Red Hat (OpenShift Service Mesh); Traefik Labs; Aspen Mesh; Grey Matter; Microsoft (Azure Service Mesh) |

| Customization & Pricing | Available on Request (10% Customization Free) |