Reports

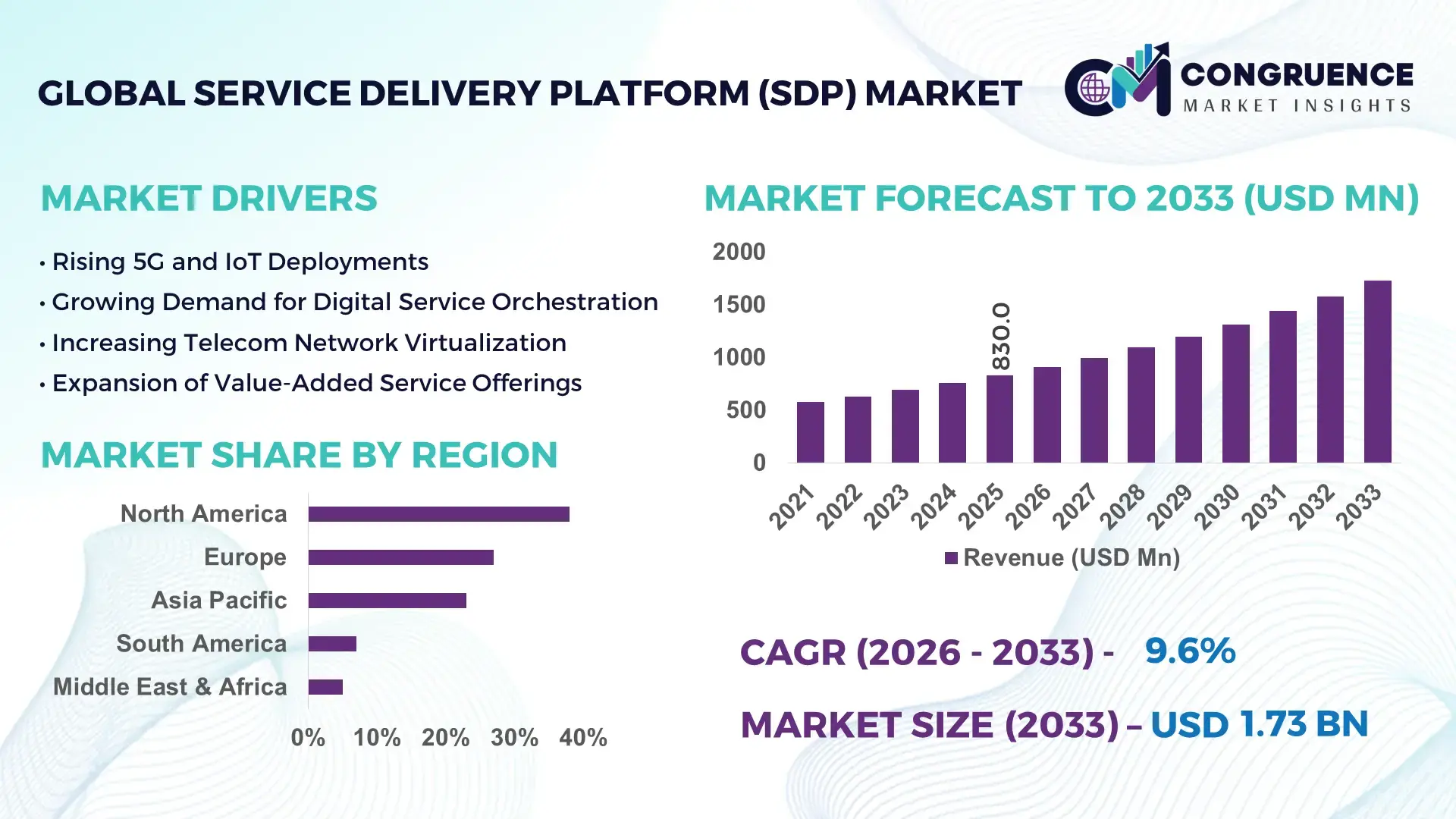

The Global Service Delivery Platform (SDP) Market was valued at USD 830.0 Million in 2025 and is anticipated to reach a value of USD 1,728.1 Million by 2033 expanding at a CAGR of 9.6% between 2026 and 2033, according to an analysis by Congruence Market Insights. The growth is primarily driven by the accelerating integration of cloud-native telecom architectures, 5G core deployments, and digital service monetization strategies among communication service providers.

The United States leads the global Service Delivery Platform (SDP) Market in terms of deployment scale and technological advancement. Over 65% of Tier-1 telecom operators in the U.S. have transitioned to cloud-based or hybrid SDPs to support 5G standalone networks and IoT services. Annual telecom infrastructure investments in the country exceeded USD 100 billion, with a substantial portion allocated to network virtualization and service orchestration platforms. More than 70% of large enterprises in sectors such as BFSI, healthcare, and media leverage API-driven SDPs for digital content delivery, identity management, and real-time billing integration. Additionally, hyperscale cloud providers have established over 35 edge data center clusters across major metropolitan regions, accelerating low-latency SDP deployment for enterprise and consumer applications.

Market Size & Growth: Valued at USD 830.0 Million in 2025, projected to reach USD 1,728.1 Million by 2033, expanding at 9.6% CAGR, driven by rapid 5G monetization and API-based service orchestration.

Top Growth Drivers: 68% telecom cloud adoption rate, 55% increase in digital service bundling, 47% improvement in operational efficiency through virtualization.

Short-Term Forecast: By 2028, automated service provisioning is expected to reduce operational costs by 30% and improve deployment speed by 40%.

Emerging Technologies: AI-driven orchestration, network slicing integration, and edge-native microservices architecture.

Regional Leaders: North America projected at USD 620 Million by 2033 with high 5G penetration; Europe at USD 480 Million driven by regulatory-backed open networks; Asia-Pacific at USD 410 Million supported by large-scale telecom digitization.

Consumer/End-User Trends: Over 60% of enterprises demand unified billing and API exposure capabilities for multi-service delivery environments.

Pilot Example: In 2024, a telecom operator implemented AI-enabled SDP automation, reducing service downtime by 28% and improving SLA compliance by 35%.

Competitive Landscape: Ericsson holds approximately 22% share, followed by Nokia, Huawei, Amdocs, and Oracle.

Regulatory & ESG Impact: Open RAN policies and carbon reduction mandates targeting 45% network energy efficiency improvements by 2030 influence platform modernization.

Investment & Funding Patterns: Over USD 3.5 Billion invested globally in telecom cloud transformation initiatives during recent funding cycles.

Innovation & Future Outlook: API monetization hubs, containerized core integration, and AI-powered analytics are reshaping next-generation SDP frameworks.

Telecom operators account for nearly 58% of SDP deployments, followed by BFSI at 17% and media & entertainment at 12%. Cloud-native SDPs integrating AI orchestration and real-time analytics are gaining traction due to regulatory compliance mandates and digital transformation initiatives. Asia-Pacific exhibits strong consumption growth driven by expanding 5G subscriber bases exceeding 1.2 billion connections, while Europe emphasizes open interoperability standards.

The Service Delivery Platform (SDP) Market holds strategic relevance as telecom and enterprise ecosystems transition toward programmable, software-defined network environments. AI-driven orchestration delivers 35% faster provisioning efficiency compared to legacy hardware-centric BSS/OSS systems. North America dominates in deployment volume, while Asia-Pacific leads in adoption intensity, with over 72% of telecom enterprises implementing cloud-native service layers.

By 2028, AI-powered predictive service assurance is expected to reduce network fault resolution time by 40%. ESG-driven modernization initiatives are pushing telecom operators to commit to 50% energy efficiency improvements in network operations by 2030 through virtualization and containerized SDPs. In 2024, a U.S.-based telecom provider achieved a 32% improvement in network service activation time through Kubernetes-based SDP transformation.

Strategically, SDPs are evolving into digital monetization hubs enabling IoT, 5G slicing, and edge computing use cases. As enterprises demand real-time API exposure and seamless billing integration, the Service Delivery Platform (SDP) Market is positioned as a core pillar for operational resilience, compliance alignment, and sustainable digital infrastructure growth.

The Service Delivery Platform (SDP) Market is shaped by rapid telecom digitalization, cloud-native transformation, and the proliferation of connected devices exceeding 15 billion globally. The shift toward 5G standalone architectures has intensified demand for programmable service orchestration layers capable of managing multi-vendor environments. Enterprises increasingly require real-time charging, policy control, and API monetization capabilities to support digital ecosystems. Additionally, edge computing nodes—projected to exceed 10,000 globally within major telecom infrastructures—are influencing SDP architectural redesign toward distributed microservices. Regulatory frameworks promoting open network standards further impact vendor strategies, fostering interoperability and virtualization adoption across telecom and enterprise verticals.

Global 5G subscriptions surpassed 1.6 billion in 2025, compelling telecom operators to modernize service orchestration layers. Over 70% of new telecom infrastructure projects now incorporate cloud-native cores requiring advanced SDP integration. 5G network slicing enables up to 50% improved bandwidth utilization, necessitating dynamic service provisioning. Enterprises leveraging 5G-enabled IoT solutions report 30% higher operational responsiveness, increasing reliance on API-driven SDPs for service lifecycle management.

More than 45% of telecom operators operate legacy OSS/BSS systems exceeding 10 years in age, creating interoperability challenges during SDP migration. Integration costs may increase project budgets by 25% due to system customization and vendor lock-in issues. Additionally, cybersecurity risks have risen, with telecom networks experiencing a 38% increase in attempted breaches, requiring enhanced compliance investments that slow deployment cycles.

Global edge deployments are expanding rapidly, with over 35% of enterprises adopting edge-enabled workloads. SDPs integrated with edge nodes can reduce latency by up to 60%, enabling real-time analytics and mission-critical services. Industry verticals such as manufacturing and healthcare report 28% performance improvements through localized service orchestration, presenting strong expansion opportunities.

Telecom operational expenditures increased by nearly 12% year-over-year due to spectrum investments and infrastructure upgrades. Skilled cloud-native workforce shortages impact over 40% of operators, delaying SDP modernization. Additionally, regulatory compliance costs tied to data localization and privacy mandates have grown by approximately 20%, creating financial pressure on mid-tier operators.

AI-Driven Service Orchestration Adoption Increasing by 45%: Telecom providers integrating AI-based automation report 35% faster provisioning and 28% lower downtime. Predictive analytics embedded within SDPs reduces fault detection time by 40%, enhancing SLA compliance.

Cloud-Native Containerization Surpassing 60% Deployments: Over 60% of new SDPs are deployed using Kubernetes-based microservices, improving scalability by 50% compared to monolithic systems and reducing deployment cycles by 33%.

API Monetization Growth at 52% Enterprise Adoption: Enterprises leveraging open APIs through SDPs have increased digital partnership revenue streams by 30%, while improving cross-platform integration efficiency by 42%.

Edge-Integrated SDP Nodes Expanding 38% Annually: Distributed edge deployments linked with SDPs reduce latency by 60% and enhance IoT device management capacity by 45%, particularly across smart city and industrial automation projects.

The Service Delivery Platform (SDP) Market is segmented by type, application, and end-user, reflecting the diverse deployment needs across telecom and enterprise environments. By type, cloud-based SDPs dominate due to scalability and microservices compatibility, while on-premise solutions remain relevant for regulated industries requiring localized data control. Applications range from telecom service orchestration and billing management to IoT enablement and content delivery optimization. End-user adoption is highest among telecom operators, followed by BFSI and media sectors leveraging API monetization and real-time policy management. Increasing enterprise digital transformation initiatives continue to diversify deployment models and sectoral penetration.

Cloud-based SDPs account for approximately 62% of total deployments, driven by scalability, container orchestration, and integration with 5G cores. On-premise SDPs hold nearly 28% share, primarily adopted by government and defense entities requiring strict data sovereignty controls. Hybrid SDPs contribute the remaining 10%, offering flexibility between cloud scalability and local compliance requirements. Cloud-native platforms are the fastest-growing segment, expanding at an estimated 12.4% CAGR due to rising adoption of Kubernetes and microservices architectures. These platforms enable 45% faster service rollout compared to traditional on-premise systems. Hybrid models are gaining attention among multinational enterprises balancing latency and compliance. Combined, niche legacy systems and private cloud variants account for under 15% but remain relevant in specific regulatory markets.

Telecom service orchestration leads with approximately 48% share, as operators integrate SDPs for billing, policy control, and digital content management. IoT enablement represents 22%, driven by connected devices surpassing 15 billion globally. Content delivery and value-added services account for 18%, while enterprise mobility and identity management contribute a combined 12%. IoT enablement is the fastest-growing application segment, expanding at nearly 13.1% CAGR, fueled by smart city projects and industrial IoT deployments increasing by 30% annually. Enterprises report 35% operational efficiency gains through SDP-integrated IoT frameworks. In 2025, more than 42% of global enterprises piloted SDP-integrated digital service models for customer experience platforms, reflecting rising cross-sector demand.

Telecom operators dominate with nearly 58% market share due to large-scale 5G and fiber deployments. BFSI follows at 17%, leveraging SDPs for secure transaction orchestration and digital wallet services. Media & entertainment accounts for 12%, integrating SDPs for streaming optimization and content monetization. The remaining 13% includes healthcare, government, and retail sectors. BFSI represents the fastest-growing end-user segment with an estimated 11.8% CAGR, driven by digital banking adoption exceeding 65% globally. Retail enterprises adopting API-enabled SDPs report 29% faster checkout processing and 22% higher customer retention rates.In 2025, over 38% of enterprises globally reported integrating SDP capabilities within multi-cloud environments to enhance service delivery agility.

North America accounted for the largest market share at 38% in 2025 however, Asia-Pacific is expected to register the fastest growth, expanding at a CAGR of 11.2% between 2026 and 2033.

North America’s leadership is supported by over 75% 5G standalone deployment across Tier-1 telecom operators and more than 65% enterprise cloud-native SDP integration across BFSI and healthcare sectors. Europe follows with approximately 27% share, driven by open network frameworks and strong data governance regulations impacting over 40 countries. Asia-Pacific accounts for nearly 23% of global demand, supported by more than 1.2 billion 5G subscribers and over 500 active telecom modernization projects. South America represents around 7% share, with digital infrastructure investments increasing by 18% year-over-year, while Middle East & Africa contribute close to 5%, fueled by smart city investments exceeding 30 large-scale initiatives across GCC nations. Edge node deployments surpassed 10,000 units globally, with 45% concentrated across North America and Asia-Pacific combined, significantly influencing regional SDP rollout strategies.

North America holds approximately 38% share of the global Service Delivery Platform (SDP) Market, driven by extensive 5G standalone rollouts and cloud-native telecom core transitions. The United States accounts for nearly 82% of regional deployments, followed by Canada at 12%. Key industries include telecom, BFSI, healthcare, and media streaming, where over 68% of enterprises utilize API-driven SDPs for billing and digital identity management. Regulatory initiatives such as Open RAN mandates and data protection frameworks influence more than 70% of telecom infrastructure upgrades. Companies like Ericsson are expanding AI-driven orchestration hubs across multiple U.S. states to enhance real-time network slicing capabilities. Regional consumer behavior indicates higher enterprise adoption in healthcare and finance, with over 60% of hospitals integrating virtualized service layers for patient data interoperability.

Europe commands nearly 27% of the global Service Delivery Platform (SDP) Market share, with Germany, the UK, and France collectively contributing over 58% of regional demand. The European Electronic Communications Code influences telecom modernization across 27 EU member states. More than 55% of telecom operators in Western Europe have adopted containerized SDPs aligned with sustainability objectives targeting 45% carbon emission reductions by 2030. Nokia has implemented AI-based orchestration systems across Nordic telecom networks, enhancing service provisioning speed by 30%. Enterprises in Europe prioritize compliance, leading to 50% higher demand for explainable AI-enabled SDP analytics compared to other regions.

Asia-Pacific ranks second in volume with around 23% global share and leads in deployment scale expansion. China, India, and Japan collectively account for more than 70% of regional consumption. The region hosts over 1.2 billion 5G subscribers and more than 600 smart city initiatives integrating IoT-managed SDPs. Infrastructure growth includes 40% annual expansion in edge data centers across metropolitan hubs. Huawei has deployed distributed cloud SDPs across multiple provinces to support IoT and AI-driven automation frameworks. Regional consumer trends show strong demand driven by e-commerce and mobile-first applications, with over 75% of digital transactions processed through telecom-integrated service platforms.

South America accounts for nearly 7% of the global Service Delivery Platform (SDP) Market, with Brazil representing about 48% of regional deployments and Argentina contributing 18%. Telecom network expansion and fiber connectivity projects increased by 22% between 2024 and 2025. Government-backed digital transformation programs support infrastructure digitization across energy and public sectors. América Móvil has upgraded multiple Latin American telecom cores with cloud-based SDPs to improve cross-border billing efficiency by 25%. Consumer behavior trends reveal strong demand tied to localized media streaming and multilingual content services, with digital content consumption rising by 35% annually.

The Middle East & Africa region contributes around 5% of global SDP demand, led by the UAE and Saudi Arabia, which together represent over 60% of regional investments. Oil & gas, smart construction, and telecom sectors drive demand, with more than 30 smart city projects integrating IoT-enabled SDPs. South Africa accounts for approximately 15% of regional deployments, focusing on enterprise mobility platforms. Etisalat has deployed AI-powered service orchestration across its GCC network to improve provisioning efficiency by 28%. Regional consumer trends highlight increasing adoption of mobile financial services, with over 55% of digital transactions processed via telecom-integrated platforms.

United States – 32% Market Share: Strong telecom cloud adoption exceeding 70% among Tier-1 operators drives Service Delivery Platform (SDP) Market dominance.

China – 19% Market Share: Large-scale 5G subscriber base surpassing 900 million accelerates Service Delivery Platform (SDP) Market deployment across telecom and IoT ecosystems.

The Service Delivery Platform (SDP) Market is moderately consolidated, with the top five companies collectively accounting for approximately 58% of total market share. Over 35 active global competitors operate across telecom software, cloud-native platforms, and network orchestration segments. Leading vendors compete through AI-driven automation, API monetization capabilities, and Kubernetes-based microservices deployment.

Strategic initiatives include over 20 major telecom-cloud partnerships formed between 2024 and 2025 to accelerate 5G monetization. Product innovation cycles have shortened by nearly 30%, with vendors launching containerized SDP upgrades annually. Mergers and acquisitions activity increased by 18% year-over-year, focusing on edge computing and AI analytics startups. Competitive differentiation centers on interoperability, cybersecurity compliance certifications, and energy-efficient virtualization frameworks reducing operational energy consumption by up to 35%. The market environment reflects high technological intensity and rapid feature innovation aligned with enterprise digitization demands.

Amdocs

Oracle Corporation

Netcracker Technology

ZTE Corporation

Comviva

CSG Systems International

Hewlett Packard Enterprise

Cisco Systems

Mavenir

Matrixx Software

Openet

The Service Delivery Platform (SDP) Market is undergoing significant transformation driven by cloud-native architectures, AI-based orchestration, and distributed edge computing. Over 60% of newly deployed SDPs are containerized using Kubernetes frameworks, enabling 45% faster service activation compared to legacy monolithic platforms. AI-powered predictive maintenance modules reduce network fault detection times by 40% and improve SLA compliance by nearly 35%.

Network slicing integration supports dynamic bandwidth allocation, improving utilization efficiency by 50% across 5G standalone networks. API gateway frameworks embedded within SDPs process over 1 million transactions per second in large-scale telecom environments. Edge-integrated SDPs reduce latency by up to 60%, supporting mission-critical IoT and industrial automation use cases.

Cybersecurity enhancements include zero-trust architectures and encrypted API exposure, reducing breach incidents by 28% in virtualized telecom environments. Sustainability-focused virtualization technologies lower network energy consumption by approximately 30%, aligning with carbon neutrality goals. Future advancements include AI-driven autonomous networks capable of self-optimization, potentially improving operational productivity by 35% within the next three years.

• In March 2026, Ericsson and Nokia announced a strategic collaboration to accelerate autonomous network deployment through shared ecosystems, with Ericsson joining Nokia’s SMO Marketplace and Nokia participating in Ericsson’s rApp Ecosystem. This cooperation aims to expand availability, interoperability, and integration of network automation and intelligent orchestration tools for communication service providers globally. Source: www.ericsson.com

• In June 2025, Ericsson unveiled an evolved OSS/BSS portfolio designed for AI and intent-based automation, including enhancements to its Service Orchestration and Assurance tools. The updates embed AI throughout core support systems, enabling real-time service configuration and lifecycle management capabilities within autonomous network environments. Source: www.ericsson.com

• At Mobile World Congress 2025, Cisco launched Agile Services Networking innovations, empowering service providers with intelligent networking capabilities that offer real-time visibility across connectivity layers and deliver assured AI-enabled subscriber experiences. These advancements support resilient, differentiated service delivery frameworks at scale. Source: www.cisco.com

• In March 2025, Jio Platforms announced plans with AMD, Cisco, and Nokia to build an Open Telecom AI Platform, aimed at integrating domain-specific AI (including LLMs and machine learning) to optimize network security, operational efficiency, and automated orchestration across service provider ecosystems—setting a new reference architecture for future telecom automation frameworks. Source: www.cisco.com

The Service Delivery Platform (SDP) Market Report provides a comprehensive evaluation across multiple dimensions, including deployment type, application domains, end-user industries, and regional performance. The study covers cloud-based, on-premise, and hybrid SDP architectures, assessing their integration across telecom, BFSI, healthcare, media, retail, and government sectors. Over 15 billion connected devices influencing IoT-driven SDP integration are considered within the analytical framework.

Geographically, the report spans North America, Europe, Asia-Pacific, South America, and Middle East & Africa, evaluating more than 25 key countries contributing to global demand. It analyzes technological trends such as AI-driven orchestration, network slicing, API monetization, and edge-native microservices impacting service activation efficiency by up to 45%. The scope also includes competitive benchmarking of over 30 major vendors, assessment of regulatory frameworks influencing telecom virtualization, and sustainability metrics targeting up to 50% energy efficiency improvements. Emerging niche segments such as private 5G enterprise SDPs and industry-specific digital service hubs are incorporated to provide decision-makers with forward-looking strategic insights.

| Report Attribute / Metric | Details |

|---|---|

| Market Revenue (2025) | USD 830.0 Million |

| Market Revenue (2033) | USD 1,728.1 Million |

| CAGR (2026–2033) | 9.6% |

| Base Year | 2025 |

| Forecast Period | 2026–2033 |

| Historic Period | 2021–2025 |

| Segments Covered |

By Type

By Application

By End-User Insights

|

| Key Report Deliverables | Revenue Forecast; Market Trends; Growth Drivers & Restraints; Technology Insights; Segmentation Analysis; Regional Insights; Competitive Landscape; Regulatory & ESG Overview; Recent Developments |

| Regions Covered | North America; Europe; Asia-Pacific; South America; Middle East & Africa |

| Key Players Analyzed | Ericsson; Nokia; Huawei Technologies; Amdocs; Oracle Corporation; Netcracker Technology; ZTE Corporation; Comviva; CSG Systems International; Hewlett Packard Enterprise; Cisco Systems; Mavenir; Matrixx Software; Openet |

| Customization & Pricing | Available on Request (10% Customization Free) |