Reports

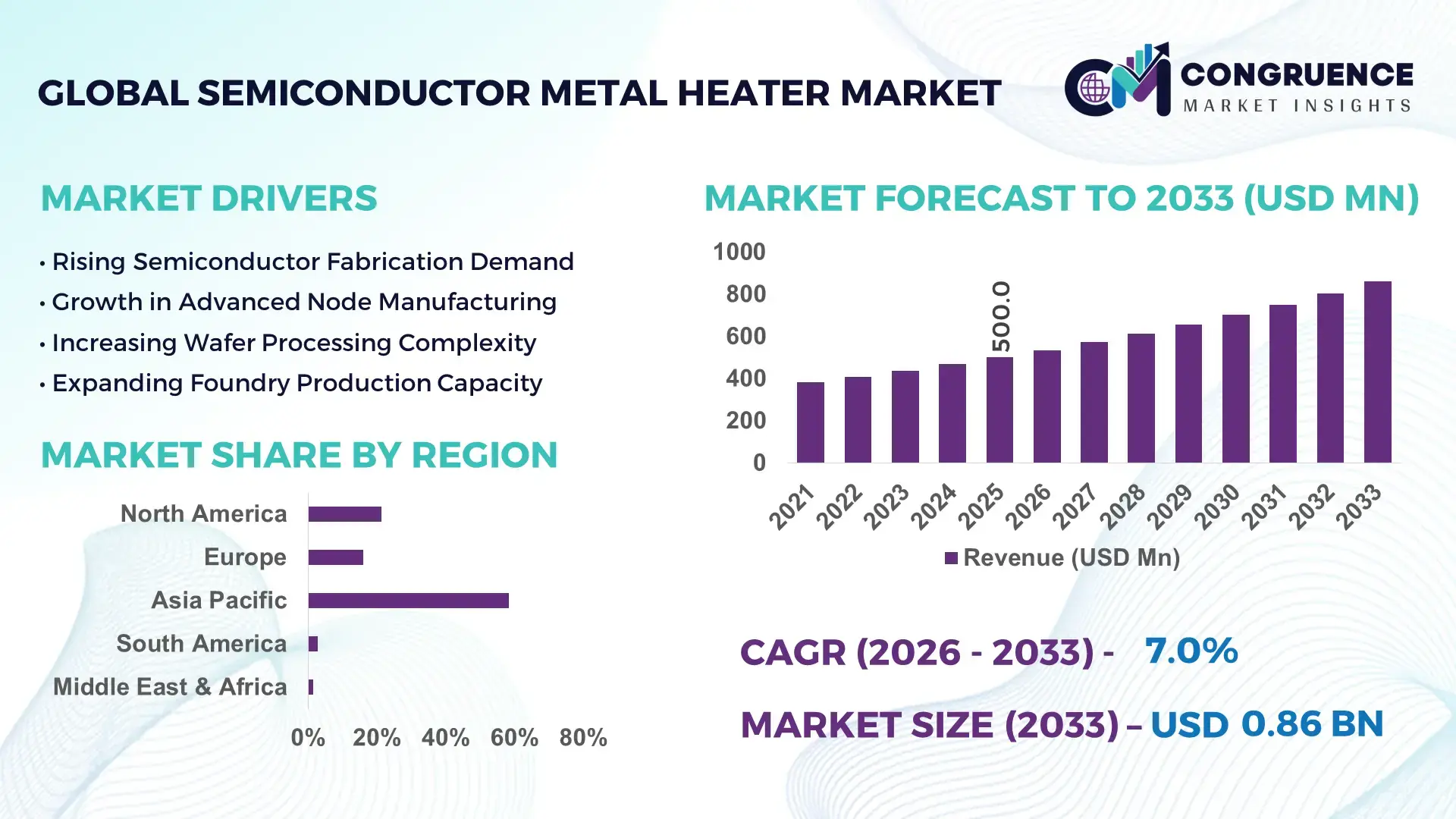

The Global Semiconductor Metal Heater Market was valued at USD 500.0 Million in 2025 and is anticipated to reach a value of USD 859.1 Million by 2033 expanding at a CAGR of 7.0% between 2026 and 2033. Growth is being accelerated by rising deployment of advanced wafer processing equipment, increasing transition to sub-5nm semiconductor fabrication, and growing investment in precision thermal management systems for etching, deposition, and lithography applications.

China remains the dominant country in the Semiconductor Metal Heater Market, accounting for nearly 34% of global semiconductor manufacturing capacity, supported by more than USD 40 billion in ongoing semiconductor infrastructure investments and strong adoption across wafer fabrication facilities. In comparison, South Korea contributes approximately 18% of global chip production capacity but demonstrates higher penetration of advanced process nodes below 7nm. Continued expansion of domestic fabs, supply-chain localization initiatives, and equipment modernization programs are reinforcing demand for high-precision metal heating technologies across critical semiconductor production environments.

Strategically, manufacturers prioritizing localized production, advanced thermal uniformity capabilities, and next-generation fab partnerships are strengthening long-term competitive positioning.

Market Size & Growth: USD 500.0 Million in 2025, projected to reach USD 859.1 Million by 2033 at 7.0% CAGR, supported by rapid expansion of advanced semiconductor fabrication facilities and precision thermal processing demand.

Top Growth Drivers: Sub-5nm chip production up 22%, wafer fabrication equipment spending up 18%, and semiconductor localization investments exceeding 25% growth across major manufacturing hubs.

Short-Term Forecast: By 2028, thermal process efficiency is expected to improve by 15% while maintenance-related downtime declines by nearly 12% in advanced fabs.

Emerging Technologies: AI-enabled process control, smart heating architectures, advanced alloy materials, and predictive thermal monitoring are reshaping equipment performance standards.

Regional Leaders: Asia Pacific exceeds USD 420 Million, North America approaches USD 190 Million, and Europe surpasses USD 120 Million, driven by fab expansion and supply-chain diversification.

Consumer/End-User Trends: More than 68% of advanced semiconductor facilities are increasing investments in precision thermal control solutions to support yield optimization.

Pilot/Case Example: In 2025, a leading wafer fabrication project achieved 14% higher process uniformity and reduced thermal variation by 11% through upgraded metal heater integration.

Competitive Landscape: Leading suppliers collectively control nearly 45% market share, with key participants including Watlow, Thermcraft, Backer Hotwatt, Tempco, and Durex Industries.

Regulatory & ESG Impact: Energy-efficient thermal systems reduce process energy consumption by approximately 10%, supporting industrial decarbonization and sustainability targets.

Investment & Funding: More than USD 70 billion in global semiconductor facility investments continues to stimulate equipment partnerships, localization, and capacity expansion initiatives.

Innovation & Future Outlook: Next-generation ultra-uniform heating systems, digital twins, and intelligent process automation are becoming central to advanced semiconductor manufacturing strategies.

The Semiconductor Metal Heater Market is increasingly shaped by demand from wafer fabrication, advanced packaging, semiconductor testing, and specialty chip manufacturing facilities. Recent innovations focus on multi-zone temperature control, enhanced thermal uniformity, and smart monitoring systems that improve process stability. Nearly 20% lower thermal deviation rates are being achieved through advanced heater designs. Ongoing semiconductor supply-chain realignment and domestic manufacturing initiatives are accelerating equipment upgrades, creating a favorable environment for strategic technology investments and operational modernization.

Semiconductor metal heaters have become strategically important as chip manufacturers pursue tighter process tolerances, higher wafer yields, and advanced node production. The market sits at the center of semiconductor manufacturing modernization, where thermal precision directly influences etching accuracy, deposition quality, and overall production efficiency. Supply-chain restructuring across China, the United States, South Korea, and India is increasing demand for localized equipment ecosystems and reliable thermal processing technologies.

Modern multi-zone semiconductor metal heaters deliver up to 18% better temperature uniformity and reduce thermal fluctuation by nearly 15% compared with conventional single-zone systems. North America continues to lead in advanced process innovation and R&D-intensive fabrication, while China deploys larger volumes of manufacturing capacity expansion projects. This contrast creates distinct opportunities for both premium-performance and high-volume equipment suppliers. Over the next two to three years, adoption of intelligent thermal monitoring systems is expected to exceed 60% of newly commissioned advanced fabrication lines.

For example, several wafer fabrication facilities are integrating predictive maintenance platforms with precision heating systems to reduce unplanned downtime and improve equipment utilization. Manufacturers are expanding strategic partnerships with semiconductor equipment providers, increasing localized production capabilities, and accelerating product development. Companies that combine thermal precision, operational reliability, and scalable manufacturing support will secure stronger competitive advantages as semiconductor production complexity continues to rise.

Rapid growth in advanced semiconductor fabrication is increasing demand for highly accurate thermal processing systems. More than 70% of leading-edge wafer production now requires precise temperature control across multiple process stages, while advanced packaging investments have increased by approximately 20% over recent years. The expansion of domestic semiconductor manufacturing initiatives in China, the United States, and India is creating sustained demand for equipment capable of maintaining tight thermal tolerances. This industrial shift directly improves process consistency, yield performance, and production throughput. In response, manufacturers are investing in multi-zone heating technologies, smart control systems, and enhanced thermal uniformity solutions. A notable strategic insight is that thermal precision is increasingly becoming a differentiating factor in semiconductor competitiveness rather than merely an equipment specification.

Metal heater manufacturers face ongoing challenges from fluctuations in specialty alloy prices and concentrated supply chains. Certain high-performance heating materials have experienced cost swings exceeding 15%, while semiconductor equipment lead times remain approximately 20% longer than pre-disruption levels in some supply channels. Dependence on specialized manufacturing inputs creates operational constraints for production planning and margin stability. Countries with limited domestic component ecosystems remain particularly exposed to procurement risks. To mitigate these pressures, companies are diversifying supplier networks, increasing regional sourcing strategies, and negotiating long-term material contracts. A key operational insight is that supply-chain resilience is becoming as important as product performance when semiconductor manufacturers evaluate equipment vendors.

The emergence of AI-enabled semiconductor manufacturing creates significant opportunities for advanced semiconductor metal heaters. Smart thermal management systems can improve process consistency by approximately 12% while reducing energy consumption by nearly 10% through real-time optimization. More than 55% of newly planned advanced fabrication facilities are expected to incorporate greater levels of equipment connectivity and predictive analytics. Japan and South Korea are actively advancing smart manufacturing initiatives that require intelligent thermal control solutions. Manufacturers are expanding R&D investments, developing integrated monitoring platforms, and forming technology partnerships to address these requirements. A non-obvious opportunity lies in combining thermal hardware with software-driven performance optimization, creating higher-value recurring service models alongside equipment sales.

As semiconductor geometries continue shrinking, maintaining consistent thermal performance across larger wafer volumes and increasingly complex production environments becomes more difficult. Temperature deviations of even 1–2% can significantly impact process outcomes in advanced manufacturing applications. Additionally, demand for highly skilled engineering personnel has risen by more than 15% across semiconductor equipment segments, creating workforce constraints. The transition toward heterogeneous integration, advanced packaging, and high-density chip architectures further increases thermal management complexity. Companies must invest in simulation technologies, digital process validation, and advanced engineering capabilities to maintain performance standards. A critical strategic challenge is balancing scalability, precision, and operational efficiency while supporting increasingly sophisticated semiconductor production requirements.

Smart Thermal Control Adoption Advanced semiconductor fabs are deploying intelligent thermal control platforms to improve process stability and yield consistency. More than 60% of newly installed wafer processing lines now incorporate digital temperature monitoring, while thermal deviation rates have declined by nearly 15% in advanced manufacturing environments. The shift toward AI-assisted process optimization is reducing manual calibration requirements and improving equipment utilization. In response, manufacturers are integrating predictive analytics and automated control software into next-generation heater systems.

Localized Equipment Supply Expansion Semiconductor supply-chain restructuring is driving increased localization of critical process equipment. China and India have expanded domestic semiconductor manufacturing initiatives, while procurement lead times for selected thermal processing components have improved by approximately 12% through regional sourcing strategies. More than 30% of equipment suppliers are increasing local assembly or component partnerships to improve responsiveness and reduce dependency on imported subsystems. This operational transition is strengthening supply resilience and shortening project deployment cycles.

Advanced Materials Integration Shift High-performance alloys and engineered metal composites are gaining traction as fabs target tighter process tolerances. New heater architectures have improved temperature uniformity by nearly 18% while extending operational life by approximately 10% under demanding process conditions. Semiconductor equipment providers are redesigning heating modules to support advanced packaging and next-generation chip fabrication requirements. The non-obvious impact is reduced maintenance frequency, allowing manufacturers to improve throughput without major infrastructure expansion.

Energy-Efficient Process Optimization Growing focus on operational efficiency is accelerating adoption of energy-optimized semiconductor metal heaters. Modern systems are lowering thermal energy consumption by approximately 10%–12%, while process cycle times have improved by nearly 8% in selected fabrication environments. Regulatory pressure around industrial energy performance and rising utility costs are reinforcing this trend. Companies are responding through automation upgrades, thermal redesign programs, and strategic partnerships focused on sustainable semiconductor manufacturing operations.

Tubular metal heaters remain the leading type segment, accounting for an estimated 42% of market demand, supported by their durability, thermal uniformity, and broad compatibility with semiconductor processing equipment. Their ability to operate reliably in high-temperature environments makes them a preferred solution for deposition, etching, and wafer-processing applications. Semiconductor manufacturers continue prioritizing proven thermal technologies that minimize process variability and support large-scale production requirements. Cartridge heaters maintain strong adoption in precision-focused applications where compact installation and localized heating are critical. Cartridge heaters represent the fastest-growing segment, with adoption increasing by approximately 9% annually across advanced semiconductor equipment installations. Their growing use in compact process chambers and high-density manufacturing systems reflects broader industry movement toward equipment miniaturization and precision control. Strip heaters and specialty configurations continue serving niche applications requiring customized thermal profiles. Manufacturers are expanding product portfolios, investing in advanced materials, and strengthening OEM partnerships to capture demand from increasingly sophisticated semiconductor production environments. This shift is directing investment toward precision-engineered heating solutions capable of supporting next-generation fabrication requirements.

Wafer processing remains the dominant application segment, contributing nearly 45% of semiconductor metal heater deployment, as thermal stability directly influences production yield and process precision. Semiconductor manufacturers continue upgrading fabrication lines to support advanced nodes, increasing demand for highly controlled heating environments. Deposition applications also account for a substantial share because thin-film quality depends heavily on temperature consistency throughout manufacturing cycles. Growing wafer complexity and tighter production tolerances continue reinforcing the importance of advanced thermal management systems. Etching applications represent the fastest-growing segment, supported by increasing production of advanced logic and memory devices. Adoption of precision thermal control systems within etching environments has increased by approximately 14% over recent years as manufacturers target improved process accuracy and reduced defect rates. Lithography and inspection-related applications are also integrating more sophisticated thermal architectures to support tighter process specifications. Equipment suppliers are responding through automation integration, process optimization partnerships, and expanded engineering support programs. Demand is increasingly shifting toward applications where temperature precision directly influences throughput, yield optimization, and operational consistency.

Semiconductor foundries remain the largest end-user segment, accounting for approximately 50% of total demand, supported by large-scale wafer production and continuous investment in fabrication capacity. These facilities rely heavily on precision thermal processing equipment to maintain yield performance and production efficiency. Integrated Device Manufacturers (IDMs) also represent a significant share due to vertically integrated manufacturing operations and ongoing investments in advanced semiconductor technologies. Large-volume production environments continue driving demand for highly reliable and scalable heating systems. Outsourced Semiconductor Assembly and Test (OSAT) providers are emerging as the fastest-growing end-user segment, with equipment adoption increasing by nearly 11% as advanced packaging technologies gain importance. Growing complexity in chip architectures is expanding thermal management requirements beyond traditional fabrication processes. Research institutes and technology development centers continue contributing demand through pilot production programs and process innovation initiatives. To strengthen market positioning, suppliers are offering customized solutions, collaborative development agreements, and performance-focused service packages tailored to distinct end-user requirements. Future demand is increasingly shifting toward organizations investing aggressively in advanced packaging and next-generation semiconductor manufacturing ecosystems.

Asia-Pacific accounted for the largest market share at 58.4% in 2025 however, North America is expected to register the fastest growth, expanding at a CAGR of 7.8% between 2026 and 2033.

North America maintains a strong position in the Semiconductor Metal Heater Market through advanced semiconductor fabrication, equipment innovation, and large-scale manufacturing investments. The region accounts for approximately 21.4% of global market demand, supported by growing deployment of advanced wafer fabrication facilities and process-intensive semiconductor manufacturing. Expansion of domestic chip production programs has increased demand for high-precision thermal processing systems across etching, deposition, and packaging applications. More than 15 major semiconductor facility expansion projects have been announced or advanced across the United States over recent years, reinforcing equipment procurement activity. Suppliers are strengthening local engineering capabilities and expanding partnerships with semiconductor equipment manufacturers to support increasingly sophisticated production environments.

United States Market Outlook: The United States serves as the primary growth engine for the regional market due to its concentration of advanced semiconductor fabrication facilities, equipment manufacturers, and technology development programs. The country leads in next-generation process node deployment and continues attracting substantial semiconductor infrastructure investment. More than 75% of North America's advanced wafer production capacity is concentrated in the U.S., creating strong demand for precision heating technologies. Domestic manufacturing initiatives, combined with expanding R&D activity, are encouraging suppliers to localize production and develop higher-performance thermal management solutions.

Europe represents a strategically important market supported by advanced industrial manufacturing, semiconductor research expertise, and increasing emphasis on energy-efficient production systems. The region contributes nearly 16% of global market demand, with Germany, France, and the Netherlands serving as key semiconductor equipment and manufacturing hubs. Semiconductor manufacturers are investing in process modernization and thermal efficiency improvements to support advanced chip production and sustainability objectives. Deployment of energy-optimized thermal processing systems has increased by approximately 12% across selected fabrication environments. Equipment suppliers are focusing on advanced materials, operational efficiency, and collaborative innovation programs to strengthen market positioning.

Germany Market Outlook: Germany remains the most influential country within the European Semiconductor Metal Heater Market due to its strong semiconductor equipment ecosystem and industrial engineering capabilities. The country hosts a significant concentration of semiconductor manufacturing and process technology facilities supporting automotive, industrial, and advanced electronics applications. Approximately 30% of Europe's semiconductor equipment activity is linked to German industrial infrastructure. Continuous investment in smart manufacturing technologies and advanced process optimization is strengthening demand for precision thermal systems across semiconductor production environments.

Asia-Pacific dominates the Semiconductor Metal Heater Market, accounting for approximately 58.4% of global demand, driven by its unmatched semiconductor manufacturing base and extensive fabrication infrastructure. The region hosts the majority of global wafer production facilities, creating sustained demand for advanced thermal processing technologies. China, South Korea, Taiwan, and Japan continue expanding fabrication capacity while increasing investment in advanced packaging and process optimization initiatives. Semiconductor production output in key manufacturing hubs has increased by more than 18% over recent years, supporting continued equipment deployment. Manufacturers are expanding production networks, strengthening supply-chain integration, and accelerating technology upgrades to support advanced semiconductor processes.

China Market Outlook: China represents the largest country-level opportunity due to its extensive semiconductor manufacturing ecosystem and ongoing domestic production expansion. The country accounts for nearly 34% of global semiconductor manufacturing capacity and continues investing heavily in fabrication infrastructure, equipment localization, and supply-chain development. Expansion of domestic semiconductor projects has accelerated procurement of precision thermal systems used in wafer fabrication and advanced packaging facilities. Equipment suppliers increasingly prioritize local partnerships, engineering support, and manufacturing presence to align with evolving domestic production requirements.

South America remains a developing market where semiconductor metal heater demand is primarily linked to electronics manufacturing expansion, industrial modernization, and technology assembly operations. The region contributes approximately 2.8% of global demand, with activity concentrated in selected manufacturing clusters. Growing adoption of automation technologies and localized electronics production is supporting gradual demand for semiconductor process equipment and related thermal systems. Recent industrial investment initiatives have increased advanced manufacturing project activity by approximately 9% across key markets. However, infrastructure limitations and limited semiconductor fabrication capacity continue constraining large-scale deployment. Companies are addressing these challenges through partnerships, technology transfer initiatives, and localized engineering support.

Brazil Market Outlook: Brazil leads regional demand due to its industrial manufacturing scale, electronics production base, and technology modernization efforts. The country serves as the primary hub for semiconductor-related assembly and electronics manufacturing activity in South America. More than 45% of the region’s electronics production capacity is concentrated in Brazil, creating opportunities for advanced thermal processing technologies. Continued investment in industrial automation and higher-value manufacturing capabilities is supporting demand for precision process equipment across emerging semiconductor-related applications.

The Middle East & Africa market is evolving through industrial diversification programs, technology infrastructure development, and strategic investments in advanced manufacturing capabilities. The region accounts for approximately 1.4% of global demand, with activity concentrated in countries pursuing industrial transformation agendas. Governments are increasing investments in technology parks, electronics manufacturing facilities, and advanced industrial ecosystems. Technology-focused infrastructure initiatives have expanded by nearly 10% across selected markets, encouraging adoption of specialized manufacturing equipment. While local semiconductor fabrication remains limited, demand is gradually increasing through industrial modernization projects and technology development initiatives.

Saudi Arabia Market Outlook: Saudi Arabia is emerging as the most strategically significant market in the region due to its industrial diversification strategy and large-scale infrastructure investments. The country continues expanding advanced manufacturing capabilities through technology-focused development programs and industrial ecosystem partnerships. More than USD 20 billion equivalent industrial technology investments have been directed toward manufacturing modernization initiatives across multiple sectors. Growing emphasis on domestic technology capabilities, combined with industrial expansion programs, is creating opportunities for suppliers of precision thermal and semiconductor-related manufacturing solutions.

The Semiconductor Metal Heater Market is characterized by competition between global thermal technology leaders such as Watlow, Durex Industries, Tempco Electric Heater, Backer Hotwatt, and Thermcraft, and specialized regional manufacturers focused on custom-engineered solutions. The top five players collectively account for approximately 45–50% of market activity, creating a moderately consolidated structure. Global leaders compete on thermal precision, reliability, and semiconductor process expertise, while regional suppliers compete through customization, shorter lead times, and pricing advantages. Competition increasingly centers on temperature uniformity, energy efficiency, and semiconductor equipment integration. Advanced thermal platforms can improve process consistency by 15–18%, while energy-optimized systems reduce consumption by nearly 10–12%. Companies are expanding engineering capabilities, forming OEM partnerships, and integrating smart monitoring technologies to strengthen customer retention. The competitive landscape is shifting toward intelligent thermal systems and localized supply chains as semiconductor manufacturers prioritize operational resilience. High qualification requirements, long validation cycles, and stringent performance standards create substantial entry barriers. Success depends on delivering superior thermal precision, application-specific engineering support, supply reliability, and continuous innovation aligned with next-generation semiconductor manufacturing requirements.

Durex Industries

Tempco Electric Heater Corporation

Backer Hotwatt

Thermcraft Inc.

Omega Engineering

Tutco Heating Solutions Group

Chromalox

Industrial Heater Corporation

Delta MFG

Wattco

Nexthermal Corporation

Thermal Corporation

Rama Corporation

Semiconductor metal heater technology is evolving from conventional resistance-based heating toward intelligent thermal management systems capable of supporting advanced wafer fabrication. Current deployments increasingly utilize multi-zone heating architectures, precision temperature sensors, and integrated control platforms. More than 60% of newly installed advanced process tools now incorporate enhanced thermal monitoring capabilities. These technologies improve temperature uniformity by approximately 15% and reduce process variability across critical semiconductor manufacturing stages.

Emerging technologies include AI-enabled thermal optimization, predictive maintenance platforms, and advanced alloy-based heater designs engineered for tighter process tolerances. Compared with traditional single-zone systems, modern multi-zone semiconductor heaters deliver nearly 18% better thermal consistency and reduce maintenance interventions by approximately 12%. Adoption is particularly strong among advanced logic and memory manufacturers seeking greater process stability and higher wafer yields. Equipment suppliers benefit through stronger differentiation and deeper integration into semiconductor production ecosystems.

Between 2026 and 2028, intelligent thermal systems, digital twins, and connected process control platforms are expected to become core competitive differentiators. Smart thermal analytics can improve equipment utilization by nearly 10%, while advanced materials enhance durability under demanding operating conditions. Companies investing early in intelligent heating architectures, integrated controls, and predictive performance optimization will secure operational advantages as semiconductor manufacturing complexity continues increasing.

May 2025 – Backer Hotwatt introduced flexible lead technology for semiconductor heating applications, enabling improved integration into compact test fixtures. The solution enhanced heating responsiveness while supporting higher throughput and lower heater failure rates in precision semiconductor testing environments. Source: www.hotwatt.com

July 2024 – Backer Hotwatt highlighted expanding semiconductor heating demand following U.S. semiconductor manufacturing investments. The company noted that the CHIPS Act had already supported 83 announced semiconductor ecosystem projects, strengthening long-term demand for precision thermal processing technologies.

September 2025 – Watlow showcased advanced semiconductor thermal solutions at SEMICON India 2025, highlighting a portfolio supported by more than 1,100 patents. The initiative strengthened engagement with semiconductor manufacturers pursuing energy-efficient and precision-controlled thermal processing systems.

November 2025 – Watlow presented intelligent semiconductor heating technologies at SEMICON Europa 2025, including thermal management platforms capable of delivering up to 50% energy savings in selected semiconductor applications. The development reinforced the industry's shift toward intelligent and sustainable thermal process optimization.

The Semiconductor Metal Heater Market Report provides comprehensive analysis across key heater technologies, semiconductor manufacturing applications, end-user groups, and major geographic markets. The study evaluates demand patterns across wafer processing, deposition, etching, lithography, advanced packaging, and testing environments while examining adoption trends among foundries, integrated device manufacturers, OSAT providers, and research organizations. More than 60% of advanced fabrication investments are increasingly linked to precision thermal management requirements, highlighting the growing importance of high-performance heating technologies.

The report further assesses competitive positioning, technology evolution, supply-chain developments, manufacturing expansion strategies, and emerging deployment trends across North America, Europe, Asia-Pacific, South America, and the Middle East & Africa. It covers intelligent thermal controls, multi-zone heating architectures, predictive maintenance integration, and advanced material innovations shaping future market direction. Strategic insights support investment prioritization, capacity planning, partnership evaluation, product development, and competitive benchmarking between 2026 and 2033, enabling stakeholders to identify operational opportunities and long-term growth priorities.

| Report Attribute / Metric | Details |

|---|---|

| Market Revenue (2025) | USD 500.0 Million |

| Market Revenue (2033) | USD 859.1 Million |

| CAGR (2026–2033) | 7.0% |

| Base Year | 2025 |

| Forecast Period | 2026–2033 |

| Historic Period | 2021–2025 |

| Segments Covered |

By Type

By Application

By End-User

|

| Key Report Deliverables | Revenue Forecast; Market Trends; Growth Drivers & Restraints; Technology Insights; Segmentation Analysis; Regional Insights; Competitive Landscape; Regulatory & ESG Overview; Recent Developments |

| Regions Covered | North America; Europe; Asia-Pacific; South America; Middle East & Africa |

| Key Players Analyzed | Watlow; Durex Industries; Tempco Electric Heater Corporation; Backer Hotwatt; Thermcraft Inc.; Omega Engineering; Tutco Heating Solutions Group; Chromalox; Industrial Heater Corporation; Delta MFG; Wattco; Nexthermal Corporation; Thermal Corporation; Rama Corporation |

| Customization & Pricing | Available on Request (10% Customization Free) |