Reports

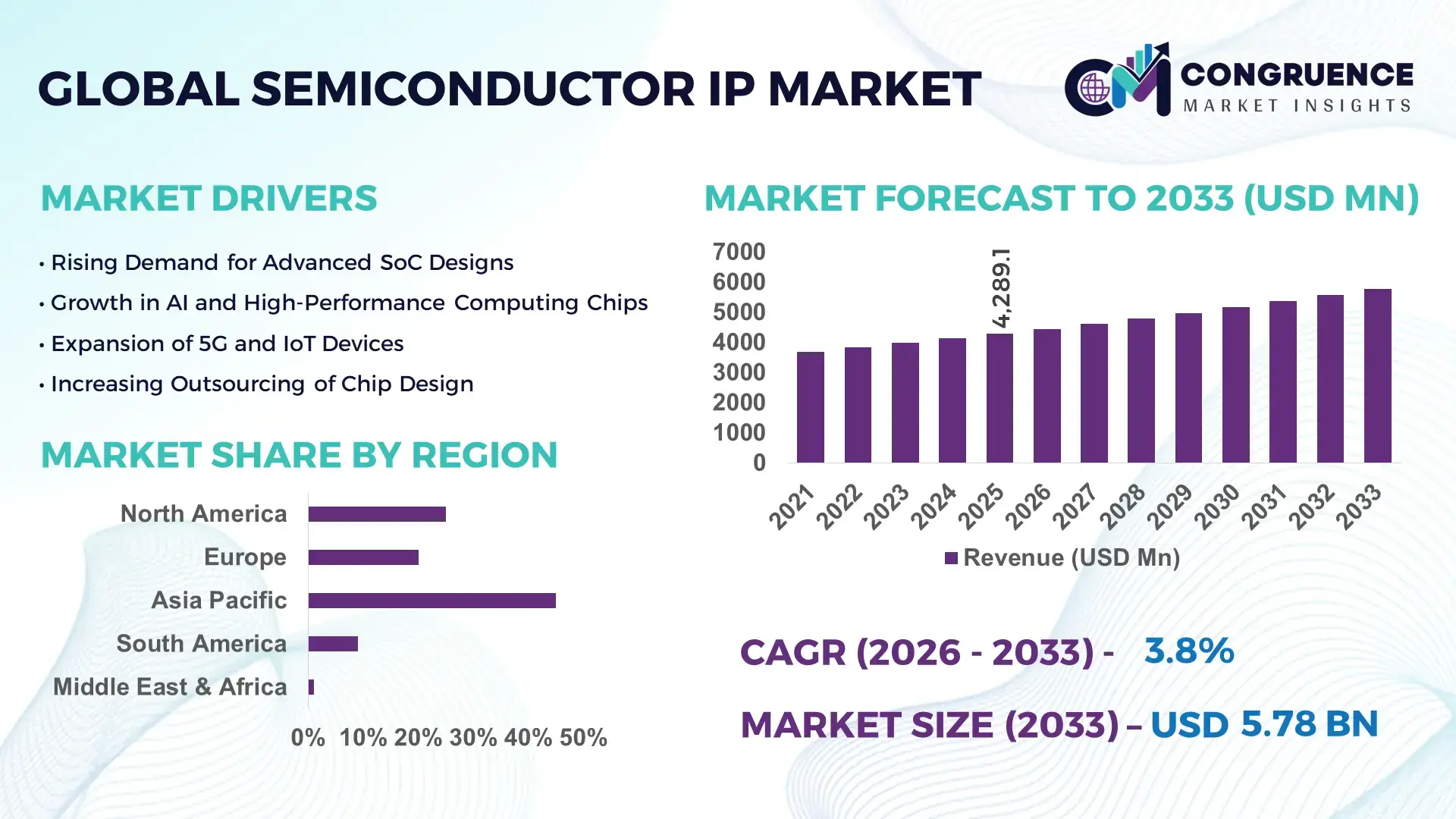

The Global Semiconductor IP Market was valued at USD 4289.08 Million in 2025 and is anticipated to reach a value of USD 5780.21 Million by 2033 expanding at a CAGR of 3.8% between 2026 and 2033. The steady expansion is primarily driven by accelerating SoC integration across AI-enabled consumer electronics, 5G infrastructure, and advanced automotive electronics platforms.

The United States leads the Semiconductor IP market with a strong concentration of fabless semiconductor companies and IP design houses. Over 60% of leading global chip design firms operate R&D facilities in the U.S., supported by multibillion-dollar federal semiconductor incentives and private investments exceeding USD 50 billion in advanced chip design and EDA ecosystems between 2022 and 2025. The country hosts major CPU, GPU, and interface IP developers supplying high-performance computing, hyperscale data centers, aerospace systems, and autonomous vehicle chipsets. More than 70% of advanced-node SoC designs below 7nm incorporate U.S.-originated processor and connectivity IP cores, reinforcing its leadership in innovation-intensive semiconductor IP licensing and customization services.

Market Size & Growth: Valued at USD 4,289.08 million in 2025, projected to reach USD 5,780.21 million by 2033 at 3.8% CAGR, driven by rising SoC complexity and AI-centric chip architectures.

Top Growth Drivers: AI chip adoption up 42%, automotive semiconductor content growth 35%, 5G chipset integration expansion 38%.

Short-Term Forecast: By 2028, advanced IP reuse strategies are expected to reduce chip development cycles by 25% and lower design costs by 18%.

Emerging Technologies: Chiplet-based architectures, RISC-V open-standard processor cores, advanced 3nm and 2nm node IP optimization.

Regional Leaders: North America projected at USD 2,150 million by 2033 with strong HPC integration; Asia-Pacific at USD 2,300 million driven by consumer electronics manufacturing; Europe at USD 950 million with automotive semiconductor specialization.

Consumer/End-User Trends: Automotive OEMs, cloud service providers, and mobile chipset vendors increasingly adopt customizable low-power processor IP.

Pilot Example: In 2024, a leading fabless firm reduced silicon respins by 30% through AI-driven IP verification tools.

Competitive Landscape: ARM Holdings holds approximately 40% share, followed by Synopsys, Cadence Design Systems, Imagination Technologies, and Rambus.

Regulatory & ESG Impact: Energy-efficient IP cores reducing chip-level power consumption by 20% align with global carbon neutrality mandates by 2030.

Investment & Funding Patterns: Over USD 12 billion invested globally in semiconductor design innovation and IP development programs between 2023 and 2025.

Innovation & Future Outlook: Integration of AI accelerators, security IP modules, and heterogeneous multi-die packaging will define next-generation semiconductor IP ecosystems.

The Semiconductor IP market serves critical industry verticals including consumer electronics contributing nearly 35% of total IP licensing demand, automotive electronics at approximately 22%, data centers and high-performance computing around 20%, and industrial IoT close to 15%. Rapid innovation in RISC-V processor cores, advanced memory interface IP such as LPDDR5X and PCIe 6.0, and embedded security modules are reshaping chip architecture efficiency. Regulatory pressure for energy-efficient computing and data privacy compliance is accelerating adoption of low-power, hardware-level encryption IP. Asia-Pacific accounts for over 45% of semiconductor IP consumption due to concentrated electronics manufacturing hubs, while Europe demonstrates strong growth in automotive-grade functional safety IP solutions. Future outlook indicates expanding demand for chiplet interoperability standards, edge AI acceleration blocks, and automotive ADAS-integrated IP platforms.

The Semiconductor IP Market plays a foundational role in enabling scalable, cost-efficient system-on-chip development across AI, automotive, telecommunications, and cloud computing industries. As chip complexity surpasses 100 billion transistors at advanced nodes, reusable processor, memory, and interface IP blocks reduce development timelines by nearly 30% compared to fully custom architectures. Chiplet-based integration delivers 20% performance improvement compared to monolithic 10nm legacy designs, while advanced 3nm process-optimized IP improves power efficiency by up to 25% versus older 7nm standards.

Asia-Pacific dominates in semiconductor production volume, while North America leads in IP adoption with over 65% of enterprises utilizing third-party licensable cores in advanced SoC programs. By 2028, AI-assisted electronic design automation tools are expected to cut verification cycles by 35%, enhancing time-to-market competitiveness. Firms are committing to ESG improvements such as 30% reduction in design-related energy simulation workloads by 2030 through optimized low-power IP frameworks.

In 2024, a U.S.-based semiconductor design firm achieved 28% silicon area optimization through AI-driven IP configuration and automated floorplanning technologies. As digital transformation accelerates across automotive electrification and edge computing sectors, the Semiconductor IP Market is positioned as a strategic pillar for resilient supply chains, regulatory compliance, advanced performance optimization, and sustainable semiconductor innovation.

The surge in AI-enabled devices and data center processors significantly boosts demand for configurable Semiconductor IP cores. AI workloads require specialized neural processing units, high-bandwidth memory controllers, and advanced interconnect IP blocks. Over 50% of newly designed SoCs integrate AI acceleration modules, increasing reliance on licensable processor IP. Automotive electronics now incorporate over 1,500 semiconductor components per electric vehicle, intensifying demand for safety-certified IP solutions. Furthermore, 5G and emerging 6G infrastructure deployments require high-speed SerDes and PCIe 6.0 interface IP, enabling faster data throughput and lower latency. These factors collectively stimulate strong demand for scalable, energy-efficient Semiconductor IP platforms.

Semiconductor IP licensing involves significant upfront fees, royalty structures, and compliance testing expenses. Advanced-node IP optimized for 3nm or 2nm fabrication can require extensive validation, increasing development overhead. Integration of third-party IP into custom SoC architectures often demands additional verification cycles, raising engineering resource allocation by nearly 15%. Smaller design startups face barriers due to limited capital for multi-core IP licensing packages. Moreover, interoperability issues between heterogeneous IP blocks may cause silicon respins, which can delay product launches by several months. These financial and technical complexities act as limiting factors, particularly for emerging fabless semiconductor firms.

The growing adoption of chiplet-based design frameworks opens substantial opportunities for modular Semiconductor IP integration. Chiplet interoperability standards enable flexible combination of processor, memory, and connectivity IP, reducing development risk by approximately 20%. RISC-V open-standard architecture adoption has increased by over 40% in embedded systems, encouraging customization and reducing dependence on proprietary instruction sets. Automotive OEMs and industrial IoT developers increasingly favor scalable RISC-V cores for application-specific SoCs. Additionally, edge AI computing expansion generates demand for ultra-low-power IP optimized for real-time analytics. These evolving architecture models provide strong growth prospects for IP vendors offering interoperable, secure, and customizable design solutions.

Global semiconductor supply chain disruptions and export control regulations create uncertainty for cross-border IP licensing agreements. Advanced-node transitions below 5nm require highly specialized design expertise and EDA compatibility, increasing R&D expenditure by nearly 20%. Strict compliance requirements related to encryption standards and automotive functional safety certifications add additional development timelines. Furthermore, talent shortages in advanced semiconductor design engineering limit scalability for IP developers. Combined with rapid technological obsolescence cycles, these challenges require continuous innovation investment, collaborative ecosystem development, and diversified geographic design capabilities to sustain long-term competitiveness in the Semiconductor IP Market.

• Over 48% Surge in RISC-V Core Deployments Across Embedded and Edge Devices

RISC-V processor IP adoption has increased by more than 48% in embedded and edge computing applications over the past three years. Over 3,500 commercial RISC-V-based chip designs were reported globally in 2024, compared to fewer than 2,000 designs in 2021. More than 60% of new microcontroller design projects in Asia-Pacific now evaluate RISC-V cores as a primary architecture option. This trend reflects growing demand for customizable, license-flexible processor IP capable of reducing silicon area by nearly 15% compared to legacy proprietary cores.

• 35% Increase in Chiplet-Based IP Integration for Advanced Node Designs

Chiplet-enabled architectures have witnessed a 35% rise in adoption within high-performance computing and data center processors. Approximately 50% of advanced-node SoCs below 5nm now integrate multi-die configurations using standardized interconnect IP. Chiplet partitioning reduces development risk by nearly 20% and enhances yield efficiency by up to 18%. North American and Taiwanese semiconductor design ecosystems are actively investing in interoperable chiplet interface IP, enabling modular scalability across AI accelerators and networking processors.

• 28% Growth in Security and Hardware Root-of-Trust IP Deployment

Hardware-level security IP modules, including cryptographic accelerators and root-of-trust blocks, have expanded by 28% in integration across automotive and IoT chipsets. Over 70% of newly certified automotive-grade SoCs now incorporate dedicated security IP compliant with ISO 21434 cybersecurity standards. Increasing data privacy mandates and secure boot requirements in connected devices have driven a 22% rise in demand for embedded encryption engines in 2024 compared to the previous year.

• 32% Expansion in AI-Optimized Memory and Interconnect IP Utilization

AI workloads have accelerated demand for high-bandwidth memory interface IP, with LPDDR5X and HBM integration increasing by 32% across next-generation GPUs and AI accelerators. Over 65% of data center accelerator designs now include advanced PCIe 5.0 or 6.0 controller IP to support high-throughput processing. Memory subsystem optimization improves bandwidth efficiency by nearly 25%, enabling lower latency for large-scale neural network training and inference tasks.

The Semiconductor IP market is segmented by type, application, and end-user industry, reflecting the diverse integration requirements of modern system-on-chip development. Processor IP, interface IP, memory IP, and security IP collectively address performance optimization, connectivity, and functional safety demands. Application-wise, consumer electronics and automotive electronics account for the largest integration volumes, followed by data centers, telecommunications, and industrial IoT. End-user insights reveal strong adoption among fabless semiconductor companies and integrated device manufacturers, while emerging growth is observed in automotive OEM design divisions and hyperscale cloud infrastructure providers. More than 70% of new SoC programs globally rely on third-party licensable IP blocks, underscoring the critical role of reusable and standards-compliant semiconductor IP components across multiple verticals.

Processor IP holds approximately 38% of total Semiconductor IP adoption, driven by extensive integration of CPU, GPU, and AI accelerator cores across advanced SoCs. Its leadership position stems from widespread deployment in over 75% of complex chip designs targeting mobile, automotive, and high-performance computing platforms. Interface IP accounts for nearly 27% of integration demand, supporting high-speed standards such as PCIe 6.0, USB4, and DDR5. Memory IP contributes around 20%, while security and analog IP together represent the remaining 15%. Processor IP remains the fastest-growing segment, expanding at an estimated 6.2% CAGR due to rising AI-centric workloads and automotive electrification trends. The increasing integration of heterogeneous multi-core architectures has boosted configurable processor core demand by nearly 30% over the past two years. Meanwhile, interface IP continues to grow steadily as 5G baseband and data center interconnect requirements intensify.

Consumer electronics leads Semiconductor IP applications with roughly 35% share, driven by smartphone SoCs, wearable devices, and smart home controllers. Over 1.4 billion smartphones shipped globally in 2024, with more than 90% integrating licensed processor and interface IP blocks. Automotive electronics accounts for approximately 24% of adoption, reflecting the increasing semiconductor content exceeding 1,500 chips per electric vehicle. Data centers and high-performance computing contribute nearly 22%, while telecommunications and industrial automation collectively represent 19%. Automotive electronics is the fastest-growing application, expanding at around 7.1% CAGR, supported by ADAS deployment growth of 40% across new vehicle models. Advanced driver-assistance processors increasingly require safety-certified and security-enhanced IP modules. Data center AI accelerators are also experiencing strong integration growth due to rising cloud workload demands.

Fabless semiconductor companies represent the leading end-user group with approximately 44% share, leveraging external IP to accelerate design cycles and reduce R&D overhead by nearly 30%. Integrated device manufacturers account for around 28% of adoption, utilizing proprietary and third-party IP combinations for diversified product portfolios. Automotive OEM-affiliated design units contribute about 15%, while cloud infrastructure and telecom equipment providers together comprise roughly 13%. Automotive OEM design divisions are the fastest-growing end-user segment, expanding at nearly 7.5% CAGR as vehicle electrification and autonomous driving development intensify. Over 65% of new EV platforms incorporate dedicated ADAS and infotainment SoCs built on licensed processor and safety IP cores. Cloud service providers have increased custom silicon initiatives by 35% in the past two years to optimize AI workload efficiency.

Asia-Pacific accounted for the largest market share at 45% in 2025 however, North America is expected to register the fastest growth, expanding at a CAGR of 5.1% between 2026 and 2033.

Asia-Pacific’s leadership is supported by high semiconductor manufacturing density, with over 70% of global chip fabrication capacity located across Taiwan, South Korea, China, and Japan. More than 60% of global consumer electronics production is concentrated in this region, driving substantial integration of processor, interface, and memory IP blocks. North America holds approximately 30% share, driven by advanced SoC design, hyperscale AI chip programs, and over 65% enterprise-level IP reuse in high-performance computing applications. Europe accounts for nearly 15%, supported by automotive semiconductor integration exceeding 1,200 chips per vehicle in premium EV models. South America and Middle East & Africa collectively contribute around 10%, with rising adoption in telecom infrastructure and industrial automation projects exceeding 18% annual deployment growth in select economies.

How Is Advanced AI Chip Design Accelerating Enterprise-Scale IP Integration?

North America represents approximately 30% of the global Semiconductor IP market share, supported by a strong concentration of fabless semiconductor firms and hyperscale cloud infrastructure providers. Over 65% of complex AI accelerator chips designed in this region incorporate third-party processor and interconnect IP blocks. Key industries driving demand include data centers, automotive ADAS platforms, aerospace electronics, and high-frequency telecom infrastructure. Government-backed semiconductor incentive programs exceeding USD 50 billion between 2022 and 2025 have strengthened domestic design capabilities and advanced-node research below 5nm. Technological transformation trends include AI-assisted chip verification, reducing validation cycles by nearly 35%, and chiplet-based heterogeneous integration improving yield by 18%. A leading local player, Synopsys, expanded its AI-driven EDA-IP co-optimization platform in 2024, enabling 25% faster design closure for advanced SoCs. Enterprise adoption behavior reflects strong uptake in healthcare and financial services, where over 55% of large organizations deploy custom silicon solutions for AI-driven analytics and secure processing.

How Are Automotive Safety Standards Driving Functional IP Innovation?

Europe accounts for approximately 15% of the global Semiconductor IP market, with Germany, the United Kingdom, and France representing over 70% of regional demand. Automotive electronics is the dominant industry vertical, contributing nearly 40% of regional IP integration volume due to high adoption of ADAS and EV control systems. More than 1,200 semiconductor components are embedded in premium electric vehicles manufactured within this region. Regulatory frameworks focused on functional safety (ISO 26262) and cybersecurity compliance have increased demand for certified processor and security IP modules by 28% over the past three years. Sustainability initiatives targeting 30% reduction in semiconductor energy consumption by 2030 are accelerating low-power IP innovation. A notable regional player, Arm, continues expanding automotive-grade CPU and GPU IP solutions optimized for real-time safety applications. Consumer behavior emphasizes regulatory-aligned and explainable hardware security features, with over 50% of automotive OEMs prioritizing certified IP integration in new vehicle platforms.

Why Is High-Volume Electronics Manufacturing Fueling IP Design Expansion?

Asia-Pacific holds nearly 45% of the Semiconductor IP market volume, ranking first globally in design and fabrication integration. China, Taiwan, Japan, South Korea, and India collectively account for over 80% of regional semiconductor consumption. The region supports more than 70% of global wafer fabrication output and over 60% of electronics assembly operations, driving substantial processor and memory IP licensing activity. Infrastructure expansion in 5G networks, with over 2.5 million base stations deployed across major economies, increases demand for high-speed interface IP blocks. Innovation hubs in Shenzhen, Hsinchu, Seoul, and Bangalore are advancing AI-enabled SoC design, with RISC-V adoption increasing by 40% in embedded systems. MediaTek, a prominent regional player, expanded its AI-integrated mobile chipset portfolio in 2024, incorporating advanced memory and connectivity IP to enhance 20% higher processing efficiency. Consumer trends reflect strong demand for mobile AI applications and e-commerce platforms, contributing to 35% growth in smartphone SoC integration projects.

How Is Telecom Infrastructure Modernization Supporting IP Adoption?

South America represents approximately 6% of the global Semiconductor IP market, with Brazil and Argentina contributing nearly 65% of regional demand. Expansion of 4G and 5G infrastructure, covering over 75% of urban populations, drives increased integration of network processor and interface IP modules. The energy and mining sectors are adopting industrial IoT platforms, leading to 22% growth in embedded controller IP usage across automation systems. Government incentives focused on digital inclusion and trade policy reforms have supported a 15% rise in domestic electronics assembly operations since 2022. Local semiconductor design startups in Brazil are collaborating with international IP vendors to develop customized microcontroller solutions for smart metering systems, improving energy efficiency by 18%. Consumer behavior patterns indicate demand tied to localized media streaming and language-specific mobile applications, boosting integration of AI-enabled processor IP in consumer devices.

What Role Does Digital Infrastructure Investment Play in Advanced IP Deployment?

Middle East & Africa accounts for approximately 4% of the global Semiconductor IP market, with the UAE and South Africa representing over 55% of regional demand. Rapid digital transformation initiatives, including smart city projects and oil & gas automation platforms, have increased deployment of industrial control SoCs by nearly 20% since 2023. Over 65% of new infrastructure projects in the Gulf region integrate AI-enabled monitoring systems requiring secure processor and connectivity IP. Trade partnerships with Asian semiconductor manufacturers have enhanced access to advanced chip design ecosystems. In 2024, a UAE-based technology hub launched an AI semiconductor innovation program supporting local startups to integrate energy-efficient processor IP into smart grid applications, targeting 25% improvement in operational efficiency. Consumer behavior trends reflect growing adoption of digital banking and e-government services, increasing secure hardware IP integration across enterprise IT infrastructure.

United States – 30% share: Strong fabless semiconductor ecosystem and high enterprise adoption of advanced Semiconductor IP in AI and cloud computing platforms.

China – 22% share: Large-scale electronics manufacturing base and expanding domestic SoC design programs driving extensive Semiconductor IP integration.

The Semiconductor IP market is moderately consolidated, with the top five companies accounting for approximately 68% of total global share. More than 120 active IP vendors operate globally, ranging from processor core specialists to niche interface and security IP providers. ARM Holdings leads with close to 40% share in licensable processor IP, followed by Synopsys and Cadence Design Systems with strong portfolios spanning interface, memory, and verification IP. Imagination Technologies and Rambus maintain competitive positions in GPU and high-speed interface IP respectively.

Strategic initiatives include multi-year licensing agreements, cross-border R&D partnerships, and AI-driven EDA-IP integration platforms. Over 35% of new product launches in 2024 focused on AI accelerator IP and chiplet interoperability solutions. Mergers and acquisitions have increased by 18% over the past two years, targeting specialized analog and security IP startups. Competitive differentiation increasingly depends on advanced-node optimization below 5nm, ESG-aligned low-power designs reducing chip energy consumption by 20%, and bundled IP-EDA toolchain solutions that shorten time-to-market by nearly 25%.

Arm Holdings

Synopsys, Inc.

Cadence Design Systems, Inc.

Imagination Technologies Group

Rambus Inc.

CEVA, Inc.

Alphawave IP Group

VeriSilicon Microelectronics

Lattice Semiconductor

SiFive, Inc.

The Semiconductor IP market is being reshaped by advanced node migration, heterogeneous integration, AI-driven design automation, and security-centric architectures. As chip designs move below 5nm, over 50% of advanced SoCs now rely on pre-verified IP blocks optimized for 3nm and emerging 2nm processes to manage signal integrity, power density, and thermal constraints. Process-optimized standard cell libraries and high-speed SerDes IP operating beyond 112G PAM4 are becoming essential for next-generation networking and data center processors.

Chiplet-based architectures represent a significant technological shift, with nearly 35% of high-performance computing chips integrating multi-die configurations. Standardized die-to-die interconnect IP, such as UCIe-compliant interfaces, reduces integration complexity by approximately 20% and improves yield efficiency by up to 15%. This modular design approach allows flexible scaling of CPU, GPU, AI accelerator, and memory components across multiple performance tiers.

AI-enabled electronic design automation tools are accelerating IP configuration and verification workflows. Over 40% of large semiconductor firms now deploy machine learning algorithms for design rule checking and predictive validation, reducing verification time by nearly 30%. Additionally, embedded security IP modules—including hardware root-of-trust, quantum-resistant cryptographic accelerators, and secure enclave architectures—are integrated in more than 70% of automotive-grade SoCs to meet stringent cybersecurity regulations.

RISC-V architecture adoption has surpassed 10 billion cumulative shipped cores globally, reflecting growing demand for customizable and royalty-flexible processor IP. Simultaneously, advanced memory IP such as LPDDR5X and HBM3E controllers supports bandwidth exceeding 1 TB/s in AI accelerators, enabling high-throughput processing for cloud-scale machine learning workloads. These technology advancements collectively strengthen design efficiency, performance scalability, and long-term ecosystem interoperability in the Semiconductor IP market.

• In April 2024, Arm introduced the Arm Neoverse V3 and CSS V3 platforms targeting data center and AI infrastructure. The new architecture delivers up to 50% higher performance for cloud-native workloads and supports advanced 3nm process technologies, enhancing hyperscale computing efficiency. Source: www.arm.com

• In March 2024, Synopsys expanded its DesignWare IP portfolio with a 224G Ethernet PHY IP solution optimized for AI and high-performance computing chips. The solution supports data rates up to 224 Gb/s per lane, addressing next-generation networking and data center bandwidth requirements. Source: www.synopsys.com

• In May 2024, Cadence launched its Tensilica NeuroEdge 130 AI Co-Processor IP, designed for edge AI applications. The processor delivers up to 30% lower power consumption for always-on AI workloads in consumer and industrial IoT devices. Source: www.cadence.com

• In February 2025, Rambus announced the expansion of its DDR5 and LPDDR5X memory interface IP portfolio, enabling support for data rates exceeding 8,800 MT/s. The enhancement targets AI accelerators and next-generation server platforms requiring higher memory bandwidth efficiency. Source: www.rambus.com

The Semiconductor IP Market Report provides a comprehensive assessment of processor IP, interface IP, memory IP, security IP, and analog IP segments, covering integration trends across advanced nodes from 28nm to sub-3nm technologies. The report evaluates adoption across major application areas including consumer electronics, automotive electronics, data centers, telecommunications infrastructure, aerospace, and industrial IoT. More than 70% of modern SoC designs incorporate third-party licensable IP, underscoring the report’s focus on reusable and standards-compliant design ecosystems.

Geographically, the scope spans North America, Europe, Asia-Pacific, South America, and Middle East & Africa, analyzing regional production density, semiconductor fabrication capacity exceeding 70% concentration in Asia-Pacific, and enterprise-level adoption rates surpassing 65% in North America. The study includes detailed examination of chiplet integration frameworks, UCIe-based interconnect IP standards, RISC-V processor adoption trends exceeding 10 billion shipped cores, and high-speed interface technologies supporting 224G data rates.

The report further addresses compliance requirements such as automotive functional safety standards and cybersecurity mandates impacting over 70% of connected device SoCs. Emerging segments including AI accelerator IP, quantum-resistant security modules, and heterogeneous multi-die packaging solutions are analyzed alongside supply chain diversification strategies. The structured coverage enables stakeholders to evaluate competitive positioning, technology evolution pathways, and cross-industry semiconductor IP deployment patterns across more than 15 key industry verticals worldwide.

| Report Attribute/Metric | Report Details |

|---|---|

|

Market Revenue in 2025 |

USD V2025 Million |

|

Market Revenue in 2033 |

USD V2033 Million |

|

CAGR (2026 - 2033) |

3.8% |

|

Base Year |

2025 |

|

Forecast Period |

2026 - 2033 |

|

Historic Period |

2021 - 2025 |

|

Segments Covered |

By Types

By Application

By End-User

|

|

Key Report Deliverable |

Revenue Forecast, Growth Trends, Market Dynamics, Segmental Overview, Regional and Country-wise Analysis, Competition Landscape |

|

Region Covered |

North America, Europe, Asia-Pacific, South America, Middle East, Africa |

|

Key Players Analyzed |

Arm Holdings , Synopsys, Inc. , Cadence Design Systems, Inc., Imagination Technologies Group, Rambus Inc., CEVA, Inc., Alphawave IP Group, VeriSilicon Microelectronics, Lattice Semiconductor, SiFive, Inc. |

|

Customization & Pricing |

Available on Request (10% Customization is Free) |