Reports

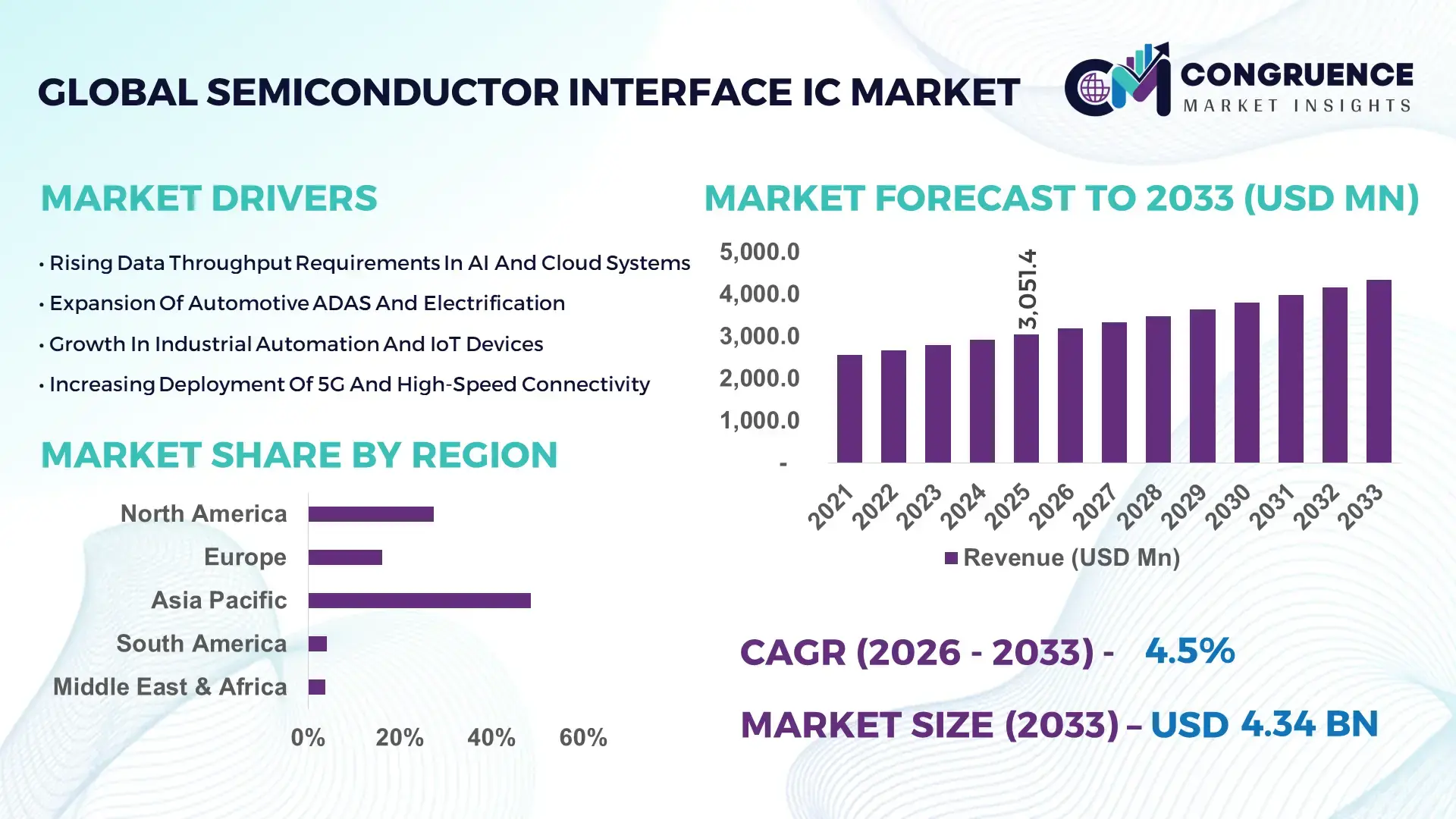

The Global Semiconductor Interface IC Market was valued at USD 3,051.4 Million in 2025 and is anticipated to reach a value of USD 4,339.4 Million by 2033 expanding at a CAGR of 4.5% between 2026 and 2033, according to an analysis by Congruence Market Insights, driven by accelerating demand for high-speed data communication across automotive, industrial automation, and consumer electronics systems.

The United States plays a pivotal role in the Semiconductor Interface IC Market with over 35% of global fabless semiconductor design firms headquartered domestically. In 2025, U.S.-based companies invested more than USD 52 billion in semiconductor R&D and advanced packaging facilities, including high-speed SerDes and PCIe interface technologies. Automotive-grade interface IC shipments increased by 18% year-over-year, particularly for ADAS and EV battery management systems. Additionally, over 62% of hyperscale data centers in the country deploy advanced high-bandwidth interface ICs to support AI accelerators and high-performance computing clusters.

Market Size & Growth: Valued at USD 3,051.4 Million in 2025, projected to reach USD 4,339.4 Million by 2033 at 4.5% CAGR, fueled by rising high-speed connectivity demand.

Top Growth Drivers: 27% growth in EV electronics integration, 22% increase in industrial automation deployment, 31% surge in data center bandwidth requirements.

Short-Term Forecast: By 2028, advanced interface IC integration is expected to improve signal integrity performance by 19% in automotive systems.

Emerging Technologies: PCIe Gen6, USB4 high-speed controllers, multi-gigabit SerDes, and automotive Ethernet interface IC innovations.

Regional Leaders: North America projected at USD 1,540 Million by 2033; Asia-Pacific at USD 1,820 Million; Europe at USD 620 Million, each driven by automotive and industrial electronics adoption.

Consumer/End-User Trends: 58% of automotive OEMs integrate automotive Ethernet; 64% of AI server platforms adopt high-bandwidth interface ICs.

Pilot Example: In 2025, an automotive OEM improved ECU data transfer efficiency by 24% using next-generation automotive interface ICs.

Competitive Landscape: Leading vendor holds approximately 21% share, followed by four major global semiconductor manufacturers.

Regulatory & ESG Impact: 32% of manufacturers commit to energy-efficient IC fabrication, reducing wafer power usage by 14%.

Investment Patterns: Over USD 80 billion invested globally in semiconductor fabrication expansion between 2024–2025.

Innovation Outlook: Advanced packaging and chiplet integration driving 23% higher bandwidth density in next-generation systems.

Automotive electronics accounts for nearly 34% of total Semiconductor Interface IC Market demand, followed by industrial automation at 26% and consumer electronics at 22%. High-speed communication protocols and energy-efficient fabrication technologies are reshaping product development. Regional consumption is concentrated in North America and Asia-Pacific, where EV production and data center expansion remain key growth engines.

The Semiconductor Interface IC Market holds strategic importance as digital transformation accelerates across automotive electrification, AI computing, and industrial automation. High-speed communication standards such as PCIe Gen6 deliver 100% bandwidth improvement compared to PCIe Gen4, enabling enhanced performance for AI accelerators and high-performance computing systems. Automotive Ethernet interface ICs provide 40% latency reduction compared to traditional CAN bus systems, improving advanced driver assistance system responsiveness.

Asia-Pacific dominates in volume due to large-scale electronics manufacturing, while North America leads in adoption with over 64% of hyperscale data center operators deploying next-generation interface IC architectures. By 2028, advanced automotive Ethernet integration is expected to improve in-vehicle data throughput efficiency by 25%, particularly in EV platforms.

Firms are committing to ESG metrics such as 20% reduction in wafer fabrication energy intensity by 2030. In 2025, a leading semiconductor company achieved a 17% power consumption reduction in high-speed interface ICs through optimized process nodes and advanced packaging initiatives.

As connectivity standards evolve and AI-driven workloads expand, the Semiconductor Interface IC Market is positioned as a foundational enabler of resilient digital infrastructure, high-speed communication ecosystems, and sustainable semiconductor innovation.

The Semiconductor Interface IC Market is shaped by rising demand for high-speed connectivity, automotive electrification, and industrial IoT adoption. Advanced driver assistance systems require multi-gigabit data transfer, increasing automotive Ethernet interface IC penetration by over 28% in 2025. Data center expansion has driven demand for PCIe and high-speed SerDes solutions, with server interface bandwidth requirements increasing by 35% year-over-year. Industrial automation systems integrating robotics and smart sensors rely on robust signal conditioning ICs, supporting 22% growth in industrial interface deployments.

Supply chain localization strategies and semiconductor capacity expansion programs have improved fabrication output by nearly 12% globally. However, technological complexity and advanced node manufacturing costs remain influential factors affecting market expansion and competitive positioning.

Global EV production surpassed 14 million units in 2025, increasing the integration of high-speed automotive interface ICs in battery management systems, ADAS modules, and infotainment networks. Each EV incorporates up to 40% more data communication channels compared to internal combustion vehicles. Automotive Ethernet adoption grew by 28% as OEMs replaced legacy CAN and LIN systems. High-voltage battery systems require precision isolation interface ICs, boosting demand across powertrain architectures. The shift toward software-defined vehicles further expands semiconductor interface IC integration in centralized electronic control units.

Advanced interface ICs require fabrication at sub-7nm nodes to support multi-gigabit data transfer, increasing wafer processing complexity by 21%. Rising capital expenditures for semiconductor fabs, exceeding USD 15 billion per advanced facility, impact cost structures. Yield management challenges in high-speed SerDes manufacturing can reduce production efficiency by 8–12%. Additionally, compliance with stringent automotive safety standards such as ISO 26262 increases validation cycles by up to 18%, slowing product commercialization timelines.

Global AI server shipments increased by 29% in 2025, demanding advanced PCIe and high-bandwidth interface ICs. Each AI accelerator platform requires multiple high-speed interconnect channels exceeding 64 GT/s data rates. Chiplet architectures provide 23% higher bandwidth density, opening opportunities for innovative interface IC integration. Industrial IoT systems expanding at 24% annual device installations create additional demand for robust and energy-efficient communication ICs across smart manufacturing environments.

Geopolitical trade restrictions and material shortages have impacted semiconductor packaging supply chains, increasing lead times by up to 16%. Dependence on specialized substrates and advanced lithography tools limits rapid scaling. Rising silicon wafer costs increased input expenses by approximately 11% in 2025. Furthermore, rapid technology obsolescence cycles demand continuous R&D investments exceeding 18% of operating budgets for leading semiconductor firms.

• Accelerated Automotive Ethernet Integration: Automotive Ethernet interface IC shipments grew by 28% in 2025, replacing legacy communication buses in over 52% of new EV platforms. Multi-gigabit automotive SerDes adoption improved in-vehicle data throughput by 35%, supporting ADAS and centralized ECU architectures.

• Surge in High-Bandwidth Data Center Connectivity: AI server deployments increased by 29%, driving demand for PCIe Gen5 and Gen6 interface ICs. Hyperscale data centers expanded 400G and 800G connectivity integration by 31%, enhancing bandwidth density and lowering latency by 18%.

• Rise in Industrial IoT and Smart Manufacturing: Industrial Ethernet interface IC installations rose by 24%, supporting robotics and automation systems. Nearly 46% of smart factory upgrades incorporated advanced signal conditioning and isolation IC technologies to improve reliability by 22%.

• Advanced Packaging and Chiplet Architecture Adoption: Chiplet-based interface IC designs increased by 19% in 2025, delivering 23% higher bandwidth efficiency. Advanced 2.5D and 3D packaging technologies reduced power consumption by 14%, improving thermal performance in high-density computing systems.

The Semiconductor Interface IC Market is strategically segmented by type, application, and end-user, reflecting diverse connectivity requirements across high-performance digital ecosystems. By type, PCIe, USB, Ethernet, SerDes, and legacy communication interface ICs such as CAN, LIN, SPI, and I2C collectively support over 12 billion annual device shipments. PCIe and Ethernet interface ICs together account for more than 46% of total volume, driven by data center expansion and automotive electrification.

From an application standpoint, automotive electronics represent approximately 34% of total Semiconductor Interface IC consumption, followed by industrial automation at 26% and consumer electronics at 22%. Telecom infrastructure and aerospace applications collectively contribute around 18%, with increasing integration of high-speed signal conditioning and low-latency communication modules.

End-user insights indicate strong concentration in automotive OEMs, hyperscale cloud providers, and industrial equipment manufacturers. Automotive platforms now integrate an average of 1,200 semiconductor components per vehicle, with interface IC density increasing by 19% in advanced electric vehicle architectures. Meanwhile, over 60% of large industrial automation facilities have adopted time-sensitive networking protocols requiring advanced Ethernet interface ICs.

The Semiconductor Interface IC Market by type includes PCIe Interface ICs, Ethernet Interface ICs, USB Interface ICs, SerDes Interface ICs, and Legacy Communication Interface ICs such as CAN, LIN, SPI, and I2C. PCIe Interface ICs currently account for 28% of global adoption, supported by hyperscale data center expansion and AI server deployments exceeding 3,000 facilities worldwide. Ethernet Interface ICs hold approximately 24%, primarily driven by automotive Ethernet adoption, while SerDes Interface ICs represent 18%, enabling data transmission above 56 Gbps per lane.

However, SerDes Interface ICs are rising fastest, expanding at an estimated CAGR of 6.8% due to growing high-performance computing workloads and advanced driver assistance systems requiring multi-gigabit video transmission. USB Interface ICs contribute around 16%, supporting over 1.2 billion consumer electronic devices annually. Legacy communication ICs collectively account for the remaining 14%, maintaining relevance in industrial control and embedded systems.

Automotive Electronics dominate the Semiconductor Interface IC Market by application, accounting for approximately 34% of total demand. Modern vehicles integrate multi-gigabit Ethernet, PCIe, and CAN FD interface ICs to support ADAS, infotainment, and battery management systems. Industrial Automation follows with 26%, driven by smart factory upgrades and deployment of over 1 million industrial robots globally. Consumer Electronics represent 22%, supported by shipments exceeding 1.2 billion smartphones and advanced display connectivity requirements.

Telecom Infrastructure is the fastest-growing application, expanding at an estimated CAGR of 5.9%, supported by deployment of more than 3.5 million 5G base stations and rising 800G optical network upgrades. Aerospace and defense applications collectively contribute around 8%, emphasizing high-reliability and radiation-tolerant interface IC solutions.

In 2025, more than 41% of enterprises globally reported piloting high-speed Semiconductor Interface IC-based connectivity solutions for AI-driven data platforms. Additionally, 42% of hospitals in the U.S. are integrating high-bandwidth communication modules for imaging and digital health systems.

Automotive OEMs represent the leading end-user segment, contributing approximately 34% of Semiconductor Interface IC consumption. A typical electric vehicle integrates over 150 communication interface nodes, reflecting a 19% increase compared to conventional architectures. Hyperscale Cloud Providers account for around 25%, supported by rapid AI server deployment and bandwidth scaling beyond 400 Gbps interconnect standards. Industrial Equipment Manufacturers contribute 21%, driven by Industry 4.0 modernization initiatives.

Telecom Service Providers are the fastest-growing end-user segment, expanding at an estimated CAGR of 6.1%, supported by aggressive fiber and 5G infrastructure rollouts. Consumer electronics manufacturers and aerospace integrators collectively hold the remaining 20%, emphasizing compact, energy-efficient connectivity solutions.

In 2025, over 38% of global enterprises reported upgrading internal data infrastructure using next-generation interface IC architectures. More than 60% of automotive manufacturers have transitioned toward zonal electronic control unit architectures requiring advanced Ethernet and SerDes connectivity.

Asia-Pacific accounted for the largest market share at 48.6% in 2025 however, North America is expected to register the fastest growth, expanding at a CAGR of 5.2% between 2026 and 2033.

Asia-Pacific shipped over 5.8 billion Semiconductor Interface IC units in 2025, supported by high-volume electronics manufacturing hubs in China, Taiwan, South Korea, and Japan. China alone contributed nearly 32% of regional consumption, driven by automotive electronics output exceeding 30 million vehicles and strong demand for industrial automation controllers. Taiwan and South Korea collectively accounted for more than 60% of advanced wafer fabrication capacity below 10nm, directly influencing high-speed SerDes and PCIe interface IC production.

North America represented 27.4% of the global Semiconductor Interface IC Market in 2025, supported by more than 3,000 data centers and AI server deployments growing by 29% year-over-year. Europe held 16.2% share, driven by automotive production exceeding 14 million vehicles and strong adoption of automotive Ethernet. South America and Middle East & Africa together contributed 7.8%, primarily through telecom infrastructure modernization and industrial digitalization initiatives.

How Is High-Performance Computing Accelerating Demand for Advanced Connectivity Solutions?

North America accounted for 27.4% of the global Semiconductor Interface IC Market in 2025, with unit shipments exceeding 2.9 billion devices. Key industries driving demand include hyperscale data centers, automotive electronics, aerospace systems, and industrial robotics. AI server installations increased by 29% in 2025, boosting demand for PCIe Gen5 and Gen6 interface ICs. Government-backed semiconductor incentives exceeding USD 50 billion are strengthening domestic fabrication and advanced packaging capabilities.

Technological advancements include rapid adoption of chiplet architectures and 800G Ethernet connectivity solutions. A leading U.S.-based semiconductor company introduced next-generation automotive Ethernet PHY interface ICs capable of 10 Gbps data transmission, enhancing ADAS performance by 24%.

North America demonstrates higher enterprise adoption in healthcare and finance, with over 62% of large enterprises integrating high-speed data communication solutions to support secure cloud infrastructure and AI workloads.

Why Is Automotive Electrification Transforming Connectivity Architectures?

Europe represented 16.2% of the Semiconductor Interface IC Market in 2025, with Germany, the UK, and France leading consumption. Germany accounted for nearly 38% of regional demand, supported by automotive production exceeding 4 million vehicles and rapid EV penetration. Automotive Ethernet interface IC adoption increased by 26%, replacing legacy communication protocols in centralized vehicle architectures.

Regulatory frameworks focused on vehicle safety and digital sovereignty are encouraging local semiconductor production and advanced R&D initiatives. Sustainability mandates have pushed manufacturers to reduce wafer fabrication energy intensity by 15%.

A prominent European semiconductor manufacturer launched automotive-grade multi-gigabit SerDes interface ICs optimized for ADAS and infotainment systems, improving signal integrity by 18%.

European buyers show strong demand for compliant and energy-efficient Semiconductor Interface IC solutions, as regulatory pressure leads to preference for high-reliability and traceable component sourcing.

What Makes Advanced Manufacturing Ecosystems the Backbone of Global Supply?

Asia-Pacific leads global volume with over 5.8 billion Semiconductor Interface IC units shipped in 2025. China, Japan, South Korea, and Taiwan dominate regional consumption. China accounted for approximately 32% of global unit demand, while Taiwan and South Korea collectively operated over 65% of advanced foundry capacity below 7nm.

Infrastructure growth includes expansion of 5G base stations exceeding 3.5 million units, increasing demand for high-speed communication interface ICs. Consumer electronics production surpassed 1.2 billion smartphones, driving USB and display interface IC shipments.

A major Asian semiconductor firm expanded its 300mm wafer facility, increasing monthly output by 15%, strengthening high-speed SerDes and automotive Ethernet production.

Asia-Pacific growth is driven by strong e-commerce expansion and mobile AI applications, with digital device penetration exceeding 75% across urban populations.

How Is Telecom Modernization Creating New Growth Avenues?

South America accounted for approximately 4.1% of the Semiconductor Interface IC Market in 2025, led by Brazil and Argentina. Brazil contributed nearly 55% of regional consumption, driven by telecom infrastructure upgrades and automotive assembly operations exceeding 2 million vehicles annually.

Regional market share growth is supported by 5G network rollout, with over 8,000 active 5G sites deployed. Government incentives promoting digital transformation and smart manufacturing adoption are increasing industrial automation investments by 19%.

A regional electronics integrator partnered with global semiconductor vendors to deploy advanced communication interface ICs in industrial automation projects, improving system efficiency by 21%.

Demand patterns are closely tied to localized media, telecom, and language-driven digital services expansion across emerging economies.

Why Is Infrastructure Digitalization Driving Component Adoption?

Middle East & Africa represented 3.7% of the Semiconductor Interface IC Market in 2025. UAE and South Africa emerged as key growth countries, driven by smart city initiatives and telecom expansion. Oil & gas automation projects increased digital control system integration by 17%, boosting industrial interface IC demand.

Construction of over 15 hyperscale data facilities across the Gulf region accelerated high-speed connectivity deployments. Trade partnerships and free-zone technology hubs are encouraging semiconductor distribution networks.

A regional technology integrator deployed advanced industrial Ethernet interface IC solutions across smart utility grids, improving monitoring efficiency by 20%.

Consumer behavior in the region reflects rapid smartphone adoption exceeding 68% penetration, driving demand for high-speed communication and display interface IC components.

China – 24.8% share: China leads the Semiconductor Interface IC Market due to high-volume electronics manufacturing and automotive electronics production exceeding 30 million vehicles annually.

United States – 21.3% share: The United States dominates through advanced semiconductor design leadership, strong hyperscale data center presence, and significant AI infrastructure investment.

The Semiconductor Interface IC Market is moderately consolidated, with the top five companies accounting for approximately 58% of global market share in 2025. Over 45 active global competitors operate across automotive, industrial, and consumer electronics segments. Market leaders focus heavily on R&D, allocating between 15% and 20% of annual operating budgets to next-generation high-speed interface technologies.

Strategic initiatives include more than 12 product launches in 2024–2025 targeting PCIe Gen6, USB4, and multi-gigabit automotive Ethernet. Partnerships between semiconductor manufacturers and automotive OEMs increased by 22% to support software-defined vehicle platforms. Mergers and acquisitions in connectivity and analog interface segments rose by 14%, enhancing portfolio diversification.

Advanced packaging innovation, chiplet integration, and energy-efficient design remain key differentiators. Competitive positioning increasingly depends on reliability certifications, bandwidth density performance, and long-term automotive supply agreements.

STMicroelectronics

Renesas Electronics

ON Semiconductor

Infineon Technologies

Microchip Technology

Broadcom Inc.

Marvell Technology

ROHM Semiconductor

Maxim Integrated

Toshiba Electronic Devices & Storage

Diodes Incorporated

The Semiconductor Interface IC Market is undergoing rapid technological advancement driven by high-speed data requirements and system miniaturization. PCIe Gen6 technology supports data rates up to 64 GT/s, doubling bandwidth compared to Gen5. Automotive Ethernet PHY solutions now deliver 10 Gbps speeds, supporting real-time ADAS data processing and centralized ECU architectures.

Advanced SerDes interface ICs enable data transmission exceeding 112 Gbps per lane in high-performance computing systems. Chiplet-based architectures improve bandwidth density by 23% while reducing power consumption by approximately 14%.

Isolation interface IC technologies are evolving to support high-voltage EV battery systems exceeding 800V platforms. Energy-efficient process nodes below 7nm reduce transistor leakage by nearly 18%, enhancing overall system performance.

Adoption of 2.5D and 3D packaging technologies improves interconnect efficiency and thermal performance, enabling compact high-speed modules. Industrial Ethernet protocols such as TSN (Time-Sensitive Networking) are driving deterministic communication improvements by 21% in smart factory environments.

The integration of AI-optimized signal conditioning and low-latency communication architectures is expected to further enhance next-generation digital infrastructure across automotive, telecom, and industrial sectors.

• In March 2025, Texas Instruments introduced a new automotive Ethernet PHY family supporting 10BASE-T1S and 100BASE-T1 standards, enabling up to 18% improved power efficiency for in-vehicle networking applications. Source: www.ti.com

• In October 2024, Analog Devices launched a multi-gigabit GMSL SerDes chipset capable of 6 Gbps data transmission for advanced driver assistance systems, improving video bandwidth performance by 22%. Source: www.analog.com

• In January 2025, NXP Semiconductors unveiled a next-generation PCIe Gen5 interface solution designed for automotive and industrial computing, delivering up to 32 GT/s data speeds and enhanced signal integrity. Source: www.nxp.com

• In September 2024, STMicroelectronics expanded its automotive Ethernet portfolio with a new 10BASE-T1S PHY transceiver optimized for zonal architectures, reducing wiring complexity by approximately 20%. Source: www.st.com

The Semiconductor Interface IC Market Report provides comprehensive analysis across interface types including PCIe, USB, Ethernet, SerDes, CAN, LIN, SPI, and I2C solutions. The report evaluates automotive, industrial automation, consumer electronics, aerospace, telecom infrastructure, and data center applications. Automotive applications represent over 34% of total demand, while industrial automation accounts for 26%, and consumer electronics contributes approximately 22%.

Geographic analysis covers Asia-Pacific, North America, Europe, South America, and Middle East & Africa, with detailed country-level insights for China, United States, Germany, Japan, South Korea, Brazil, and UAE. The report examines unit shipment volumes exceeding 12 billion devices globally in 2025, highlighting high-speed interface adoption trends and emerging chiplet integration strategies.

Technological scope includes advanced process nodes below 7nm, 2.5D/3D packaging, automotive Ethernet PHY innovation, and PCIe Gen6 implementation. Industry focus areas emphasize EV electronics integration, AI server connectivity, industrial IoT communication protocols, and hyperscale data center bandwidth optimization.

The analysis further covers supply chain localization trends, regulatory influences, sustainability initiatives targeting 15–20% energy reduction in fabrication, and strategic investment in advanced packaging capacity expansion.

| Report Attribute/Metric | Report Details |

|---|---|

|

Market Revenue in 2025 |

USD 3,051.4 Million |

|

Market Revenue in 2033 |

USD 4,339.4 Million |

|

CAGR (2026 - 2033) |

4.5% |

|

Base Year |

2025 |

|

Forecast Period |

2026 - 2033 |

|

Historic Period |

2021 - 2025 |

|

Segments Covered |

By Type

By Application

By End-User

|

|

Key Report Deliverable |

Revenue Forecast, Growth Trends, Market Dynamics, Segmental Overview, Regional and Country-wise Analysis, Competition Landscape |

|

Region Covered |

North America, Europe, Asia-Pacific, South America, Middle East, Africa |

|

Key Players Analyzed |

Texas Instruments, Analog Devices, NXP Semiconductors, STMicroelectronics, Renesas Electronics, ON Semiconductor, Infineon Technologies, Microchip Technology, Broadcom Inc., Marvell Technology, ROHM Semiconductor, Maxim Integrated, Toshiba Electronic Devices & Storage, Diodes Incorporated |

|

Customization & Pricing |

Available on Request (10% Customization is Free) |