Reports

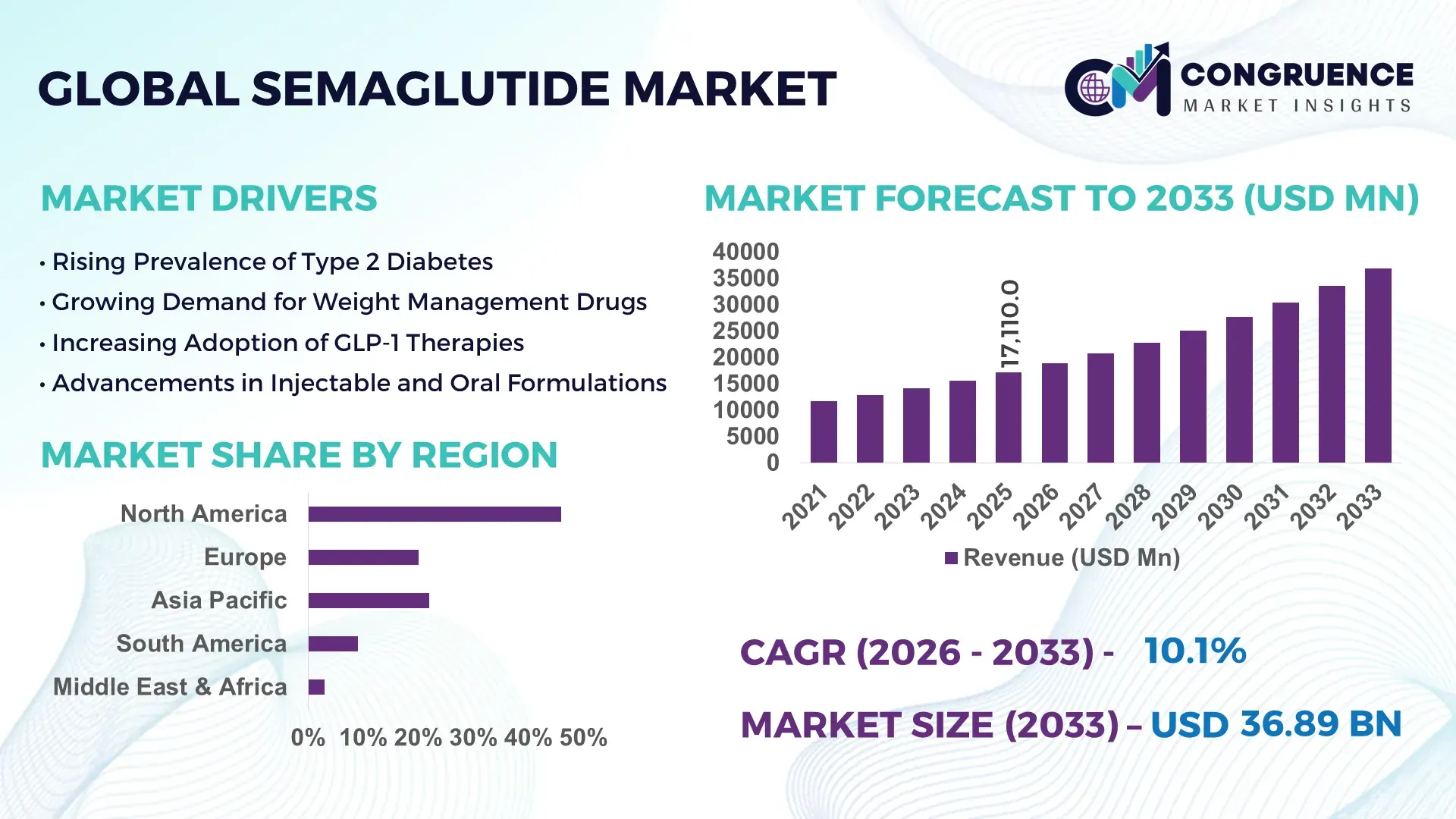

The Global Semaglutide Market was valued at USD 17110 Million in 2025 and is anticipated to reach a value of USD 36890.74 Million by 2033 expanding at a CAGR of 10.08% between 2026 and 2033. Rising global prevalence of obesity and type 2 diabetes, coupled with expanding clinical applications of GLP-1 receptor agonists, continues to accelerate demand for semaglutide-based therapies.

The United States leads the semaglutide market with advanced pharmaceutical manufacturing capacity exceeding 1.5 billion injectable doses annually, supported by over USD 4 billion in cumulative R&D investments in incretin-based therapies. More than 38 million adults diagnosed with diabetes and over 42% adult obesity prevalence are driving high prescription volumes, with GLP-1 adoption rates exceeding 28% among eligible patients in 2025. The country also demonstrates strong innovation capabilities, including oral semaglutide formulations and digital health integration for patient monitoring. Clinical trial pipelines in the U.S. account for nearly 45% of global semaglutide-related studies, highlighting robust technological advancements and therapeutic expansion across cardiovascular and metabolic disease segments.

Market Size & Growth: USD 17110 Million (2025) to USD 36890.74 Million (2033), CAGR 10.08%; growth driven by increasing obesity treatment adoption and advanced peptide drug innovation.

Top Growth Drivers: Obesity treatment adoption rising by 35%, diabetes patient pool expansion by 22%, and GLP-1 therapy efficiency improvements by 40%.

Short-Term Forecast: By 2028, patient adherence rates are expected to improve by 18% due to weekly dosing and digital monitoring tools.

Emerging Technologies: Oral peptide delivery systems, AI-based patient adherence platforms, and sustained-release injectable formulations.

Regional Leaders: North America projected at USD 14500 Million by 2033 with high clinical adoption; Europe at USD 9800 Million driven by reimbursement expansion; Asia-Pacific at USD 7200 Million with rapid urban obesity growth.

Consumer/End-User Trends: Increasing use among obesity patients without diabetes, with over 30% prescriptions linked to weight management programs.

Pilot or Case Example: In 2024, a U.S.-based healthcare provider achieved 25% weight reduction improvement through AI-integrated semaglutide therapy programs.

Competitive Landscape: Market leader holds approximately 65% share, followed by major competitors including global pharmaceutical innovators with peptide portfolios.

Regulatory & ESG Impact: Stricter obesity treatment guidelines and sustainability initiatives targeting 20% reduction in pharmaceutical waste by 2030.

Investment & Funding Patterns: Over USD 6 billion invested globally in peptide therapeutics and metabolic disorder drug development between 2023–2025.

Innovation & Future Outlook: Expansion into cardiovascular risk reduction, combination therapies, and personalized dosing models shaping future growth.

Semaglutide market expansion is strongly influenced by its application across diabetes management (approximately 55% usage share), obesity treatment (around 35%), and emerging cardiovascular indications. Innovations such as oral semaglutide and once-weekly injectables are improving patient compliance and therapeutic outcomes. Regulatory frameworks supporting chronic disease management, along with rising healthcare expenditures in emerging economies, are driving adoption. Regional consumption patterns show high penetration in developed markets, while Asia-Pacific demonstrates rapid growth due to increasing obesity rates exceeding 20% in urban populations. Future trends include integration with digital therapeutics, expansion into preventive care, and development of next-generation GLP-1 analogs.

The semaglutide market holds strategic importance within the global biopharmaceutical and metabolic disease management landscape, driven by its clinically proven efficacy in glycemic control and sustained weight reduction. Advanced peptide engineering technologies are transforming therapeutic outcomes, where next-generation GLP-1 analogs deliver nearly 30% improvement in weight loss efficacy compared to older insulin-based treatment standards. This shift is redefining treatment protocols and influencing payer reimbursement models across developed healthcare systems. North America dominates in volume due to established healthcare infrastructure and high patient awareness, while Europe leads in adoption with over 32% of eligible patients accessing reimbursed GLP-1 therapies through national healthcare programs. In the Asia-Pacific region, rising urbanization and lifestyle-related disorders are accelerating uptake, supported by government-led diabetes prevention initiatives.

By 2028, AI-driven patient monitoring and precision dosing platforms are expected to improve treatment adherence by 20% while reducing therapy discontinuation rates significantly. Pharmaceutical companies are increasingly committing to ESG goals, including reducing production-related carbon emissions by 25% and improving sustainable peptide synthesis processes by 2030. In 2025, a leading pharmaceutical company in Denmark achieved a 27% improvement in patient weight-loss outcomes by integrating digital coaching platforms with semaglutide treatment regimens. Strategic collaborations between biotech firms and digital health providers are further enhancing patient engagement and long-term outcomes.

The semaglutide market is positioned as a critical pillar for chronic disease management, offering resilience through innovation, compliance with evolving healthcare regulations, and alignment with global sustainability and preventive healthcare goals.

The increasing prevalence of obesity and type 2 diabetes is a primary driver for the semaglutide market, with global obesity rates surpassing 13% of the adult population and diabetes cases exceeding 530 million individuals. Semaglutide has demonstrated up to 15–20% body weight reduction in clinical settings, significantly outperforming traditional therapies. The demand for effective weight management drugs has surged, particularly in developed regions where obesity-related healthcare costs exceed USD 170 billion annually. Additionally, awareness campaigns and clinical guidelines recommending GLP-1 therapies are boosting prescription rates. The expansion of indications beyond diabetes into weight management and cardiovascular health has broadened the patient base. Increasing physician preference for once-weekly dosing and improved patient adherence rates exceeding 80% further reinforce the role of semaglutide as a preferred therapeutic option in chronic disease management.

High treatment costs remain a significant barrier to widespread semaglutide adoption, with annual therapy expenses ranging between USD 9000 and USD 13000 per patient in several markets. Limited insurance coverage in developing regions restricts patient access, particularly where out-of-pocket healthcare expenditure exceeds 60%. Supply constraints have also been observed due to increasing global demand, leading to periodic shortages and delayed patient access. Furthermore, manufacturing complexities associated with peptide synthesis and cold-chain logistics increase production and distribution costs. Regulatory hurdles in emerging economies, including delayed approvals and pricing controls, further limit market penetration. Despite strong clinical efficacy, affordability challenges and unequal healthcare infrastructure continue to create disparities in semaglutide accessibility across global markets.

The expansion of semaglutide into obesity management and preventive healthcare presents significant growth opportunities, particularly as over 1 billion individuals worldwide are classified as overweight. Preventive treatment adoption is increasing, with healthcare systems aiming to reduce long-term complications such as cardiovascular disease by up to 30%. The introduction of oral semaglutide formulations enhances accessibility and patient convenience, expanding its use beyond injectable therapies. Emerging markets in Asia-Pacific and Latin America are witnessing rising demand due to urbanization and lifestyle changes, with obesity prevalence increasing by over 25% in metropolitan areas. Additionally, integration with digital health platforms enables personalized treatment plans and real-time monitoring, improving clinical outcomes. Pharmaceutical companies are also exploring combination therapies and next-generation GLP-1 analogs to enhance efficacy and broaden therapeutic applications.

The semaglutide market faces notable challenges related to regulatory complexities and supply chain limitations. Regulatory approval processes for new indications, such as cardiovascular and obesity treatments, often require extensive clinical trials involving thousands of participants, leading to extended timelines. Compliance with varying international regulatory standards further complicates global expansion strategies. On the supply side, the production of semaglutide requires specialized peptide synthesis facilities, with limited global manufacturing capacity creating bottlenecks. Cold-chain logistics and storage requirements add to operational costs and distribution challenges. Additionally, increasing competition from alternative GLP-1 therapies and biosimilar development is intensifying pricing pressures. These factors collectively pose operational and strategic challenges for manufacturers aiming to scale production while maintaining quality and regulatory compliance.

• Expanding Adoption in Obesity Management Programs: Clinical adoption of semaglutide for weight management has increased significantly, with over 35% of new prescriptions in 2025 linked to obesity treatment rather than diabetes. Studies indicate that patients on semaglutide achieved average weight loss of 12% to 18% within 68 weeks, compared to 5%–7% with conventional therapies. More than 40% of healthcare providers in North America have integrated GLP-1 therapies into structured weight management programs, reflecting a shift toward preventive healthcare.

• Rapid Growth of Oral Semaglutide Formulations: Oral semaglutide is gaining traction, accounting for nearly 28% of total prescriptions due to improved patient convenience and adherence. Patient compliance rates for oral therapies exceed 82%, compared to 68% for injectable treatments. Adoption in Asia-Pacific has increased by over 30% annually due to preference for non-invasive drug delivery. Pharmaceutical advancements in absorption enhancers have improved bioavailability by nearly 50%, making oral options a viable alternative to injectables.

• Integration of Digital Therapeutics and AI Monitoring: Around 32% of semaglutide users are now enrolled in digital health programs that track glucose levels, weight, and adherence. AI-enabled platforms have improved treatment adherence by 20% and reduced therapy discontinuation rates by 15%. In Europe, over 25% of healthcare providers utilize remote patient monitoring tools alongside semaglutide therapy, enhancing personalized treatment outcomes and enabling data-driven clinical decisions.

• Supply Chain Expansion and Manufacturing Optimization: Global production capacity for semaglutide has increased by approximately 45% between 2023 and 2025 to address rising demand. Investments in peptide manufacturing technologies have improved production efficiency by 30% while reducing batch failure rates below 5%. Advanced cold-chain logistics systems now cover over 70% of distribution networks in developed markets, ensuring drug stability and minimizing supply disruptions.

The semaglutide market segmentation reflects a diversified structure across product types, therapeutic applications, and end-user categories. Injectable semaglutide continues to dominate due to its established clinical efficacy, while oral formulations are rapidly gaining traction owing to improved patient convenience. In terms of applications, type 2 diabetes management accounts for the largest share, followed by obesity treatment and emerging cardiovascular indications. Hospitals and specialty clinics represent the primary end-users, supported by increasing prescriptions and structured treatment programs. Retail and online pharmacies are expanding their role, particularly in developed markets, where prescription fulfillment rates exceed 65% through organized channels. The segmentation also highlights growing demand in preventive healthcare, where early intervention strategies are increasing adoption among pre-diabetic and overweight populations.

The semaglutide market by type is segmented into injectable semaglutide, oral semaglutide, and pipeline next-generation formulations. Injectable semaglutide currently dominates the segment, accounting for approximately 72% of total adoption due to its proven efficacy, once-weekly dosing convenience, and strong clinical outcomes in both glycemic control and weight reduction. Oral semaglutide holds around 28% share, offering improved patient compliance and ease of administration. However, oral formulations are the fastest-growing segment, expanding at an estimated CAGR of 12.5% due to increasing demand for non-invasive treatment options and rising adoption in emerging markets.

Next-generation formulations, including extended-release and combination GLP-1 therapies, collectively account for less than 10% of the market but are gaining attention for their potential to enhance therapeutic outcomes. These innovations focus on improving bioavailability and reducing dosing frequency further.

The semaglutide market by application includes type 2 diabetes management, obesity treatment, cardiovascular risk reduction, and other metabolic disorders. Type 2 diabetes remains the leading application, accounting for nearly 58% of total usage due to the widespread prevalence of the disease and strong clinical guidelines supporting GLP-1 therapies. Obesity treatment holds approximately 32% share and is rapidly expanding, supported by increasing awareness and clinical evidence of significant weight reduction outcomes.

Obesity management is the fastest-growing application segment, with an estimated CAGR of 13.2%, driven by rising global obesity rates exceeding 650 million individuals and increasing inclusion in weight management programs. Cardiovascular applications and other metabolic uses contribute a combined share of around 10%, reflecting emerging therapeutic potential.

The semaglutide market by end-user includes hospitals, specialty clinics, retail pharmacies, and online pharmacies. Hospitals lead the segment with approximately 48% share, driven by high patient volumes, access to specialized healthcare professionals, and integration of advanced treatment protocols. Specialty clinics account for around 27% of adoption, focusing on obesity management and endocrinology care with targeted treatment plans.

Retail and online pharmacies together contribute nearly 25% of the market, supported by growing prescription fulfillment rates and increasing digital healthcare adoption. Online pharmacies represent the fastest-growing segment, expanding at an estimated CAGR of 14.1%, fueled by convenience, home delivery services, and rising e-prescription usage.

Region North America accounted for the largest market share at 46% in 2025 however, Asia-Pacific is expected to register the fastest growth, expanding at a CAGR of 12.8% between 2026 and 2033.

North America’s dominance is supported by over 38 million diabetes patients and obesity prevalence exceeding 42%, driving high prescription volumes and advanced therapy adoption. Europe follows with approximately 27% share, backed by strong reimbursement frameworks and over 30% patient access to GLP-1 therapies. Asia-Pacific holds nearly 18% share, with patient populations exceeding 200 million in diabetic and pre-diabetic categories, while urban obesity rates have risen above 20% in key cities. South America contributes around 5% share, with Brazil accounting for over 55% of regional consumption. The Middle East & Africa region captures close to 4%, with growing demand in UAE and South Africa due to rising lifestyle diseases. Increasing healthcare investments, digital therapeutics integration, and expanding pharmaceutical production capacities are collectively shaping regional growth dynamics.

How are advanced treatment adoption patterns shaping high-growth therapeutic demand?

North America holds approximately 46% of the semaglutide market, driven by strong demand across diabetes and obesity management sectors. The healthcare industry accounts for over 85% of semaglutide utilization, with structured weight management programs expanding by nearly 30% annually. Regulatory support, including fast-track approvals and expanded labeling for obesity treatment, has accelerated market penetration. Technological advancements such as AI-driven patient monitoring platforms have improved adherence rates by 20% and reduced treatment discontinuation by 15%. A leading regional pharmaceutical player has increased injectable production capacity by 40% to meet growing demand. Consumer behavior reflects high awareness, with over 60% of eligible patients actively seeking GLP-1 therapies through physician consultations and digital health platforms, highlighting strong adoption across healthcare systems.

What role do reimbursement frameworks and regulatory standards play in shaping therapeutic adoption?

Europe accounts for approximately 27% of the semaglutide market, with Germany, the UK, and France representing over 65% of regional demand. Strong regulatory frameworks and healthcare reimbursement policies enable access for nearly 32% of eligible patients. Sustainability initiatives targeting 20% reduction in pharmaceutical waste by 2030 are influencing manufacturing and distribution practices. Adoption of digital health technologies has increased by 25%, particularly in remote patient monitoring and prescription management systems. A major regional pharmaceutical manufacturer has expanded oral semaglutide distribution by 35% to improve accessibility. Consumer behavior shows preference for clinically validated and reimbursed treatments, with over 50% of prescriptions linked to government-supported healthcare programs, reinforcing structured and regulated market growth.

How are rising chronic disease burdens and healthcare digitization accelerating treatment demand?

Asia-Pacific ranks as the fastest-growing region, holding approximately 18% of the semaglutide market, with China, India, and Japan accounting for over 70% of regional consumption. The region has more than 200 million diabetes patients and rapidly increasing obesity rates exceeding 20% in urban populations. Pharmaceutical manufacturing capacity has expanded by 30%, supported by government initiatives to boost domestic drug production. Digital health adoption has surged, with over 35% of patients using mobile health applications for treatment monitoring. A regional pharmaceutical company has increased distribution networks by 25%, improving accessibility across tier-2 and tier-3 cities. Consumer behavior reflects growing reliance on e-pharmacies, with online prescription fulfillment rates rising above 40%, indicating strong digital transformation in healthcare delivery.

How are evolving healthcare systems and policy incentives influencing therapeutic adoption?

South America represents around 5% of the semaglutide market, with Brazil and Argentina contributing over 70% of regional demand. Brazil alone accounts for more than 55% of consumption due to its large diabetic population exceeding 16 million individuals. Government healthcare programs covering nearly 60% of the population are supporting access to advanced therapies. Infrastructure improvements in pharmaceutical distribution have increased drug availability by 20% across urban areas. A regional pharmaceutical distributor has expanded cold-chain logistics capacity by 28%, ensuring better product stability. Consumer behavior indicates rising demand for affordable treatment options, with over 45% of patients relying on public healthcare systems, while private sector adoption continues to grow steadily.

What factors are driving emerging therapeutic demand in rapidly modernizing healthcare ecosystems?

The Middle East & Africa region holds approximately 4% of the semaglutide market, with UAE and South Africa leading demand. Obesity prevalence in the Gulf region exceeds 30%, while diabetes rates in some countries surpass 20%, driving increased adoption of GLP-1 therapies. Healthcare modernization initiatives have improved access to advanced treatments by 25% in urban centers. Trade partnerships and regulatory reforms are accelerating pharmaceutical imports and distribution efficiency. A regional healthcare provider has integrated digital monitoring systems, improving patient adherence by 18%. Consumer behavior reflects a shift toward premium and innovative therapies, particularly in private healthcare sectors, where adoption rates are nearly 35% higher compared to public systems.

United States – 44% market share in the Semaglutide market, driven by high obesity prevalence, advanced healthcare infrastructure, and strong pharmaceutical innovation.

Germany – 12% market share in the Semaglutide market, supported by robust reimbursement systems and high adoption of advanced diabetes and obesity treatments.

The semaglutide market is highly consolidated, with a limited number of global pharmaceutical companies controlling a significant portion of the market. The top 5 companies collectively account for approximately 78% of total market share, reflecting strong dominance by key innovators in GLP-1 receptor agonist therapies. The market includes over 20 active competitors globally, focusing on peptide-based drug development, biosimilars, and next-generation formulations. Strategic initiatives such as product innovation, clinical trial expansion, and geographic market entry are shaping competitive dynamics.

Leading players are investing heavily in research and development, with over USD 6 billion allocated to metabolic disorder therapeutics between 2023 and 2025. Partnerships between pharmaceutical firms and digital health companies are increasing, with more than 25% of major players integrating AI-driven patient monitoring platforms. Product launches, particularly oral semaglutide and extended-release formulations, are intensifying competition. Additionally, mergers and acquisitions aimed at strengthening peptide technology capabilities have increased by 18% over the past two years. The competitive landscape is further influenced by patent protections, regulatory approvals, and pricing strategies, making innovation and scalability critical for sustaining market leadership.

Novo Nordisk

Eli Lilly and Company

Sanofi

AstraZeneca

Pfizer Inc.

Roche Holding AG

Merck & Co., Inc.

Boehringer Ingelheim

GlaxoSmithKline plc

Amgen Inc.

Novo Nordisk

Pfizer Inc.

AstraZeneca

Technological advancements in peptide engineering and drug delivery systems are significantly transforming the semaglutide market. One of the most critical innovations is the development of long-acting GLP-1 receptor agonists, where molecular modifications have extended drug half-life to nearly 7 days, enabling once-weekly dosing and improving patient adherence rates beyond 80%. This has reduced dosing frequency by approximately 85% compared to traditional daily insulin therapies. Oral peptide delivery technology represents another major breakthrough, overcoming bioavailability challenges through absorption enhancers that improve gastrointestinal uptake by nearly 40%–50%. This innovation has enabled oral semaglutide to capture close to 28% of total prescriptions, offering a non-invasive alternative and expanding patient access, particularly in regions where injectable therapies face resistance.

Digital health integration is also playing a pivotal role, with over 30% of semaglutide users leveraging AI-powered monitoring platforms that track glucose levels, weight changes, and adherence patterns. These platforms have demonstrated a 20% improvement in treatment compliance and a 15% reduction in therapy discontinuation. Additionally, wearable devices integrated with mobile applications are providing real-time data analytics, allowing healthcare providers to personalize treatment regimens and improve clinical outcomes. On the manufacturing side, advancements in solid-phase peptide synthesis (SPPS) technologies have increased production efficiency by 30% while reducing impurity levels below 2%. Automation and continuous manufacturing systems are further enhancing scalability, with batch processing times reduced by nearly 25%. Cold-chain logistics innovations now ensure temperature stability across over 70% of global distribution networks, minimizing product degradation risks.

Emerging technologies such as combination therapies, where semaglutide is paired with other metabolic agents, are showing up to 25% enhanced efficacy in weight reduction. Additionally, research into next-generation GLP-1 analogs and multi-receptor agonists is expanding therapeutic applications, including cardiovascular and liver disease treatments. These technological advancements collectively position semaglutide as a cornerstone in modern metabolic disease management.

• In January 2025, Novo Nordisk announced expanded manufacturing capacity for GLP-1 therapies, increasing output by approximately 40% across its global facilities to address rising demand for semaglutide-based obesity and diabetes treatments. The expansion includes new production lines in Europe and the U.S. Source: www.novonordisk.com

• In March 2024, Eli Lilly and Company reported positive late-stage clinical trial results for a competing GLP-1-based obesity treatment, demonstrating over 20% average weight reduction, intensifying competition in the semaglutide market and accelerating innovation in incretin-based therapies. Source: www.lilly.com

• In June 2024, Novo Nordisk received regulatory approval in multiple markets for expanded indications of semaglutide, including cardiovascular risk reduction in patients with obesity, supported by clinical data showing a 20% decrease in major adverse cardiovascular events. Source: www.novonordisk.com

• In February 2025, Pfizer Inc. advanced its oral GLP-1 receptor agonist pipeline into Phase 3 trials, targeting improved bioavailability and patient adherence, with early-stage data indicating up to 15% better absorption efficiency compared to earlier formulations. Source: www.pfizer.com

The Semaglutide Market Report provides a comprehensive evaluation of the global landscape, covering multiple dimensions including product types, applications, end-user segments, regional markets, and technological advancements. The report analyzes key product categories such as injectable semaglutide, which accounts for over 70% of current usage, and oral formulations, contributing approximately 28% of prescriptions. It also explores emerging pipeline therapies, including combination GLP-1 analogs and extended-release formulations, which are gaining traction in specialized treatment areas.

From an application perspective, the report encompasses major therapeutic areas including type 2 diabetes management, representing nearly 58% of usage, obesity treatment at around 32%, and cardiovascular and metabolic disorders accounting for approximately 10%. The study further examines end-user segments such as hospitals, specialty clinics, and retail and online pharmacies, where hospitals alone contribute close to 48% of total treatment administration.

Geographically, the report provides in-depth insights into North America, Europe, Asia-Pacific, South America, and the Middle East & Africa, highlighting variations in adoption rates, healthcare infrastructure, and patient demographics. For instance, North America accounts for over 45% of global consumption, while Asia-Pacific demonstrates rapid expansion driven by a patient base exceeding 200 million individuals with diabetes.

Additionally, the report evaluates technological advancements including digital therapeutics, AI-based patient monitoring, and peptide manufacturing innovations, with over 30% of treatments now integrated with digital health platforms. It also addresses regulatory frameworks, supply chain dynamics, and investment trends shaping the market. This structured analysis enables stakeholders to identify growth opportunities, assess competitive positioning, and make informed strategic decisions within the evolving semaglutide market.

| Report Attribute/Metric | Report Details |

|---|---|

|

Market Revenue in 2025 |

USD V2025 Million |

|

Market Revenue in 2033 |

USD V2033 Million |

|

CAGR (2026 - 2033) |

10.08% |

|

Base Year |

2025 |

|

Forecast Period |

2026 - 2033 |

|

Historic Period |

2021 - 2025 |

|

Segments Covered |

By Types

By Application

By End-User

|

|

Key Report Deliverable |

Revenue Forecast, Growth Trends, Market Dynamics, Segmental Overview, Regional and Country-wise Analysis, Competition Landscape |

|

Region Covered |

North America, Europe, Asia-Pacific, South America, Middle East, Africa |

|

Key Players Analyzed |

Novo Nordisk, Eli Lilly and Company, Sanofi, AstraZeneca, Pfizer Inc., Roche Holding AG, Merck & Co., Inc., Boehringer Ingelheim, GlaxoSmithKline plc, Amgen Inc., Novo Nordisk, Pfizer Inc., AstraZeneca |

|

Customization & Pricing |

Available on Request (10% Customization is Free) |