Reports

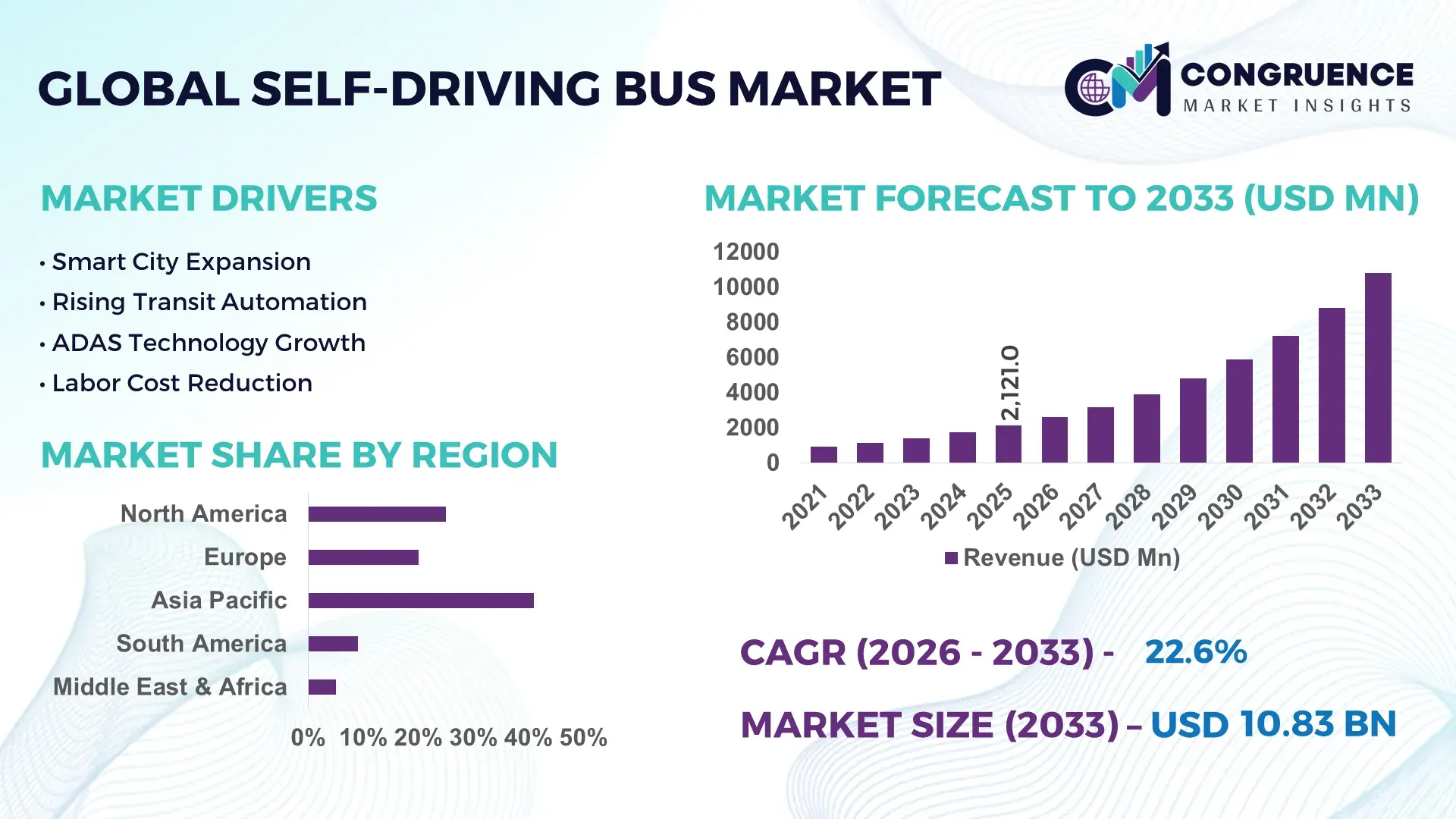

The Global Self-Driving Bus Market was valued at USD 2120.98 Million in 2025 and is anticipated to reach a value of USD 10825.8 Million by 2033 expanding at a CAGR of 22.6% between 2026 and 2033. Rapid deployment of AI-based fleet navigation, smart city transit corridors, and labor-cost optimization programs is accelerating procurement of autonomous electric buses across urban mobility networks, particularly in high-density metropolitan regions facing driver shortages and emission mandates.

China dominates the global self-driving bus market with nearly 38% of large-scale autonomous transit pilot capacity, supported by over USD 4.5 billion in intelligent transport infrastructure investments and nationwide V2X deployment across key urban clusters in 2026. The United States maintains stronger software integration capabilities, while China leads in fleet-scale commercialization with autonomous shuttle utilization rates exceeding 72% in controlled urban zones. Europe continues expanding regulatory-backed autonomous public transport corridors following energy security reforms linked to post-Russia-Ukraine supply chain restructuring.

Transit operators and mobility technology providers are prioritizing scalable autonomous fleet ecosystems, making early infrastructure alignment and AI transit integration critical for long-term competitive positioning.

Market Size & Growth: USD 2120.98 million in 2025 to USD 10825.8 million by 2033, driven by AI fleet automation, smart transit infrastructure, and electric mobility integration at 22.6% growth.

Top Growth Drivers: Driver shortage impact rose 31%, urban electrification projects expanded 28%, and intelligent transport investments increased 35% globally in 2026.

Short-Term Forecast: By 2028, autonomous bus operators are projected to reduce fleet operating costs by 24% while improving route efficiency by 29%.

Emerging Technologies: Advanced LiDAR, edge AI, and V2X communication systems improved obstacle detection accuracy by 41% and reduced latency by 33%.

Regional Leaders: Asia-Pacific surpasses USD 4.1 billion with smart corridor expansion, North America exceeds USD 2.8 billion through AI software integration, and Europe crosses USD 2.2 billion via regulatory-backed zero-emission transit deployment.

Consumer/End-User Trends: Nearly 46% of urban transit agencies prioritize autonomous shuttle procurement to address labor shortages and improve last-mile connectivity.

Pilot/Case Example: In 2026, autonomous electric bus pilots in major Chinese smart cities reduced human intervention incidents by 37% and improved fleet uptime by 26%.

Competitive Landscape: Leading autonomous mobility firms control approximately 44% combined market share, with competition intensifying among electric bus manufacturers, AI software providers, and sensor integration specialists.

Regulatory & ESG Impact: Zero-emission transit mandates lowered projected fleet emissions by 32%, while autonomous routing systems reduced idle energy consumption by 18%.

Investment & Funding: Global autonomous transit investments exceeded USD 6.3 billion in 2026, led by public-private partnerships and smart infrastructure expansion initiatives.

Innovation & Future Outlook: Level-4 autonomous fleet platforms, digital twin transit management, and predictive maintenance systems are reshaping high-growth urban mobility ecosystems worldwide.

The Self-Driving Bus Market is expanding rapidly across urban public transportation, airport mobility, university campuses, and industrial smart zones where autonomous fleet efficiency delivers measurable operational savings. Advanced sensor fusion systems and AI-based predictive routing improved route optimization performance by nearly 34% in 2026, while semiconductor localization initiatives reduced deployment bottlenecks in Asia-Pacific manufacturing hubs. Increasing integration of autonomous electric shuttle ecosystems is strengthening long-term strategic transit modernization and infrastructure planning discussions.

The self-driving bus market is becoming strategically important as transit operators, smart city planners, and automotive technology firms compete to modernize urban mobility infrastructure while reducing labor dependency and fleet inefficiencies. Regulatory acceleration for autonomous transport testing in China, the United States, and Germany is reshaping procurement priorities, while semiconductor localization and battery supply-chain restructuring after global logistics disruptions are improving deployment stability. Public transit authorities are increasingly integrating autonomous electric shuttles into airport corridors, industrial parks, and university networks where operational consistency and route predictability generate measurable utilization gains.

AI-enabled autonomous buses equipped with edge computing and V2X communication systems are delivering nearly 27% lower operating costs compared to legacy diesel transit fleets through optimized routing, predictive maintenance, and reduced idle time. China leads in scaled autonomous transit deployment with multi-city smart corridor integration, while Germany focuses on precision safety validation and interoperable public transport systems. Over the next two years, controlled-route autonomous shuttle deployments are projected to expand by more than 30% across dedicated urban mobility zones.

In 2026, several mobility operators expanded partnerships with telecom providers and sensor manufacturers to improve low-latency fleet communication and real-time navigation reliability. Companies are prioritizing modular autonomous platforms, localized software integration, and battery ecosystem partnerships to strengthen deployment economics. Competitive advantage increasingly depends on scalable fleet orchestration, regulatory adaptability, and infrastructure-aligned autonomous transit ecosystems.

Government-backed intelligent transportation programs and urban electrification policies are accelerating autonomous bus adoption across high-density transit corridors. China increased connected road infrastructure deployment by 34% in 2026, while autonomous shuttle pilot approvals in the United States expanded nearly 29% across municipal mobility projects. Rising labor shortages in public transportation operations pushed transit agencies toward AI-driven fleet automation capable of reducing route management costs by approximately 22%. In response, automotive OEMs and mobility software providers are expanding strategic partnerships with telecom firms and mapping technology companies to strengthen V2X communication capabilities. A notable operational shift is the integration of autonomous buses into airport logistics and industrial campus transit systems, where predictable route structures improve fleet utilization and reduce idle energy consumption. Companies prioritizing closed-loop mobility ecosystems are gaining faster regulatory clearance and stronger infrastructure alignment advantages.

Large-scale deployment remains constrained by expensive smart road infrastructure, sensor calibration requirements, and inconsistent regulatory interoperability standards. Advanced LiDAR and onboard computing systems still account for nearly 26% of total autonomous bus production costs, while charging infrastructure gaps delay fleet electrification projects in several urban transport hubs. In India and parts of Southeast Asia, fewer than 18% of city transit corridors currently support reliable V2X communication compatibility required for Level-4 autonomous operations. Semiconductor supply concentration in East Asia continues creating component procurement volatility, increasing deployment lead times for fleet operators. To reduce operational exposure, companies are diversifying sensor sourcing strategies, localizing software integration, and shifting toward modular vehicle architectures that simplify maintenance and reduce retrofit costs. Firms with vertically integrated AI and battery ecosystems maintain stronger deployment resilience and procurement flexibility.

Fleet-as-a-Service deployment models are creating new monetization pathways for autonomous transit providers by lowering upfront ownership costs for municipalities and private operators. Shared autonomous mobility programs improved fleet utilization efficiency by nearly 31% in controlled urban zones during 2026, while predictive maintenance platforms reduced unplanned downtime by approximately 24%. Japan and Singapore are accelerating smart mobility corridor investments tied to aging population transport requirements and low-emission urban transit mandates. Companies are increasingly integrating digital twin simulation platforms and AI traffic orchestration systems to optimize route density and passenger throughput before physical deployment. A non-obvious opportunity is emerging within industrial parks, ports, and healthcare campuses where autonomous shuttle demand remains underserved despite high operational predictability. Mobility firms are expanding through telecom alliances, charging infrastructure partnerships, and software subscription ecosystems that create recurring operational revenue streams.

Scaling autonomous bus operations across multiple cities remains difficult due to fragmented traffic systems, inconsistent digital infrastructure, and evolving cybersecurity requirements. Real-time data processing loads increased more than 38% as fleet operators integrated higher-resolution sensor arrays and AI navigation platforms into dense urban environments. Cybersecurity risks linked to connected vehicle communication systems are intensifying, particularly in North American and European smart transit networks where public infrastructure digitization expanded rapidly after 2025. Workforce shortages in AI fleet maintenance, autonomous systems diagnostics, and safety validation engineering are also slowing deployment consistency. Companies must invest heavily in cloud-edge orchestration, simulation-based safety testing, and standardized interoperability frameworks to maintain operational reliability at scale. The strongest long-term market position will belong to operators capable of combining infrastructure partnerships, cyber resilience, and adaptive fleet intelligence within unified mobility ecosystems.

Dedicated Smart Route Expansion Autonomous bus deployment on pre-mapped urban corridors increased by nearly 33% during 2026 as municipalities prioritized controlled-route operations to reduce traffic unpredictability and safety validation costs. China and Singapore accelerated lane-digitization projects following stricter intelligent transport regulations, while transit operators improved fleet punctuality by approximately 21% through AI traffic coordination systems. Companies are scaling partnerships with telecom providers and HD mapping firms to strengthen real-time route optimization and low-latency navigation infrastructure.

Battery Swapping Integration Growth Autonomous electric bus operators are increasingly adopting battery swapping platforms to reduce charging downtime and improve fleet utilization across high-frequency transit networks. Swapping-enabled fleets reduced idle charging time by nearly 40% and improved operational availability by 27% in dense urban transit hubs. Bus manufacturers in South Korea and China are restructuring supply partnerships around modular battery ecosystems, allowing operators to stabilize energy management costs amid lithium procurement volatility and rising electricity demand pressures.

Autonomous Campus Transit Scaling University campuses, industrial parks, and healthcare facilities emerged as high-efficiency deployment zones due to predictable route environments and lower infrastructure complexity. Controlled-campus autonomous shuttle deployments expanded more than 29% in 2026, while onboard remote monitoring reduced manual intervention rates by 35%. Mobility providers are targeting these semi-closed environments to accelerate commercialization timelines, validate AI navigation systems faster, and establish recurring service contracts before wider municipal deployment approvals.

Fleet Intelligence Platform Adoption Transit operators are shifting from standalone autonomous vehicles toward centralized fleet orchestration platforms integrating predictive maintenance, cybersecurity monitoring, and passenger analytics. AI-driven maintenance scheduling lowered unexpected vehicle downtime by approximately 24%, while cloud-edge fleet coordination improved route response speed by 18%. Following increased cyber-risk scrutiny in connected mobility systems, companies in Germany and the United States expanded software alliances and digital twin simulation capabilities to strengthen operational resilience and regulatory compliance.

Electric Buses dominate the self-driving bus market due to lower operating costs, easier software integration, and compatibility with zero-emission urban mobility policies. In 2026, electric autonomous buses accounted for nearly 46% of total pilot deployments across China, Germany, and the United States, supported by expanding fast-charging infrastructure and AI-enabled energy management systems. Operators reported up to 28% lower maintenance costs compared to diesel-based autonomous transit fleets. Autonomous Transit Buses continue gaining strategic importance for municipal smart corridor projects where large passenger capacity and centralized fleet control improve urban mobility efficiency. Companies are prioritizing battery optimization, modular autonomous driving stacks, and scalable vehicle architectures to accelerate procurement and regulatory approvals.

Shuttle Buses represent the fastest-growing segment as airports, industrial campuses, and healthcare facilities increasingly deploy compact autonomous fleets within controlled environments. Shuttle-based deployments improved route utilization by approximately 31% during 2026 due to predictable operating conditions and lower infrastructure complexity. Hybrid Buses maintain relevance in regions with incomplete charging infrastructure, while Mini Buses are expanding within low-density urban transport and tourism circuits. Manufacturers are strengthening partnerships with battery suppliers, AI software firms, and telecom operators to diversify deployment flexibility and reduce operational integration risks.

Public Transportation remains the leading application segment due to large-scale fleet requirements, rising labor shortages, and increasing government investment in smart urban mobility infrastructure. Autonomous public transit corridors improved average route efficiency by approximately 26% during 2026, while AI-assisted fleet scheduling reduced idle time by nearly 19% in high-density metropolitan networks. Transit agencies in China and Germany accelerated autonomous bus integration to support low-emission mobility mandates and optimize operational continuity. Smart City Transport is emerging as a strategically important segment as municipalities integrate connected traffic systems, V2X communication, and predictive fleet coordination platforms into long-term urban modernization programs.

Campus Mobility is the fastest-growing application area because universities, healthcare campuses, and industrial parks provide lower-risk deployment environments with predictable traffic patterns. Controlled-campus shuttle systems reduced internal transit waiting times by nearly 34% and improved operational consistency through centralized monitoring platforms. Airport Transportation continues expanding through automated passenger transfer systems designed to optimize terminal connectivity and reduce labor-intensive operations. Tourism Services are increasingly adopting autonomous mini-bus fleets in structured sightseeing circuits where route predictability supports safer deployment. Mobility providers are scaling cloud-based fleet management, sensor analytics, and infrastructure partnerships to strengthen operational performance and deployment scalability.

Public Transport Authorities remain the dominant end-user group due to extensive fleet ownership, infrastructure control, and direct involvement in urban mobility modernization programs. In 2026, municipal transit agencies represented nearly 48% of active autonomous bus procurement programs globally, driven by labor shortages, emission reduction mandates, and increasing smart corridor investments. Large-scale operators improved route optimization efficiency by approximately 23% using AI-integrated traffic orchestration platforms. Smart City Projects are becoming increasingly influential as governments integrate autonomous mobility into broader digital infrastructure frameworks combining intelligent traffic management, connected roads, and predictive transit analytics.

Fleet Management Companies represent the fastest-growing end-user segment as outsourced mobility operations gain traction across airports, campuses, and industrial transport networks. Managed autonomous fleets reduced operational downtime by nearly 27% through predictive diagnostics and centralized vehicle monitoring systems. Airport Operators continue investing in autonomous transit to streamline terminal connectivity and improve passenger flow efficiency, while Educational Campuses increasingly deploy autonomous shuttle networks to address internal mobility demand. Tourism Operators are adopting smaller autonomous fleets for structured destination transport services. Companies are responding through subscription-based fleet models, customized software ecosystems, and telecom integration partnerships designed to improve deployment flexibility and long-term operational scalability.

Asia-Pacific accounted for the largest market share at 41% in 2025 however, Middle East & Africa is expected to register the fastest growth, expanding at a CAGR of 24.1% between 2026 and 2033.

AI-Integrated Urban Transit Deployment

North America maintains a strong position in autonomous public transit through advanced AI software integration, smart mobility infrastructure, and high-value pilot deployments across urban corridors. The region represented nearly 26% of global autonomous bus deployments in 2025, supported by municipal automation funding and expanding connected road infrastructure. Transit agencies increasingly prioritize autonomous electric shuttle integration to reduce driver shortages and improve route efficiency in controlled mobility zones. In 2026, several large-scale airport and university transit projects improved fleet utilization by approximately 22% using predictive route orchestration systems. Companies are strengthening partnerships with telecom operators, mapping providers, and cybersecurity firms to support scalable fleet coordination and regulatory compliance across multiple states.

United States Market Outlook: The United States leads regional deployment activity through strong enterprise participation, advanced autonomous driving software ecosystems, and expanding smart transit corridor projects. Urban mobility operators accelerated pilot commercialization across airport transit, university campuses, and municipal shuttle networks during 2026. More than 35 cities expanded connected infrastructure testing programs supporting Level-4 autonomous vehicle operations. Domestic technology firms are prioritizing AI validation platforms, cloud-edge fleet intelligence, and strategic sensor partnerships to strengthen deployment scalability and improve operational resilience.

Sustainability-Driven Autonomous Transit Modernization

Europe is advancing autonomous bus adoption through aggressive zero-emission mobility targets, integrated public transport modernization programs, and harmonized autonomous vehicle testing frameworks. The region contributed approximately 24% of global smart transit infrastructure deployments in 2025, with Germany, France, and the Nordic countries leading intelligent mobility integration. Autonomous electric buses operating within regulated urban corridors reduced operational energy consumption by nearly 18% during 2026. Transit operators are investing heavily in interoperable mobility systems, AI-assisted route optimization, and digital traffic coordination platforms to strengthen network efficiency. Public-private mobility partnerships are accelerating autonomous fleet deployment within smart city modernization initiatives across key metropolitan transport corridors.

Germany Market Outlook: Germany remains the region’s strongest autonomous mobility hub due to advanced automotive engineering capabilities, intelligent infrastructure investment, and supportive regulatory testing frameworks. Autonomous shuttle deployments expanded significantly across industrial parks and urban transit pilot corridors in 2026, while connected traffic infrastructure projects increased by approximately 27%. German mobility companies are strengthening collaborations with semiconductor suppliers, telecom firms, and AI software developers to improve autonomous fleet safety validation and long-term transit interoperability.

Large-Scale Smart Mobility Commercialization

Asia-Pacific leads the global self-driving bus market through extensive smart city investments, strong electric vehicle manufacturing capacity, and rapid deployment of connected transportation infrastructure. The region accounted for nearly 41% of global autonomous transit activity in 2025, supported by large-scale urban mobility modernization programs across China, Japan, and South Korea. Autonomous shuttle fleet deployment density increased by approximately 36% during 2026 as municipalities accelerated dedicated smart corridor expansion. Regional manufacturers are integrating AI navigation systems, V2X communication platforms, and modular battery technologies to improve operational efficiency and deployment scalability. Strong semiconductor supply chain integration and localized production capabilities continue strengthening the region’s autonomous transit competitiveness.

China Market Outlook: China dominates the regional market through aggressive intelligent transport infrastructure investment, large-scale autonomous pilot commercialization, and strong domestic EV manufacturing ecosystems. Multiple Tier-1 cities expanded autonomous public transit testing zones during 2026, while connected road infrastructure coverage increased significantly across smart urban districts. Chinese mobility firms are accelerating vertical integration strategies combining battery production, AI software development, and autonomous fleet management systems to strengthen deployment speed and reduce operational dependency on imported technology components.

Urban Mobility Digitization Expansion

South America is gradually advancing autonomous bus deployment through smart mobility modernization projects concentrated within large metropolitan transport systems. Brazil and Chile are leading regional adoption due to expanding electric mobility programs and increasing investment in connected public transportation infrastructure. The region represented approximately 6% of emerging autonomous transit pilot activity in 2025, with controlled-environment shuttle deployments expanding by nearly 19% during 2026. Transit operators are prioritizing autonomous electric mini-buses for airport connectivity and structured urban transit routes where infrastructure limitations remain manageable. Companies are responding through localized fleet partnerships, charging infrastructure collaboration, and modular deployment strategies designed to reduce implementation costs and operational complexity.

Brazil Market Outlook: Brazil remains the region’s most strategically significant market because of its large urban transit demand, growing EV ecosystem, and expanding smart mobility pilot projects. Major metropolitan transport authorities increased autonomous shuttle testing initiatives during 2026 to improve traffic efficiency and reduce fuel dependency within high-density urban corridors. Brazilian mobility operators are partnering with telecom providers and charging infrastructure developers to strengthen fleet connectivity, while public transit modernization programs continue supporting intelligent transportation deployment priorities.

Smart Infrastructure Investment Acceleration

Middle East & Africa is emerging as the fastest-growing self-driving bus market due to large-scale smart city investment programs, advanced transport modernization initiatives, and government-backed digital infrastructure expansion. Gulf countries are rapidly integrating autonomous mobility solutions into airport transit, tourism infrastructure, and urban smart corridor development projects. In 2026, autonomous shuttle deployment activity across major Gulf smart city projects increased by approximately 32%, supported by intelligent traffic management system investments and connected mobility frameworks. Regional operators are prioritizing autonomous electric transit fleets to improve sustainability targets and reduce operational inefficiencies. Technology providers are strengthening partnerships with infrastructure developers and telecom operators to accelerate deployment scalability within controlled urban environments.

United Arab Emirates Market Outlook: The United Arab Emirates leads regional autonomous mobility deployment through aggressive smart city investment, advanced digital infrastructure integration, and strong regulatory support for intelligent transport systems. Dubai and Abu Dhabi expanded autonomous public transport pilot programs during 2026, while connected mobility infrastructure investment continued rising across urban modernization projects. UAE-based operators are focusing on AI-enabled fleet coordination, autonomous tourism transport, and integrated smart corridor deployment strategies to position the country as a global intelligent mobility innovation hub.

The self-driving bus market is dominated by competition between global electric bus manufacturers, autonomous driving software firms, and intelligent mobility platform providers including EasyMile, Navya, Karsan, WeRide, Baidu Apollo, and Local Motors. The top five players collectively control nearly 52% of active commercial autonomous shuttle deployments through integrated hardware-software ecosystems and long-term municipal partnerships. Competition is centered on AI navigation accuracy, fleet scalability, battery efficiency, and deployment speed, with advanced route orchestration systems improving operational efficiency by approximately 24% and predictive maintenance reducing downtime by nearly 21%. Chinese mobility firms are competing aggressively on deployment scale and infrastructure integration, while European companies emphasize safety validation and interoperable public transit systems. Companies are expanding through telecom alliances, battery ecosystem integration, and autonomous fleet management partnerships. Rising cybersecurity compliance requirements and high smart infrastructure costs remain major entry barriers. Winning depends on scalable fleet intelligence, regulatory adaptability, and vertically integrated autonomous mobility ecosystems.

EasyMile

Navya

Karsan

WeRide

Baidu Apollo

AB Volvo

Scania

Yutong Bus

Proterra

NFI Group

Hyundai Motor Company

Toyota Motor Corporation

Blue Bird Corporation

Zhengzhou Yutong Group Co., Ltd.

AI-driven perception systems, LiDAR fusion, and V2X communication platforms currently define core self-driving bus operations across smart transit corridors. In 2026, nearly 48% of autonomous shuttle deployments integrated multi-sensor fusion architectures that improved obstacle recognition accuracy by approximately 32% compared to camera-only legacy systems. Edge AI processors reduced route response latency by 27%, enabling smoother navigation within high-density urban environments. Transit operators benefit from lower manual intervention rates and improved fleet utilization, while technology providers gain competitive advantage through scalable fleet orchestration platforms and predictive maintenance integration.

Emerging technologies between 2026 and 2028 include digital twin transit simulation, battery-swapping infrastructure, and cloud-edge autonomous fleet coordination. Digital twin route validation shortened deployment testing cycles by nearly 24%, while battery-swapping platforms improved operational uptime by approximately 35% versus conventional charging-based electric fleets. Adoption is accelerating within airports, industrial campuses, and smart city transport systems where controlled-route predictability improves commercialization speed. Companies are expanding telecom partnerships and AI software alliances to strengthen real-time fleet synchronization and cybersecurity resilience.

Disruptive development is shifting toward Level-4 autonomous transit ecosystems integrating generative AI route analytics and centralized mobility intelligence platforms. Advanced autonomous buses now deliver nearly 29% lower operating costs than conventional diesel fleets through optimized energy management and predictive diagnostics. Companies investing early in interoperable software, semiconductor localization, and intelligent infrastructure partnerships are expected to secure stronger deployment scalability and regulatory positioning through 2028.

March 2026 – WeRide expanded its strategic collaboration with NVIDIA and Grab to accelerate Southeast Asian autonomous mobility deployment using the NVIDIA DRIVE Hyperion platform, supporting a roadmap exceeding 2,600 active Robotaxis globally by 2026 and strengthening large-scale fleet commercialization capabilities. Source: ir.weride.ai

March 2026 – Karsan announced driverless autonomous public transportation operations beginning in 2026 while targeting expansion across Northern Europe. Electric vehicles accounted for 67% of company turnover in 2025, reinforcing its competitive positioning in advanced electric autonomous transit manufacturing. Source: karsan.com

November 2024 – Baidu Apollo received Hong Kong approval for autonomous vehicle testing involving 10 self-driving vehicles under the city’s new regulatory framework, marking its first autonomous deployment authorization outside mainland China and strengthening international expansion readiness. Source: reuters.com

April 2026 – WeRide and Lenovo announced plans to jointly deploy 200,000 autonomous vehicles globally over five years, one of the sector’s largest commercialization initiatives, significantly expanding production scalability, AI computing integration, and enterprise-level autonomous mobility deployment capacity. Source: ir.weride.ai

The Self-Driving Bus Market report delivers comprehensive analysis across autonomous transit technologies, deployment models, operational infrastructure, and competitive mobility ecosystems between 2026 and 2033. The study covers key vehicle categories including Electric Buses, Hybrid Buses, Shuttle Buses, Mini Buses, and Autonomous Transit Buses, alongside application analysis spanning Public Transportation, Airport Transportation, Campus Mobility, Smart City Transport, and Tourism Services. More than 45% of assessed deployments are concentrated within controlled-route urban and campus transit systems where AI-based fleet coordination and connected mobility infrastructure accelerate commercialization.

The report evaluates strategic adoption trends across North America, Europe, Asia-Pacific, South America, and Middle East & Africa, highlighting deployment concentration, infrastructure readiness, and enterprise expansion strategies. It includes assessment of AI navigation systems, V2X communication, digital twin simulation, predictive maintenance platforms, and cybersecurity integration. The analysis supports investment planning, smart mobility partnerships, competitive benchmarking, infrastructure modernization decisions, and long-term autonomous transit positioning across municipal, industrial, and commercial mobility ecosystems.

| Report Attribute/Metric | Report Details |

|---|---|

|

Market Revenue in 2025 |

USD 2120.98 Million |

|

Market Revenue in 2033 |

USD 10825.8 Million |

|

CAGR (2026 - 2033) |

22.6% |

|

Base Year |

2025 |

|

Forecast Period |

2026 - 2033 |

|

Historic Period |

2021 - 2025 |

|

Segments Covered |

By Type

By Application

By End-User

|

|

Key Report Deliverable |

Revenue Forecast, Growth Trends, Market Dynamics, Segmental Overview, Regional and Country-wise Analysis, Competition Landscape |

|

Region Covered |

North America, Europe, Asia-Pacific, South America, Middle East, Africa |

|

Key Players Analyzed |

EasyMile, Navya, Karsan, WeRide, Baidu Apollo, AB Volvo, Scania, Yutong Bus, Proterra, NFI Group, Hyundai Motor Company, Toyota Motor Corporation, Blue Bird Corporation, Zhengzhou Yutong Group Co., Ltd. |

|

Customization & Pricing |

Available on Request (10% Customization is Free) |