Reports

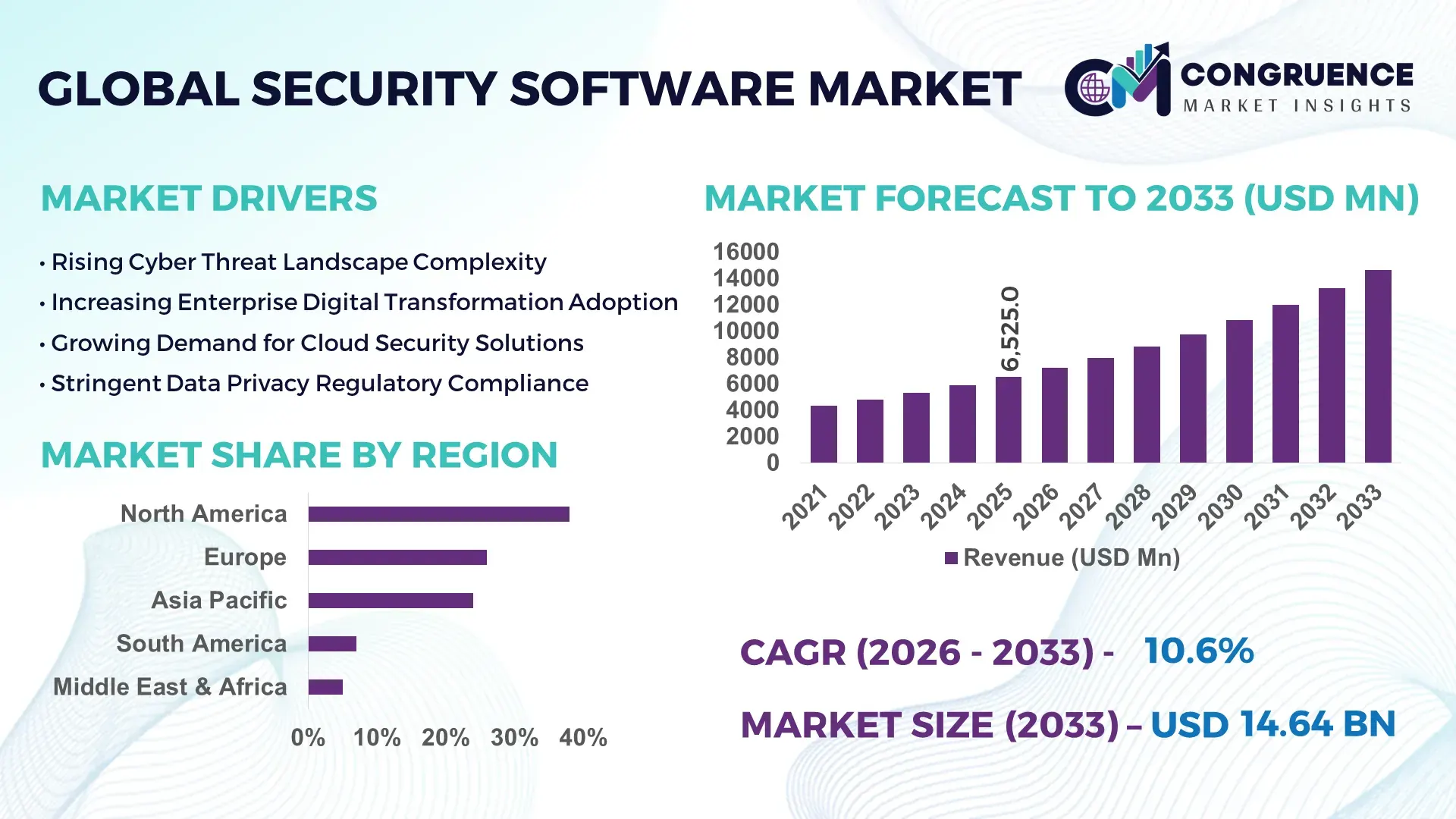

The Global Security Software Market was valued at USD 6,525.0 Million in 2025 and is anticipated to reach a value of USD 14,640.8 Million by 2033 expanding at a CAGR of 10.63% between 2026 and 2033, according to an analysis by Congruence Market Insights. This growth is primarily driven by the increasing frequency of cyberattacks and the rising need for advanced data protection across enterprises.

The United States dominates the global Security Software Market with strong enterprise adoption, high cybersecurity spending, and advanced infrastructure. In 2025, over 68% of large enterprises in the U.S. deployed integrated security platforms, while cybersecurity investments exceeded USD 90 billion annually. The country leads in cloud security implementation, with nearly 72% of organizations utilizing multi-layered protection frameworks. Additionally, over 60% of financial institutions and 55% of healthcare providers in the U.S. actively deploy AI-based threat detection systems, reflecting robust technological integration and high demand across critical industries.

Market Size & Growth: USD 6,525.0 Million in 2025, projected to reach USD 14,640.8 Million by 2033, growing at 10.63%, driven by rising cyber threats and digital transformation.

Top Growth Drivers: Cloud adoption increased by 65%, ransomware attacks surged by 45%, and endpoint security demand rose by 52%.

Short-Term Forecast: By 2028, enterprises are expected to reduce cybersecurity breach costs by 30% through automation and AI integration.

Emerging Technologies: AI-driven threat detection, zero-trust architecture, and blockchain-based security frameworks are transforming protection systems.

Regional Leaders: North America projected at USD 5,800 Million by 2033 with enterprise focus; Asia-Pacific USD 4,200 Million driven by SMEs; Europe USD 3,600 Million led by compliance-driven adoption.

Consumer/End-User Trends: Over 70% of enterprises prioritize cloud-based security, while SMEs adoption increased by 48% due to SaaS models.

Pilot or Case Example: In 2025, a U.S. financial firm implemented AI security tools, reducing threat detection time by 42% and system downtime by 28%.

Competitive Landscape: Market leader holds approximately 18% share, followed by major players including IBM, Microsoft, Cisco, Palo Alto Networks, and Fortinet.

Regulatory & ESG Impact: GDPR and global data protection laws increased compliance-driven adoption by 40%, while ESG initiatives push 25% reduction in energy-intensive security operations.

Investment & Funding Patterns: Over USD 25 billion invested globally in cybersecurity startups, with increasing venture capital in AI-based security solutions.

Innovation & Future Outlook: Integration of AI, automation, and predictive analytics is expected to enhance threat prevention efficiency by over 50%.

Security software demand is driven by BFSI (32%), IT & telecom (26%), and healthcare (18%) sectors, with increasing adoption of AI-based threat detection systems. Regulatory compliance mandates and rising cloud infrastructure usage accelerate demand, while emerging trends such as zero-trust architecture and automation-driven cybersecurity solutions are reshaping enterprise security strategies globally.

The Security Software Market holds strategic importance as organizations increasingly depend on digital ecosystems, cloud platforms, and connected devices. Cybersecurity is no longer a support function but a core business enabler, protecting critical infrastructure, intellectual property, and customer data. Enterprises are allocating up to 12–15% of their IT budgets to cybersecurity solutions, reflecting its rising priority. Advanced technologies such as AI-based threat detection are reshaping the landscape, where AI-driven systems deliver 40% faster threat identification compared to traditional rule-based security systems.

From a regional perspective, North America dominates in volume due to high enterprise spending and advanced infrastructure, while Asia-Pacific leads in adoption growth with over 62% of SMEs integrating cloud-based security solutions. This divergence highlights the shift toward scalable and cost-effective solutions in emerging markets. By 2028, AI-driven automation is expected to reduce incident response time by 35%, improving overall cybersecurity resilience.

Compliance and ESG considerations are becoming critical. Firms are committing to reducing energy consumption in data centers by 20% by 2030 through efficient security infrastructure and green cloud deployments. Data privacy regulations such as GDPR and CCPA have increased compliance spending by over 30%, further strengthening market demand.

A practical example includes a 2025 initiative in the United States, where a large enterprise implemented zero-trust architecture, achieving a 45% reduction in unauthorized access incidents and improving system reliability by 25%. Looking ahead, the Security Software Market will continue to serve as a pillar of resilience, compliance, and sustainable growth, enabling organizations to securely navigate digital transformation.

The Security Software Market is shaped by rapid digital transformation, increasing cyber threats, and the growing complexity of IT environments. Organizations are shifting toward cloud-based infrastructures, with over 70% of enterprises deploying hybrid or multi-cloud systems, creating new vulnerabilities that require advanced protection. The proliferation of IoT devices, estimated to exceed 29 billion connected devices globally by 2030, further expands the attack surface, increasing the need for robust endpoint and network security solutions. Additionally, regulatory frameworks such as GDPR and industry-specific compliance requirements have intensified the adoption of security software. Businesses are also focusing on automation and AI-driven solutions to manage security operations efficiently, as manual threat detection proves inadequate against evolving cyber risks. The rise of remote work has increased endpoint exposure by over 50%, driving demand for identity and access management solutions. Overall, the market is influenced by continuous technological innovation, regulatory pressures, and evolving threat landscapes.

The rapid increase in cyber threats is a major driver for the Security Software Market. In 2025, ransomware attacks increased by over 45%, while phishing incidents impacted nearly 70% of global organizations. Enterprises are responding by strengthening cybersecurity frameworks, with over 65% implementing multi-layered security architectures. The rise in data breaches, with an average of 2,200 cyberattacks occurring daily worldwide, has made proactive threat detection essential. Additionally, sectors such as BFSI and healthcare, which handle sensitive data, have increased their security spending significantly, with over 60% adopting AI-powered threat detection tools. Cloud adoption has further intensified security needs, as over 72% of businesses now operate in cloud environments, requiring advanced security solutions to protect distributed data systems. This growing threat landscape continues to drive investment and innovation in security software solutions.

High implementation and maintenance costs remain a significant restraint for the Security Software Market. Advanced security solutions, particularly those involving AI and machine learning, require substantial upfront investment, making them less accessible for small and medium enterprises. On average, enterprises spend between 8% to 12% of their IT budgets on cybersecurity, which can strain financial resources. Additionally, integration complexities with legacy systems increase deployment time by up to 30%, discouraging adoption. Skilled cybersecurity professionals are also in short supply, with a global workforce gap exceeding 3 million professionals, further raising operational costs. Maintenance and continuous updates of security systems require additional expenditure, making long-term adoption challenging for budget-constrained organizations. These factors collectively limit widespread adoption, particularly in emerging economies.

The expansion of cloud computing presents significant opportunities for the Security Software Market. Over 75% of enterprises are expected to transition to cloud-based infrastructure, creating demand for scalable and flexible security solutions. Cloud security adoption has increased by nearly 60%, driven by the need to protect distributed workloads and remote access environments. Additionally, the rise of Software-as-a-Service (SaaS) platforms has enabled cost-effective deployment, particularly for SMEs, boosting adoption rates by over 48%. Emerging technologies such as zero-trust security models and AI-based threat analytics are creating new avenues for innovation. The increasing use of IoT devices, projected to exceed 29 billion globally, further drives demand for advanced security frameworks. These factors collectively create a favorable environment for market expansion and technological advancement.

The increasing complexity of cyberattacks presents a major challenge for the Security Software Market. Modern threats such as advanced persistent threats (APTs) and AI-driven malware are becoming more sophisticated, making traditional security systems less effective. Over 60% of cyberattacks now involve multi-vector strategies, targeting multiple entry points simultaneously. Additionally, zero-day vulnerabilities continue to rise, with organizations taking an average of 21 days to identify and mitigate such threats. The rapid evolution of attack techniques requires continuous updates and innovation in security solutions, increasing operational complexity. Furthermore, the shortage of skilled cybersecurity professionals limits the ability of organizations to effectively manage and respond to threats. These challenges highlight the need for advanced, automated, and adaptive security systems.

AI-Driven Threat Detection Adoption Rising Rapidly: Over 65% of enterprises have integrated AI-based security systems to enhance threat detection capabilities. These systems reduce false positives by nearly 35% and improve response efficiency by 40%. Automated security operations are increasingly replacing manual monitoring, particularly in financial and healthcare sectors.

Growth of Zero-Trust Security Models: Approximately 58% of organizations have adopted zero-trust frameworks, with implementation improving access control efficiency by 30%. Enterprises deploying zero-trust architectures report a 45% reduction in unauthorized access incidents, highlighting strong adoption across regulated industries.

Expansion of Cloud-Based Security Solutions: Cloud security solutions account for nearly 62% of deployments, driven by remote work and hybrid infrastructure. Businesses report a 38% improvement in scalability and a 28% reduction in infrastructure costs through cloud-based security platforms.

Increased Investment in Endpoint Security: Endpoint security adoption has risen by 52%, with organizations protecting an average of 135 endpoints per enterprise. Advanced endpoint detection systems have reduced breach incidents by 33%, especially in IT and telecom sectors with high device connectivity.

The Security Software Market is segmented based on type, application, and end-user, reflecting diverse adoption patterns across industries. Network security, endpoint security, cloud security, and application security represent the primary product categories, each addressing specific vulnerabilities in modern IT environments. Applications range from enterprise data protection and identity management to fraud detection and infrastructure security. End-users include BFSI, healthcare, IT & telecom, government, and retail sectors, each with distinct security requirements. BFSI and IT sectors dominate due to high data sensitivity, while healthcare shows rapid adoption due to increasing digitalization. The growing use of cloud platforms and IoT devices further influences segmentation trends, driving demand for scalable and integrated security solutions across multiple industries.

Network security leads the segment with approximately 34% share due to its critical role in protecting enterprise infrastructure from external threats. Endpoint security follows with around 26%, driven by the rise in remote work and device proliferation. Cloud security is the fastest-growing segment, with an expected CAGR of 14.8%, supported by increasing cloud adoption across enterprises. Application security accounts for nearly 18%, focusing on safeguarding software and digital applications from vulnerabilities. Other types, including identity and access management and data security, collectively contribute around 22% of the market, serving niche but essential roles in comprehensive security frameworks.

• In 2025, a global enterprise security deployment protected over 1 million endpoints using AI-driven endpoint security tools, improving threat detection efficiency by 40%.

Enterprise data protection dominates with approximately 36% share, as organizations prioritize safeguarding sensitive information. Network protection accounts for 24%, while application security holds around 20%. Cloud security applications are the fastest-growing, with a CAGR of 15.2%, driven by hybrid cloud adoption. Other applications contribute nearly 20%, including identity management and fraud detection. In 2025, over 42% of enterprises globally reported implementing advanced security solutions for customer data protection, while 60% of organizations prioritized cloud-based security platforms.

• In 2025, over 150 large enterprises implemented AI-powered threat detection systems, improving breach prevention rates by 35%.

BFSI leads with approximately 32% share due to high regulatory requirements and data sensitivity. IT & telecom follows with 26%, while healthcare accounts for 18%. Retail and government sectors collectively contribute around 24%. Healthcare is the fastest-growing segment, with a CAGR of 13.9%, driven by digital health adoption. In 2025, over 55% of healthcare organizations implemented AI-based security solutions, while 48% of SMEs adopted cloud security platforms.

• In 2025, over 500 financial institutions enhanced cybersecurity frameworks, reducing fraud incidents by 30% through AI integration.

North America accounted for the largest market share at 38% in 2025 however, Asia-Pacific is expected to register the fastest growth, expanding at a CAGR of 12.4% between 2026 and 2033.

Europe holds approximately 26% share, driven by strict regulatory compliance, while Asia-Pacific accounts for 24%, supported by rapid digitalization. South America and Middle East & Africa collectively contribute around 12%, reflecting emerging adoption trends. Over 70% of enterprises in North America utilize advanced cybersecurity solutions, compared to 62% in Asia-Pacific. Cloud security adoption exceeds 65% in developed regions, while emerging markets show adoption rates around 48%, indicating strong future growth potential.

North America holds approximately 38% market share, driven by strong demand from BFSI, healthcare, and IT sectors. Regulatory frameworks such as CCPA and HIPAA push organizations to adopt robust security measures. Over 70% of enterprises deploy cloud-based security solutions, reflecting high digital maturity. Technological advancements, including AI-driven threat detection, are widely adopted. A major U.S.-based company implemented AI security tools, reducing breach incidents by 35%. Consumer behavior shows higher adoption in healthcare and finance sectors.

Europe accounts for around 26% market share, with Germany, the UK, and France leading adoption. GDPR regulations drive compliance-focused security investments, with over 65% of enterprises implementing advanced data protection systems. Emerging technologies such as zero-trust models are widely adopted. Regional players focus on secure cloud infrastructure, enhancing data privacy. Consumer behavior reflects strong demand for compliance-driven solutions.

Asia-Pacific represents approximately 24% market share, with China, India, and Japan as key contributors. Rapid digitalization and cloud adoption drive demand, with over 62% of SMEs adopting security solutions. Technology hubs and innovation centers accelerate AI-based security deployment. A regional company implemented scalable cloud security platforms, improving efficiency by 30%. Consumer trends show growth driven by mobile applications and e-commerce.

South America holds around 7% market share, led by Brazil and Argentina. Growth is driven by increasing digital infrastructure and financial sector expansion. Government initiatives promote cybersecurity adoption, with over 45% of enterprises implementing basic security frameworks. Consumer behavior reflects rising demand for localized security solutions.

Middle East & Africa accounts for approximately 5% share, with UAE and South Africa leading growth. Demand is driven by oil & gas and construction sectors. Technological modernization and government initiatives boost adoption. Over 40% of enterprises are investing in advanced security solutions. Consumer trends show increasing awareness of cybersecurity risks.

United States – 38% Market share: Strong enterprise cybersecurity investment and advanced technological adoption

China – 16% Market share: Rapid digitalization and large-scale enterprise demand

The Security Software Market is moderately fragmented, with over 150 active global and regional players competing across various segments. The top five companies collectively account for approximately 45% of the market, indicating a balanced competitive environment. Leading players focus on innovation, strategic partnerships, and acquisitions to strengthen their market position. Over 60% of companies are investing in AI-based security solutions, while 48% prioritize cloud security integration.

Product launches and platform enhancements are common, with an average of 20–25 new solutions introduced annually. Strategic collaborations between technology firms and cybersecurity providers are increasing, enhancing solution capabilities. The market is characterized by rapid technological evolution, with companies focusing on automation, predictive analytics, and integrated security platforms to maintain competitive advantage.

IBM Corporation

Cisco Systems Inc.

Palo Alto Networks Inc.

Fortinet Inc.

Check Point Software Technologies Ltd.

Trend Micro Inc.

Symantec Corporation

McAfee Corp.

CrowdStrike Holdings Inc.

FireEye Inc.

Sophos Group plc

Kaspersky Lab

Rapid7 Inc.

The Security Software Market is undergoing significant technological transformation driven by advancements in artificial intelligence, machine learning, and cloud computing. AI-based threat detection systems are capable of analyzing over 1 million events per second, improving detection accuracy by 40% compared to traditional systems. Machine learning algorithms are widely used for behavioral analysis, enabling early identification of anomalies and reducing false positives by up to 35%. Cloud-native security solutions are gaining traction, with over 60% of enterprises deploying security tools directly within cloud environments, improving scalability and response times.

Zero-trust architecture is becoming a standard approach, with nearly 58% of organizations adopting it to enhance access control and minimize unauthorized entry. Blockchain technology is also emerging as a tool for securing data transactions, with pilot implementations improving data integrity by 30%. Additionally, automation in security operations is reducing response times by up to 45%, allowing organizations to handle threats more efficiently.

The integration of Internet of Things (IoT) security solutions is another key trend, as the number of connected devices continues to grow. Advanced endpoint detection and response (EDR) systems are capable of monitoring thousands of devices simultaneously, reducing breach incidents by 33%. These technological advancements are shaping the future of the Security Software Market, enabling organizations to build resilient and adaptive cybersecurity frameworks.

• In November 2025, Palo Alto Networks and IBM announced a joint Quantum-Safe Readiness solution to help enterprises identify cryptographic risks and transition to quantum-resistant security frameworks. The solution enables real-time protection and automated inventory of cryptographic assets across hybrid environments. Source: www.paloaltonetworks.com

• In December 2025, Palo Alto Networks partnered with Google Cloud to accelerate secure cloud and AI adoption, focusing on protecting AI workloads and expanding cloud-native security capabilities for enterprises operating in multi-cloud environments.

• In June 2025, Microsoft launched its European Security Program, offering free AI-powered cybersecurity services, including enhanced threat intelligence sharing and nation-state attack protection, aimed at strengthening digital resilience across European governments and enterprises.

• In October 2024, IBM released its updated X-Force Threat Intelligence Index, reporting a 44% increase in attacks targeting public-facing applications and highlighting the growing role of AI-enabled threat detection in identifying vulnerabilities across enterprise systems.

The Security Software Market Report provides a comprehensive analysis of key industry segments, including network security, endpoint protection, cloud security, and application security. The report covers diverse applications such as enterprise data protection, identity management, and infrastructure security across multiple industries, including BFSI, healthcare, IT & telecom, retail, and government sectors. It evaluates regional markets across North America, Europe, Asia-Pacific, South America, and Middle East & Africa, highlighting variations in adoption rates, technological advancements, and regulatory frameworks.

The report also examines technological developments such as AI-driven threat detection, zero-trust architecture, and cloud-native security platforms. It includes insights into consumer behavior, enterprise adoption patterns, and emerging trends such as IoT security and automation in cybersecurity operations. Additionally, the report outlines competitive dynamics, profiling key players and their strategic initiatives, including product innovations, partnerships, and market expansion efforts.

Furthermore, the scope extends to analyzing investment trends, regulatory impacts, and industry-specific requirements influencing demand. The report aims to provide decision-makers with actionable insights into market dynamics, enabling informed strategic planning and investment decisions in the evolving Security Software Market.

| Report Attribute / Metric | Details |

|---|---|

| Market Revenue (2025) | USD 6,525.0 Million |

| Market Revenue (2033) | USD 14,640.8 Million |

| CAGR (2026–2033) | 10.63% |

| Base Year | 2025 |

| Forecast Period | 2026–2033 |

| Historic Period | 2021–2025 |

| Segments Covered |

By Type

By Application

By End-User Insights

|

| Key Report Deliverables | Revenue Forecast; Market Trends; Growth Drivers & Restraints; Technology Insights; Segmentation Analysis; Regional Insights; Competitive Landscape; Regulatory & ESG Overview; Recent Developments |

| Regions Covered | North America; Europe; Asia-Pacific; South America; Middle East & Africa |

| Key Players Analyzed | Microsoft Corporation; IBM Corporation; Cisco Systems Inc.; Palo Alto Networks Inc.; Fortinet Inc.; Check Point Software Technologies Ltd.; Trend Micro Inc.; Symantec Corporation; McAfee Corp.; CrowdStrike Holdings Inc.; FireEye Inc.; Sophos Group plc; Kaspersky Lab; Rapid7 Inc. |

| Customization & Pricing | Available on Request (10% Customization Free) |