Reports

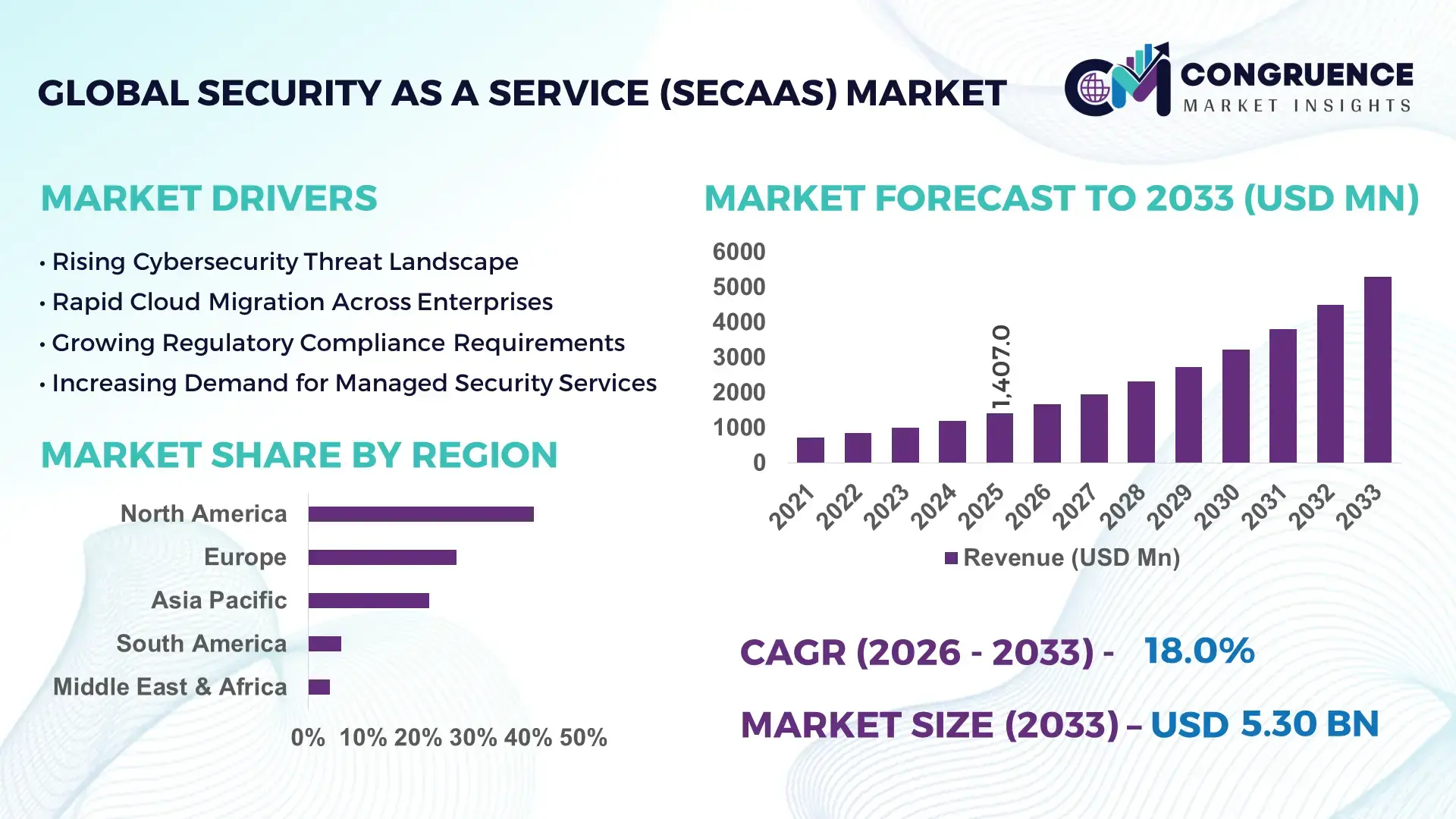

The Global Security as a Service (SECaaS) Market was valued at USD 1,407.0 Million in 2025 and is anticipated to reach a value of USD 5,299.5 Million by 2033 expanding at a CAGR of 18.03% between 2026 and 2033, according to an analysis by Congruence Market Insights. The market growth is primarily driven by rapid cloud migration, rising cyberattack frequency, and enterprise demand for scalable, subscription-based security models that reduce capital expenditure while enhancing real-time threat intelligence capabilities.

The United States dominates the global Security as a Service (SECaaS) Market, supported by high enterprise cybersecurity spending exceeding USD 90 billion annually across public and private sectors. Over 72% of large enterprises in the U.S. have adopted at least one cloud-delivered security solution, with Zero Trust architectures implemented in more than 58% of federal agencies. The country hosts over 1,500 cybersecurity firms, including major managed security service providers operating large-scale Security Operations Centers (SOCs) handling billions of threat events daily. Investment in AI-driven threat detection surpassed USD 8 billion in 2025, while cloud-native security deployments expanded across BFSI, healthcare, and defense sectors, reflecting strong production capacity and technological innovation in advanced threat analytics and automated response systems.

Market Size & Growth: Valued at USD 1,407.0 Million in 2025, projected to reach USD 5,299.5 Million by 2033, expanding at 18.03% CAGR; growth fueled by 65% enterprise shift toward cloud-first IT strategies.

Top Growth Drivers: 72% cloud workload migration rate; 48% increase in ransomware incidents; 55% cost savings through outsourced security models.

Short-Term Forecast: By 2028, AI-enabled SOC automation is expected to reduce incident response time by 40%.

Emerging Technologies: AI-driven threat intelligence, Zero Trust Network Access (ZTNA), Secure Access Service Edge (SASE) frameworks.

Regional Leaders: North America projected above USD 2,100 Million by 2033 with strong federal adoption; Europe nearing USD 1,400 Million driven by GDPR compliance; Asia-Pacific exceeding USD 1,100 Million with 60% SME cloud-security uptake.

Consumer/End-User Trends: BFSI and healthcare collectively represent over 45% of deployments, prioritizing real-time monitoring and compliance automation.

Pilot or Case Example: In 2025, a U.S. financial institution reduced phishing-related breaches by 37% through AI-powered SECaaS implementation.

Competitive Landscape: Market leader holds approximately 18% share, followed by IBM, Cisco, Palo Alto Networks, Fortinet, and Trend Micro.

Regulatory & ESG Impact: Data protection laws and cyber resilience directives are pushing 62% of enterprises to increase managed security budgets.

Investment & Funding Patterns: Over USD 12 billion invested globally in cybersecurity startups in 2025, with strong venture funding in AI security platforms.

Innovation & Future Outlook: Integration of quantum-resistant encryption and predictive threat analytics is shaping next-generation SECaaS platforms.

BFSI contributes approximately 28% of total deployments, followed by healthcare at 17% and IT & telecom at 15%. AI-driven threat analytics and SASE platforms are reshaping delivery models, while regulatory frameworks such as data protection mandates drive compliance-centric adoption. North America leads consumption, though Asia-Pacific shows rapid SME onboarding. Increasing integration with edge computing and IoT security reflects strong forward momentum for resilient digital infrastructure.

The Security as a Service (SECaaS) Market holds strategic relevance as organizations transition from perimeter-based defenses to cloud-native, identity-centric security frameworks. Enterprises are reallocating up to 35% of their IT security budgets toward subscription-based models to enhance scalability and predictive analytics. AI-driven extended detection and response (XDR) platforms deliver 45% faster threat containment compared to traditional Security Information and Event Management (SIEM) systems. North America dominates in deployment volume, while Asia-Pacific leads in adoption momentum, with nearly 60% of mid-sized enterprises implementing managed cloud security solutions.

By 2028, AI-powered automation within managed SOC environments is expected to cut operational security costs by 30% while improving threat detection accuracy by 25%. Firms are committing to ESG-aligned cyber resilience targets, including 20% reductions in data-center energy use through optimized cloud-security configurations by 2030. In 2025, a major U.S.-based cloud provider achieved a 42% reduction in breach response time through automated playbook orchestration integrated within its SECaaS stack.

Strategically, the market is moving toward SASE convergence, Zero Trust enforcement, and quantum-safe encryption readiness. These initiatives position the Security as a Service (SECaaS) Market as a foundational pillar of enterprise resilience, regulatory compliance, and sustainable digital transformation in an increasingly complex threat environment.

The Security as a Service (SECaaS) Market is shaped by accelerating digital transformation, growing threat sophistication, and increasing regulatory oversight. Enterprises are managing over 60% of workloads in cloud environments, intensifying demand for scalable identity management, endpoint protection, and network security services. The average cost of a data breach has surpassed USD 4 million globally, prompting proactive investments in continuous monitoring and threat intelligence. Additionally, more than 50% of organizations report cybersecurity skills shortages, reinforcing reliance on outsourced managed security providers. Integration of AI-based anomaly detection, automation in incident response, and API-based cloud security orchestration further define the evolving competitive landscape of the Security as a Service (SECaaS) Market.

Over 75% of enterprises globally have adopted hybrid or multi-cloud strategies, creating complex security perimeters requiring continuous monitoring. Cloud-native applications generate 3x more telemetry data than traditional IT systems, demanding advanced analytics and automated response mechanisms. Ransomware attacks increased by nearly 50% year-over-year, compelling organizations to adopt managed detection and response services. Approximately 68% of CIOs prioritize cloud security spending over on-premise upgrades, reflecting structural shifts in cybersecurity strategies. The increasing use of remote work models, with 58% of employees accessing corporate systems remotely at least once weekly, further strengthens demand for secure access service edge (SASE) and Zero Trust deployments within the Security as a Service (SECaaS) Market.

Cross-border data transfer restrictions affect over 40% of multinational enterprises operating in regulated industries. Compliance with region-specific regulations often requires localized data storage, increasing deployment complexity for global SECaaS providers. Integration with legacy infrastructure remains challenging, as nearly 35% of large enterprises still operate mission-critical systems on outdated architectures. Vendor lock-in concerns impact 30% of IT leaders when selecting cloud-based security providers. Additionally, false positive rates in automated threat detection systems can exceed 15%, increasing operational workload and potentially slowing broader adoption of fully automated security frameworks.

AI-powered behavioral analytics can detect anomalies with 35% higher accuracy compared to rule-based systems. Automation reduces incident response time by up to 40%, enabling leaner security teams to manage high alert volumes efficiently. The rise of IoT ecosystems, with over 29 billion connected devices projected globally, creates significant demand for scalable endpoint security services. SMEs represent a substantial untapped segment, as only 45% currently deploy managed cloud-security solutions. Increasing government funding for cyber resilience programs and smart city initiatives also opens new vertical opportunities for integrated SECaaS platforms.

The global cybersecurity workforce gap exceeds 3 million professionals, limiting in-house expertise and increasing dependence on managed providers. High demand for skilled analysts drives wage inflation, increasing operational costs for service vendors. Approximately 52% of organizations report difficulty retaining cybersecurity professionals beyond two years. Rapidly evolving threat vectors, including AI-generated phishing and deepfake-based social engineering, require continuous skill upgrades and tool enhancements. Moreover, over 25% of enterprises experience alert fatigue due to excessive threat notifications, reducing operational efficiency and creating challenges for effective incident prioritization within the Security as a Service (SECaaS) Market.

AI-Driven Threat Detection Improving Accuracy by 35%: AI-based anomaly detection systems now analyze over 1 billion security events daily across large enterprises. Organizations deploying AI-enabled SECaaS platforms report 35% higher detection precision and 28% fewer false positives, improving operational efficiency and reducing analyst workload by nearly 30%.

Rapid Expansion of Zero Trust Architectures with 58% Enterprise Adoption: More than 58% of large enterprises have implemented Zero Trust principles, segmenting networks and enforcing identity-based access. Multi-factor authentication usage has risen to 70% across cloud environments, reducing credential-based breaches by approximately 45%.

SASE Framework Adoption Growing Across 60% of Distributed Workforces: Secure Access Service Edge integration has expanded among 60% of multinational firms managing hybrid workforces. Organizations report 32% improvement in secure remote access performance and 25% reduction in VPN-related vulnerabilities after SASE deployment.

SME Cloud-Security Uptake Surpassing 50% in Emerging Economies: Over 50% of SMEs in Asia-Pacific and Latin America have adopted subscription-based endpoint and email security services. Automated patch management solutions reduce system downtime by 20% and improve compliance readiness scores by 18% across small enterprises.

The Security as a Service (SECaaS) Market is segmented by type, application, and end-user, reflecting diverse enterprise security needs. Cloud-based email security and endpoint protection solutions represent widespread adoption across digital enterprises. Applications span network security, identity access management, data loss prevention, and SIEM-based analytics. BFSI, healthcare, government, IT & telecom, and retail remain key end-user sectors due to high regulatory oversight and digital transaction volumes. Increasing hybrid work models and rising cloud workload penetration continue reshaping segmentation dynamics, with identity-centric security solutions gaining traction globally.

The Security as a Service (SECaaS) Market by type includes Email Security, Endpoint Security, Cloud Security, Network Security, Data Loss Prevention (DLP), Identity & Access Management (IAM), Security Information & Event Management (SIEM), and Managed Detection & Response (MDR). Email security currently accounts for approximately 28% of total adoption due to persistent phishing attacks and business email compromise incidents. Endpoint security holds nearly 22%, driven by remote workforce device expansion exceeding 55% globally. Cloud security solutions contribute around 18%, reflecting increased multi-cloud deployment strategies. However, Managed Detection & Response (MDR) is the fastest-growing type, expanding at nearly 21% annually, supported by increasing enterprise outsourcing of SOC operations. IAM solutions account for about 15%, reflecting the expansion of zero-trust frameworks. The remaining segments, including DLP and network security, collectively represent roughly 17% of adoption, supporting regulatory compliance and data governance initiatives.

Applications of Security as a Service (SECaaS) span Network Security (30% share), Endpoint Security (24%), Identity & Access Management (20%), Data Protection (15%), and Compliance Monitoring (11%). Network security remains the leading application due to rising distributed infrastructure exposure and increasing DDoS incidents affecting global enterprises. Endpoint security adoption has grown significantly as over 58% of employees operate remotely at least part-time. Identity & Access Management is the fastest-growing application, expanding at approximately 20% annually, supported by biometric and multi-factor authentication adoption rates exceeding 65% in large enterprises. Data protection services, including encryption and DLP, support regulatory mandates across healthcare and financial institutions. Remaining applications contribute around 26% collectively, supporting operational resilience and audit readiness. In 2025, more than 40% of enterprises globally reported piloting AI-driven security monitoring platforms for compliance automation. Over 62% of financial institutions implemented continuous authentication tools to strengthen digital banking security.

The BFSI sector leads the Security as a Service (SECaaS) Market with approximately 32% share due to high digital transaction volumes and stringent cybersecurity mandates. IT & telecom follows at around 21%, driven by extensive cloud infrastructure operations. Healthcare accounts for nearly 18%, reflecting increased protection of electronic health records and connected medical devices. Government entities contribute about 14%, focusing on national cybersecurity modernization programs. Retail and e-commerce together represent nearly 10%, protecting digital payment ecosystems. Healthcare is the fastest-growing end-user segment, expanding at nearly 19% annually due to rising ransomware targeting hospitals and telehealth platforms. Over 45% of hospitals globally are investing in cloud-delivered endpoint protection systems. Approximately 60% of large enterprises across sectors have adopted at least one managed security service platform. The remaining sectors collectively account for about 15% of adoption, supporting cross-industry digital transformation initiatives.

North America accounted for the largest market share at 41% in 2025 however, Asia-Pacific is expected to register the fastest growth, expanding at a CAGR of 21% between 2026 and 2033.

North America’s dominance is supported by over 72% enterprise cloud adoption and cybersecurity budgets exceeding 12% of total IT spending across Fortune 1000 firms. Europe held approximately 27% share, driven by regulatory compliance mandates affecting more than 65% of enterprises operating under GDPR-aligned frameworks. Asia-Pacific represented nearly 22% of global demand in 2025, with more than 58% of SMEs adopting at least one managed security service. South America accounted for 6% share, reflecting growing digital banking penetration above 70% in Brazil and Argentina. The Middle East & Africa contributed around 4%, supported by smart city investments surpassing USD 25 billion across the Gulf region. Globally, over 68% of organizations now outsource at least one cybersecurity function, indicating structural demand expansion across regions.

North America holds approximately 41% of the global Security as a Service (SECaaS) Market share, supported by strong enterprise digitization across BFSI, healthcare, defense, and retail sectors. Over 75% of large enterprises deploy managed detection and response solutions, while 58% have adopted Zero Trust frameworks. Regulatory developments such as updated federal cybersecurity mandates and state-level privacy regulations have compelled over 62% of enterprises to enhance cloud-security monitoring. AI-driven SOC platforms process more than 1.5 billion daily security events across major providers. A leading regional player, Palo Alto Networks, expanded its AI-powered XDR platform in 2025, enabling automated response actions that reduced incident resolution time by 40%. Consumer behavior shows higher adoption in finance and healthcare institutions, where over 70% of firms prioritize outsourced cloud-security models for compliance and risk mitigation.

Europe accounts for approximately 27% of the global Security as a Service (SECaaS) Market. Key markets include Germany, the UK, and France, collectively contributing over 60% of regional demand. More than 68% of enterprises in Western Europe have integrated managed identity and access management services to meet GDPR and NIS2 directive requirements. Sustainability initiatives encourage energy-efficient data center operations, with 35% of firms integrating green IT policies into cybersecurity strategies. Adoption of SASE frameworks has grown among 52% of multinational corporations. A notable regional company, Atos, expanded its managed SOC network across 15 European cities, supporting over 3,000 enterprise clients. Consumer behavior reflects regulatory-driven purchasing decisions, as 64% of enterprises prioritize compliance-ready SECaaS platforms with audit-tracking features.

Asia-Pacific represents nearly 22% of global volume and ranks second in deployment scale. China, India, and Japan collectively account for more than 65% of regional consumption. Over 60% of SMEs in India and Southeast Asia utilize subscription-based endpoint protection services, while Japan reports 55% adoption of managed cloud firewall platforms. Expansion of 5G infrastructure and e-commerce ecosystems, with digital payment penetration exceeding 75% in key economies, increases cybersecurity demand. A regional technology provider, Trend Micro (Japan), strengthened its AI-based threat detection platform in 2025, improving detection speed by 38%. Consumer behavior reflects strong mobile-first security preferences, as 67% of businesses prioritize mobile endpoint security and API protection for cloud-native applications.

South America accounts for approximately 6% of global Security as a Service (SECaaS) Market share. Brazil and Argentina represent nearly 70% of regional demand, driven by digital banking users exceeding 120 million across both countries. Infrastructure upgrades in energy and telecom sectors have pushed over 48% of large enterprises to adopt managed firewall and DDoS mitigation services. Government-backed cybersecurity strategies introduced in 2024 increased public-sector cloud security investments by 18%. A regional cybersecurity firm in Brazil expanded its managed SOC operations to monitor over 500 enterprise clients in 2025. Consumer trends show growing reliance on managed email security solutions, particularly in media and fintech sectors where phishing incidents rose by 32%.

The Middle East & Africa contributes nearly 4% to the global Security as a Service (SECaaS) Market. The UAE and Saudi Arabia account for over 55% of regional deployment, supported by smart city and digital transformation programs exceeding USD 30 billion in infrastructure commitments. Oil & gas enterprises, representing 35% of industrial cybersecurity demand, are integrating managed network monitoring solutions. South Africa shows 45% enterprise adoption of cloud-based endpoint protection. Governments have introduced national cybersecurity frameworks, requiring compliance audits for 60% of public institutions. A UAE-based cybersecurity integrator expanded AI-powered threat analytics platforms across 200 enterprises in 2025, improving incident visibility by 33%. Consumer behavior emphasizes data sovereignty and secure cloud storage adoption.

United States – 38% Market Share: Dominates due to high enterprise cybersecurity budgets, over 70% cloud workload migration, and strong Zero Trust enforcement across federal agencies.

Germany – 9% Market Share: Strong position supported by strict data protection regulations and over 65% enterprise compliance-driven security deployments.

The Security as a Service (SECaaS) Market exhibits a moderately fragmented structure with over 250 active global and regional competitors offering cloud-native security platforms, managed detection and response services, and SASE solutions. The top five companies collectively account for approximately 52% of total market share, indicating a competitive yet innovation-driven environment. Market leaders differentiate through AI-powered analytics, automation capabilities, and integrated cloud-security ecosystems.

Strategic partnerships and acquisitions remain prominent, with more than 40 cybersecurity-related mergers recorded in 2024–2025. Around 65% of leading vendors expanded managed SOC capabilities to support hybrid and multi-cloud environments. Product innovation focuses on AI-driven XDR, quantum-resistant encryption pilots, and automated compliance monitoring. Approximately 58% of vendors now integrate machine learning algorithms to reduce false positives by over 30%. Competitive intensity is further shaped by regional providers targeting SMEs, which represent nearly 36% of total customer base. Continuous platform upgrades, vertical-specific security modules, and subscription-based pricing models define the evolving competitive dynamics of the Security as a Service (SECaaS) Market.

Fortinet

Trend Micro

Check Point Software Technologies

Zscaler

Broadcom (Symantec Enterprise Security)

McAfee Enterprise

CrowdStrike

Sophos

Atos

Orange Cyberdefense

Tata Consultancy Services

The Security as a Service (SECaaS) Market is undergoing rapid technological transformation driven by AI, automation, and cloud-native architectures. AI-powered Extended Detection and Response (XDR) platforms analyze more than 1 billion security events daily in large enterprises, improving detection precision by up to 35%. Machine learning-based anomaly detection reduces false positives by approximately 28%, lowering analyst workload and improving response prioritization.

Secure Access Service Edge (SASE) integration is accelerating, with over 60% of multinational firms consolidating networking and security functions into unified cloud-delivered frameworks. Zero Trust Network Access (ZTNA) deployments now protect more than 58% of enterprise environments, replacing legacy VPN infrastructure and reducing credential-based breaches by nearly 45%.

Automation technologies such as Security Orchestration, Automation, and Response (SOAR) platforms decrease incident response time by up to 40%. Quantum-resistant encryption pilots are being tested across financial institutions to future-proof data protection strategies. API security solutions have gained importance as 83% of web traffic now involves API calls, increasing exposure to injection and authentication attacks.

Edge computing integration and IoT security frameworks are expanding, especially in manufacturing and smart city deployments, where over 29 billion connected devices require continuous monitoring. These technological advancements collectively reinforce operational resilience, regulatory compliance, and predictive risk management within the Security as a Service (SECaaS) Market.

• In November 2025, Palo Alto Networks and IBM announced a quantum-safe readiness solution to help enterprises identify cryptographic vulnerabilities and migrate critical infrastructure to quantum-resistant security controls, combining IBM’s quantum transformation services with Palo Alto’s cryptographic visibility tools; the solution is expected to be available in early 2026, addressing future-proof cybersecurity needs. Source: www.paloaltonetworks.in

• On January 28, 2025, IBM and Palo Alto Networks jointly published findings from a global survey showing that 75% of organizations pursuing security platform consolidation believe that better integration across hybrid cloud, AI, and security platforms significantly enhances operational efficiencies and business outcomes, also highlighting almost 52% of companies struggling with fragmented security stacks in complex enterprise environments. Source: www.newsroom.ibm.com

• In August 2025, Cisco and AT&T launched a unified Secure Access Service Edge (SASE) solution combining AT&T’s network expertise with Cisco Secure Access technology, delivering centralized security, intelligent SD-WAN routing, multilayer threat defense, and automated workflows for enterprises seeking simplified cloud-centric security and connectivity operations. Source: www.newsroom.cisco.com

• In February 2026, Cisco Systems announced a major expansion of its AI Defense and AI-aware SASE capabilities to secure agent-based AI systems and the AI supply chain. Innovations include new tools for AI Bill of Materials (AI BOM) governance, real-time agentic security guardrails, and multi-turn red teaming to protect enterprise AI assets. Source: www.investor.cisco.com

The Security as a Service (SECaaS) Market Report provides comprehensive coverage across solution types, deployment models, industry verticals, enterprise sizes, and geographic regions. It evaluates core segments including network security, endpoint protection, email security, IAM, DLP, cloud workload protection, and SASE frameworks. The report examines applications across BFSI, healthcare, IT & telecom, retail, manufacturing, energy, and government sectors, collectively representing over 80% of deployment demand.

Geographically, the scope spans North America, Europe, Asia-Pacific, South America, and the Middle East & Africa, incorporating country-level analysis for more than 15 major economies. Enterprise segmentation differentiates large corporations, accounting for 64% of adoption, and SMEs representing 36% with expanding subscription-based security uptake.

Technological analysis includes AI-driven XDR, SOAR automation, Zero Trust architectures, API security frameworks, and quantum-resistant encryption initiatives. The report also explores infrastructure modernization trends, regulatory compliance impacts affecting over 65% of enterprises globally, and the growing need for managed SOC services.

Additionally, the study evaluates competitive positioning, innovation pipelines, partnership ecosystems, and strategic initiatives influencing industry evolution. By integrating quantitative metrics and qualitative business insights, the report supports decision-makers in strategic planning, investment prioritization, risk assessment, and digital transformation roadmap development within the Security as a Service (SECaaS) Market.

| Report Attribute / Metric | Details |

|---|---|

| Market Revenue (2025) | USD 1,407.0 Million |

| Market Revenue (2033) | USD 5,299.5 Million |

| CAGR (2026–2033) | 18.03% |

| Base Year | 2025 |

| Forecast Period | 2026–2033 |

| Historic Period | 2021–2025 |

| Segments Covered |

By Type

By Application

By End-User

|

| Key Report Deliverables | Revenue Forecast; Market Trends; Growth Drivers & Restraints; Technology Insights; Segmentation Analysis; Regional Insights; Competitive Landscape; Regulatory & ESG Overview; Recent Developments |

| Regions Covered | North America; Europe; Asia-Pacific; South America; Middle East & Africa |

| Key Players Analyzed | Cisco Systems; IBM; Palo Alto Networks; Fortinet; Trend Micro; Check Point Software Technologies; Zscaler; Broadcom (Symantec Enterprise Security); McAfee Enterprise; CrowdStrike; Sophos; Atos; Orange Cyberdefense; Tata Consultancy Services |

| Customization & Pricing | Available on Request (10% Customization Free) |