Reports

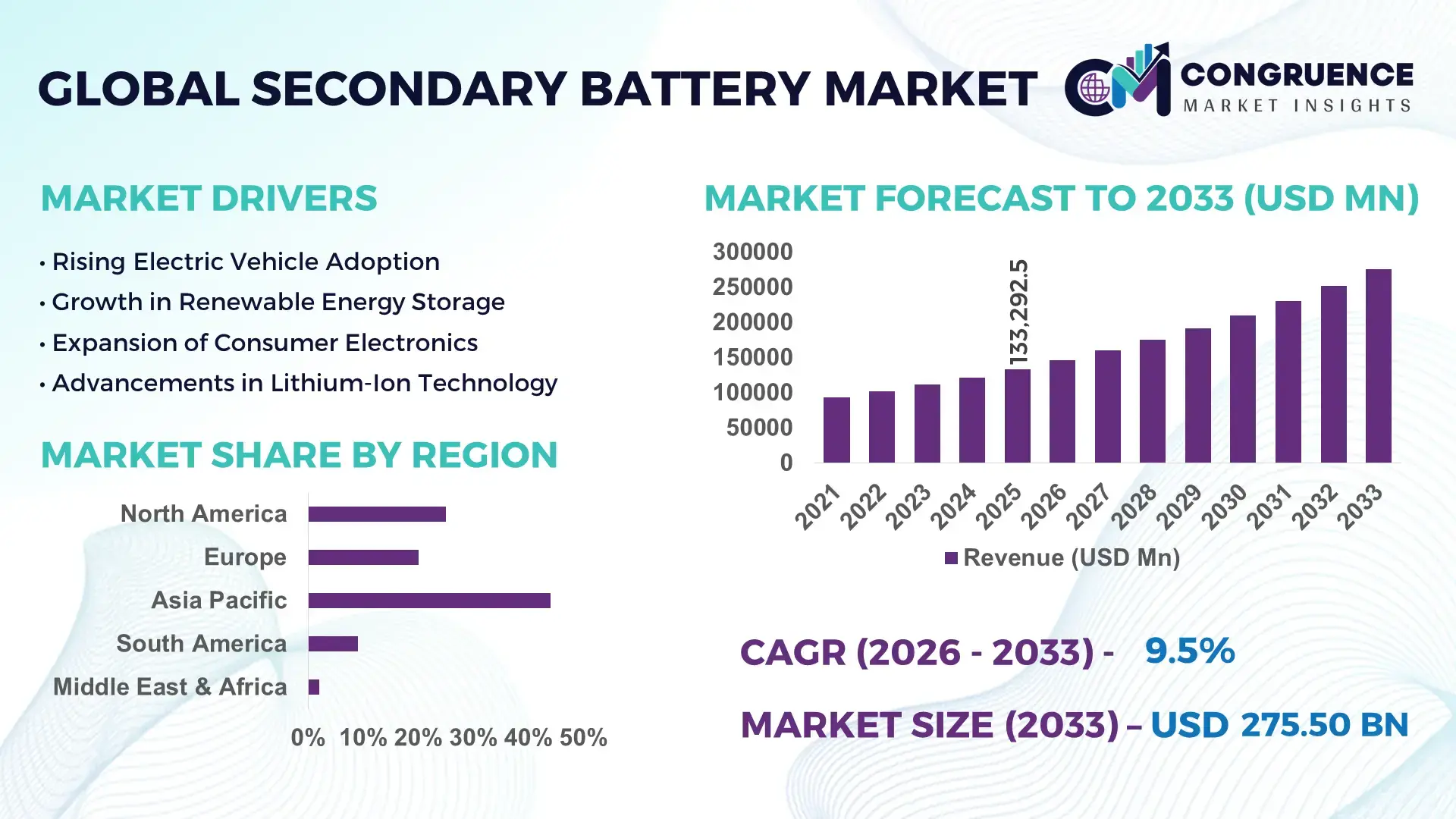

The Global Secondary Battery Market was valued at USD 133292.48 Million in 2025 and is anticipated to reach a value of USD 275498.11 Million by 2033 expanding at a CAGR of 9.5% between 2026 and 2033. Rapid electrification across automotive manufacturing and utility-scale energy storage accelerated high-density lithium-ion and solid-state secondary battery deployment, with battery pack energy efficiency improving by over 18% compared to conventional nickel-based systems in large-scale commercial applications during 2026.

China continues to dominate the global secondary battery market with more than 43% of global cell manufacturing capacity supported by multi-billion-dollar investments across electric vehicle, grid storage, and industrial electronics sectors. The country’s advanced battery ecosystem benefits from vertically integrated raw material processing and domestic EV adoption exceeding 38% of total new vehicle sales in 2026. In comparison, North America expanded localized battery manufacturing by over 24% following strategic supply-chain diversification initiatives linked to geopolitical trade tensions and critical mineral security policies. South Korea and Japan strengthened high-performance cathode and fast-charging battery innovation, reducing charging time by nearly 30% in premium automotive applications.

Manufacturers are prioritizing regionalized production, advanced chemistry partnerships, and raw material security to strengthen long-term competitiveness in the high-growth global secondary battery market.

Market Size & Growth: Global market reached USD 133292.48 Million in 2025 and is projected at USD 275498.11 Million by 2033, driven by EV battery localization and advanced energy storage expansion at 9.5% CAGR.

Top Growth Drivers: EV adoption contributed 38% demand growth, grid-scale storage installations rose 27%, and industrial automation battery usage expanded 19%.

Short-Term Forecast: By 2028, battery pack costs are projected to decline 21% while charging efficiency improves 17% through advanced cell engineering.

Emerging Technologies: AI-based battery management, silicon-anode chemistry, and solid-state platforms improved operational efficiency by nearly 15% in pilot deployments.

Regional Leaders: Asia-Pacific surpassed USD 88 Billion with strong EV penetration, North America exceeded USD 41 Billion through localized giga-factories, and Europe crossed USD 36 Billion supported by clean-energy regulations.

Consumer/End-User Trends: Over 46% of automotive buyers preferred long-range battery-powered vehicles with fast-charging capability below 25 minutes.

Pilot/Case Example: In 2026, a utility-scale storage project in Europe improved renewable energy utilization efficiency by 28% using advanced lithium-iron-phosphate systems.

Competitive Landscape: Chinese manufacturers controlled nearly 41% global supply share alongside major players including CATL, LG Energy Solution, Panasonic, Samsung SDI, and BYD.

Regulatory & ESG Impact: Carbon-neutral manufacturing initiatives reduced battery production emissions by approximately 16% across regulated facilities in Europe and Asia.

Investment & Funding: Global investments exceeded USD 95 Billion in battery plants, recycling infrastructure, and mineral supply partnerships amid regional supply-chain restructuring.

Innovation & Future Outlook: Next-generation sodium-ion and solid-state batteries are reshaping strategic energy storage planning with improved thermal stability exceeding 20%.

Automotive applications account for nearly 61% of global secondary battery demand, followed by consumer electronics and utility-scale energy storage systems. Advanced lithium-iron-phosphate and silicon-anode battery innovations are improving cycle life and thermal efficiency while supporting faster commercial deployment. Asia-Pacific remains the strongest production and consumption hub, whereas North America is rapidly expanding localized manufacturing due to supply-chain security initiatives and clean-energy incentives. Battery recycling integration emerged as a major industry trend, with material recovery efficiency surpassing 72% in advanced facilities. These developments are positioning the industry for deeper vertical integration, technology partnerships, and long-term strategic capacity expansion.

The secondary battery market has become strategically critical for automotive competitiveness, grid resilience, and industrial electrification as governments and manufacturers restructure supply chains around energy security and localized production. Battery manufacturing localization accelerated after critical mineral export controls and clean-energy incentive programs reshaped procurement priorities across China, the United States, and Europe. More than 35% of new industrial energy storage projects commissioned in 2026 integrated advanced battery systems with digital monitoring platforms to improve operational continuity and peak-load balancing.

Advanced lithium-iron-phosphate batteries now deliver nearly 22% lower thermal management costs compared to legacy nickel-cadmium systems while extending cycle life beyond 4,500 charge cycles in commercial deployment environments. China maintains scale advantages through vertically integrated cathode and refining infrastructure, whereas the United States is expanding domestic cell manufacturing capacity through giga-factory partnerships and recycling integration. Japan and South Korea continue leading premium solid-state and high-density battery innovation focused on fast-charging mobility and aerospace-grade storage systems.

A major logistics operator in Germany recently deployed AI-enabled secondary battery storage systems that reduced facility energy fluctuations by 18% while improving renewable power utilization consistency. Companies are increasing investments in battery recycling, sodium-ion technology, and long-term mineral sourcing agreements to strengthen supply resilience and manufacturing flexibility through 2028. Competitive leadership will increasingly depend on localized production ecosystems, advanced chemistry commercialization, and integrated energy management capabilities.

Electric vehicle production and utility-scale energy storage deployment continue to reshape global secondary battery demand patterns. China accounted for more than 38% of global EV sales in 2026, while stationary battery installations for renewable integration increased by nearly 26% across industrial power networks. The United States accelerated domestic battery manufacturing incentives following strategic supply-chain restructuring policies tied to critical mineral dependency reduction. This shift directly increased localized cathode and cell production investments, reducing logistics exposure and improving procurement stability. Automotive manufacturers and industrial operators are responding through long-term lithium sourcing agreements, battery recycling partnerships, and vertically integrated production expansion. A notable operational trend involves manufacturers prioritizing lithium-iron-phosphate chemistry for commercial fleets due to lower thermal risk and nearly 15% lower lifecycle maintenance costs compared to legacy battery platforms.

Volatility in lithium, nickel, and cobalt procurement continues to pressure operational margins and deployment planning across the secondary battery market. Battery-grade lithium processing costs fluctuated by more than 19% during recent supply-chain disruptions, while over 32% of manufacturers reported extended procurement lead times for critical materials. Limited charging and grid infrastructure expansion in India and parts of Southeast Asia is restricting large-scale deployment consistency for advanced battery systems. These constraints increase project costs, delay industrial electrification programs, and reduce manufacturing predictability for automotive and storage providers. Companies are mitigating exposure through localized refining investments, multi-country sourcing contracts, and accelerated sodium-ion battery development. A key strategic response includes recycling-based material recovery systems capable of reducing virgin raw material dependency by nearly 20% in high-volume manufacturing operations.

Next-generation battery chemistry platforms and circular manufacturing models are creating high-value expansion opportunities across mobility, industrial storage, and smart infrastructure sectors. Sodium-ion battery pilots demonstrated nearly 14% lower raw material dependency compared to conventional lithium-ion systems, while AI-enabled battery management software improved energy optimization efficiency by approximately 18% in commercial deployments. Japan and South Korea are aggressively investing in solid-state battery ecosystems targeting faster charging performance and improved thermal stability for premium mobility applications. Simultaneously, India is expanding domestic battery assembly and recycling capacity through production-linked manufacturing initiatives supporting localized industrial ecosystems. Companies are strengthening competitive positioning through strategic technology licensing, automated giga-factory expansion, and closed-loop recycling infrastructure. An emerging strategic advantage involves integrating second-life battery systems into industrial energy storage networks, reducing operational energy costs while extending asset utilization cycles.

Long-term scalability of the secondary battery market depends on resolving integration complexity across energy infrastructure, manufacturing systems, and digital battery management platforms. More than 29% of industrial operators reported interoperability limitations between advanced battery storage systems and legacy grid infrastructure during large-scale deployment projects. Cybersecurity exposure linked to connected battery management software increased operational risk as smart energy ecosystems expanded across transportation and utility networks. Germany and the United States are facing workforce shortages in electrochemistry engineering and battery recycling operations, slowing specialized manufacturing scale-up and maintenance capabilities. Companies must address these barriers through advanced automation, cybersecurity investment, and specialized technical workforce development. A critical operational challenge involves balancing rapid capacity expansion with sustainability compliance, particularly as battery recycling regulations and carbon-traceability requirements become stricter across international manufacturing supply chains.

Localized Cell Manufacturing Expansion Battery manufacturers are restructuring supply chains through domestic giga-factory expansion and regional sourcing agreements as governments tighten critical mineral policies. The United States increased localized battery component production by 24% in 2026, while India accelerated cell assembly incentives supporting over 18% growth in domestic pack integration. Companies are reducing logistics exposure and import dependency through vertically integrated cathode processing and automated production lines, lowering operational lead times by nearly 15%.

AI-Driven Battery Optimization Systems Industrial operators are rapidly deploying AI-enabled battery management platforms to improve charging precision, thermal monitoring, and predictive maintenance. Smart battery analytics reduced energy loss rates by approximately 17% in commercial storage systems and improved battery lifespan by over 12% in fleet applications. South Korean manufacturers are integrating cloud-based diagnostics and digital twin modeling into advanced battery ecosystems to strengthen operational consistency and reduce maintenance downtime.

Recycling Infrastructure Scaling Rapidly Battery recycling has shifted from compliance activity to strategic raw material recovery infrastructure. Advanced recovery facilities in Germany and China achieved lithium and nickel recovery efficiency above 72%, helping manufacturers reduce virgin material dependency amid supply-chain volatility. Automotive and electronics companies are expanding closed-loop recycling partnerships to stabilize procurement costs, while automated dismantling systems improved material processing speed by nearly 20% during high-volume operations.

Shift Toward Alternative Chemistries Sodium-ion and solid-state battery development accelerated as manufacturers responded to lithium pricing instability and thermal safety pressures. Sodium-ion pilot deployments reduced raw material exposure by nearly 14%, while solid-state prototypes improved charging speed by approximately 30% compared to conventional lithium-ion configurations. Japanese battery producers and automotive OEMs are prioritizing long-duration storage partnerships and advanced electrolyte research to strengthen commercialization readiness for next-generation mobility and industrial storage systems.

Lithium-Ion Batteries remain the dominant segment due to superior energy density, scalability, and integration efficiency across electric mobility and industrial storage applications. More than 64% of newly deployed secondary battery systems in 2026 utilized lithium-ion chemistry because of faster charging capability and nearly 18% higher operational efficiency compared to Nickel-Metal Hydride Batteries. Solid-State Batteries represent the fastest-growing segment as automotive manufacturers prioritize thermal stability and ultra-fast charging for premium electric vehicles. Japanese and South Korean companies increased solid-state pilot investments by over 25% to strengthen commercialization readiness. Lead-Acid Batteries continue maintaining strategic relevance in low-cost backup power systems and industrial equipment because of established recycling infrastructure and lower upfront deployment costs. Nickel-Cadmium Batteries are experiencing declining adoption due to environmental restrictions, while Nickel-Metal Hydride Batteries retain selective demand in hybrid mobility applications. Companies are shifting R&D investments toward advanced lithium chemistry optimization, silicon-anode integration, and scalable solid-state manufacturing ecosystems.

Electric Vehicles represent the leading application segment as automotive electrification programs continue accelerating battery deployment intensity across passenger and commercial mobility platforms. More than 58% of global secondary battery consumption in 2026 was linked to electric vehicle manufacturing, supported by charging infrastructure modernization and stricter vehicle emission regulations. Renewable Energy Storage is emerging as the fastest-growing application as utilities integrate battery systems into renewable power balancing and peak-load stabilization networks. Industrial-scale renewable storage deployments increased by approximately 23% during recent grid modernization projects. Energy Storage Systems are also expanding rapidly across smart manufacturing and logistics operations seeking energy resilience and operational continuity. Consumer Electronics maintain stable demand through portable devices and wearable technology integration, while Telecommunications Backup systems remain operationally critical for uninterrupted network uptime. Companies are responding through automated pack manufacturing, modular battery architecture deployment, and strategic partnerships with utility operators and automotive OEMs.

Automotive remains the dominant end-user segment due to large-scale electric vehicle production, battery platform standardization, and continuous charging infrastructure expansion. Nearly 61% of advanced secondary battery deployments in 2026 were connected to automotive manufacturing and fleet electrification programs. Energy and Utilities is the fastest-growing end-user category as utilities expand battery-backed renewable integration and grid balancing infrastructure, with deployment activity increasing by approximately 27% across utility-scale storage projects. Industrial Manufacturing is strengthening adoption through automated warehouse systems and smart factory backup power integration to reduce operational disruptions. Telecommunications operators continue deploying secondary batteries to support 5G network continuity and remote tower reliability, while Aerospace and Defense sectors are increasing investments in lightweight high-density battery platforms for mission-critical applications. Electronics Industry demand remains stable through portable consumer devices and industrial electronics integration. Companies are targeting these segments through customized battery modules, long-term supply agreements, and vertically integrated manufacturing ecosystems.

Asia-Pacific accounted for the largest market share at 46% in 2025 however, North America is expected to register the fastest growth, expanding at a CAGR of 10.8% between 2026 and 2033.

Localized manufacturing and energy resilience expansion

North America is strengthening its position through accelerated battery localization, utility-scale energy storage deployment, and electric mobility infrastructure modernization. The United States and Canada increased domestic battery cell investments by over 28% during 2026 as automotive OEMs prioritized regional supply-chain security and reduced import dependency. Industrial energy storage installations expanded nearly 21% across logistics, manufacturing, and renewable integration projects. Companies are investing in lithium refining partnerships, recycling infrastructure, and AI-enabled battery management systems to improve operational continuity and procurement stability. Advanced manufacturing automation reduced battery assembly lead times by approximately 14%, supporting faster commercial deployment and large-scale fleet electrification initiatives.

United States Market Outlook: The United States continues leading North American secondary battery expansion through giga-factory development, federal clean-energy manufacturing incentives, and advanced grid modernization programs. Domestic battery manufacturing utilization improved by nearly 24% in 2026 as automotive companies accelerated electric vehicle platform integration and localized procurement agreements. Industrial operators are also increasing investment in utility-scale battery storage systems supporting renewable energy balancing and backup infrastructure resilience.

Regulatory-led sustainability transformation accelerating adoption

Europe remains a strategically important market due to aggressive decarbonization policies, advanced recycling infrastructure, and industrial electrification programs. Germany, France, and Sweden are expanding localized battery ecosystems to reduce dependence on imported battery materials and strengthen energy transition targets. More than 31% of newly commissioned industrial energy projects in Europe integrated advanced secondary battery storage systems during 2026. Battery recycling efficiency improvements exceeding 70% are helping manufacturers stabilize material procurement costs while supporting sustainability compliance requirements. Companies are prioritizing closed-loop manufacturing partnerships, renewable-powered giga-factory operations, and advanced solid-state battery pilot programs to strengthen long-term competitiveness.

Germany Market Outlook: Germany maintains strong operational leadership through automotive electrification, industrial automation, and battery recycling infrastructure expansion. More than 39% of large automotive suppliers in Germany increased battery-related production capacity during 2026 to support EV platform standardization and regional procurement requirements. The country also benefits from advanced engineering expertise, smart manufacturing integration, and strong policy alignment supporting low-emission industrial transformation.

Production scale and supply-chain integration dominance

Asia-Pacific leads the global secondary battery market through large-scale manufacturing capacity, vertically integrated supply chains, and rapid electric mobility adoption. China, Japan, and South Korea collectively control a substantial share of global cathode processing, lithium refining, and battery cell production activity. China alone contributed over 43% of global battery manufacturing capacity in 2026, supported by aggressive electric vehicle deployment and industrial energy storage integration. Japanese and South Korean enterprises are scaling solid-state battery research and premium high-density storage systems for automotive and aerospace applications. Companies continue prioritizing the region for cost-efficient production, component sourcing, and large-volume commercial deployment capabilities.

China Market Outlook: China remains the most influential country in the secondary battery market due to integrated mineral processing, advanced cell manufacturing ecosystems, and strong domestic EV demand. Electric vehicles represented more than 38% of total new vehicle sales in 2026, directly accelerating battery deployment volumes. The country also benefits from localized cathode supply chains, automated giga-factory operations, and strong industrial coordination between battery manufacturers, automotive OEMs, and energy storage developers.

Industrial electrification and mining integration growth

South America is emerging as a strategic market driven by mining-sector electrification, renewable energy integration, and gradual expansion of industrial battery infrastructure. Brazil and Chile are increasing deployment of secondary battery systems across utility-scale renewable projects and industrial backup applications. Battery-supported renewable storage capacity expanded by approximately 18% during 2026 as energy operators focused on grid reliability improvements. However, infrastructure limitations and dependence on imported battery components continue constraining rapid commercialization. Companies are responding through localized assembly partnerships, lithium supply agreements, and regional energy storage collaborations to improve operational accessibility and deployment efficiency.

Brazil Market Outlook: Brazil is strengthening its role through renewable energy integration, industrial automation growth, and expanding electric mobility infrastructure. More than 22% of newly developed renewable projects in Brazil integrated battery-backed storage systems in 2026 to improve grid stability and power continuity. The country also benefits from rising industrial electrification demand, government-backed clean-energy initiatives, and increasing enterprise investment in localized battery deployment capabilities.

Energy diversification and infrastructure modernization momentum

The Middle East & Africa market is gaining traction through smart infrastructure modernization, renewable energy diversification, and telecommunications network expansion. Saudi Arabia, the United Arab Emirates, and South Africa are increasing investments in battery-supported energy systems to strengthen grid resilience and industrial power continuity. Utility-scale battery storage deployments across the Gulf region increased by nearly 20% during 2026 as governments accelerated clean-energy transition initiatives. Telecommunications operators are also expanding advanced backup battery systems to support remote connectivity and digital infrastructure reliability. Companies are targeting the region through energy partnerships, localized service networks, and integrated battery deployment projects supporting industrial modernization strategies.

Saudi Arabia Market Outlook: Saudi Arabia is expanding secondary battery deployment through large-scale renewable energy programs, industrial diversification projects, and smart city infrastructure investments. Utility operators increased battery-backed renewable integration by approximately 19% during 2026 to improve power stability across high-demand industrial zones. The country’s long-term infrastructure modernization strategy, combined with growing electric mobility initiatives and energy diversification programs, continues attracting advanced battery technology providers and industrial energy partnerships.

China – 43% market share in the Secondary Battery market driven by integrated battery manufacturing capacity, strong EV adoption, and localized mineral processing infrastructure.

United States – 18% market share in the Secondary Battery market supported by giga-factory expansion, battery localization incentives, and accelerating utility-scale energy storage deployment.

CATL, LG Energy Solution, Panasonic, Samsung SDI, and BYD collectively control nearly 54% of the global secondary battery market, competing through production scale, battery chemistry innovation, and supply-chain integration. Chinese manufacturers compete aggressively against Japanese and South Korean technology leaders by reducing cell production costs nearly 16% through vertically integrated sourcing. Premium battery developers focus on fast-charging efficiency improvements exceeding 20%, while regional manufacturers prioritize customized industrial storage systems and localized delivery speed. Strategic partnerships with automotive OEMs, lithium refiners, and energy operators intensified during 2026. High capital requirements, mineral security pressures, and manufacturing automation capabilities remain major entry barriers. Winning requires scalable production, chemistry innovation, and supply-chain resilience.

CATL

LG Energy Solution

Panasonic Energy

Samsung SDI

BYD

SK On

Contemporary Amperex Technology

Toshiba Corporation

Hitachi Energy

GS Yuasa Corporation

Saft Groupe

EnerSys

Exide Industries

Amara Raja Energy & Mobility

Advanced lithium-ion chemistry continues dominating the secondary battery market through higher energy density, AI-enabled battery management systems, and fast-charging architecture integration. More than 68% of newly commissioned electric mobility platforms in 2026 integrated intelligent battery monitoring software that improved thermal efficiency by nearly 16% and reduced maintenance downtime by 11%. Compared with legacy nickel-cadmium systems, advanced lithium-iron-phosphate batteries deliver approximately 22% longer operational lifecycle and nearly 18% lower thermal management costs. Automotive OEMs and utility operators are scaling automated cell diagnostics and predictive charging systems to strengthen deployment reliability and optimize fleet-level energy utilization.

Emerging technologies between 2026 and 2028 are centered on sodium-ion chemistry, silicon-anode integration, and solid-state battery commercialization. Sodium-ion pilot deployments reduced raw material dependency by almost 14%, while solid-state prototypes improved charging speed by approximately 30% compared to conventional lithium-ion configurations. Japan and South Korea are aggressively expanding solid-state research alliances targeting premium electric mobility and aerospace storage systems. Companies adopting next-generation electrolyte technologies and modular battery architecture are gaining operational flexibility, lower cooling requirements, and improved safety performance under large-scale industrial workloads.

Disruptive innovation is increasingly driven by AI-assisted battery design, closed-loop recycling automation, and ultra-fast charging ecosystems. AI-based virtual battery modeling shortened development cycles by nearly 20% in commercial testing environments, while advanced recycling systems improved lithium recovery efficiency above 72%. Chinese manufacturers are strengthening competitive advantage through vertically integrated supply chains and sodium-ion industrialization, whereas North American enterprises are prioritizing localized giga-factory automation and battery recycling infrastructure. Companies acting now through technology partnerships, chemistry diversification, and digital energy integration will secure stronger long-term manufacturing resilience and deployment scalability.

April 2026 – CATL unveiled its third-generation Shenxing superfast-charging battery supporting 10%–98% charging within 6 minutes and 27 seconds, strengthening ultra-fast EV infrastructure competitiveness and high-performance mobility deployment strategies.

May 2026 – CATL and HyperStrong signed a 60GWh sodium-ion battery supply partnership, marking the world’s largest sodium-ion storage agreement and accelerating industrial-scale commercialization of alternative battery chemistry systems. Source: CATL

September 2025 – LG Energy Solution introduced North America-focused prismatic LFP battery prototypes and next-generation ESS platforms, strengthening localized value-chain integration and expanding advanced energy storage deployment flexibility across industrial applications. Source: LG Corporation

January 2026 – CATL received the World Economic Forum MINDS Award for AI-driven lithium-ion battery design technology, reducing battery development complexity and improving virtual performance optimization efficiency for commercial-scale manufacturing ecosystems. S

The Secondary Battery Market report provides comprehensive analysis across battery types, applications, end-users, operational technologies, and regional deployment patterns shaping industrial energy storage and electric mobility ecosystems between 2026 and 2033. The report evaluates Lithium-Ion Batteries, Solid-State Batteries, Lead-Acid Batteries, Nickel-Metal Hydride Batteries, and Nickel-Cadmium Batteries while covering applications including electric vehicles, renewable energy storage, telecommunications backup, industrial equipment, and consumer electronics. More than 60% of market demand concentration is analyzed through automotive electrification and utility-scale storage integration trends.

The study further examines enterprise expansion strategies, battery recycling infrastructure, localized manufacturing ecosystems, AI-enabled battery management technologies, and next-generation chemistry commercialization. Regional assessment covers Asia-Pacific, North America, Europe, South America, and Middle East & Africa with detailed operational insights into manufacturing hubs, supply-chain restructuring, and deployment scalability. The report supports strategic investment planning, technology benchmarking, partnership evaluation, and competitive positioning through analysis of production expansion, procurement security, infrastructure modernization, and evolving industrial battery adoption trends.

| Report Attribute/Metric | Report Details |

|---|---|

|

Market Revenue in 2025 |

USD 133292.48 Million |

|

Market Revenue in 2033 |

USD 275498.11 Million |

|

CAGR (2026 - 2033) |

9.5% |

|

Base Year |

2025 |

|

Forecast Period |

2026 - 2033 |

|

Historic Period |

2021 - 2025 |

|

Segments Covered |

By Type

By Application

By End-User

|

|

Key Report Deliverable |

Revenue Forecast, Growth Trends, Market Dynamics, Segmental Overview, Regional and Country-wise Analysis, Competition Landscape |

|

Region Covered |

North America, Europe, Asia-Pacific, South America, Middle East, Africa |

|

Key Players Analyzed |

CATL, LG Energy Solution, Panasonic Energy, Samsung SDI, BYD, SK On, Contemporary Amperex Technology, Toshiba Corporation, Hitachi Energy, GS Yuasa Corporation, Saft Groupe, EnerSys, Exide Industries, Amara Raja Energy & Mobility |

|

Customization & Pricing |

Available on Request (10% Customization is Free) |