Reports

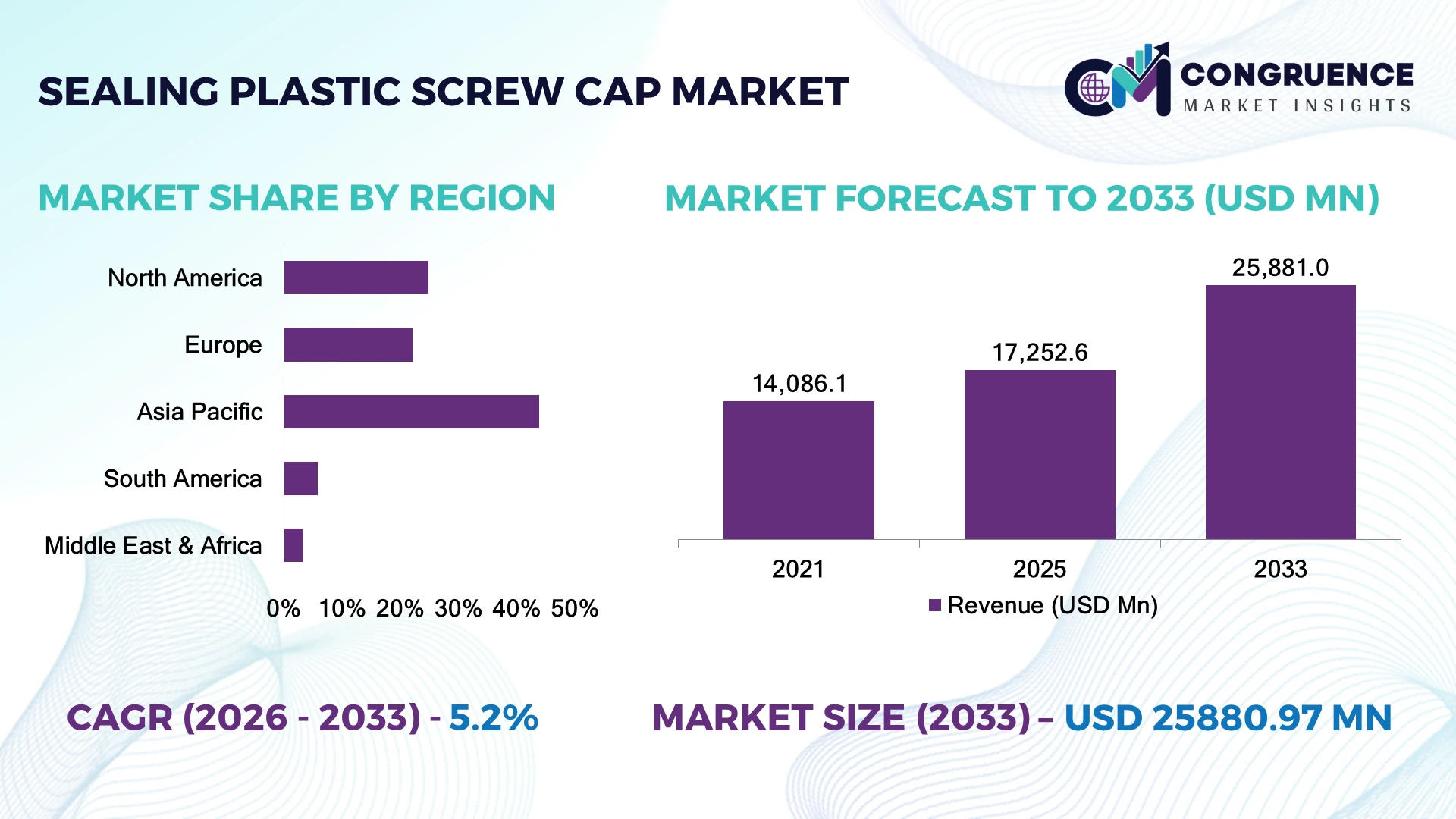

The Global Sealing Plastic Screw Cap Market was valued at USD 17,252.6 Million in 2025 and is anticipated to reach a value of USD 25,881.0 Million by 2033 expanding at a CAGR of 5.2% between 2026 and 2033. Growth is driven by rising demand for lightweight, tamper-evident packaging, recyclable closures, and high-speed filling lines across beverage, pharmaceutical, and personal care manufacturing.

China leads the global market with approximately 31% production capacity, supported by large-scale beverage packaging, pharmaceutical manufacturing, and investments in automated injection molding. Smart manufacturing has improved production efficiency by nearly 22%, while India continues expanding rapidly through packaging capacity additions for FMCG exports. Amid ongoing global supply-chain diversification after Red Sea shipping disruptions, manufacturers are strengthening regional production networks and recycled resin integration to improve supply resilience.

Companies securing sustainable resin supply, advanced closure technologies, and automated manufacturing capabilities will strengthen long-term competitive positioning.

Market Size & Growth: USD 17,252.6 Million in 2025 reaching USD 25,881.0 Million by 2033 at 5.2% CAGR, driven by sustainable packaging adoption.

Top Growth Drivers: Recyclable packaging 39%, beverage packaging 34%, pharmaceutical closures 27%.

Short-Term Forecast: By 2028, automated capping reduces packaging defects by 18% and line efficiency improves 15%.

Emerging Technologies: AI inspection, lightweight closure design, digital molding improve consistency and reduce resin consumption.

Regional Leaders: Asia-Pacific leads, North America advances premium closures, Europe accelerates recycled-content adoption.

Consumer/End-User Trends: Nearly 58% of FMCG brands prioritize recyclable and lightweight closure solutions.

Pilot/Case Example: 2026 lightweight cap deployment lowered plastic consumption by 14% without compromising seal integrity.

Competitive Landscape: Top suppliers collectively control approximately 42% share through innovation and global manufacturing.

Regulatory & ESG Impact: Recycled polymer usage increased by 23% following stricter packaging sustainability regulations.

Investment & Funding: More than USD 1.3 Billion supports automated molding, recycling, and regional production expansion.

Innovation & Future Outlook: Smart tamper-evident closures and tethered cap technologies reshape advanced packaging strategies.

The Sealing Plastic Screw Cap Market is evolving through lightweight closure engineering, recycled polymer integration, and precision molding technologies serving beverages, pharmaceuticals, food, and personal care packaging. Approximately 46% of new product launches emphasize recyclable material compatibility as manufacturers adapt to stricter packaging regulations and resilient regional supply chains, setting the stage for broader strategic transformation.

The Sealing Plastic Screw Cap Market has become strategically important as packaging manufacturers balance sustainability targets, product safety, and production efficiency. Regulations promoting recyclable packaging and extended producer responsibility are accelerating investment in lightweight closures, tethered caps, and recycled polymer processing. Global brand owners increasingly prioritize packaging standardization to improve supply-chain flexibility while reducing material intensity.

Advanced compression molding and AI-assisted quality inspection deliver approximately 20% higher production efficiency than conventional molding systems while lowering defect rates by nearly 16%. Europe leads sustainable closure innovation through recycled-content integration, whereas Asia-Pacific dominates manufacturing scale with expanding beverage, pharmaceutical, and FMCG packaging capacity. Over the next two to three years, automated inspection systems are expected to exceed 60% deployment among large-scale packaging facilities, improving throughput and consistency.

Manufacturers are expanding regional molding operations, partnering with recycled resin suppliers, and investing in digital manufacturing platforms to strengthen supply resilience. For example, beverage packaging producers increasingly deploy tethered cap designs alongside lightweight closures to meet evolving packaging requirements without disrupting filling operations. Companies combining sustainable material innovation, manufacturing automation, and high-performance sealing technologies will secure stronger competitive positioning and long-term operational advantage.

Demand for sealing plastic screw caps is accelerating as beverage, pharmaceutical, and personal care manufacturers adopt lightweight, tamper-evident packaging compatible with high-speed production. Nearly 61% of bottled beverage packaging now relies on plastic screw closures, while lightweight cap designs reduce polymer consumption by approximately 14–18%. The European Union's tethered-cap packaging requirements have accelerated product redesign and automation investments across global packaging facilities. This regulatory shift is driving manufacturers to upgrade injection-compression molding systems and digital inspection technologies. Companies are expanding production capacity, investing in recycled resin compatibility, and partnering with FMCG brands to develop next-generation closures. A key strategic advantage now lies in integrating sustainable material innovation with high-output manufacturing without compromising sealing performance or line efficiency.

Volatility in polypropylene and HDPE prices continues to pressure profitability across the sealing plastic screw cap value chain, with resin accounting for nearly 55% of total manufacturing costs. Compliance with recycled-content and food-contact regulations requires additional validation, increasing production qualification time by approximately 12%. Supply disruptions affecting specialty additives and food-grade polymers have challenged manufacturers in China and Europe, impacting delivery schedules for premium closure products. Companies are mitigating these risks through localized resin sourcing, long-term procurement contracts, and greater use of mechanically recycled polymers where regulations permit. Operational resilience increasingly depends on balancing raw material flexibility with consistent closure quality and regulatory compliance across multiple packaging sectors.

Smart packaging integration creates new opportunities beyond conventional sealing performance. Intelligent screw caps incorporating QR authentication, NFC tracking, and tamper verification can improve supply-chain visibility by nearly 20%, while advanced lightweight designs reduce packaging weight by approximately 16%. Japan and Germany are accelerating investment in digital packaging technologies alongside chemically recycled polymers suitable for food-contact applications. Manufacturers are expanding R&D around mono-material closures, digital watermarking, and AI-optimized mold design to strengthen circular packaging ecosystems. An emerging strategic opportunity lies in combining connected packaging with sustainable closure engineering, enabling consumer engagement, product authentication, and regulatory compliance within a single packaging solution.

Maintaining consistent sealing performance while increasing recycled content remains a significant execution challenge. Closure systems using recycled polymers can exhibit dimensional variation exceeding 8% unless molding parameters are tightly controlled, while global manufacturers report quality inspection workloads increasing by approximately 15% during material transitions. Diverse recycling standards and packaging specifications across major export markets complicate production standardization. Companies must invest in advanced process monitoring, AI-enabled vision inspection, and precision tooling to ensure consistent torque, leakage resistance, and product safety. Long-term competitiveness depends on developing manufacturing systems capable of delivering sustainable closures at industrial scale without sacrificing filling-line compatibility or operational reliability.

Lightweight Closure Engineering Lightweight cap designs now reduce plastic consumption by 15–20% while maintaining sealing integrity. Nearly 48% of newly introduced beverage closures emphasize resin optimization to lower packaging weight and transportation costs. Manufacturers are redesigning molds, upgrading compression molding equipment, and collaborating with beverage producers to improve sustainability without affecting high-speed bottling performance.

Tethered Cap Adoption Accelerates Packaging regulations are driving rapid adoption of tethered plastic screw caps, with implementation exceeding 65% across new beverage packaging programs targeting regulated markets. Manufacturers are restructuring production lines and investing in new tooling platforms to support compliant closure designs while minimizing operational disruption and preserving filling efficiency during large-scale packaging transitions.

Automation Enhances Quality Control AI-enabled optical inspection systems now improve defect detection accuracy by approximately 25% while reducing manual inspection requirements by nearly 30%. Automated molding analytics optimize cavity performance and reduce scrap generation. Packaging companies are scaling smart manufacturing platforms to improve consistency, shorten production cycles, and strengthen supply reliability across global packaging operations.

Recycled Polymer Integration Expands Food-grade recycled polymer utilization has increased by approximately 22% within premium closure manufacturing programs as circular packaging initiatives gain momentum. Manufacturers are forming strategic resin partnerships, qualifying advanced recycled materials, and investing in precision processing technologies. A notable shift is the simultaneous optimization of sustainability targets and closure performance rather than treating them as competing priorities.

Continuous Thread (CT) caps accounted for approximately 47.8% of the Sealing Plastic Screw Cap Market in 2025 due to their compatibility with high-speed bottling, dependable resealability, and broad use across beverage, food, pharmaceutical, and personal care packaging. Their standardized dimensions simplify integration with automated filling lines and reduce packaging downtime by nearly 15%. Tethered caps are the fastest-growing segment as sustainability regulations reshape beverage packaging, particularly across Europe. Child-resistant caps continue expanding in pharmaceutical packaging where regulatory compliance is essential, while tamper-evident and dispensing screw caps retain strong demand in food and personal care applications requiring product safety and controlled dispensing.

Manufacturers are investing in lightweight CT closures, tethered-cap tooling, and mono-material designs to improve recyclability and production efficiency. Around 34% of new closure development programs emphasize sustainable designs that reduce resin usage without compromising sealing performance. Investment priorities continue shifting toward regulatory-compliant closures with digital manufacturing capabilities and advanced molding precision.

According to findings released by the European Plastics Converters association during 2025, beverage packaging manufacturers accelerated conversion toward tethered plastic closures following implementation of new packaging compliance requirements across European markets.

Beverage packaging represented approximately 44.9% of global demand in 2025, supported by high production volumes for bottled water, carbonated drinks, dairy beverages, and edible oils. High-speed bottling operations rely on precision-molded screw caps to maintain seal integrity and production efficiency. Pharmaceutical packaging is the fastest-growing application as stricter drug safety regulations increase adoption of tamper-evident and child-resistant closures. Food packaging maintains stable growth through sauces, condiments, and packaged ingredients, while personal care and household chemicals increasingly adopt dispensing closures that improve consumer convenience and reduce product waste.

Companies are expanding application-specific product portfolios through lightweight closures, improved liner technologies, and automation-compatible cap designs. Nearly 41% of packaging investments now target application-specific customization, enabling stronger product differentiation and greater filling-line compatibility across multiple consumer industries. Demand continues shifting toward premium closures combining sustainability with enhanced functionality.

Based on a 2025 enterprise packaging survey conducted by PMMI, beverage manufacturers ranked closure compatibility and filling-line efficiency among the highest priorities for new packaging equipment investments, reinforcing demand for advanced screw cap technologies.

Beverage manufacturers accounted for approximately 42.6% of total demand in 2025 owing to continuous high-volume bottling operations, standardized packaging formats, and extensive deployment of automated capping systems. Pharmaceutical companies represent the fastest-growing end-user segment as regulatory compliance, counterfeit prevention, and patient safety increase demand for child-resistant and tamper-evident closures. Food processors continue investing in improved shelf-life packaging, while personal care manufacturers increasingly prioritize premium dispensing systems. Household chemical producers maintain consistent demand for leak-resistant screw caps supporting safe transportation and consumer handling.

Manufacturers are tailoring closure designs through customer-specific tooling, sustainable resin selection, and collaborative packaging development. Approximately 37% of new commercial contracts involve customized closure specifications for major brand owners, reflecting a strategic shift toward value-added packaging rather than standardized commodity products. Companies strengthening co-development capabilities and regional manufacturing footprints are securing long-term supply agreements with leading consumer goods producers.

According to a 2025 industry assessment published by PMMI, more than 70% of consumer packaged goods manufacturers identified packaging automation and closure reliability among their highest operational priorities when upgrading filling and packaging lines.

Asia-Pacific accounted for the largest market share at 43.8% in 2025 however, Middle East & Africa is expected to register the fastest growth, expanding at a CAGR of 6.4% between 2026 and 2033.

Strong automation and sustainable packaging investments strengthen manufacturing leadership

North America represented approximately 24.9% of the global Sealing Plastic Screw Cap Market in 2025, supported by highly automated beverage, pharmaceutical, and personal care packaging industries. Manufacturers continue replacing conventional closures with lightweight, recyclable screw caps compatible with high-speed filling systems. More than 72% of large packaging plants now operate automated inspection and capping technologies, improving throughput and reducing production waste. Investments in food-grade recycled resin processing and advanced injection-compression molding are strengthening domestic production capabilities. Strategic partnerships between packaging converters and major consumer goods companies are accelerating commercialization of tethered and lightweight closure solutions while enhancing regional supply resilience.

United States Market Outlook: The United States remains the regional leader through its extensive beverage bottling infrastructure, advanced pharmaceutical packaging industry, and large consumer goods manufacturing base. More than 65% of regional closure production supports beverage and food applications, while continuous investment in digital manufacturing, precision tooling, and recycled polymer processing enables manufacturers to improve efficiency, reduce material consumption, and strengthen domestic packaging supply chains.

Regulatory compliance drives sustainable closure transformation

Europe accounted for approximately 22.1% of global demand, driven by strict packaging sustainability regulations and widespread adoption of recyclable closure technologies. Beverage manufacturers are rapidly transitioning toward tethered screw caps and lightweight packaging to improve recyclability while maintaining filling-line performance. Nearly 58% of new closure production programs emphasize recycled-content compatibility and mono-material packaging solutions. Packaging companies continue modernizing molding operations and expanding precision manufacturing capacity to meet evolving regulatory requirements while supporting circular economy objectives across food, beverage, and pharmaceutical sectors.

Germany Market Outlook: Germany leads the European market through advanced plastics processing, precision tooling expertise, and strong beverage packaging production. High investment in automated molding equipment and sustainable packaging innovation supports large-scale manufacturing efficiency. Domestic producers continue developing lightweight closures and recycled polymer-compatible designs while collaborating closely with FMCG and pharmaceutical companies to accelerate commercialization of compliant packaging solutions.

Manufacturing scale and export competitiveness reinforce regional dominance

Asia-Pacific contributed approximately 43.8% of the global market in 2025, supported by extensive packaging manufacturing ecosystems across beverages, pharmaceuticals, edible oils, and personal care products. China, India, and Southeast Asia continue expanding high-speed molding capacity to serve domestic consumption and export demand. More than 31% of global closure production originates from China alone, while automated manufacturing has improved production efficiency by approximately 22%. Regional manufacturers increasingly integrate lightweight materials, digital quality control, and automated assembly to strengthen competitiveness and support multinational packaging supply chains.

China Market Outlook: China remains the largest production hub owing to its integrated plastics supply chain, large beverage packaging industry, and advanced injection molding infrastructure. Continuous investment in intelligent manufacturing, recycled polymer processing, and export-oriented packaging facilities enables domestic manufacturers to deliver high-volume, cost-efficient screw caps while improving product consistency for international consumer goods brands.

Food and beverage packaging expansion supports steady demand

South America accounted for approximately 5.8% of the global market, with demand driven primarily by beverage bottling, edible oil packaging, and expanding processed food industries. Packaging manufacturers continue upgrading production lines with automated capping equipment to improve operational efficiency and reduce material waste. Regional growth remains supported by investment in consumer goods manufacturing, although resin price volatility and logistics infrastructure continue influencing production economics. Companies increasingly localize closure manufacturing to improve supply reliability and reduce dependence on imported packaging components.

Brazil Market Outlook: Brazil represents the largest regional market through its extensive beverage industry, food processing sector, and established plastics manufacturing base. Packaging companies continue expanding domestic molding capacity and introducing lightweight closure technologies compatible with high-speed bottling systems. Growing investment in recycled plastics processing and regional manufacturing strengthens long-term competitiveness while improving packaging supply resilience.

Industrial diversification accelerates modern packaging investments

Middle East & Africa represented approximately 3.4% of the global market in 2025 while recording the fastest projected expansion through increasing food processing, pharmaceutical manufacturing, and bottled beverage production. Governments continue supporting industrial diversification through investments in packaging infrastructure and domestic manufacturing. Advanced molding equipment, automated production lines, and modern recycling facilities are improving operational capabilities. Regional packaging companies increasingly establish partnerships with multinational consumer goods manufacturers to expand local closure production and reduce import dependency.

Saudi Arabia Market Outlook: Saudi Arabia leads regional development through significant investment in food processing, pharmaceutical manufacturing, and industrial packaging infrastructure under national industrial diversification initiatives. Modern plastics conversion facilities continue expanding production capacity for high-quality sealing closures, while increasing adoption of automated molding technologies strengthens domestic manufacturing capability and reduces reliance on imported packaging products.

Global packaging leaders including Berry Global, BERICAP, AptarGroup, Silgan Closures, and Closure Systems International compete against regional closure manufacturers serving food, beverage, and pharmaceutical markets. The top five companies collectively account for approximately 46% of global market share. Competition centers on lightweight engineering, tethered-cap compliance, and manufacturing efficiency rather than price alone. Lightweight closures reduce resin consumption by 12–18%, while AI-enabled inspection improves defect detection by nearly 25% and automated compression molding increases production efficiency by approximately 20%. Companies compete through regional capacity expansion, recycled-resin partnerships, vertical integration with packaging converters, and rapid commercialization of mono-material closures. The competitive landscape is shifting toward sustainability-led innovation as regulatory compliance increasingly determines supplier selection. High tooling investment, food-contact certification, and precision molding capabilities create significant entry barriers for new manufacturers. Success depends on combining advanced closure design, scalable automated production, sustainable material expertise, and dependable global supply capabilities that consistently meet evolving packaging regulations.

Berry Global

BERICAP

AptarGroup

Silgan Closures

Closure Systems International

UNITED CAPS

Guala Closures

Weener Plastics

Georg MENSHEN

Pact Group

Nippon Closures Co., Ltd.

ALPLA Group

Manufacturers are advancing sealing plastic screw cap production through high-speed compression molding, AI-powered vision inspection, and lightweight engineering. Approximately 64% of newly installed closure production lines now integrate automated optical quality inspection, reducing defect rates by nearly 24%. Digital mold monitoring improves dimensional consistency while predictive maintenance minimizes unplanned downtime, enabling higher productivity and lower operating costs across beverage, food, and pharmaceutical packaging.

Emerging technologies include tethered-cap engineering, mono-material closure architecture, digital watermark compatibility, and food-grade recycled resin processing. Compared with conventional injection-molded closures, modern lightweight compression-molded designs reduce material consumption by approximately 16% while maintaining equivalent sealing performance. Nearly 42% of premium closure programs now prioritize PCR-compatible designs to satisfy sustainability requirements. Companies with integrated resin sourcing, precision tooling, and automation capabilities gain stronger operational advantages through faster commercialization and improved regulatory compliance.

Between 2026 and 2028, AI-driven process optimization, advanced polymer formulations, and smart authentication features will reshape product differentiation. QR-enabled traceability, anti-counterfeit technologies, and intelligent closure inspection will strengthen supply-chain transparency. Manufacturers investing in automated molding, recyclable material innovation, and digital production systems will improve manufacturing flexibility, reduce operational costs, and secure stronger partnerships with global consumer goods companies as sustainable packaging requirements continue expanding.

April 2024: Berry Global introduced new lightweight screw closures for protein powder packaging, reducing closure weight by up to 33% while supporting food-contact PCR compatibility. The innovation lowers material consumption and strengthens sustainable packaging performance. Source: berryglobal.com

September 2024: Berry Global launched the recyclable Pical tamper-evident pouring closure for edible oils and sauces using a mono-material HDPE design, improving recyclability while eliminating secondary tamper sleeves. Source: berryglobal.com

July 2025: BERICAP expanded its Drinktec portfolio with industrialized sport caps, lightweight closures, and dairy tethered-cap solutions supporting mandatory European beverage closure regulations. The portfolio covers 100% of major beverage neck finishes. Source: bericap.com

March 2025: Amcor and Berry Global received regulatory clearance supporting their strategic combination, accelerating innovation, manufacturing integration, and circular packaging capabilities with targeted annual synergies of approximately USD 650 million. Source: Packaging industry market intelligence.

This report delivers comprehensive analysis of the Sealing Plastic Screw Cap Market across closure types, material technologies, applications, end-user industries, and regional demand patterns. It evaluates continuous thread, tethered, child-resistant, tamper-evident, and dispensing closures used throughout beverage, food, pharmaceutical, personal care, and household packaging. The study also examines manufacturing technologies, lightweight engineering, recycled polymer integration, and intelligent production systems influencing product development and operational competitiveness.

The report assesses deployment trends across North America, Europe, Asia-Pacific, South America, and the Middle East & Africa, supported by quantitative evaluation of segment shares, production concentration, enterprise adoption, and technology penetration. Competitive benchmarking covers leading manufacturers, product innovation, capacity expansion, and sustainability strategies to support investment planning, market entry, product positioning, supply-chain optimization, and long-term business expansion between 2026 and 2033.

| Report Attribute/Metric | Report Details |

|---|---|

|

Market Revenue in 2025 |

USD 17,252.6 Million |

|

Market Revenue in 2033 |

USD 25,881.0 Million |

|

CAGR (2026 - 2033) |

5.2% |

|

Base Year |

2025 |

|

Forecast Period |

2026 - 2033 |

|

Historic Period |

2021 - 2025 |

|

Segments Covered |

By Type

By Application

By End-User

|

|

Key Report Deliverable |

Revenue Forecast, Growth Trends, Market Dynamics, Segmental Overview, Regional and Country-wise Analysis, Competition Landscape |

|

Region Covered |

North America, Europe, Asia-Pacific, South America, Middle East, Africa |

|

Key Players Analyzed |

Berry Global, BERICAP, AptarGroup, Silgan Closures, Closure Systems International, UNITED CAPS, Guala Closures, Weener Plastics, Georg MENSHEN, Pact Group, Nippon Closures Co., Ltd., ALPLA Group |

|

Customization & Pricing |

Available on Request (10% Customization is Free) |