Reports

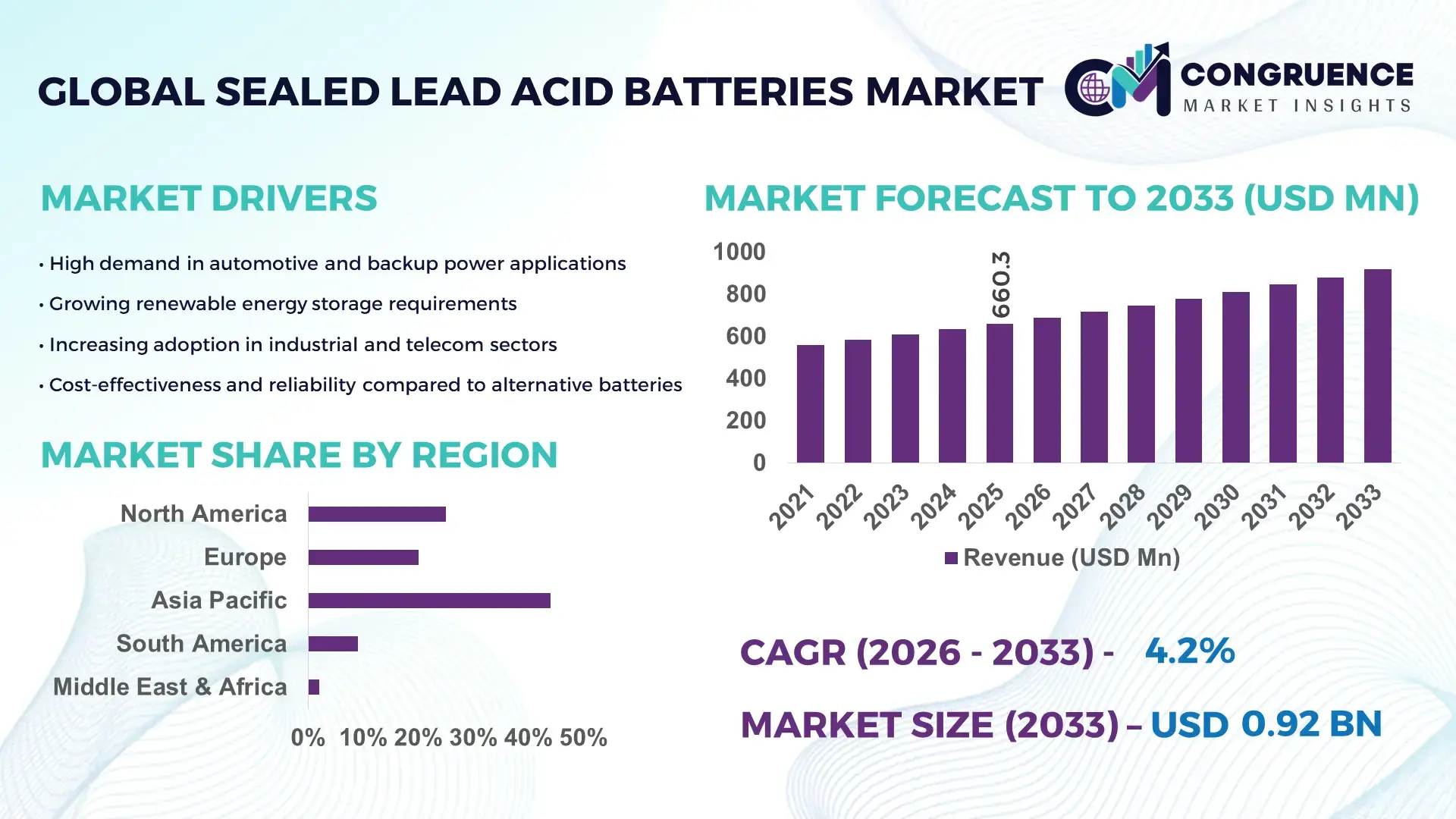

The Global Sealed Lead Acid Batteries Market was valued at USD 660.25 Million in 2025 and is anticipated to reach a value of USD 917.59 Million by 2033 expanding at a CAGR of 4.2% between 2026 and 2033. Rising demand for reliable, low-maintenance energy storage solutions across automotive, telecom, UPS, and renewable backup applications continues to support steady market expansion.

China remains the dominant country in the sealed lead acid batteries market, supported by its extensive manufacturing ecosystem and vertically integrated lead supply chain. The country operates more than 2,000 battery manufacturing facilities, with an annual production capacity exceeding 300 million units across automotive, telecom, and industrial segments. Investment in advanced AGM and gel battery technologies has increased by over 15% annually since 2023, driven by telecom tower installations and electric two-wheeler demand. China’s automotive battery production surpasses 80 million units annually, while domestic consumption in backup power and mobility applications accounts for nearly 60% of its total output. Continuous modernization of recycling infrastructure enables recovery rates above 95%, reinforcing supply stability and cost competitiveness in the global sealed lead acid batteries industry.

Market Size & Growth: Valued at USD 660.25 Million in 2025, projected to reach USD 917.59 Million by 2033 at a CAGR of 4.2%, driven by expanding telecom infrastructure and backup power demand.

Top Growth Drivers: Telecom tower expansion 18%, UPS installations growth 22%, automotive replacement demand 15%.

Short-Term Forecast: By 2028, production efficiency is expected to improve by 12% and average battery lifecycle performance by 10% through advanced plate design optimization.

Emerging Technologies: Adoption of AGM technology, carbon-enhanced lead electrodes, and smart battery monitoring systems integrated with IoT platforms.

Regional Leaders: Asia-Pacific projected at USD 420 Million by 2033 with strong telecom adoption; North America at USD 210 Million driven by data center expansion; Europe at USD 165 Million supported by renewable backup integration.

Consumer/End-User Trends: Automotive aftermarket users account for over 40% of demand, while telecom and UPS sectors show rising preference for maintenance-free VRLA batteries.

Pilot or Case Example: In 2024, a telecom infrastructure project in Southeast Asia achieved 14% downtime reduction using advanced AGM sealed lead acid batteries.

Competitive Landscape: Clarios holds approximately 20% share, followed by GS Yuasa, Exide Industries, East Penn Manufacturing, and EnerSys.

Regulatory & ESG Impact: Stricter battery recycling mandates and carbon reduction policies are accelerating closed-loop manufacturing and sustainable lead recovery systems.

Investment & Funding Patterns: Over USD 1.1 Billion invested globally since 2023 in capacity expansion, automation upgrades, and recycling modernization initiatives.

Innovation & Future Outlook: Integration with hybrid energy storage systems and microgrid applications, alongside cost-efficient carbon additives, is shaping the next phase of market evolution.

The sealed lead acid batteries market is structurally supported by automotive starting, lighting, and ignition systems contributing nearly 45% of global demand, followed by telecom and UPS applications at approximately 30%, and industrial backup systems representing around 15%. Recent product innovations include high-rate discharge AGM batteries, deep-cycle gel variants for renewable storage, and enhanced grid alloy formulations that extend cycle life by up to 20%. Environmental regulations mandating responsible lead recycling and extended producer responsibility programs are strengthening sustainable manufacturing practices. Asia-Pacific accounts for over half of global consumption, while North America and Europe demonstrate stable replacement-driven growth. Emerging trends such as integration with solar microgrids, rising demand from data centers, and cost-competitive energy storage for off-grid applications are expected to create long-term opportunities for manufacturers and investors.

The strategic relevance of the Sealed Lead Acid Batteries Market lies in its role as a dependable, cost-efficient backbone for critical backup power, automotive ignition systems, telecom towers, and industrial UPS infrastructure. Despite the rise of lithium-based chemistries, sealed lead acid batteries remain indispensable in applications requiring proven safety, robust temperature tolerance, and mature recycling ecosystems exceeding 95% material recovery rates. Advanced Absorbent Glass Mat (AGM) technology delivers up to 18% longer cycle life compared to conventional flooded lead acid batteries, while carbon-enhanced lead plates improve charge acceptance by nearly 25% over older grid designs.

Asia-Pacific dominates in production volume, while North America leads in adoption with over 65% of data center and telecom enterprises utilizing valve-regulated lead acid (VRLA) systems for standby applications. By 2028, AI-enabled battery monitoring systems are expected to reduce unexpected downtime in telecom infrastructure by 15% through predictive maintenance analytics. Firms are committing to ESG performance improvements such as 20% reduction in manufacturing emissions and 98% closed-loop recycling rates by 2030. In 2024, a major Indian battery manufacturer achieved a 12% improvement in production efficiency through automation and smart quality-control integration. As infrastructure electrification accelerates globally, the Sealed Lead Acid Batteries Market is positioned as a pillar of resilience, regulatory compliance, and sustainable industrial growth.

The rapid expansion of telecom towers and hyperscale data centers significantly drives the Sealed Lead Acid Batteries Market. More than 7 million telecom towers operate globally, with Asia accounting for nearly 45% of installations, each requiring reliable VRLA battery backup. Data centers demand uninterrupted power supply systems capable of delivering high discharge rates within milliseconds during grid failure. AGM sealed lead acid batteries offer proven reliability and cost advantages, making them a preferred solution for over 60% of mid-sized facilities. Furthermore, 5G deployment has increased backup capacity requirements by approximately 20% per site due to higher energy consumption. The need for grid stabilization and mission-critical uptime continues to sustain strong procurement volumes across telecom and IT infrastructure segments.

The growing adoption of lithium-ion battery systems presents competitive pressure on the Sealed Lead Acid Batteries Market. Lithium-ion solutions provide up to 40% higher energy density and nearly 30% longer operational lifespan compared to traditional VRLA batteries. Declining lithium-ion pack prices, which have fallen by more than 80% over the past decade, have narrowed the cost differential in certain stationary storage applications. Additionally, lithium-ion systems require up to 50% less physical space for equivalent capacity, creating advantages in urban data centers. As sustainability frameworks emphasize lower lifecycle emissions, some enterprises are transitioning to lithium-based chemistries for large-scale energy storage projects, limiting expansion opportunities in specific high-growth segments.

Renewable energy expansion and decentralized microgrid installations create measurable opportunities for the Sealed Lead Acid Batteries Market. Off-grid solar installations exceeded 500 million units globally, many requiring cost-effective storage solutions for rural electrification. Deep-cycle gel batteries offer durable cycling performance and tolerance to high ambient temperatures, making them suitable for developing regions. Hybrid energy systems combining solar panels with VRLA batteries can reduce diesel generator dependency by up to 35%. Additionally, emerging markets in Africa and Southeast Asia are investing heavily in community microgrids, where initial capital cost sensitivity favors sealed lead acid technology. These applications support broader electrification goals while maintaining manageable upfront investment requirements.

Volatility in lead prices and tightening environmental regulations create structural challenges for the Sealed Lead Acid Batteries Market. Lead constitutes nearly 60–70% of total battery weight, making production highly sensitive to commodity price fluctuations. In recent years, lead price swings of more than 15% within short periods have affected procurement strategies and inventory planning. Additionally, stricter hazardous waste handling rules and emission control requirements demand capital investment in filtration, recycling, and compliance systems. Manufacturing facilities must allocate significant budgets toward environmental monitoring and worker safety programs. These cost pressures, combined with competition from alternative chemistries, necessitate operational efficiency and technological innovation to maintain profitability and regulatory alignment.

• Rapid Expansion of AGM Technology Adoption: Absorbent Glass Mat (AGM) batteries now account for nearly 48% of total sealed lead acid battery installations in telecom and UPS applications. AGM variants offer up to 20% longer service life and 15% faster recharge capability compared to conventional flooded systems. Industrial facilities are increasingly specifying AGM batteries due to their spill-proof design and vibration resistance, particularly in high-density data centers where downtime tolerance is below 1%. This transition is also reducing maintenance intervention frequency by approximately 25%, improving operational reliability across mission-critical infrastructure.

• Surge in Telecom Tower Backup Modernization: Global telecom operators are upgrading over 30% of existing tower sites with advanced VRLA battery banks to support 5G deployment. Power consumption per 5G site is 18–25% higher than 4G infrastructure, increasing demand for higher-capacity sealed lead acid batteries. In emerging Asian markets, more than 40% of rural telecom towers now rely on hybrid solar-VRLA configurations, cutting diesel generator runtime by nearly 35%. This modernization trend is reinforcing stable procurement cycles and strengthening demand for high-rate discharge batteries with extended float life performance.

• Strengthening Closed-Loop Recycling and ESG Compliance: Recycling rates for lead in sealed lead acid batteries exceed 95%, making them among the most recycled consumer products globally. Over 70% of manufacturers have implemented automated smelting and emission control systems to reduce particulate emissions by 20% since 2023. Regulatory mandates in Europe require up to 85% material recovery efficiency, prompting manufacturers to invest in advanced refining technologies. These sustainability-driven upgrades are lowering raw material dependency by nearly 30% through reclaimed lead utilization, reinforcing supply chain resilience and ESG alignment.

• Integration of Smart Battery Monitoring Systems: Approximately 35% of newly installed industrial sealed lead acid battery systems now incorporate IoT-enabled monitoring modules. Predictive analytics tools are reducing unexpected battery failures by 15% and extending operational lifespan by nearly 10%. In large-scale UPS installations exceeding 500 kVA capacity, real-time thermal and voltage monitoring has improved maintenance scheduling accuracy by 22%. The growing adoption of intelligent battery management platforms is enhancing asset visibility and supporting proactive performance optimization across telecom, healthcare, and data center environments.

The Sealed Lead Acid Batteries Market is comprehensively segmented by type, application, and end-user, reflecting diversified demand patterns across automotive, telecom, industrial, and infrastructure ecosystems. By type, Absorbent Glass Mat (AGM), Gel, and conventional flooded sealed batteries address varying performance and cost requirements. By application, automotive starting, lighting, and ignition (SLI) systems represent the largest installed base due to recurring replacement cycles across more than 1.4 billion vehicles globally, while telecom and UPS systems form a substantial share driven by uninterrupted power needs. Renewable energy storage and industrial backup applications further strengthen market depth, particularly in regions with unstable grid networks. From an end-user perspective, automotive manufacturers and aftermarket distributors dominate procurement volumes, while telecom operators, data center companies, and industrial enterprises maintain steady institutional demand. This segmentation highlights a structurally balanced market supported by both high-volume consumer replacement and mission-critical infrastructure investments.

Absorbent Glass Mat (AGM) batteries currently account for approximately 46% of total sealed lead acid battery adoption, while Gel batteries hold nearly 28% and conventional flooded sealed variants represent about 16%; however, carbon-enhanced AGM configurations are expanding fastest at a CAGR of 5.6% through 2033 due to 20% higher charge acceptance and nearly 18% longer service life compared to older flooded standards. AGM batteries lead because of low internal resistance, vibration tolerance, and spill-proof construction suitable for telecom towers and data centers where downtime tolerance is below 1%. Gel batteries are increasingly deployed in renewable and off-grid installations where temperature resilience improves cycle durability by around 15%, while flooded sealed types remain relevant in cost-sensitive automotive and light industrial applications; collectively, these non-AGM segments contribute roughly 54% of installations.

Automotive SLI applications represent nearly 44% of global sealed lead acid battery utilization, while telecom backup accounts for around 26%, yet UPS and data center installations are rising fastest at a CAGR of 6.1% through 2033 supported by double-digit growth in hyperscale computing facilities. Automotive leadership stems from replacement intervals averaging 3–5 years across a global vehicle parc exceeding 1.4 billion units, ensuring consistent volume turnover. Telecom installations are expanding as 5G infrastructure increases per-site power consumption by 18–25%, prompting larger VRLA battery banks, while healthcare and financial institutions rely heavily on high-rate discharge AGM systems to secure operational continuity. Renewable storage and mobility equipment collectively represent approximately 30% of total installations, benefiting from hybrid solar integration and off-grid electrification initiatives.

Automotive OEMs and aftermarket distributors constitute approximately 48% of sealed lead acid battery consumption, while telecom operators represent about 22%; however, data center operators are the fastest-growing end-user segment, expanding at a CAGR of 6.4% as enterprise cloud adoption and digital infrastructure investments intensify globally. Automotive demand remains stable due to predictable replacement cycles and increasing vehicle ownership in Asia-Pacific and Latin America, whereas telecom providers prioritize VRLA systems to mitigate grid instability and reduce diesel dependency by up to 35% in hybrid solar sites. Industrial manufacturing facilities, healthcare institutions, and renewable energy integrators collectively contribute nearly 30% of market demand, with adoption rates exceeding 60% in mission-critical environments requiring immediate backup response.

Asia-Pacific accounted for the largest market share at 52% in 2025 however, North America is expected to register the fastest growth, expanding at a CAGR of 5.1% between 2026 and 2033.

Asia-Pacific’s dominance is supported by annual production volumes exceeding 300 million sealed lead acid battery units, with China and India collectively contributing over 65% of regional output. Automotive replacement demand across the region represents nearly 45% of total consumption, while telecom infrastructure accounts for approximately 28% due to more than 4 million active tower installations. North America, holding around 21% share in 2025, is witnessing accelerated expansion driven by data center capacity additions exceeding 10 GW annually and healthcare infrastructure modernization projects. Europe contributes roughly 18% of global demand, supported by strict recycling regulations requiring over 85% material recovery. South America and the Middle East & Africa together represent nearly 9% of total consumption, primarily linked to grid instability and off-grid solar deployment. Regional diversification, infrastructure digitization, and rising backup power requirements collectively shape competitive positioning and supply chain strategies in the global sealed lead acid batteries market.

How Is Critical Infrastructure Modernization Driving Industrial Backup Demand?

North America accounts for approximately 21% of the global sealed lead acid batteries market share, supported by strong demand from automotive aftermarket, telecom, healthcare, and financial data centers. The region operates over 5,000 large-scale data centers, many requiring high-rate discharge VRLA battery systems to ensure uptime reliability above 99.99%. Healthcare and finance sectors demonstrate higher enterprise adoption, with more than 65% of hospitals and Tier III facilities using AGM-based UPS systems. Regulatory frameworks emphasize safe battery recycling and emission controls, with recovery rates exceeding 95%. Technological advancements include IoT-enabled battery monitoring systems adopted in nearly 35% of new industrial installations. East Penn Manufacturing, a major regional producer, continues expanding automated production lines and investing in closed-loop recycling facilities processing over 500,000 tons of lead annually, reinforcing supply stability and ESG compliance.

Why Are Sustainability Mandates Reshaping Industrial Energy Storage Decisions?

Europe represents nearly 18% of the global sealed lead acid batteries market, with Germany, the United Kingdom, and France accounting for more than 60% of regional demand. Automotive replacement cycles remain stable, while renewable backup and telecom sectors contribute nearly 30% of installations. Stringent environmental directives require up to 85%–95% battery material recovery, accelerating investments in advanced recycling and low-emission smelting facilities. Adoption of AGM and gel technologies is increasing, particularly in industrial automation and renewable microgrid systems. Digital monitoring integration has expanded across 40% of new UPS installations. Exide Technologies, headquartered in Europe, has upgraded multiple facilities to enhance production automation and reduce operational emissions by nearly 20%, aligning with regional sustainability targets. Regulatory pressure continues to encourage transparent lifecycle management and higher performance standards across enterprise deployments.

What Factors Are Fueling High-Volume Manufacturing and Infrastructure Deployment?

Asia-Pacific leads global production and consumption with 52% market share, driven by China, India, and Japan. China alone manufactures over 80 million automotive batteries annually, while India’s telecom sector operates more than 700,000 towers requiring VRLA backup systems. Infrastructure expansion, rapid urbanization, and rising vehicle ownership exceeding 300 million registered vehicles collectively sustain high-volume demand. Regional manufacturing hubs benefit from vertically integrated lead recycling networks achieving recovery rates above 95%. Innovation trends include carbon-enhanced AGM plates and improved deep-cycle gel batteries tailored for high-temperature climates. GS Yuasa in Japan continues investing in advanced plate design and smart battery systems to improve cycle durability by nearly 15%. Consumer behavior in this region emphasizes cost efficiency and large-scale deployment, particularly in automotive replacement and off-grid electrification projects.

How Is Grid Instability Supporting Backup Power Investments?

South America holds approximately 5% of the global sealed lead acid batteries market, with Brazil and Argentina representing more than 70% of regional consumption. Automotive replacement demand contributes nearly 50% of installations, while telecom and off-grid solar systems account for about 30%. Energy reliability challenges, including periodic grid outages in certain urban centers, are increasing reliance on VRLA battery banks. Government programs promoting rural electrification and renewable hybrid systems have expanded decentralized storage deployments by over 12% in recent years. Trade policies encouraging domestic battery assembly are also supporting localized production. Moura Batteries, a prominent regional manufacturer, has expanded its recycling and manufacturing operations to process hundreds of thousands of units annually. Consumer purchasing behavior remains highly price-sensitive, favoring durable and recyclable sealed lead acid solutions.

Why Is Infrastructure Expansion Increasing Demand for Reliable Energy Storage?

The Middle East & Africa region accounts for nearly 4% of global sealed lead acid battery demand, driven by oil & gas facilities, construction projects, and telecom network expansion. The UAE and Saudi Arabia lead infrastructure modernization investments, while South Africa represents a significant automotive replacement market with millions of vehicles requiring periodic battery replacement. Off-grid solar installations across Sub-Saharan Africa exceed 50 million systems, many incorporating gel batteries for durability in high-temperature environments. Industrial backup installations are expanding alongside smart city projects and data center developments. Regulatory frameworks increasingly emphasize safe battery disposal and recycling compliance. Regional consumer behavior prioritizes durability under extreme climate conditions, leading to preference for heat-resistant VRLA and gel battery technologies in commercial and industrial deployments.

China – 38% market share: China leads the sealed lead acid batteries market due to large-scale production capacity exceeding 300 million units annually and strong automotive and telecom demand.

United States – 16% market share: The United States maintains dominance through extensive automotive aftermarket consumption and widespread deployment of VRLA systems across data centers and healthcare infrastructure.

The Sealed Lead Acid Batteries market operates within a moderately consolidated competitive environment, characterized by approximately 60–80 active global and regional manufacturers competing across automotive, telecom, UPS, and industrial segments. The top five companies collectively account for nearly 55% of global market share, indicating strong brand positioning and established distribution networks, while regional players maintain influence in cost-sensitive and localized markets. Large manufacturers focus on high-volume automotive replacement batteries and premium AGM variants for data centers and telecom towers, where performance reliability above 99% uptime is critical.

Strategic initiatives shaping competition include capacity expansion programs exceeding 10% annual output increases in Asia-Pacific, vertical integration into lead recycling achieving recovery rates above 95%, and automation upgrades that reduce manufacturing defects by nearly 15%. Partnerships with telecom operators and data center developers are strengthening long-term supply agreements, particularly for VRLA systems supporting 5G networks and hyperscale infrastructure. Product innovation centers on carbon-enhanced plates improving charge acceptance by 20% and IoT-enabled battery monitoring solutions adopted in nearly 35% of new industrial installations. Competitive intensity is further influenced by price sensitivity in emerging markets, where localized producers compete on durability and cost efficiency, while global leaders differentiate through technology upgrades, ESG compliance, and closed-loop manufacturing systems.

Clarios

GS Yuasa Corporation

EnerSys

East Penn Manufacturing Company

Exide Industries Limited

Amara Raja Energy & Mobility Limited

C&D Technologies

Trojan Battery Company

HBL Power Systems Limited

Leoch International Technology Limited

The Sealed Lead Acid Batteries market is experiencing a wave of technological enhancements that are shifting performance benchmarks and influencing procurement decisions. Advanced Absorbent Glass Mat (AGM) construction remains the predominant technology, accounting for approximately 46% of installations across automotive, telecom, and UPS systems due to its spill-proof design and improved vibration resistance. Recent improvements in AGM plate formulation, including carbon-enhanced lead alloys, have delivered up to 20% higher charge acceptance and extended deep-cycle durability by nearly 18% compared to older grid standards. Gel battery technology continues to advance as well, offering better tolerance to high ambient temperatures and reduced water loss, making it suitable for off-grid solar storage and industrial backup in harsh environments.

Emerging smart battery management technologies are integrating IoT sensors and predictive analytics tools into sealed lead acid systems, with adoption rates approaching 35% in new industrial and data center installations. These systems continuously monitor thermal gradients, voltage fluctuations, and state-of-charge levels, improving maintenance scheduling accuracy by nearly 22% and reducing unexpected failure events by approximately 15%. Wireless communication modules are enabling remote diagnostics and asset health scoring, which supports large-scale UPS and telecom networks with real-time performance insights.

In manufacturing, increased automation and robotics deployment has reduced production cycle times by up to 12% while enhancing consistency in plate alignment and electrolyte distribution. Closed-loop recycling technologies are strengthening sustainability credentials, achieving material recovery rates above 95% and lowering dependence on primary lead. Additionally, modular battery rack designs are facilitating faster installation and serviceability, particularly in hyperscale data centers and critical infrastructure projects where uptime reliability thresholds exceed 99.99%. These technology trends collectively position sealed lead acid batteries as resilient and adaptable energy storage solutions across established and emerging applications.

• In January 2024, EnerSys completed the acquisition of Bren-Tronics for approximately USD 208 million, strengthening its industrial energy systems portfolio and expanding advanced battery and charging solutions for defense and critical infrastructure markets. The move enhances vertical integration and global distribution capabilities. Source: www.enersys.com

• In 2024, Clarios released its Sustainability Report confirming a 99% recycling rate for lead-acid batteries in North America and highlighting continued investment in closed-loop recycling systems processing millions of batteries annually, reinforcing supply security and environmental stewardship in the sealed lead acid batteries market. Source: www.clarios.com

• In April 2024, Exide Industries commenced operations at its lithium-ion cell manufacturing facility in Bengaluru with an initial capacity of 6 GWh, marking a strategic diversification initiative while continuing leadership in conventional lead-acid battery production across automotive and industrial segments. Source: www.exideindustries.com

• In February 2025, GS Yuasa announced expansion initiatives to increase automotive lead-acid battery production capacity in Southeast Asia, aiming to strengthen supply stability for motorcycle and passenger vehicle markets amid rising regional demand. Source: www.gs-yuasa.com

The Sealed Lead Acid Batteries Market Report provides a comprehensive evaluation of product types, applications, technologies, end-user industries, and geographic coverage across major global regions. The scope encompasses key battery variants including Absorbent Glass Mat (AGM), Gel, and other valve-regulated lead acid (VRLA) configurations, collectively serving automotive, telecom, UPS, renewable energy, and industrial backup systems. Automotive starting, lighting, and ignition applications represent a substantial portion of unit demand due to a global vehicle parc exceeding 1.4 billion units, while telecom infrastructure with more than 7 million tower sites worldwide drives stable institutional procurement.

The report analyzes regional performance across Asia-Pacific, North America, Europe, South America, and the Middle East & Africa, covering production hubs with capacities exceeding 300 million units annually and recycling ecosystems achieving over 95% material recovery rates. It evaluates technological advancements such as carbon-enhanced electrodes delivering up to 20% improved charge acceptance, smart monitoring systems adopted in nearly 35% of new industrial installations, and modular rack designs optimized for data center deployments requiring uptime reliability above 99.99%.

Industry focus areas include automotive OEMs and aftermarket distributors, telecom operators, healthcare institutions, financial data centers, manufacturing plants, and off-grid solar integrators. The scope further addresses regulatory frameworks governing hazardous material handling, extended producer responsibility mandates, and ESG compliance targets emphasizing emission reduction and closed-loop recycling. Emerging niche segments such as hybrid solar-VRLA microgrids, rural electrification programs exceeding 500 million off-grid installations globally, and high-temperature industrial applications are also examined to provide decision-makers with a multidimensional strategic outlook.

| Report Attribute/Metric | Report Details |

|---|---|

|

Market Revenue in 2025 |

USD V2025 Million |

|

Market Revenue in 2033 |

USD V2033 Million |

|

CAGR (2026 - 2033) |

4.2% |

|

Base Year |

2025 |

|

Forecast Period |

2026 - 2033 |

|

Historic Period |

2021 - 2025 |

|

Segments Covered |

By Types

By Application

By End-User

|

|

Key Report Deliverable |

Revenue Forecast, Growth Trends, Market Dynamics, Segmental Overview, Regional and Country-wise Analysis, Competition Landscape |

|

Region Covered |

North America, Europe, Asia-Pacific, South America, Middle East, Africa |

|

Key Players Analyzed |

Clarios, GS Yuasa Corporation, EnerSys, East Penn Manufacturing Company, Exide Industries Limited, Amara Raja Energy & Mobility Limited, C&D Technologies, Trojan Battery Company, HBL Power Systems Limited, Leoch International Technology Limited |

|

Customization & Pricing |

Available on Request (10% Customization is Free) |