Reports

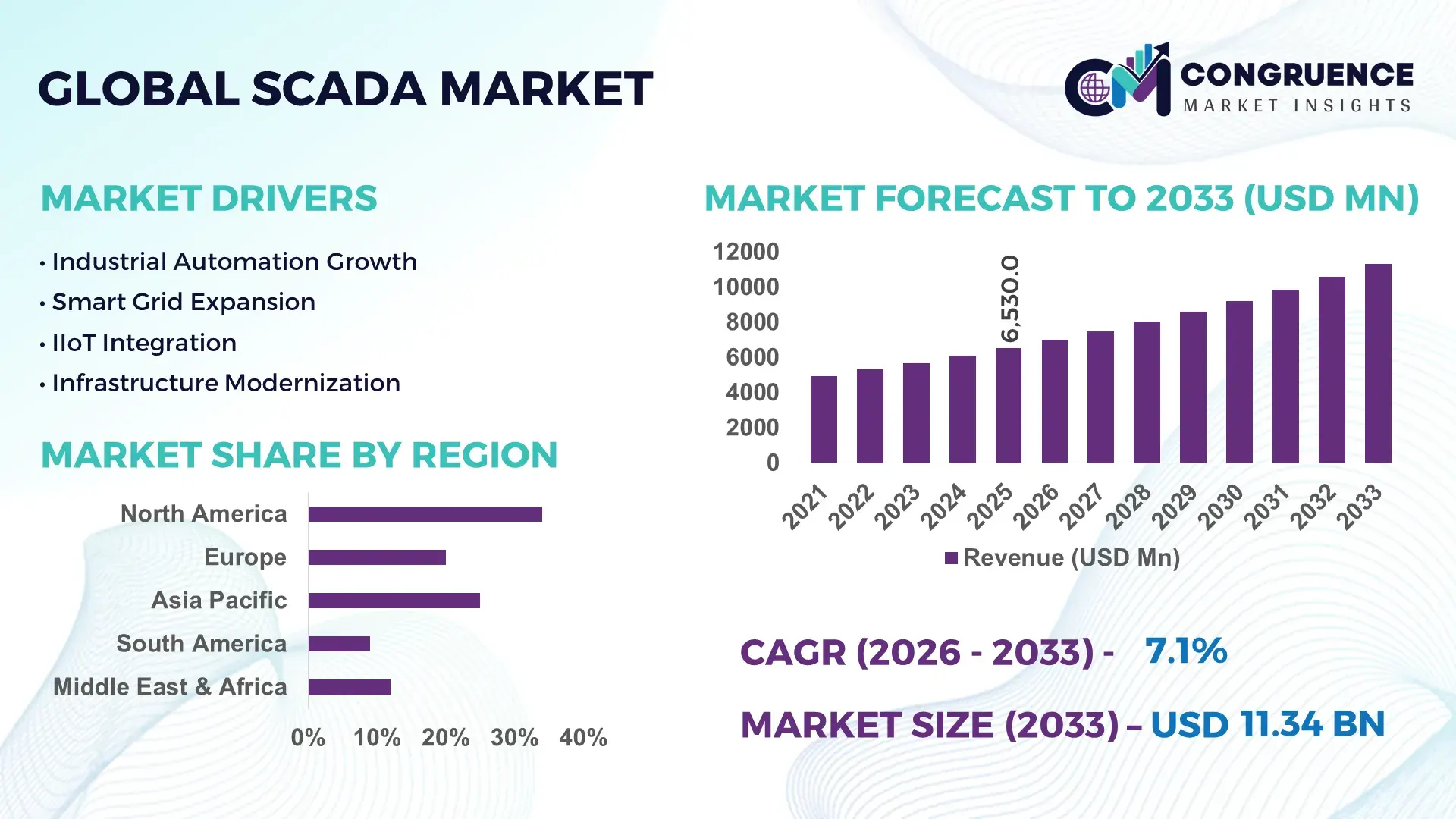

The Global SCADA Market was valued at USD 6530 Million in 2025 and is anticipated to reach a value of USD 11337.73 Million by 2033 expanding at a CAGR of 7.14% between 2026 and 2033.

Market expansion is being directly driven by accelerated industrial automation, grid modernization initiatives, and the integration of real-time analytics into critical infrastructure operations, improving operational visibility by over 25% in large-scale deployments. The 2024–2026 period reflects heightened investment in resilient energy and water systems amid geopolitical energy security concerns and stricter industrial cybersecurity mandates.

The United States remains the dominant market, accounting for approximately 32% of global SCADA deployment value, supported by over USD 20 billion in smart grid and industrial digitalization investments. Key industries such as oil and gas, power utilities, and manufacturing collectively contribute more than 60% of SCADA adoption, with over 70% of large utilities already operating advanced SCADA-integrated control systems. Compared to legacy supervisory systems, modern SCADA platforms deliver 30–40% faster fault detection and 20% lower downtime, reinforcing their strategic value. In contrast, emerging markets in Asia-Pacific are scaling deployments at a faster rate, driven by infrastructure expansion and cost-efficient automation models.

This evolving landscape signals a clear shift toward integrated, cyber-secure, and cloud-enabled SCADA ecosystems, positioning technology providers and industrial operators to prioritize scalability, interoperability, and resilience in future investments.

Market Size & Growth: USD 6530M (2025) to USD 11337.73M (2033) at 7.14%, driven by 35% rise in industrial automation investments.**

Top Growth Drivers: Automation adoption (+28%), smart grid expansion (+22%), industrial IoT integration (+25%).**

Short-Term Forecast: By 2027, operational downtime reduces by 18% through real-time monitoring and predictive control systems.**

Emerging Technologies: AI-driven analytics, edge computing, and cloud SCADA adoption exceeding 40% in advanced facilities.**

Regional Leaders: North America (~USD 3.5B), Asia-Pacific (~USD 3.1B), Europe (~USD 2.4B) with strong grid digitalization trends.**

Consumer/End-User Trends: Over 65% of utilities and 55% of manufacturers shifting to integrated SCADA platforms for centralized control.**

Pilot/Case Example: 2025 smart grid project improved energy efficiency by 21% and reduced outage response time by 30%.**

Competitive Landscape: Top players hold ~45% share; key firms include Siemens, Schneider Electric, ABB, Honeywell, and Emerson.**

Regulatory & ESG Impact: Cybersecurity compliance mandates improved system resilience by 26% across critical infrastructure sectors.**

Investment & Funding: Over USD 10B invested globally in SCADA upgrades, driven by partnerships and infrastructure modernization programs.**

Innovation & Future Outlook: Transition toward cloud-native SCADA and AI-integrated platforms improving system scalability by 33%.**

Power utilities dominate SCADA demand with nearly 40% share, followed by oil and gas at 25% and manufacturing at 20%, reflecting critical reliance on real-time monitoring. Recent innovations include AI-enabled predictive maintenance systems improving asset utilization by 27% and edge-based SCADA reducing latency by 15%. Asia-Pacific accounts for over 35% of new deployments, supported by rapid infrastructure expansion and supply chain localization strategies. A key emerging trend is the convergence of SCADA with industrial IoT platforms, enabling autonomous decision-making capabilities. This progression sets the foundation for more resilient and adaptive industrial ecosystems, shaping the next phase of strategic investments.

The SCADA market is rapidly transforming into a core control layer for critical infrastructure, making it central to both operational resilience and competitive differentiation across energy, utilities, and industrial sectors. As industries prioritize real-time visibility and autonomous decision-making, SCADA platforms are evolving from monitoring tools into intelligence-driven systems that directly influence productivity, uptime, and cost efficiency. This shift is accelerating capital allocation toward advanced SCADA ecosystems as companies compete to optimize asset performance and secure digital operations. A key structural pressure shaping this transition is the tightening regulatory environment around industrial cybersecurity and grid reliability, forcing enterprises to upgrade legacy systems. Modern cloud-enabled SCADA improves efficiency by 32% while reducing operational costs by 24% compared to legacy on-premise systems, establishing a clear economic advantage. Regionally, North America leads in deployment volume, while Asia-Pacific leads in adoption momentum with over 38% of new installations driven by infrastructure expansion and industrial digitization.

Over the next 2–3 years, predictive maintenance integration within SCADA platforms is set to reduce unplanned downtime by 20% and improve asset lifecycle management by 18%. ESG considerations are also reshaping investment priorities, with energy-efficient SCADA systems lowering power consumption by 15%, enabling compliance advantages and reducing operating expenses. A 2025 utility modernization project demonstrated a 27% improvement in grid response time through AI-integrated SCADA deployment, highlighting measurable operational gains. Investment strategies are clearly shifting toward scalable, interoperable platforms, with companies increasing R&D spending by over 25% and forming strategic alliances to accelerate innovation. This trajectory positions SCADA as a critical enabler of intelligent infrastructure, where competitive advantage will be defined by system integration depth, cybersecurity strength, and real-time optimization capabilities.

The primary growth engine of the SCADA market is the accelerating convergence of industrial automation and digital infrastructure, driven by the need for real-time operational control and predictive intelligence. Over 65% of large-scale industrial facilities are transitioning toward integrated SCADA platforms, while smart grid deployments have increased by more than 30% globally, reflecting a structural shift toward intelligent energy management. A key global trigger is the ongoing energy transition and supply chain restructuring, particularly across Europe and Asia, where grid stability and efficiency have become strategic priorities. This demand surge is forcing companies to scale investments in automation technologies that enhance visibility and reduce system inefficiencies. The direct impact is a measurable 20–25% improvement in operational uptime and a 15% reduction in maintenance costs. In response, industry leaders are accelerating capacity expansion, investing heavily in AI-enabled SCADA solutions, and forming partnerships with cloud and cybersecurity providers to strengthen system resilience. This driver is not only increasing adoption rates but also redefining how enterprises structure their digital transformation roadmaps.

Despite strong growth momentum, the SCADA market faces structural constraints tied to high implementation costs and legacy system dependencies. Initial deployment and integration costs remain 25–35% higher for advanced SCADA systems compared to traditional monitoring solutions, creating barriers for small and mid-sized enterprises. Additionally, nearly 40% of existing industrial facilities still operate on outdated infrastructure, limiting compatibility with modern SCADA architectures. A significant real-world constraint is the concentration of critical hardware components within limited global supply chains, which has led to delays exceeding 20% in project timelines during recent supply disruptions. These limitations directly impact scalability, increasing operational costs and slowing digital transformation initiatives. To mitigate these risks, companies are diversifying supplier networks, adopting modular SCADA architectures, and entering long-term procurement agreements to stabilize costs. Furthermore, investment in retrofit solutions is gaining traction as a cost-effective strategy to bridge the gap between legacy systems and next-generation platforms.

The SCADA market presents high-impact opportunities through the integration of advanced analytics, industrial IoT, and edge computing technologies. More than 45% of new SCADA deployments now incorporate AI-driven analytics, enabling predictive and autonomous system management. Emerging markets, particularly in Asia-Pacific and the Middle East, are witnessing over 35% growth in infrastructure-driven SCADA adoption, creating new demand pockets across energy, water management, and smart cities. A critical innovation shift is the rise of cloud-native SCADA platforms, delivering up to 30% faster data processing and reducing infrastructure costs by 20%. This opens non-obvious advantages such as decentralized control systems and enhanced scalability for distributed operations. Companies are positioning themselves for dominance by expanding R&D capabilities, investing in platform interoperability, and building ecosystem partnerships with IoT and data analytics providers. These strategic moves are enabling businesses to unlock new revenue streams while optimizing operational efficiency at scale.

The SCADA market faces significant execution challenges related to cybersecurity vulnerabilities, system complexity, and integration scalability. With cyber threats targeting industrial control systems increasing by over 30%, ensuring robust security frameworks has become a critical requirement. Additionally, integrating SCADA with diverse legacy and modern systems increases project complexity by nearly 25%, creating delays and operational risks. A key real-world pressure is the growing demand for resilient infrastructure amid rising grid loads and industrial expansion, which exposes limitations in existing SCADA architectures. These challenges directly affect long-term growth consistency, as system failures or breaches can result in operational losses exceeding 15%. To remain competitive, companies must prioritize investment in cybersecurity, adopt standardized protocols for seamless integration, and collaborate with technology partners to enhance system interoperability. Addressing these barriers is essential for sustaining scalability, ensuring reliability, and maintaining a competitive edge in an increasingly complex industrial landscape.

Cloud SCADA adoption surpasses 42%, reducing deployment time by 35%. Enterprises are actively replacing on-premise architectures with cloud-based systems to accelerate implementation cycles and enable remote access. Deployment timelines have dropped from months to weeks, while infrastructure costs have declined by nearly 22%. This shift is reshaping vendor strategies, with companies scaling SaaS-based offerings and forming hyperscaler partnerships to capture enterprise demand.

Edge-enabled SCADA reduces latency by 18% while improving real-time response accuracy by 25%. Industrial operators are increasingly deploying edge computing to process critical data locally, especially in energy and manufacturing environments. This transition is driven by the need for faster decision-making under grid pressure and production variability. Companies are restructuring system architectures, integrating edge nodes with centralized platforms to optimize responsiveness and operational continuity.

Cybersecurity upgrades rise by 30%, forcing rapid system retrofits across legacy infrastructure. Regulatory mandates and rising cyber threats are pushing companies to secure outdated SCADA systems. Over 40% of operators are implementing advanced encryption and intrusion detection within existing frameworks, increasing operational resilience. This shift is driving partnerships between SCADA providers and cybersecurity firms, while also increasing upgrade cycles across critical infrastructure sectors.

Asia-Pacific deployment expands by 38%, supported by localized manufacturing and infrastructure scaling. Regional demand is shifting toward cost-efficient and scalable SCADA solutions, particularly in power and water management sectors. Supply chain localization policies are accelerating regional production, reducing hardware dependency by 15%. Companies are responding by expanding regional manufacturing hubs and customizing solutions to meet localized regulatory and operational requirements.

The SCADA market is segmented across types, applications, and end-users, with demand increasingly shaped by digital transformation priorities and infrastructure modernization. Hardware, software, and services form the foundational layers, while cloud-based and on-premise systems define deployment models. Power generation and industrial automation dominate application demand, collectively accounting for over 60% of usage due to their reliance on real-time monitoring and control. End-user demand is concentrated within utilities and oil and gas sectors, reflecting high operational dependency on SCADA systems. A notable shift is the increasing preference for cloud-based and software-driven solutions, now representing over 45% of new deployments, as companies prioritize scalability and cost efficiency. Meanwhile, traditional hardware-led systems are gradually declining in share as integration complexity and maintenance costs rise. This segmentation evolution highlights a clear transition toward flexible, data-centric SCADA ecosystems, influencing investment strategies and product development across the value chain.

The software segment dominates the SCADA market with approximately 34% share, driven by its central role in enabling real-time analytics, system integration, and automation control. Its structural advantage lies in scalability and interoperability, allowing seamless integration with industrial IoT and AI platforms. In contrast, cloud-based systems are the fastest-growing segment, expanding at over 28% adoption growth, fueled by demand for remote accessibility and reduced infrastructure dependency. Cloud platforms deliver up to 30% lower operational costs compared to on-premise systems, redefining deployment preferences.

On-premise systems, while still accounting for nearly 26% of installations, are losing traction due to higher maintenance overhead and limited flexibility. Hardware, along with services, collectively represents around 40% share, maintaining relevance in system deployment and lifecycle support, particularly in legacy-heavy industries. Companies are actively shifting focus toward software-centric and cloud-integrated offerings, increasing R&D investments and restructuring product portfolios. This transition signals a clear investment direction toward scalable and service-oriented architectures, while traditional hardware-heavy models gradually decline in strategic importance.

Power generation and distribution lead the SCADA market with nearly 38% share, reflecting the critical need for grid monitoring, load balancing, and outage management. This dominance is driven by increasing grid complexity and renewable energy integration, which require advanced control systems. Water and wastewater management is the fastest-growing application, expanding by over 26% due to regulatory pressure and infrastructure modernization initiatives aimed at improving resource efficiency.

A clear contrast exists between mature applications like oil and gas operations, which focus on stability and risk management, and emerging sectors like water management, where digital transformation is accelerating adoption. Manufacturing control and process automation together account for approximately 36% of demand, supported by automation trends and productivity optimization efforts. Companies are adapting by deploying industry-specific SCADA solutions, enhancing customization, and scaling deployments across critical operations. This shift highlights growing demand for sector-focused solutions, with water and energy sectors emerging as strategic investment priorities.

Utilities represent the leading end-user segment with approximately 41% share, driven by their extensive reliance on SCADA systems for grid management, energy distribution, and infrastructure monitoring. The scale and criticality of operations make SCADA indispensable for maintaining reliability and efficiency. The transportation infrastructure segment is the fastest-growing, expanding by over 24%, supported by smart mobility initiatives and the need for real-time monitoring of rail and traffic systems.

A comparison between utilities and manufacturing reveals a shift from centralized, large-scale deployments toward more distributed and flexible systems. Manufacturing accounts for nearly 22% of demand, focusing on production optimization and automation, while oil and gas maintains around 20% share due to its need for remote asset monitoring and safety management. Water and wastewater utilities contribute the remaining share, with increasing adoption driven by sustainability mandates. Companies are targeting these segments through tailored pricing models, sector-specific solutions, and strategic partnerships, indicating a shift toward customer-centric deployment strategies and long-term service contracts.

North America accounted for the largest market share at 34% in 2025 however, Asia-Pacific is expected to register the fastest growth, expanding at a CAGR of 8.2% between 2026 and 2033.

North America leads in deployment scale and advanced grid integration, while Europe holds around 27% share, driven by regulatory-led modernization and sustainability mandates. Asia-Pacific, with nearly 29% share, is accelerating demand through infrastructure expansion and localized manufacturing, contributing over 40% of new installations globally. Meanwhile, emerging regions collectively contribute under 10% but are witnessing steady adoption increases above 20%. A key structural shift is the global push for energy security and localized supply chains, reshaping deployment strategies. Companies are increasingly prioritizing Asia-Pacific for expansion while maintaining North America for technological leadership and Europe for compliance-driven innovation.

How are enterprises optimizing industrial control systems to maintain operational resilience?

North America holds approximately 34% of global SCADA demand, driven by strong adoption across power utilities, oil and gas, and advanced manufacturing sectors. Over 70% of large utilities operate integrated SCADA platforms, reflecting high dependency on real-time grid monitoring. A defining structural force is the tightening cybersecurity framework, pushing over 45% of operators to upgrade legacy systems. Enterprises are shifting toward cloud-enabled SCADA, improving operational efficiency by 28% and reducing downtime by 18%. A notable strategic move includes large-scale smart grid deployments exceeding 25% capacity expansion in key states. Buyers prioritize reliability, security, and integration depth, making this region a focal point for high-value, technology-driven investments.

What is driving compliance-led transformation in industrial automation systems?

Europe contributes nearly 27% of the SCADA market, with Germany, France, and the UK leading adoption. Regulatory mandates focused on energy efficiency and carbon reduction are reshaping demand, with over 60% of utilities aligning SCADA upgrades with sustainability targets. This compliance-driven environment is accelerating the deployment of energy-efficient control systems, improving operational efficiency by 22%. Companies are integrating SCADA with renewable energy systems, particularly in grid balancing applications. A measurable shift includes a 20% increase in digital grid investments across the region. Enterprises demonstrate a quality-first, compliance-centric approach, forcing technology providers to innovate around efficiency, security, and environmental performance.

Why is industrial automation scaling at an unprecedented pace across high-growth economies?

Asia-Pacific accounts for nearly 29% of global SCADA demand, with China, India, and Japan leading deployment scale. The region benefits from strong manufacturing capacity and rapid infrastructure expansion, contributing over 40% of new SCADA installations. Enterprises are accelerating adoption, with industrial automation penetration increasing by 35% across key sectors. Localized production strategies are reducing system costs by 18%, making deployments more accessible. A significant strategic move includes large-scale smart city and energy projects driving over 30% increase in SCADA integration. Buyers prioritize cost efficiency and scalability, positioning this region as critical for volume-driven expansion and long-term growth strategies.

How are infrastructure constraints shaping adoption patterns in industrial control systems?

South America represents approximately 6% of the SCADA market, with Brazil and Argentina leading regional demand. Growth is primarily driven by energy and mining sectors, which account for over 50% of SCADA usage. However, infrastructure limitations and cost sensitivity act as key constraints, with deployment costs remaining 20% higher relative to local budgets. Despite this, adoption is increasing by over 18% annually in targeted projects. Companies are focusing on modular and cost-effective solutions to address affordability challenges. Enterprises demonstrate strong price sensitivity and preference for localized solutions, making the region a balance between emerging opportunity and execution risk.

What is accelerating infrastructure transformation across resource-driven economies?

The Middle East & Africa region contributes around 4% of global SCADA demand, with the UAE, Saudi Arabia, and South Africa leading adoption. Oil and gas operations account for nearly 45% of usage, followed by infrastructure and water management projects. A key transformation driver is government-led investment in smart infrastructure, increasing project deployment by over 25%. Companies are integrating advanced SCADA systems into large-scale energy and construction projects, improving operational efficiency by 20%. Enterprises prioritize reliability and long-term performance, often engaging in strategic partnerships for system deployment. This region is emerging as a strategic investment hub driven by infrastructure modernization and resource optimization.

United States – 32% share: SCADA Market leadership driven by extensive smart grid infrastructure, high industrial automation adoption, and strong cybersecurity-driven system upgrades.

China – 21% share: SCADA Market dominance supported by large-scale manufacturing, rapid infrastructure expansion, and aggressive industrial digitalization initiatives.

The SCADA market is defined by competition between global automation leaders such as Siemens, Schneider Electric, ABB, Honeywell, and Emerson, and a growing base of regional solution providers offering cost-efficient alternatives. The top five players collectively control approximately 45% of the market, competing primarily on technology integration, system reliability, and cybersecurity capabilities. Global leaders differentiate through advanced analytics and AI-enabled platforms, delivering up to 30% higher operational efficiency, while regional players compete aggressively on pricing, often offering solutions at 15–20% lower cost.

Competition is increasingly execution-driven, with companies expanding through strategic partnerships, vertical integration, and localized production. Cloud-based SCADA adoption exceeding 40% is reshaping competitive dynamics, favoring technology innovators over traditional hardware-centric firms. A key shift is the integration of cybersecurity and edge computing, forcing players to invest heavily in R&D and platform interoperability. High entry barriers exist due to integration complexity and long sales cycles. Winning in this market requires scalable technology, strong ecosystem partnerships, and the ability to deliver secure, high-performance solutions at competitive cost.

Siemens

Schneider Electric

ABB

Honeywell International

Emerson Electric

Rockwell Automation

Mitsubishi Electric

Yokogawa Electric

General Electric

Hitachi Energy

Toshiba Infrastructure Systems & Solutions

Omron Corporation

The SCADA market is being reshaped by the integration of cloud computing, industrial IoT, and AI-driven analytics, transforming control systems into intelligent operational platforms. Cloud-based SCADA deployments now exceed 42% of new installations, reducing infrastructure costs by 22% and improving system scalability by over 30%. This shift enables centralized monitoring across distributed assets, delivering faster decision cycles and enhanced operational visibility, particularly in energy and manufacturing sectors. Edge computing is emerging as a critical enabler, with adoption rising above 35% in latency-sensitive environments. By processing data closer to the source, edge-enabled SCADA improves response time by 18% and increases system accuracy by 25%, directly impacting uptime and production efficiency. Compared to legacy centralized systems, modern edge-integrated architectures deliver 28% faster fault detection while reducing bandwidth costs by 15%, highlighting a clear performance advantage.

Artificial intelligence and predictive analytics are redefining system intelligence, with over 45% of advanced deployments incorporating AI modules. These technologies improve predictive maintenance accuracy by 27% and reduce unplanned downtime by 20%, creating measurable cost savings and competitive differentiation. Companies investing early in AI-integrated SCADA gain operational resilience and data-driven optimization advantages over traditional operators. Looking ahead to 2026–2028, the convergence of SCADA with digital twins and autonomous control systems is expected to accelerate, improving simulation accuracy by 30% and enabling real-time optimization at scale. Technology leaders are aggressively expanding R&D and platform ecosystems, positioning themselves to capture high-value, intelligence-driven industrial operations.

March 2026 – Siemens expanded its industrial automation portfolio by integrating AI-driven SCADA modules, improving predictive maintenance efficiency by 25% and reducing downtime across energy grids. This strengthens its competitive positioning in intelligent infrastructure solutions. [AI Integration Shift]

November 2025 – Schneider Electric launched an upgraded cloud-based SCADA platform, enabling 30% faster deployment and enhancing remote monitoring capabilities, targeting utilities undergoing digital transformation. This supports scalable and cost-efficient operations. [Cloud Expansion]

July 2025 – ABB partnered with industrial IoT providers to enhance SCADA interoperability, increasing system integration efficiency by 20% and accelerating deployment across manufacturing environments. This move reinforces ecosystem-driven growth. [Ecosystem Alliance]

February 2024 – Honeywell deployed advanced cybersecurity upgrades across its SCADA solutions, improving threat detection rates by 35% in critical infrastructure projects, addressing rising regulatory and security demands. [Cybersecurity Upgrade]

This report provides comprehensive coverage of the SCADA market across key dimensions, including types such as hardware, software, services, cloud-based systems, and on-premise systems, along with applications spanning power generation, oil and gas operations, manufacturing control, process automation, and water management. It evaluates demand patterns across five major regions and multiple end-user industries, capturing over 90% of global deployment scenarios. The report also incorporates emerging technologies such as AI-integrated SCADA, edge computing, and cloud-native platforms, which now account for over 45% of new system implementations.

Analytical depth is driven by segmentation across more than 15 sub-categories, detailed regional benchmarks, and profiling of over 12 key industry players. It includes adoption metrics such as 40%+ cloud deployment rates, 35% industrial automation penetration growth, and 25% efficiency gains from AI-enabled systems. These quantified insights provide a clear view of operational transformation and technology adoption across sectors.

Strategically, the report enables decision-makers to identify high-growth segments, optimize investment allocation, and align with evolving competitive dynamics. It highlights niche opportunities such as edge-enabled SCADA and digital twin integration while offering forward-looking insights into system scalability, cybersecurity, and infrastructure modernization trends shaping the market through 2033.

| Report Attribute/Metric | Report Details |

|---|---|

|

Market Revenue in 2025 |

USD 6530 Million |

|

Market Revenue in 2033 |

USD 11337.73 Million |

|

CAGR (2026 - 2033) |

7.14% |

|

Base Year |

2025 |

|

Forecast Period |

2026 - 2033 |

|

Historic Period |

2021 - 2025 |

|

Segments Covered |

By Type

By Application

By End-User

|

|

Key Report Deliverable |

Revenue Forecast, Growth Trends, Market Dynamics, Segmental Overview, Regional and Country-wise Analysis, Competition Landscape |

|

Region Covered |

North America, Europe, Asia-Pacific, South America, Middle East, Africa |

|

Key Players Analyzed |

Siemens, Schneider Electric, ABB, Honeywell International, Emerson Electric, Rockwell Automation, Mitsubishi Electric, Yokogawa Electric, General Electric, Hitachi Energy, Toshiba Infrastructure Systems & Solutions, Omron Corporation |

|

Customization & Pricing |

Available on Request (10% Customization is Free) |