Reports

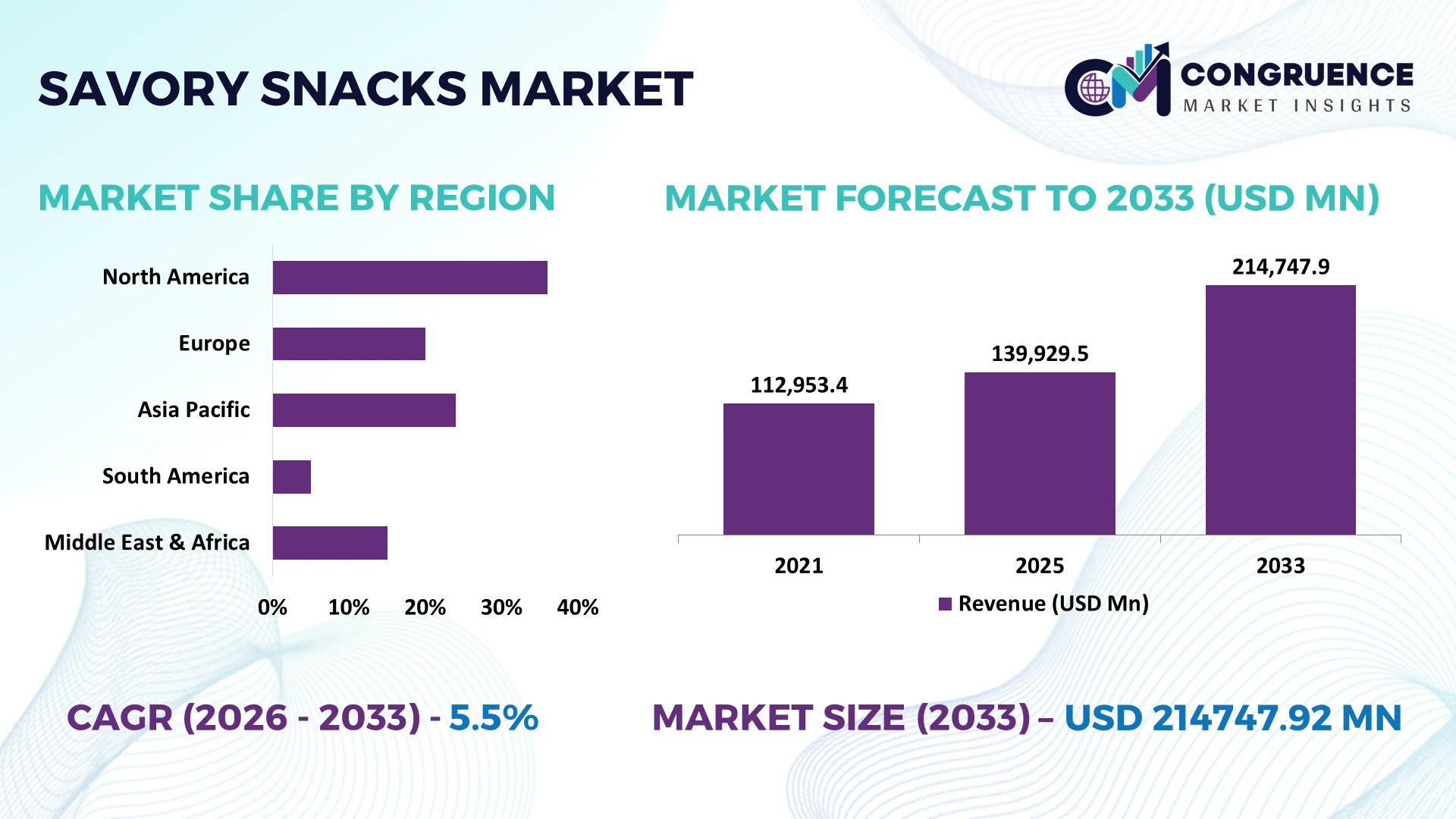

The Global Savory Snacks Market was valued at USD 139929.5 Million in 2025 and is anticipated to reach a value of USD 214747.92 Million by 2033 expanding at a CAGR of 5.5% between 2026 and 2033. Rising investments in healthier snack formulations, AI-enabled food processing, premium flavor innovation, and automated packaging systems are accelerating production efficiency and category expansion across global retail channels.

The United States dominates the global savory snacks market with approximately 29% consumption share, supported by over 78% automated processing across large manufacturing facilities and continued investment in advanced food production technologies. Compared with India, where organized packaged snack penetration has crossed 19% in urban markets, the U.S. benefits from higher premium product adoption and stronger private-label expansion. Following the 2026 Red Sea shipping disruptions, leading manufacturers accelerated regional sourcing and packaging localization to strengthen supply resilience and reduce logistics dependence.

Manufacturers prioritizing regional production, automation, and premium product innovation are strengthening long-term competitiveness while improving operational resilience across high-growth markets.

Market Size & Growth: USD 139929.5 Million (2025) to USD 214747.92 Million (2033) at a CAGR of 5.5%, supported by AI-enabled manufacturing, premium product innovation, and automated food processing.

Top Growth Drivers: Healthy snacking demand (+24%), premium flavor adoption (+18%), and organized retail expansion (+21%) continue to strengthen global market momentum.

Short-Term Forecast: By 2027, automated production systems are expected to reduce manufacturing waste by 12% while improving packaging efficiency by nearly 15%.

Emerging Technologies: AI-based quality inspection, robotic packaging, and digital production monitoring improve manufacturing efficiency by more than 20% across advanced facilities.

Regional Leaders: North America (~USD 67 Billion), Asia-Pacific (~USD 61 Billion), and Europe (~USD 52 Billion) lead expansion through premiumization, retail modernization, and digital commerce adoption.

Consumer Trends: More than 58% of urban consumers increasingly prefer protein-rich, baked, and reduced-sodium savory snack products for regular consumption.

Pilot Example: A 2026 AI-powered production modernization program improved manufacturing throughput by 17% while reducing quality defects by 14%.

Competitive Landscape: The top five manufacturers collectively account for nearly 38% market share, led by PepsiCo, Mondelez International, Kellogg, Nestlé, and Calbee.

Regulatory & ESG Impact: Sustainable packaging initiatives have lowered virgin plastic consumption by approximately 20% while supporting compliance with evolving environmental regulations.

Investment & Funding: More than USD 2.5 Billion has been directed toward manufacturing expansion, automation upgrades, strategic partnerships, and regional supply-chain diversification.

Innovation & Future Outlook: Clean-label formulations, plant-based ingredients, precision seasoning technologies, and smart manufacturing platforms continue to reshape competitive positioning across the global market.

The Savory Snacks Market continues to expand through strong demand for baked snacks, protein-enriched products, and clean-label innovations across retail and convenience channels. Around 35% of newly launched products now emphasize functional ingredients or reduced-fat formulations, while AI-enabled quality control and automated seasoning technologies improve production consistency. During 2026, regional ingredient sourcing and localized manufacturing strengthened supply-chain resilience, creating a solid foundation for the strategic market discussion.

The Savory Snacks Market has become strategically important as manufacturers compete through premiumization, healthier formulations, and resilient production networks rather than pricing alone. Supply-chain restructuring following global logistics disruptions has accelerated regional ingredient sourcing and localized manufacturing, reducing procurement risk while improving production continuity. Retail digitalization and data-driven product planning are also reshaping portfolio decisions, enabling companies to respond faster to changing consumer preferences and shorten product launch cycles.

AI-enabled quality inspection and automated seasoning systems deliver approximately 18% higher production efficiency and reduce product waste by nearly 12% compared with conventional manual quality control. The United States leads in automated food processing and private-label innovation, while India records faster expansion in organized packaged snack consumption supported by modern retail and digital commerce. Over the next two to three years, automated production deployment across medium and large manufacturing facilities is expected to exceed 65%, improving consistency and inventory planning.

Leading manufacturers are expanding regional production facilities, investing in sustainable packaging, and forming ingredient partnerships to strengthen supply security. A recent deployment of AI-based production monitoring enabled double-digit improvements in throughput while reducing quality deviations across multiple processing lines. Companies combining localized sourcing, advanced manufacturing technologies, and continuous product innovation will strengthen competitive positioning and maintain long-term operational resilience.

Growing consumer preference for healthier and premium snack categories is accelerating investment in advanced food manufacturing and product diversification. More than 58% of urban consumers now prefer baked, protein-rich, or reduced-sodium snacks, while automated processing improves production efficiency by approximately 20% and lowers material waste by nearly 12%. India continues expanding organized snack manufacturing through new processing facilities, while the United States increases investment in AI-enabled quality management. In response, manufacturers are expanding production capacity, strengthening supplier partnerships, and introducing clean-label product portfolios. Companies integrating automation with rapid product innovation achieve stronger retail positioning, faster commercialization, and greater operational flexibility.

Fluctuating prices of edible oils, potatoes, corn, and seasoning ingredients continue to pressure manufacturing economics and supply stability. Ingredient procurement costs have experienced periodic fluctuations exceeding 15%, while transportation expenses remain elevated in several international trade corridors. The 2026 continuation of shipping route adjustments has increased procurement complexity for globally sourced ingredients. Manufacturers are responding through localized sourcing strategies, multi-country supplier agreements, and long-term procurement contracts to stabilize operations. Companies with diversified supplier networks and flexible production planning maintain stronger inventory control and protect product availability despite ongoing supply-chain uncertainty.

Demand for functional nutrition creates new opportunities beyond traditional savory snack categories. Approximately 35% of recent product launches emphasize clean-label ingredients, plant proteins, or added nutritional value, while AI-driven production analytics improve manufacturing efficiency by nearly 18%. Japan and South Korea continue advancing precision food processing technologies, encouraging wider adoption of smart manufacturing platforms. Companies are increasing investment in R&D, collaborating with ingredient innovators, and expanding premium product portfolios designed for health-conscious consumers. The combination of personalized nutrition and digital manufacturing creates differentiated market positioning with higher operational efficiency and stronger customer retention.

Maintaining consistent product quality across geographically distributed manufacturing facilities remains a significant execution challenge. Nearly 42% of food manufacturers continue operating mixed production environments where legacy equipment limits seamless digital integration, while workforce training requirements increase implementation timelines by approximately 15%. Cross-facility data standardization and equipment interoperability have become major operational priorities, particularly for multinational producers. Companies are investing in cloud-connected manufacturing platforms, workforce upskilling, and standardized production protocols to improve consistency. Successfully integrating digital operations across diverse production sites will determine long-term competitiveness, manufacturing resilience, and brand reliability.

AI-Driven Production Optimization AI-enabled inspection systems and automated seasoning lines are becoming standard across large manufacturing facilities, improving production efficiency by nearly 20% while reducing product defects by approximately 15%. Labor shortages and rising operating costs are accelerating automation deployment, particularly in the United States. Manufacturers are expanding smart factory investments and integrating real-time production analytics to strengthen throughput, reduce downtime, and improve batch consistency across multiple product categories.

Localized Ingredient Procurement Strategies Manufacturers are restructuring sourcing networks as regional procurement now accounts for nearly 40% of ingredient purchasing among leading producers, reducing logistics disruptions by approximately 18%. Ongoing shipping route adjustments during 2026 encouraged greater reliance on domestic suppliers in India and North America. Companies are establishing long-term agricultural partnerships, expanding local processing capacity, and redesigning procurement models to improve inventory stability while lowering transportation complexity.

Premium Functional Product Expansion Nearly 35% of newly introduced savory snacks now feature clean-label ingredients, higher protein content, or reduced sodium formulations, while premium product sales have expanded by roughly 22% in organized retail. Consumer preference for healthier alternatives continues reshaping product portfolios. Manufacturers are increasing investment in formulation research, premium packaging, and ingredient innovation to differentiate offerings while strengthening brand positioning across supermarkets and digital retail platforms.

Digital Retail Portfolio Acceleration Online snack purchases have increased by approximately 26%, supported by AI-powered demand forecasting and integrated inventory management systems that improve order fulfillment by nearly 16%. Enterprise retailers are using consumer analytics to optimize product assortment and promotional planning. Leading manufacturers are strengthening omnichannel partnerships, expanding direct-to-consumer operations, and deploying digital merchandising strategies to improve inventory visibility and accelerate market responsiveness.

Potato Chips remain the leading segment with an estimated market share of approximately 39% due to efficient large-scale manufacturing, broad consumer acceptance, and cost-effective production. Standardized processing technology and extensive retail availability support consistent output and strong shelf presence. Extruded Snacks continue expanding through flavor innovation and automated production, while Popcorn benefits from increasing preference for lighter snack alternatives. Nuts & Seeds maintain stable demand as health-conscious consumers seek nutrient-rich options with higher perceived nutritional value.

Meat Snacks represent the fastest-growing segment as protein-focused diets and premium convenience foods reshape purchasing behavior. Product launches featuring clean-label ingredients have increased by nearly 30%, while automated processing improves manufacturing efficiency by approximately 18%. Leading companies are expanding premium portfolios, strengthening ingredient partnerships, and investing in advanced processing technologies to capture evolving consumer preferences. Investment priorities increasingly favor higher-value snack categories capable of delivering stronger margins while maintaining diversified product portfolios.

Retail Consumption leads the market with an estimated share of approximately 56%, supported by supermarket expansion, private-label growth, and broad household purchasing frequency. Convenience Stores remain an important distribution channel because of impulse purchasing behavior, while Foodservice continues strengthening demand through menu diversification and packaged snack offerings. Vending Machines maintain relevance across transportation hubs, workplaces, and educational institutions through expanding cashless payment integration.

Online Retail is the fastest-growing application as digital grocery platforms increase product accessibility and personalized recommendations improve purchasing conversion. Online snack purchases have expanded by approximately 26%, while AI-enabled inventory planning improves fulfillment efficiency by nearly 16%. Companies are strengthening omnichannel distribution, expanding fulfillment partnerships, and optimizing digital merchandising strategies to capture changing consumer purchasing behavior. Operational focus continues shifting toward integrated retail ecosystems capable of supporting rapid inventory replenishment and enhanced customer engagement.

Households account for approximately 68% of total savory snack consumption due to frequent purchases, broad product availability, and increasing preference for convenient packaged foods. Restaurants and Hotels continue supporting demand through complementary food offerings and hospitality services, while Institutional Catering maintains stable procurement for schools, workplaces, and healthcare facilities. Established purchasing patterns continue favor standardized packaging and consistent product availability across multiple distribution channels.

Cafés represent the fastest-growing end-user segment as premium snacking and beverage pairing strategies attract urban consumers seeking convenient meal alternatives. Premium snack menu additions have increased by approximately 24%, while customized packaging solutions improve operational efficiency by nearly 14%. Manufacturers are introducing foodservice-exclusive product formats, expanding distribution partnerships, and developing premium flavor portfolios tailored to hospitality operators. Competitive positioning increasingly depends on customized offerings that align with changing consumer preferences and evolving out-of-home consumption patterns.

North America accounted for the largest market share at 34.8% in 2025 however, Asia-Pacific is expected to register the fastest growth, expanding at a 6.8% CAGR between 2026 and 2033.

Advanced Manufacturing and Premium Product Leadership

North America maintains the strongest position through highly automated food processing infrastructure, mature retail networks, and continuous premium product innovation. The region contributes approximately 35% of global savory snack production, supported by widespread deployment of AI-enabled quality inspection and automated packaging technologies across large manufacturing facilities. More than 75% of major production plants utilize advanced processing systems to improve production consistency and reduce operational waste. Private-label expansion, healthier snack portfolios, and localized ingredient procurement continue strengthening operational resilience. Manufacturers are expanding regional processing facilities while increasing investments in digital manufacturing platforms, enabling faster product commercialization, improved inventory planning, and stronger responsiveness to evolving consumer preferences.

United States Market Outlook: The United States leads the regional market through large-scale manufacturing capacity, integrated agricultural supply chains, and extensive retail distribution. More than 78% of leading snack production facilities utilize advanced automation technologies, supporting higher production efficiency and consistent quality standards. Manufacturers continue investing in premium formulations, AI-driven production monitoring, and sustainable packaging while strengthening domestic ingredient sourcing to improve long-term operational resilience.

Sustainability and Clean-Label Transformation

Europe continues strengthening its market position through sustainable food production, clean-label innovation, and modernized manufacturing infrastructure. The region represents approximately 27% of global market demand, supported by strict product quality standards and increasing investment in recyclable packaging technologies. More than 60% of new premium snack launches emphasize natural ingredients or reduced additives. Food manufacturers continue modernizing production facilities through automation while strengthening regional supplier partnerships to improve ingredient traceability and operational efficiency. Sustainability targets and packaging optimization remain central to enterprise investment strategies across established food manufacturing hubs.

Germany Market Outlook: Germany remains the region's industrial leader due to advanced food processing capabilities, efficient manufacturing infrastructure, and strong engineering expertise. Automated production systems are deployed across more than 70% of large processing facilities, improving manufacturing consistency and reducing operational waste. Companies continue expanding premium product portfolios while investing in energy-efficient processing equipment and sustainable packaging technologies to maintain competitiveness across domestic and export markets.

Manufacturing Scale and Consumer Expansion

Asia-Pacific continues recording the strongest operational expansion through rapid manufacturing capacity growth, urbanization, and organized retail development. The region accounts for approximately 31% of global production, supported by expanding food processing investments and increasing adoption of automated packaging technologies. Modern manufacturing facilities have improved production efficiency by nearly 18%, while digital commerce continues accelerating packaged snack distribution. Manufacturers are strengthening regional processing capacity, expanding localized ingredient sourcing, and introducing products tailored to evolving consumer preferences. The combination of manufacturing scale and growing domestic consumption reinforces the region's strategic importance.

India Market Outlook: India has emerged as the fastest-developing national market through expanding organized food manufacturing, modern retail penetration, and digital grocery adoption. Urban packaged snack consumption continues increasing steadily, while automated production investments improve manufacturing efficiency across large processing plants. Companies are expanding regional production facilities, strengthening agricultural sourcing partnerships, and introducing affordable premium products designed for diverse consumer segments and nationwide distribution.

Retail Expansion Supports Consumption Growth

South America continues strengthening its savory snacks industry through retail modernization, agricultural resource availability, and expanding domestic manufacturing. The region contributes approximately 8% of global market activity, supported by growing supermarket penetration and increasing investment in local food processing facilities. Automated packaging deployment has improved production efficiency by nearly 14% among larger manufacturers. Companies continue balancing expansion opportunities with infrastructure and logistics limitations by strengthening domestic supplier relationships and increasing investment in regional production capabilities. Product localization and cost optimization remain important competitive priorities.

Brazil Market Outlook: Brazil leads the regional market through its extensive agricultural base, established food manufacturing sector, and large consumer population. Processing facilities continue expanding automation to improve operational productivity and product consistency. Manufacturers are strengthening local sourcing agreements, investing in distribution infrastructure, and expanding premium snack portfolios while improving production flexibility to address changing consumer preferences and retail requirements.

Investment-Led Food Industry Modernization

The Middle East & Africa market continues progressing through food manufacturing investments, modern retail expansion, and increasing processing infrastructure development. The region represents approximately 6% of global market activity, while investment in automated packaging and regional production facilities continues expanding. Production efficiency has improved by nearly 15% across recently modernized facilities. Companies are increasing localization efforts, strengthening regional distribution partnerships, and expanding manufacturing capabilities to reduce import dependence. Government-backed industrial diversification programs continue supporting long-term food processing development across key markets.

Saudi Arabia Market Outlook: Saudi Arabia remains the region's leading investment destination due to expanding food manufacturing infrastructure, industrial diversification initiatives, and modern retail development. Manufacturers continue establishing local production facilities while increasing automation deployment to improve manufacturing efficiency and supply security. Strategic investment in domestic processing capacity, regional logistics, and food technology modernization strengthens the country's position as an important production and distribution hub.

The Savory Snacks Market is led by PepsiCo, Mondelez International, Kellogg, Nestlé, and Calbee, competing directly against strong regional manufacturers that leverage localized flavors, agile pricing, and faster retail execution. The top five companies collectively control approximately 38% of the global market, while regional brands defend share through country-specific product portfolios and efficient distribution. Competition centers on manufacturing automation, premium product innovation, and supply-chain resilience rather than price alone. AI-enabled quality control improves production efficiency by nearly 20%, while automated packaging lowers material waste by about 12%, creating measurable operational advantages. Leading companies are expanding regional manufacturing, forming agricultural sourcing partnerships, and integrating processing with packaging operations to strengthen supply security and shorten replenishment cycles. The competitive landscape is shifting toward premium clean-label products, localized sourcing, and smart manufacturing, increasing pressure on companies dependent on conventional production systems. High capital requirements, retailer shelf competition, and ingredient sourcing complexity remain significant entry barriers. Sustainable success depends on automation leadership, differentiated product innovation, resilient sourcing networks, and rapid commercialization capabilities.

PepsiCo

Mondelez International

Kellogg

Nestlé

Calbee

Intersnack Group

Conagra Brands

Campbell Soup Company

ITC Limited

Hain Celestial Group

Grupo Bimbo

Want Want China Holdings

Arca Continental

Lorenz Snack-World

Food manufacturers are rapidly deploying AI-based quality inspection, automated seasoning systems, and robotic packaging to improve operational consistency and production efficiency. AI-driven visual inspection reduces product defects by approximately 15%, while automated process control improves line efficiency by nearly 20%. More than 65% of large manufacturing facilities are integrating digital production monitoring with enterprise planning platforms, enabling predictive maintenance, real-time quality management, and improved inventory synchronization. These technologies reduce manual intervention, strengthen throughput, and enhance responsiveness to changing retail demand.

Emerging technologies include machine learning-based demand forecasting, digital twins for production optimization, and smart sensor networks that continuously monitor temperature, moisture, and seasoning accuracy. Compared with conventional production environments, integrated smart manufacturing improves equipment utilization by approximately 18% while reducing production waste by nearly 12%. Leading multinational manufacturers benefit most because they possess the infrastructure and investment capacity to scale advanced automation across multiple production sites, creating stronger supply-chain resilience and faster product launches.

Between 2026 and 2028, cloud-connected manufacturing platforms, AI-assisted formulation development, and intelligent warehouse automation will become strategic differentiators across the industry. Companies adopting predictive production planning, automated material handling, and digital traceability will improve operational agility while reducing fulfillment delays. Manufacturers delaying digital transformation risk higher operating costs, slower commercialization, and weaker competitive positioning as intelligent manufacturing becomes the industry benchmark.

March 2024 Mondelez International released its fifth annual State of Snacking report, revealing that 91% of consumers snack daily, reinforcing demand for premium and health-oriented portfolios while guiding future product innovation and category investments.

May 2024 Mondelez International showcased omnichannel merchandising capabilities and collaborative product innovations at the Sweets & Snacks Expo, strengthening digital retail execution and customer engagement across snack categories with expanded omnichannel activation. Source: Mondelez International IR

January 2025 PepsiCo completed its USD 1.2 billion acquisition of Siete Foods, adding products distributed across more than 40,000 retail locations and significantly expanding its better-for-you savory snacks portfolio through strategic portfolio diversification. Source: PepsiCo

April 2025 Mondelez International reported that approximately 96% of its packaging was designed to be recyclable under its Snacking Made Right strategy, strengthening sustainable packaging leadership and reinforcing long-term operational resilience across global snack manufacturing. Source: Mondelez International

The report provides a comprehensive assessment of the global savory snacks industry by evaluating competitive positioning, operational trends, manufacturing strategies, product innovation, and evolving consumer demand. It analyzes key segments including Potato Chips, Extruded Snacks, Popcorn, Nuts & Seeds, and Meat Snacks across Retail Consumption, Foodservice, Convenience Stores, Online Retail, and Vending Machines. End-user coverage includes Households, Restaurants, Hotels, Cafés, and Institutional Catering, supported by analysis across North America, Europe, Asia-Pacific, South America, and the Middle East & Africa.

The study examines technology adoption including AI-enabled manufacturing, robotic packaging, digital quality inspection, and smart supply-chain management, with automation deployment exceeding 65% across major production facilities. It evaluates competitive strategies, regional manufacturing expansion, sustainability initiatives, procurement transformation, and premium product innovation to support investment decisions, market entry planning, capacity expansion, partnership evaluation, and long-term competitive positioning between 2026 and 2033.

| Report Attribute/Metric | Report Details |

|---|---|

Market Revenue in 2025 | USD 139929.5 Million |

Market Revenue in 2033 | USD 214747.92 Million |

CAGR (2026 - 2033) | 5.5% |

Base Year | 2025 |

Forecast Period | 2026 - 2033 |

Historic Period | 2021 - 2025 |

Segments Covered | By Type

By Application

By End-User

|

Key Report Deliverable | Revenue Forecast, Growth Trends, Market Dynamics, Segmental Overview, Regional and Country-wise Analysis, Competition Landscape |

Region Covered | North America, Europe, Asia-Pacific, South America, Middle East, Africa |

Key Players Analyzed | PepsiCo, Mondelez International, Kellogg, Nestlé, Calbee, Intersnack Group, Conagra Brands, Campbell Soup Company, ITC Limited, Hain Celestial Group, Grupo Bimbo, Want Want China Holdings, Arca Continental, Lorenz Snack-World |

Customization & Pricing | Available on Request (10% Customization is Free) |