Reports

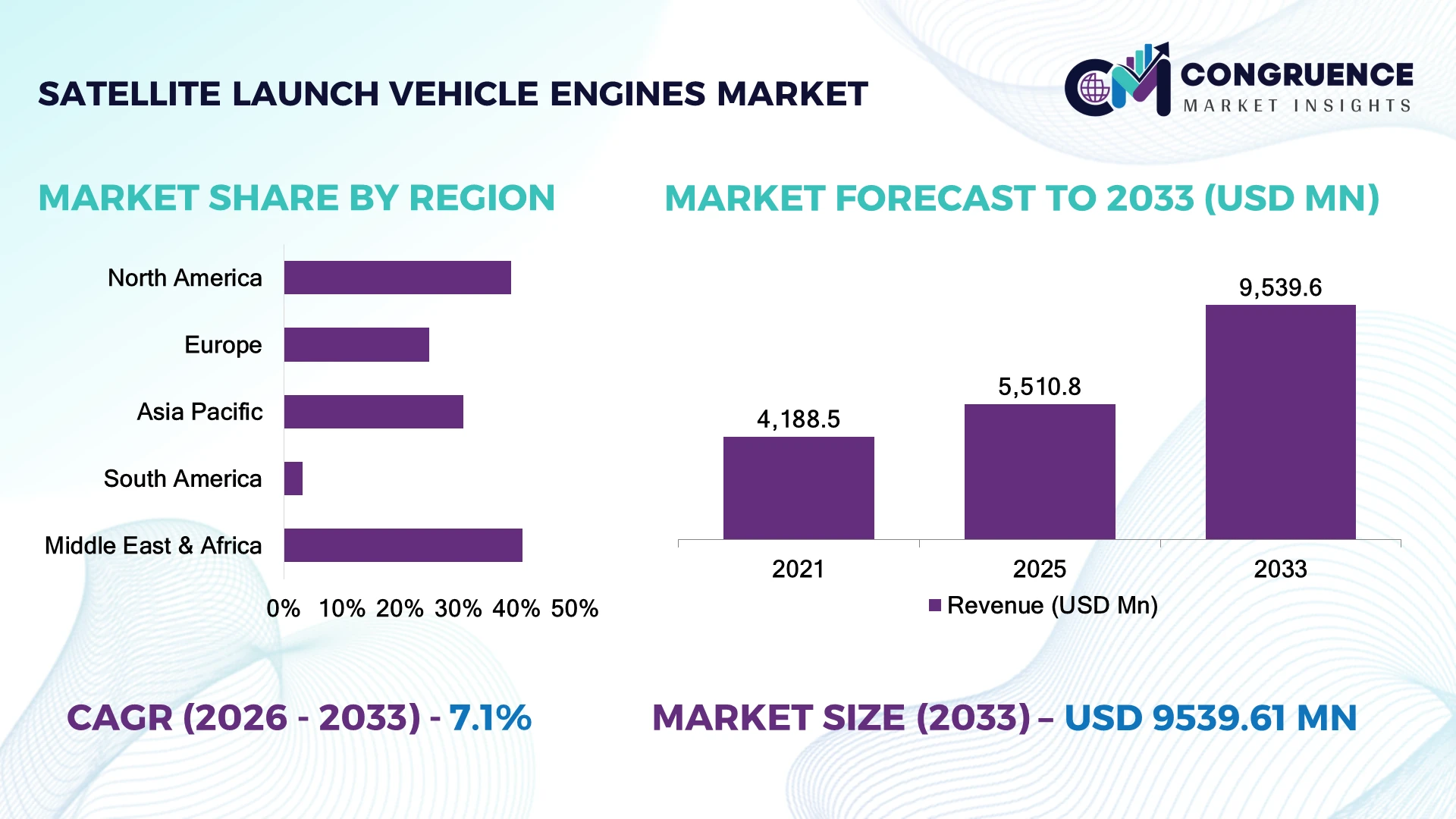

The Global Satellite Launch Vehicle Engines Market was valued at USD 5,510.8 Million in 2025 and is anticipated to reach a value of USD 9,539.6 Million by 2033 expanding at a CAGR of 7.1% between 2026 and 2033. Growth is being driven by increasing reusable launch vehicle programs, expanding satellite constellation deployments, and rapid adoption of high-efficiency cryogenic and methane-fueled propulsion systems.

The United States leads the Satellite Launch Vehicle Engines Market with approximately 42% of global launch engine manufacturing capacity, supported by investments exceeding USD 22 billion across commercial launch systems, defense space programs, and propulsion technologies. Compared with China, the United States maintains stronger commercial launch activity, while China continues expanding state-backed launch infrastructure and engine production. Ongoing geopolitical competition in space access continues accelerating domestic propulsion manufacturing and strategic supply-chain localization.

Strategic investment in reusable propulsion technologies and advanced engine manufacturing capabilities is becoming essential for sustaining long-term launch competitiveness.

Market Size & Growth: Valued at USD 5,510.8 Million in 2025 and projected to reach USD 9,539.6 Million by 2033 at a CAGR of 7.1%, driven by reusable launch systems and satellite constellation expansion.

Top Growth Drivers: Commercial satellite launches (+32%), reusable rocket adoption (+27%), and defense space missions (+21%) accelerate market demand.

Short-Term Forecast: By 2028, engine refurbishment costs decline by 16%, while launch turnaround efficiency improves by approximately 19%.

Emerging Technologies: Methane propulsion, AI-assisted engine diagnostics, and additive manufacturing improve propulsion efficiency by nearly 18%.

Regional Leaders: North America exceeds USD 3.45 Billion, Asia-Pacific approaches USD 2.75 Billion, and Europe surpasses USD 1.86 Billion through launch infrastructure expansion.

Consumer/End-User Trends: Nearly 52% of commercial launch providers prioritize reusable engine architectures for higher launch frequency.

Pilot/Case Example: A 2026 reusable engine validation program reduced refurbishment time by 22% while improving mission readiness by 15%.

Competitive Landscape: The top five manufacturers control approximately 61% market share, led by SpaceX, ArianeGroup, Blue Origin, Aerojet Rocketdyne, and Avio.

Regulatory & ESG Impact: Reusable propulsion systems reduce engine hardware consumption by approximately 24% across repeated launch operations.

Investment & Funding: Industry investments exceed USD 9.1 Billion, driven by propulsion innovation, launch infrastructure expansion, and public-private partnerships.

Innovation & Future Outlook: Reusable methane engines, digital engine control, and additive manufacturing are transforming next-generation launch vehicle propulsion.

Satellite launch vehicle engines are becoming central to commercial space transportation, national security missions, and deep-space exploration as launch providers seek greater reliability and faster mission turnaround. Reusable propulsion systems now support nearly 38% of newly developed launch vehicle programs. Expanding domestic propulsion manufacturing and localized aerospace supply chains are reinforcing technological resilience, creating a strong foundation for the strategic market developments ahead.

The Satellite Launch Vehicle Engines Market has become strategically important as governments and commercial operators compete to expand launch capacity, reduce mission costs, and strengthen sovereign access to space. Rising investments in reusable launch vehicles, defense satellites, and commercial constellation programs are reshaping propulsion development priorities, while supply-chain localization is encouraging domestic production of critical engine components and advanced aerospace materials.

Modern methane-fueled and reusable rocket engines improve operational efficiency by approximately 24% compared with conventional expendable propulsion systems while reducing refurbishment requirements and supporting higher launch frequency. North America leads commercial propulsion innovation and reusable engine deployment, whereas Asia-Pacific continues expanding manufacturing capacity and state-supported launch infrastructure. Over the next two to three years, reusable propulsion technologies are expected to power more than 45% of newly introduced orbital launch systems, improving launch economics and operational flexibility.

Launch providers are increasingly integrating additive manufacturing, digital engine monitoring, and automated production into propulsion development programs to shorten production cycles and improve reliability. Companies are expanding engine testing infrastructure, strengthening strategic supplier partnerships, and investing in next-generation cryogenic and methane propulsion technologies. These initiatives position advanced launch vehicle engines as the cornerstone of competitive space transportation, enabling higher launch cadence, improved operational resilience, and long-term strategic advantage across the global space industry.

Rapid expansion of reusable launch systems is fundamentally transforming propulsion demand as commercial launch providers and national space agencies seek higher launch cadence with lower operational costs. Nearly 49% of newly developed orbital launch programs now incorporate reusable engine architectures, while engine refurbishment technologies reduce turnaround time by approximately 22% and improve fleet utilization by nearly 18%. The United States continues expanding reusable launch infrastructure through commercial space partnerships, encouraging broader adoption of methane-fueled and staged-combustion engines. This transition lowers mission costs while increasing launch availability. Engine manufacturers are responding through additive manufacturing investments, expanded hot-fire testing facilities, strategic propulsion partnerships, and next-generation reusable engine development optimized for frequent orbital missions.

Dependence on high-temperature superalloys, precision turbomachinery components, and aerospace-grade composite materials continues limiting production scalability. Advanced propulsion materials account for nearly 35% of total engine manufacturing costs, while specialized turbopump assemblies increase production complexity by approximately 27%. Export controls affecting strategic aerospace materials and specialized machining equipment have intensified procurement challenges for several engine manufacturers. These structural constraints extend production schedules, increase qualification costs, and reduce manufacturing flexibility. Companies are mitigating risk by localizing critical component manufacturing, qualifying multiple material suppliers, securing long-term procurement agreements, and investing in alternative alloys that maintain propulsion performance while strengthening supply-chain resilience.

Next-generation methane propulsion, digital engineering platforms, and automated production technologies are opening substantial opportunities across commercial and government launch programs. More than 43% of advanced launch vehicle designs now prioritize methane-fueled propulsion, while additive manufacturing reduces engine component production time by approximately 31% and lowers material waste by nearly 24%. Japan is expanding investment in reusable propulsion technologies and digitally integrated aerospace manufacturing to strengthen launch competitiveness. Companies are increasing R&D spending, expanding additive manufacturing capacity, collaborating with advanced materials specialists, and integrating digital twins into engine validation. A significant strategic opportunity lies in designing modular propulsion platforms that simplify maintenance while supporting multiple launch vehicle configurations.

Long-term competitiveness depends on validating propulsion systems capable of consistent performance across repeated launch cycles, extreme thermal environments, and multiple mission profiles. Approximately 38% of propulsion development schedules are dedicated to qualification and verification activities, while integrated engine testing requirements have increased by nearly 25% for reusable launch systems. France continues strengthening propulsion certification standards through advanced aerospace testing programs supporting European launch capabilities. Extended qualification cycles increase development costs, delay commercialization, and complicate production planning. Manufacturers must expand digital simulation capabilities, modernize engine testing infrastructure, strengthen engineering partnerships, and automate verification processes to achieve reliable, repeatable propulsion performance while supporting increasing launch frequency.

Methane Engines Gain Momentum: Commercial launch providers are accelerating deployment of methane-fueled propulsion systems, improving combustion efficiency by approximately 17% while reducing refurbishment requirements by nearly 20%. Expanding reusable launch programs are driving this transition. Manufacturers are increasing cryogenic engine production, scaling testing infrastructure, and strengthening strategic propulsion partnerships.

Additive Manufacturing Expands Production: Aerospace companies are producing increasingly complex engine components through metal additive manufacturing, reducing fabrication time by approximately 34% while lowering material waste by nearly 26%. Supply-chain resilience has become a strategic priority. Engine developers are automating production workflows and expanding digital manufacturing capabilities to improve scalability.

Digital Engine Health Monitoring: AI-assisted diagnostics and digital twin technologies now improve predictive maintenance accuracy by approximately 23% while reducing unexpected engine inspection requirements by nearly 18%. Continuous performance monitoring is shortening operational decision cycles. Companies are integrating intelligent control software and advanced telemetry across reusable propulsion platforms.

Integrated Supply Chain Localization: Domestic production of combustion chambers, turbopumps, and propulsion electronics is expanding as strategic aerospace programs prioritize secure manufacturing. Local sourcing has reduced critical component lead times by approximately 19% while improving production continuity by nearly 16%. Engine manufacturers are restructuring supplier networks and expanding vertically integrated propulsion manufacturing to strengthen long-term launch readiness.

Liquid Propulsion Engines account for approximately 57% of the Satellite Launch Vehicle Engines Market owing to their superior thrust modulation, restart capability, and higher mission flexibility across commercial, defense, and scientific launch programs. Their compatibility with reusable launch vehicles and advanced cryogenic systems makes them the preferred choice for medium- and heavy-lift missions. Methane-fueled liquid engines represent the fastest-growing segment as launch providers prioritize reusability, cleaner combustion, and reduced refurbishment requirements. Solid propulsion engines continue serving defense and tactical launch applications because of their storage stability and rapid launch readiness, while hybrid propulsion systems are gaining strategic interest for small launch vehicles requiring lower operational complexity. Companies are expanding reusable engine programs, investing in additive manufacturing, and strengthening partnerships with launch providers to accelerate next-generation propulsion development.

Investment priorities are steadily shifting toward reusable liquid propulsion platforms supported by digital engine monitoring, lightweight materials, and modular manufacturing that improve operational efficiency while lowering lifecycle costs for orbital launch missions.

According to the 2025 International Astronautical Federation (IAF), reusable liquid propulsion technologies remain the primary focus of new commercial launch vehicle development as operators seek higher launch frequency and lower refurbishment requirements.

Commercial Satellite Launches account for approximately 46% of engine demand, supported by expanding low Earth orbit constellations, broadband connectivity programs, and Earth observation deployments. Frequent launch schedules and increasing payload diversity continue driving demand for highly reliable and reusable propulsion systems. Government and Defense Missions represent the fastest-growing application as countries expand sovereign launch capabilities, missile warning satellites, and secure communication infrastructure. Scientific Exploration missions continue generating demand for high-performance cryogenic propulsion, while technology demonstration launches maintain strategic importance for validating next-generation engine architectures. Nearly 41% of newly developed orbital launch vehicles now incorporate reusable propulsion technologies designed to improve mission economics and operational flexibility.

Manufacturers are expanding engine testing infrastructure, automating production, and strengthening partnerships with satellite operators and launch service providers. Greater integration of digital engineering and modular propulsion systems is improving deployment efficiency across both commercial and government missions.

A 2026 assessment presented through the International Academy of Astronautics highlighted commercial launch services as the largest contributor to global launch activity, reinforcing investment in reusable propulsion technologies.

Commercial Launch Service Providers account for approximately 51% of Satellite Launch Vehicle Engine procurement due to increasing orbital launch frequency, reusable rocket deployment, and expanding satellite constellation programs. Government Space Agencies represent the fastest-growing end-user group as national investments in sovereign launch capability, deep-space exploration, and strategic defense missions continue accelerating. Defense organizations remain major users for dedicated national security launch systems, while research institutions contribute steady demand through technology validation and scientific exploration missions. Approximately 37% of recently announced launch infrastructure investments are directed toward reusable propulsion systems and advanced engine testing facilities.

Engine manufacturers are targeting these customer groups through long-term supply agreements, customized propulsion platforms, strategic co-development programs, and vertically integrated manufacturing. Companies are also expanding after-launch engineering support, digital monitoring capabilities, and propulsion upgrade programs to strengthen customer retention and improve long-term operational performance.

According to the 2025 Space Foundation industry assessment, commercial launch operators continue increasing investment in reusable propulsion infrastructure as launch cadence becomes a primary competitive differentiator.

North America accounted for the largest market share at 39.1% in 2025 however, Asia-Pacific is expected to register the fastest growth, expanding at a CAGR of 8.3% between 2026 and 2033.

Reusable Propulsion Drives Regional Leadership

North America dominates the Satellite Launch Vehicle Engines Market through its extensive commercial launch ecosystem, advanced propulsion manufacturing capabilities, and sustained defense space investments. The region contributes nearly 39% of global market demand, supported by increasing deployment of reusable launch vehicles and expanding satellite constellation programs. Approximately 58% of regional orbital launches now utilize reusable propulsion technologies, significantly improving launch frequency and operational efficiency. Aerospace manufacturers continue expanding hot-fire testing infrastructure, additive manufacturing capacity, and advanced engine assembly facilities while strengthening partnerships between launch providers and propulsion developers to accelerate commercialization of next-generation liquid rocket engines.

United States Market Outlook: The United States leads regional growth through its unmatched launch infrastructure, advanced propulsion R&D ecosystem, and large-scale commercial launch activity. More than 61% of North America's launch engine manufacturing capacity is concentrated in the country, supported by continuous investment in reusable methane engines, digital engine control systems, and vertically integrated aerospace manufacturing. Strong collaboration among commercial launch companies, government agencies, and advanced materials suppliers continues reinforcing long-term propulsion technology leadership.

Advanced Cryogenic Technologies Strengthen Competitiveness

Europe maintains a strong market position through advanced cryogenic propulsion expertise, institutional launch programs, and growing investment in sustainable launch technologies. The region accounts for approximately 25% of global propulsion demand, supported by modernization of heavy-lift launch systems and increasing adoption of reusable engine technologies. Nearly 35% of ongoing propulsion development programs focus on improving engine efficiency, lightweight structures, and digital manufacturing. Aerospace companies continue strengthening industrial partnerships while expanding engine testing and qualification capabilities to enhance launch reliability.

France Market Outlook: France remains Europe's propulsion technology leader through its concentration of aerospace manufacturers, engine development facilities, and launch system integration expertise. The country's advanced cryogenic propulsion programs and extensive industrial supply chain continue supporting European launch independence. Approximately 46% of Europe's large launch vehicle propulsion engineering activities are associated with French aerospace organizations, strengthening innovation across advanced engine platforms.

Expanding Launch Capacity Accelerates Engine Production

Asia-Pacific represents the fastest-growing Satellite Launch Vehicle Engines Market through rapid expansion of domestic launch programs, state-supported aerospace manufacturing, and increasing commercial launch investments. The region contributes approximately 33% of global launch vehicle production activity, encouraging significant expansion of propulsion manufacturing infrastructure. China, India, Japan, and South Korea continue investing in reusable propulsion research, advanced testing facilities, and indigenous engine technologies. Regional manufacturers have improved engine production efficiency by approximately 17% through greater automation and digital manufacturing integration.

China Market Outlook: China leads the regional market through large-scale launch vehicle production, expanding commercial launch capabilities, and integrated propulsion manufacturing infrastructure. More than 55% of Asia-Pacific's orbital launch engine manufacturing activity is concentrated within China, supported by continuous investment in reusable methane engines, advanced cryogenic propulsion, and domestic aerospace supply chains. These capabilities continue strengthening China's long-term competitiveness in global launch services.

National Space Infrastructure Builds Momentum

South America is gradually strengthening its propulsion ecosystem through national satellite programs, launch infrastructure modernization, and aerospace technology investments. Brazil remains the primary regional contributor, supported by continued development of launch facilities and aerospace engineering capabilities. Approximately 19% of regional aerospace investment programs now prioritize propulsion research, launch infrastructure, and advanced manufacturing capabilities. Although dependence on imported propulsion technologies remains significant, strategic international collaborations are improving engineering expertise and supporting future launch capability expansion.

Brazil Market Outlook: Brazil represents the region's leading market through its established aerospace industry, launch infrastructure development, and national satellite initiatives. Continued modernization of propulsion testing capabilities and increased collaboration with international aerospace organizations are strengthening domestic engineering expertise. Growing investment in launch vehicle technologies and advanced aerospace manufacturing continues positioning Brazil as South America's primary propulsion development hub.

Strategic Space Investments Expand Capabilities

The Middle East & Africa market is steadily advancing as governments prioritize satellite infrastructure, national space programs, and aerospace technology investments. Gulf countries continue strengthening institutional space capabilities while increasing investment in advanced engineering partnerships and launch-related technologies. Around 16% of recently announced regional space infrastructure projects include propulsion research, spacecraft engineering, or launch technology development. Strategic international cooperation is accelerating knowledge transfer and strengthening long-term aerospace industrial capabilities.

United Arab Emirates Market Outlook: The United Arab Emirates leads regional market development through sustained investment in national space initiatives, advanced research programs, and international aerospace partnerships. The country's long-term strategy emphasizes technology development, engineering capability, and satellite innovation rather than domestic launch engine manufacturing alone. Continued investment in advanced space technologies and collaborative propulsion research is strengthening its role as the region's leading aerospace innovation center.

Commercial launch leaders including SpaceX, Blue Origin, ArianeGroup, Avio, and Rocket Lab compete directly on reusable propulsion, while government-backed engine developers challenge private manufacturers through sovereign launch programs and domestic production. The top five organizations collectively control approximately 61% of the market. Competition is driven by engine reusability, thrust efficiency, manufacturing speed, and supply-chain control rather than pricing alone. Additive manufacturing reduces engine production time by nearly 30%, reusable propulsion lowers refurbishment requirements by approximately 22%, and vertically integrated manufacturing shortens critical component lead times by around 17%. Companies are expanding engine testing facilities, securing strategic materials, forming propulsion partnerships, and integrating digital manufacturing across production lines. Competitive momentum has shifted toward methane-fueled reusable engines supported by automated production and advanced simulation. Qualification complexity, propulsion testing infrastructure, and specialized materials remain significant entry barriers. Winning requires reusable propulsion expertise, industrial-scale manufacturing, rapid certification, and dependable launch performance.

SpaceX

Blue Origin

ArianeGroup

Avio S.p.A.

Rocket Lab

Firefly Aerospace

Ursa Major

IHI Corporation

Mitsubishi Heavy Industries

Northrop Grumman Corporation

L3Harris Technologies

ISRO Propulsion Complex

Reusable propulsion, methane-fueled combustion, and additive manufacturing are transforming satellite launch vehicle engine development by improving operational efficiency and reducing production complexity. Approximately 54% of next-generation launch engine programs now incorporate reusable architectures, while advanced metal additive manufacturing reduces component production time by nearly 32%. Digital engine health monitoring and AI-assisted combustion optimization further improve propulsion reliability, supporting higher launch cadence across commercial and government missions.

The most significant technology transition is the shift from expendable kerosene propulsion toward reusable methane-fueled engines. Compared with conventional expendable propulsion systems, reusable methane engines reduce refurbishment effort by approximately 24% while improving operational efficiency by nearly 20%. Commercial launch providers and vertically integrated aerospace manufacturers gain the strongest competitive advantage through lower lifecycle costs, faster launch preparation, and simplified maintenance. Digital twin simulation and automated hot-fire diagnostics are further accelerating engine validation while reducing development cycles.

Between 2026 and 2028, full-flow staged combustion, advanced ceramic composites, and intelligent engine control systems will redefine propulsion competitiveness. Reusable engine deployment is expected to exceed 50% across newly introduced orbital launch platforms. Companies investing in automated manufacturing, advanced materials, and integrated propulsion testing infrastructure will improve production scalability, strengthen supply resilience, and secure leadership as rapid launch responsiveness becomes the defining competitive advantage.

November 2024 – ArianeGroup secured European Space Agency contracts to advance the reusable Prometheus engine and Themis demonstrator, supporting a 120-ton thrust-class reusable engine program that strengthens Europe's reusable launch capability. Source: ArianeGroup

June 2025 – ArianeGroup signed a CNES contract to develop a next-generation methalox engine delivering 200–300 tons of thrust using full-flow staged combustion technology, significantly expanding Europe's heavy-lift propulsion roadmap. Source: ArianeGroup

July 2025 – ArianeGroup successfully demonstrated four consecutive ignitions of its reusable Prometheus rocket engine during hot-fire testing, validating rapid restart capability and accelerating reusable propulsion maturity for future launch vehicles. Source: European Space Agency

January 2025 – Blue Origin successfully placed the New Glenn launch vehicle into orbit during its inaugural mission using seven BE-4 engines, demonstrating orbital capability and strengthening competition within the commercial heavy-lift launch market. Source: Reuters.

This report provides comprehensive analysis of the Satellite Launch Vehicle Engines Market across propulsion types, launch applications, end-users, and major geographic regions. It evaluates liquid, solid, hybrid, and reusable propulsion technologies while assessing deployment across commercial satellite launches, government missions, defense programs, and scientific exploration. The study examines engine architecture, manufacturing technologies, propulsion testing, reusable systems, and competitive participation across leading aerospace manufacturers. More than 60% of market activity is concentrated within reusable and liquid propulsion technologies, reflecting ongoing modernization across the global launch industry.

The report delivers strategic insights supporting investment planning, propulsion technology selection, manufacturing expansion, and competitive positioning between 2026 and 2033. It evaluates regional propulsion capabilities, launch infrastructure, advanced manufacturing adoption, and emerging opportunities in methane engines, additive manufacturing, and digital propulsion engineering. Coverage extends to reusable launch systems, cryogenic propulsion, intelligent engine monitoring, and next-generation testing capabilities, enabling stakeholders to identify high-value growth opportunities, operational priorities, and long-term competitive strategies across the evolving global space transportation ecosystem.

| Report Attribute/Metric | Report Details |

|---|---|

|

Market Revenue in 2025 |

USD 5,510.8 Million |

|

Market Revenue in 2033 |

USD 9,539.6 Million |

|

CAGR (2026 - 2033) |

7.1% |

|

Base Year |

2025 |

|

Forecast Period |

2026 - 2033 |

|

Historic Period |

2021 - 2025 |

|

Segments Covered |

By Type

By Application

By End-User

|

|

Key Report Deliverable |

Revenue Forecast, Growth Trends, Market Dynamics, Segmental Overview, Regional and Country-wise Analysis, Competition Landscape |

|

Region Covered |

North America, Europe, Asia-Pacific, South America, Middle East, Africa |

|

Key Players Analyzed |

SpaceX, Blue Origin, ArianeGroup, Avio S.p.A., Rocket Lab, Firefly Aerospace, Ursa Major, IHI Corporation, Mitsubishi Heavy Industries, Northrop Grumman Corporation, L3Harris Technologies, ISRO Propulsion Complex |

|

Customization & Pricing |

Available on Request (10% Customization is Free) |