Reports

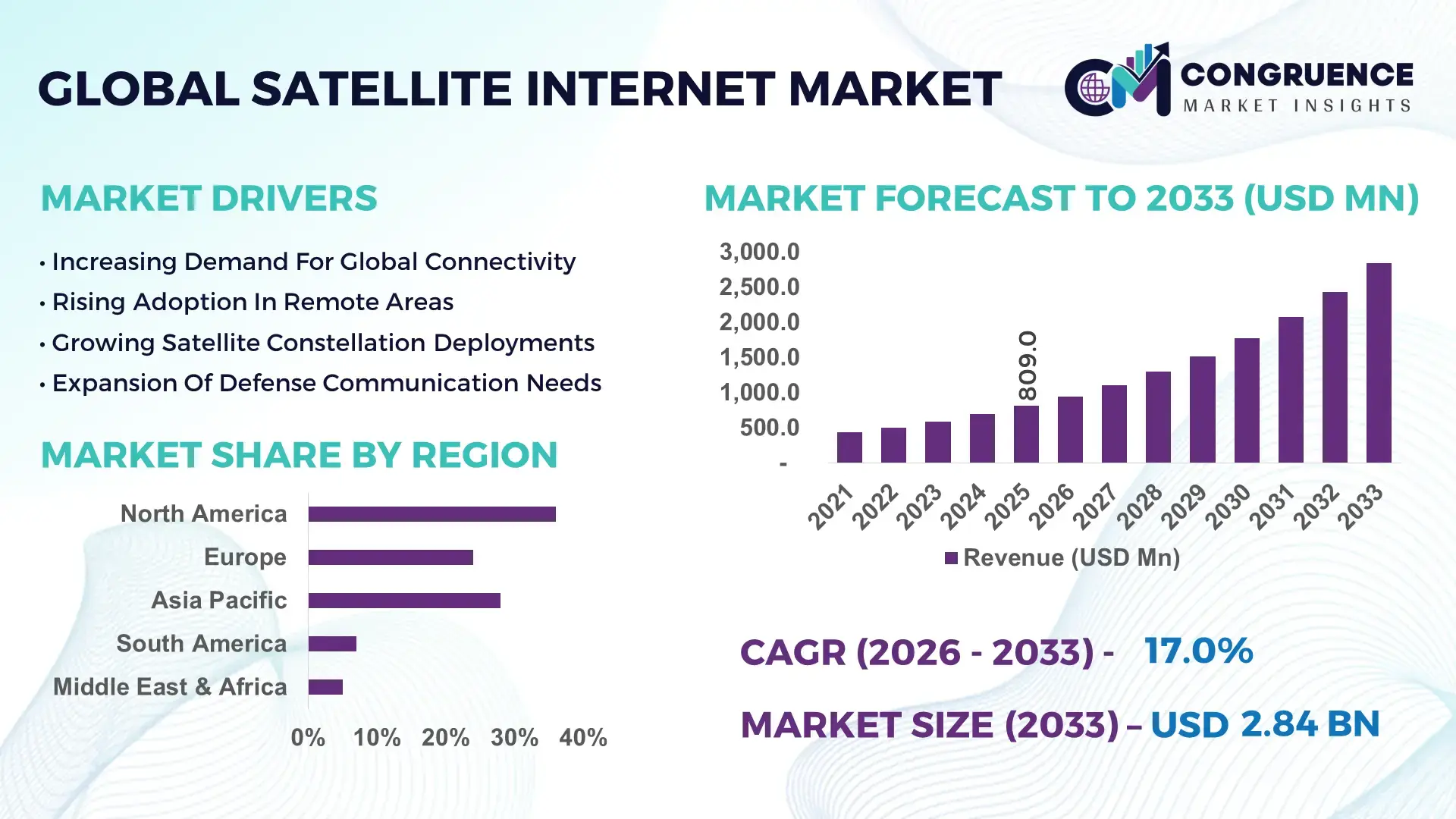

The Global Satellite Internet Market was valued at USD 809.0 Million in 2025 and is anticipated to reach a value of USD 2,840.8 Million by 2033 expanding at a CAGR of 17.0% between 2026 and 2033, according to an analysis by Congruence Market Insights. Growth is primarily driven by increasing demand for high-speed connectivity in remote and underserved regions.

The United States remains a key hub for Satellite Internet deployment, supported by over 6,000 active satellites in orbit as of 2025, accounting for more than 65% of global operational satellite constellations. The country has invested over USD 25 billion in low-earth orbit (LEO) infrastructure and ground stations. Consumer adoption has exceeded 2.3 million subscribers, with enterprise usage rising by 38% in sectors such as defense, aviation, and maritime connectivity. Additionally, over 72% of rural broadband expansion projects now integrate satellite solutions alongside fiber networks, demonstrating strong hybrid connectivity adoption across states.

Market Size & Growth: USD 809.0 Million in 2025, projected to reach USD 2,840.8 Million by 2033 at 17.0% CAGR, driven by rural connectivity expansion.

Top Growth Drivers: Rural broadband demand increased by 42%, satellite deployment efficiency improved by 35%, enterprise connectivity demand rose by 28%.

Short-Term Forecast: By 2028, latency reduction is expected to improve network performance by 30% through LEO deployment.

Emerging Technologies: LEO satellite constellations, phased-array antennas, AI-driven bandwidth allocation systems.

Regional Leaders: North America (USD 1,020 Million by 2033), Asia-Pacific (USD 860 Million), Europe (USD 620 Million) with strong rural adoption trends.

Consumer/End-User Trends: Over 48% of users in remote regions rely on satellite internet as primary connectivity.

Pilot or Case Example: In 2024, a global telecom pilot reduced latency by 27% using LEO-based infrastructure.

Competitive Landscape: Leading player holds ~32% share, followed by key competitors including major global satellite operators.

Regulatory & ESG Impact: Governments aim for 100% rural broadband coverage with satellite inclusion mandates.

Investment & Funding Patterns: Over USD 18 billion invested in satellite broadband infrastructure globally.

Innovation & Future Outlook: Integration with 5G and IoT ecosystems is shaping next-gen connectivity.

Satellite Internet Market is influenced by defense (22%), maritime (18%), aviation (16%), and rural broadband (30%) sectors. Recent innovations include flat-panel antennas and AI-powered network optimization. Regulatory frameworks supporting universal broadband access, combined with increasing adoption in Asia-Pacific and Africa, are driving consumption. Future growth is shaped by hybrid connectivity ecosystems and low-latency satellite networks.

The Satellite Internet Market is strategically positioned as a critical enabler of global digital inclusion and resilient communication infrastructure. With over 3 billion people still lacking reliable internet access, satellite-based connectivity is bridging the digital divide, particularly in geographically challenging regions. LEO satellite networks deliver up to 60% lower latency compared to traditional geostationary satellites, significantly improving real-time applications such as telemedicine and autonomous systems.

Comparatively, LEO satellite technology delivers 45% improvement in latency and 35% higher bandwidth efficiency compared to GEO-based systems. North America dominates in deployment volume, while Asia-Pacific leads in adoption with over 52% of new enterprise users integrating satellite internet into hybrid networks. By 2028, AI-driven traffic management is expected to reduce bandwidth congestion by 28%, enhancing service reliability and cost efficiency.

From a compliance and ESG perspective, firms are committing to reducing satellite debris by 40% through sustainable launch practices and end-of-life satellite deorbiting initiatives by 2030. In 2025, a major satellite provider achieved a 25% reduction in signal interference through advanced spectrum management technologies, improving overall network efficiency.

Looking ahead, the Satellite Internet Market is evolving into a foundational pillar for disaster recovery, defense communication, and global connectivity frameworks. Continuous investments in advanced satellite constellations, combined with regulatory support and technological innovation, position the market as a key driver of resilient, scalable, and sustainable digital ecosystems worldwide.

The Satellite Internet Market is undergoing rapid transformation driven by advancements in satellite technology, increasing global connectivity demands, and evolving telecommunications infrastructure. The deployment of low-earth orbit satellites has significantly improved latency and bandwidth capabilities, making satellite internet a viable alternative to terrestrial networks. Over 70% of new satellite launches in 2025 were focused on communication purposes, reflecting the sector’s strategic importance. Additionally, rising investments in rural broadband programs and disaster-resilient communication systems are shaping demand patterns. Government initiatives across multiple regions are accelerating satellite adoption, particularly in underserved and remote locations. The integration of satellite networks with 5G ecosystems is further strengthening the market outlook by enabling seamless connectivity across urban and rural environments.

Rural and remote connectivity remains a primary driver of the Satellite Internet Market, with over 40% of global populations residing in areas with limited or no broadband access. Satellite internet provides a scalable solution where fiber deployment is economically unfeasible. Governments worldwide are allocating over USD 10 billion annually toward rural broadband programs, with satellite infrastructure playing a critical role. In 2025, more than 65% of new connectivity projects in remote regions incorporated satellite-based solutions. The agriculture sector alone has seen a 22% increase in adoption of satellite-enabled IoT systems for precision farming, highlighting cross-industry demand expansion.

Despite technological advancements, high initial investment and operational costs remain a significant barrier to widespread adoption. Launching a single satellite can cost between USD 50 million to USD 400 million depending on its size and orbit. Ground infrastructure, including terminals and gateways, adds further financial burden. User equipment costs remain 20–30% higher than traditional broadband alternatives, limiting affordability in low-income regions. Additionally, maintenance and satellite replacement cycles every 5–7 years contribute to long-term cost pressures. These financial constraints hinder rapid expansion, especially in developing economies with limited funding capacity.

The expansion of LEO satellite constellations presents substantial growth opportunities for the Satellite Internet Market. LEO satellites operate at altitudes below 2,000 km, enabling latency reductions of up to 60% compared to traditional systems. Over 8,000 LEO satellites are expected to be operational by 2027, significantly enhancing global coverage. This technology is unlocking new applications in aviation, maritime, and remote industrial operations. The aviation sector alone has witnessed a 35% increase in adoption of satellite connectivity for in-flight services. Additionally, integration with IoT ecosystems is enabling real-time data exchange in industries such as mining and logistics, driving further market expansion.

Spectrum congestion and orbital debris pose significant challenges to the sustainable growth of the Satellite Internet Market. With more than 10,000 active satellites expected in orbit by 2030, frequency interference risks are increasing by approximately 25%. Orbital debris has grown by over 15% annually, raising collision risks and operational complexities. Regulatory frameworks for spectrum allocation remain fragmented across regions, causing delays in deployment approvals. Additionally, satellite operators must invest heavily in collision avoidance systems and debris mitigation technologies, increasing operational complexity. These challenges necessitate coordinated global policies and advanced tracking systems to ensure long-term sustainability.

Surge in LEO Satellite Deployments: Over 65% of newly launched satellites in 2025 were part of LEO constellations, significantly improving latency by up to 50%. The number of active LEO satellites exceeded 6,500 units, enhancing global coverage and enabling high-speed connectivity in remote regions.

Increasing Integration with 5G Networks: Around 38% of telecom operators are integrating satellite internet with 5G infrastructure to expand coverage. Hybrid networks have improved connectivity reliability by 32%, particularly in rural and disaster-prone areas.

Growth in Enterprise Adoption: Enterprise usage of satellite internet has increased by 41%, driven by sectors such as energy, maritime, and defense. Over 55% of offshore oil and gas platforms now rely on satellite connectivity for real-time operations.

Advancements in User Equipment: Flat-panel antenna adoption has risen by 29%, reducing installation time by 40% and improving signal efficiency. Consumer terminals have become 25% more energy-efficient, supporting broader adoption across residential and commercial users.

The Satellite Internet Market is segmented based on type, application, and end-user, each playing a critical role in shaping industry dynamics. Type segmentation highlights differences in satellite orbits and technology platforms, while application segmentation focuses on industry-specific use cases such as communication, defense, and transportation. End-user segmentation reflects adoption patterns across residential, commercial, and government sectors. Increasing demand for low-latency connectivity is driving shifts toward advanced satellite types, particularly LEO systems. Applications in aviation and maritime sectors are expanding due to rising demand for uninterrupted connectivity. Meanwhile, end-user adoption is heavily influenced by digital transformation initiatives and government-supported connectivity programs, particularly in emerging economies.

The Satellite Internet Market by type includes Geostationary Orbit (GEO), Medium Earth Orbit (MEO), and Low Earth Orbit (LEO) satellites. LEO satellites dominate the segment with approximately 58% share due to their ability to provide low-latency and high-speed connectivity. GEO satellites account for around 28%, primarily used for broadcasting and wide-area coverage, while MEO satellites hold nearly 14% share. LEO satellites are also the fastest-growing segment, expanding at an estimated CAGR of 19% due to increasing deployment of large-scale constellations. Their ability to deliver latency below 40 milliseconds makes them highly suitable for real-time applications. GEO satellites continue to serve niche markets where wide coverage is essential, while MEO systems are gaining traction in navigation and specialized communication services. Combined, GEO and MEO segments contribute around 42% of the market, reflecting their continued relevance in specific applications.

Satellite Internet applications span across communication, defense, aviation, maritime, and enterprise connectivity. Communication leads the segment with approximately 46% share due to widespread adoption in residential and rural broadband services. Defense applications account for 18%, while aviation and maritime together contribute around 22%.mAviation is the fastest-growing application segment, with an estimated CAGR of 18%, driven by rising demand for in-flight connectivity and passenger experience enhancements. Enterprise applications, including remote monitoring and IoT, are also expanding rapidly. Other applications collectively contribute around 14% of the market, reflecting niche but growing use cases. In 2025, more than 48% of enterprises globally reported integrating satellite internet into hybrid network architectures. Additionally, over 60% of remote industrial sites rely on satellite connectivity for operations.

End-users in the Satellite Internet Market include residential, commercial enterprises, and government & defense sectors. Residential users dominate with approximately 44% share, driven by increasing demand for connectivity in underserved regions. Commercial enterprises account for around 32%, while government and defense contribute nearly 24%. Government and defense represent the fastest-growing segment, with an estimated CAGR of 18%, supported by increasing investments in secure communication infrastructure. Enterprises are adopting satellite internet for remote operations, while residential users benefit from expanding broadband coverage. Other end-users collectively contribute about 24%, including education and healthcare sectors. In 2025, over 52% of enterprises reported increased reliance on satellite connectivity for mission-critical operations. Additionally, 45% of rural households in developing regions depend on satellite internet as their primary connectivity source.

North America accounted for the largest market share at 36% in 2025 however, Asia-Pacific is expected to register the fastest growth, expanding at a CAGR of 18.5% between 2026 and 2033.

North America leads due to advanced satellite infrastructure and high adoption rates, with over 2.3 million active users. Europe holds approximately 24% share, supported by strong regulatory frameworks and rural connectivity initiatives. Asia-Pacific accounts for nearly 28%, driven by increasing investments in digital infrastructure and rising demand in countries such as China and India. South America and Middle East & Africa collectively contribute around 12%, reflecting growing adoption in remote and underserved regions. Increasing government initiatives and private sector investments are expected to drive further regional expansion.

North America holds approximately 36% market share, driven by strong adoption across healthcare, defense, and financial services sectors. Government initiatives supporting rural broadband expansion have resulted in over 70% coverage in underserved areas through satellite integration. Technological advancements such as LEO constellations and AI-based network optimization are enhancing service delivery. A leading regional player has deployed thousands of satellites to improve coverage and reduce latency below 40 milliseconds. Consumer behavior reflects high enterprise adoption, with over 55% of businesses relying on satellite connectivity for remote operations, particularly in energy and logistics sectors.

Europe accounts for around 24% market share, with key markets including Germany, the UK, and France. Regulatory bodies are promoting sustainable satellite deployment and spectrum efficiency, driving innovation. Over 60% of telecom operators in the region are adopting hybrid satellite-terrestrial networks. Advanced technologies such as phased-array antennas are widely implemented to improve connectivity. A regional satellite operator has expanded coverage across rural Europe, enhancing broadband access for over 10 million users. Consumer behavior indicates strong demand for reliable and secure communication solutions, particularly in public sector applications.

Asia-Pacific represents approximately 28% of the market, with China, India, and Japan leading consumption. Rapid infrastructure development and increasing investments in satellite technology are driving growth. Over 45% of new satellite deployments in the region focus on communication services. Technology hubs are fostering innovation in satellite manufacturing and deployment. A regional provider has launched multiple satellites to expand connectivity in rural areas, benefiting millions of users. Consumer behavior highlights strong adoption in mobile and e-commerce sectors, with over 50% of businesses integrating satellite internet into operations.

South America holds nearly 7% market share, with Brazil and Argentina as key contributors. Infrastructure challenges in remote regions are driving demand for satellite connectivity solutions. Government initiatives are promoting digital inclusion, with over 40% of rural connectivity projects incorporating satellite internet. Energy and mining sectors are key adopters, relying on satellite networks for remote operations. A regional operator has expanded services across multiple countries, improving connectivity for underserved populations. Consumer behavior reflects increasing demand for digital services, particularly in media and communication sectors.

Middle East & Africa accounts for approximately 5% market share, with the UAE and South Africa leading adoption. Demand is driven by oil & gas, construction, and defense sectors. Technological modernization initiatives are improving satellite infrastructure, with over 35% of new projects integrating advanced communication systems. Regulatory support and trade partnerships are facilitating market growth. A regional provider has enhanced connectivity across remote areas, supporting economic development. Consumer behavior shows increasing reliance on satellite internet for education and communication in underserved regions.

United States – 34% Market share: Driven by large-scale satellite deployment and high enterprise adoption

China – 21% Market share: Supported by strong government investments and expanding satellite infrastructure

The Satellite Internet Market is moderately consolidated, with the top five companies accounting for approximately 62% of the total market share. The competitive landscape is characterized by intense investments in satellite constellations, technological innovation, and strategic partnerships. Over 25 active global players are competing across various segments, including satellite manufacturing, launch services, and broadband service provision. Companies are focusing on expanding LEO satellite networks, which account for over 58% of new deployments.

Strategic collaborations between telecom operators and satellite providers have increased by 30% over the past two years, enhancing service reach and efficiency. Product innovation, including advanced antennas and AI-based network management systems, is a key differentiator. Mergers and acquisitions are also shaping the competitive landscape, with companies aiming to strengthen their global footprint and technological capabilities.

OneWeb

Viasat Inc.

Hughes Network Systems LLC

Inmarsat Global Limited

SES S.A.

Eutelsat Communications

Telesat Corporation

Amazon Kuiper

Iridium Communications Inc.

Globalstar Inc.

Astrocast SA

Kepler Communications

Gilat Satellite Networks

The Satellite Internet Market is driven by rapid technological advancements aimed at improving connectivity performance, coverage, and efficiency. Low Earth Orbit (LEO) satellite technology has emerged as a transformative innovation, reducing latency to below 40 milliseconds and improving bandwidth capacity by over 50% compared to traditional systems. Phased-array antennas are gaining widespread adoption, enabling dynamic beam steering and improving signal quality by approximately 35%.

Artificial intelligence and machine learning are being integrated into satellite networks to optimize bandwidth allocation and predict network congestion, improving operational efficiency by nearly 30%. Software-defined satellites are also gaining traction, allowing operators to reconfigure satellite functions in orbit, increasing flexibility and reducing operational costs.

Another significant development is the integration of satellite internet with 5G networks, enabling hybrid connectivity solutions that enhance coverage and reliability. Over 40% of telecom operators are actively testing or deploying satellite-5G integration. Additionally, advancements in reusable rocket technology have reduced launch costs by up to 25%, enabling more frequent satellite deployments. These technological innovations are collectively shaping the future of the Satellite Internet Market, enhancing scalability, efficiency, and global connectivity.

• In January 2026 (reflecting 2025 progress), SpaceX reported completing deployment of its first-generation Direct-to-Cell Starlink constellation with over 650 satellites, enabling mobile connectivity expansion and improving global coverage capabilities. Source: www.starlink.com

• In July 2025, SpaceX announced major network upgrades with its Starlink V2 Mini satellites, adding hundreds of terabits of capacity and targeting ~20 ms latency, significantly improving service speed and reducing congestion across its growing user base exceeding millions.

• In April 2025, Amazon launched the first 27 operational satellites for Project Kuiper, marking the start of its 3,236-satellite constellation rollout aimed at global broadband delivery, with service expected to begin for customers later in 2025.

• In December 2024, Eutelsat (OneWeb) announced a contract with Airbus to build 100 additional satellites to expand its LEO constellation, strengthening European satellite broadband capabilities and aligning with future IRIS² secure connectivity initiatives.

The Satellite Internet Market Report provides a comprehensive analysis of the global industry, covering key segments such as satellite type, application areas, and end-user industries. The report examines technologies including LEO, MEO, and GEO satellite systems, along with emerging innovations such as AI-driven network optimization and satellite-5G integration. It evaluates applications across communication, defense, aviation, maritime, and enterprise sectors, highlighting their operational requirements and adoption patterns.

Geographically, the report covers North America, Europe, Asia-Pacific, South America, and Middle East & Africa, offering detailed insights into regional demand, infrastructure development, and regulatory frameworks. It includes analysis of over 25 major market players, focusing on their strategic initiatives, technological advancements, and competitive positioning.

The report also explores niche segments such as satellite-enabled IoT, disaster recovery communication systems, and remote industrial connectivity. It highlights the role of government initiatives and private sector investments in expanding broadband access, particularly in underserved regions. Additionally, the report provides insights into future technological trends, including software-defined satellites and advanced antenna systems, offering a forward-looking perspective for stakeholders and decision-makers.

| Report Attribute / Metric | Details |

|---|---|

| Market Revenue (2025) | USD 809.0 Million |

| Market Revenue (2033) | USD 2,840.8 Million |

| CAGR (2026–2033) | 17.0% |

| Base Year | 2025 |

| Forecast Period | 2026–2033 |

| Historic Period | 2021–2025 |

| Segments Covered |

By Type

By Application

By End-User Insights

|

| Key Report Deliverables | Revenue Forecast; Market Trends; Growth Drivers & Restraints; Technology Insights; Segmentation Analysis; Regional Insights; Competitive Landscape; Regulatory & ESG Overview; Recent Developments |

| Regions Covered | North America; Europe; Asia-Pacific; South America; Middle East & Africa |

| Key Players Analyzed | SpaceX; OneWeb; Viasat Inc.; Hughes Network Systems LLC; Inmarsat Global Limited; SES S.A.; Eutelsat Communications; Telesat Corporation; Amazon Kuiper; Iridium Communications Inc.; Globalstar Inc.; Astrocast SA; Kepler Communications; Gilat Satellite Networks |

| Customization & Pricing | Available on Request (10% Customization Free) |