Reports

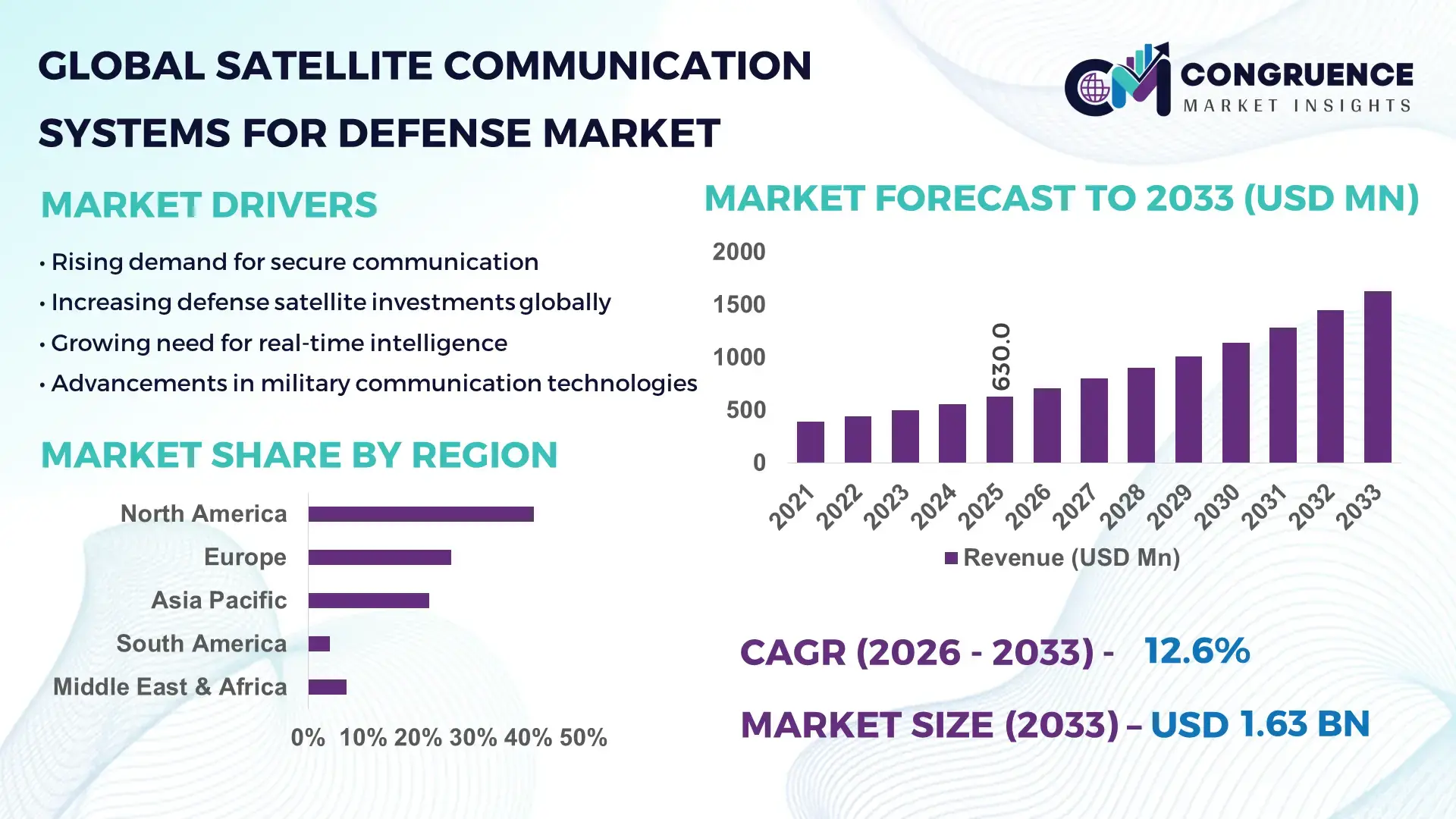

The Global Satellite Communication Systems for Defense Market was valued at USD 630.0 Million in 2025 and is anticipated to reach a value of USD 1,628.0 Million by 2033 expanding at a CAGR of 12.6% between 2026 and 2033, according to an analysis by Congruence Market Insights. The growth is primarily driven by increasing demand for secure, real-time battlefield communication and enhanced situational awareness across modern defense operations.

The United States leads the Satellite Communication Systems for Defense Market with significant advancements in military satellite infrastructure and defense-grade communication networks. The country operates over 180 military and dual-use satellites, accounting for nearly 45% of global defense satellite deployments. Annual defense space investments exceed USD 30 billion, with major programs focusing on protected communications, low Earth orbit (LEO) constellations, and anti-jamming technologies. Approximately 62% of U.S. defense communication systems rely on satellite-based platforms for mission-critical operations. Additionally, over 70% of modern defense applications—including intelligence, surveillance, reconnaissance (ISR), and unmanned systems—integrate satellite communication systems to ensure uninterrupted connectivity and data exchange across global theaters.

Market Size & Growth: Valued at USD 630.0 Million in 2025, projected to reach USD 1,628.0 Million by 2033, growing at 12.6% CAGR due to rising defense digitization and secure communication needs.

Top Growth Drivers: Secure communication adoption increased by 48%, ISR dependency rose by 52%, satellite-enabled UAV operations improved by 46%.

Short-Term Forecast: By 2028, latency reduction is expected to improve by 35% through LEO satellite deployments.

Emerging Technologies: Integration of AI-driven signal processing, software-defined satellites, and quantum encryption protocols.

Regional Leaders: North America (USD 680M by 2033) leads in innovation; Asia-Pacific (USD 420M) sees rapid deployment; Europe (USD 360M) focuses on defense autonomy.

Consumer/End-User Trends: Defense agencies account for over 75% of usage, with growing reliance on unmanned systems and real-time analytics.

Pilot or Case Example: In 2025, a NATO pilot reduced communication latency by 28% using hybrid satellite-terrestrial networks.

Competitive Landscape: Market leader holds ~24% share, followed by 4–5 key players with strong defense contracts.

Regulatory & ESG Impact: Governments enforcing secure spectrum usage and targeting 20% reduction in energy consumption in satellite operations by 2030.

Investment & Funding Patterns: Over USD 18 billion invested globally in defense satellite programs between 2023–2025.

Innovation & Future Outlook: Increasing adoption of multi-orbit satellite architectures and autonomous network management systems.

Satellite Communication Systems for Defense Market is driven by aerospace, military intelligence, and surveillance sectors contributing over 65% combined share. Advances in anti-jamming technologies and AI-based communication protocols are enhancing operational efficiency by 30%. Regulatory focus on secure spectrum allocation and rising defense budgets in Asia-Pacific and Europe are influencing growth. Increasing adoption of LEO constellations and hybrid communication models is shaping future deployment strategies.

The Satellite Communication Systems for Defense Market plays a critical role in enabling secure, resilient, and real-time communication for modern military operations. With over 68% of global defense operations relying on satellite-enabled connectivity, these systems are integral to intelligence gathering, command coordination, and mission-critical data transfer. The adoption of software-defined satellites delivers 40% improvement in bandwidth flexibility compared to traditional fixed-architecture satellites, enabling dynamic reconfiguration during operations.

North America dominates in volume, while Asia-Pacific leads in adoption with over 58% of defense modernization programs integrating satellite communication technologies. The increasing deployment of low Earth orbit (LEO) constellations is reshaping communication latency and coverage capabilities. By 2028, AI-driven network optimization is expected to improve communication efficiency by 35% while reducing operational downtime by 25%.

From a compliance and ESG perspective, defense organizations are committing to sustainability goals, targeting 22% reduction in satellite energy consumption and improved lifecycle management by 2030. In 2025, the United States achieved a 30% improvement in secure communication resilience through the deployment of hybrid multi-orbit satellite systems integrating LEO and GEO architectures.

Strategically, the market is evolving toward autonomous, AI-enabled satellite networks that enhance mission agility and resilience. The Satellite Communication Systems for Defense Market is expected to remain a cornerstone of defense infrastructure, supporting secure operations, regulatory compliance, and sustainable technological advancement globally.

The Satellite Communication Systems for Defense Market is shaped by increasing geopolitical tensions, rising defense budgets, and the growing need for secure, high-speed communication systems. Over 70% of modern military operations now depend on satellite-based connectivity for intelligence, surveillance, reconnaissance (ISR), and battlefield coordination. The transition from traditional geostationary satellites to multi-orbit architectures, including low Earth orbit (LEO) and medium Earth orbit (MEO), is enhancing coverage and reducing latency by up to 40%. Additionally, more than 60% of defense organizations are integrating AI-enabled communication systems to optimize bandwidth allocation and improve network resilience. The market is also influenced by the increasing deployment of unmanned aerial vehicles (UAVs), with over 55% of UAV operations relying on satellite communication systems. Furthermore, spectrum congestion and cybersecurity threats are driving investments in advanced encryption and anti-jamming technologies, which are now implemented in approximately 48% of newly deployed systems globally.

The demand for secure and real-time communication has become a critical driver in the Satellite Communication Systems for Defense Market, with over 72% of defense operations requiring uninterrupted connectivity across remote and hostile environments. Satellite communication systems enable encrypted data transmission, reducing interception risks by nearly 45% compared to conventional communication systems. The rise in intelligence, surveillance, and reconnaissance (ISR) missions—accounting for over 60% of defense communication usage—has further accelerated adoption. Additionally, modern warfare strategies emphasize network-centric operations, where real-time data exchange improves decision-making efficiency by approximately 35%. The increasing deployment of unmanned systems, including drones and autonomous vehicles, has also contributed to demand, with nearly 58% of these systems relying on satellite links for navigation and control. Governments worldwide are investing heavily in secure satellite networks, leading to a 50% increase in advanced encryption integration across new defense communication platforms.

High infrastructure and deployment costs remain a major restraint for the Satellite Communication Systems for Defense Market, as satellite development, launch, and maintenance require substantial capital investment. The cost of deploying a single defense-grade satellite can exceed USD 200 million, while launch expenses alone account for nearly 30–35% of total project costs. Additionally, ground station infrastructure and maintenance contribute to over 25% of operational expenses. Smaller economies face challenges in allocating defense budgets toward satellite communication systems, limiting adoption rates. Furthermore, the complexity of integrating advanced encryption and anti-jamming technologies increases system costs by approximately 20%. Lifecycle management, including satellite replacement every 10–15 years, adds to financial pressure. These high costs often delay procurement decisions, particularly in emerging economies where defense spending is constrained.

The expansion of low Earth orbit (LEO) satellite constellations presents significant opportunities for the Satellite Communication Systems for Defense Market by enhancing communication speed, coverage, and reliability. LEO satellites operate at altitudes below 2,000 km, reducing latency by up to 50% compared to traditional geostationary satellites. Over 65% of new satellite deployments are focused on LEO constellations, enabling real-time data transmission critical for defense operations. These systems also provide global coverage, supporting remote and mobile military units. Additionally, the integration of LEO satellites with existing geostationary infrastructure is improving network resilience by 40%. Defense organizations are increasingly investing in multi-orbit architectures, with over 55% planning to deploy hybrid communication systems within the next five years. This shift creates opportunities for technology providers to develop scalable and cost-efficient satellite communication solutions tailored to defense applications.

Cybersecurity threats and spectrum congestion pose significant challenges to the Satellite Communication Systems for Defense Market, as increasing reliance on satellite networks makes them vulnerable to cyberattacks and signal interference. Approximately 47% of defense communication systems have reported attempted cyber intrusions, highlighting the need for robust security frameworks. Advanced jamming techniques can disrupt satellite signals, affecting nearly 30% of communication reliability in high-risk zones. Additionally, spectrum congestion has intensified due to the rapid increase in satellite launches, with over 8,000 active satellites competing for limited frequency bands. This congestion can reduce signal quality and increase latency by up to 20%. Regulatory constraints on spectrum allocation further complicate deployment, especially in densely populated regions. Addressing these challenges requires continuous investment in encryption technologies, spectrum management solutions, and resilient communication architectures.

Rapid adoption of multi-orbit satellite architectures: Over 62% of defense communication networks are transitioning to multi-orbit systems integrating LEO, MEO, and GEO satellites, improving coverage redundancy by 45% and reducing communication downtime by 30% in mission-critical operations.

Increasing integration of AI in satellite communication systems: Nearly 58% of defense organizations have implemented AI-based signal optimization tools, enhancing bandwidth utilization efficiency by 35% and reducing network congestion by 28% across deployed systems.

Growth in anti-jamming and secure communication technologies: Approximately 48% of newly deployed satellite systems now include advanced anti-jamming capabilities, increasing signal reliability by 40% in high-risk environments and reducing interception risks by 33%.

Expansion of LEO satellite constellations for defense use: Over 65% of planned satellite launches for defense purposes focus on LEO constellations, reducing latency by 50% and improving real-time communication capabilities for over 70% of unmanned defense systems globally.

The Satellite Communication Systems for Defense Market is segmented based on type, application, and end-user, reflecting diverse operational requirements across military and defense sectors. Communication terminals, transponders, and receivers form the core product types, each supporting specific functions such as signal transmission, reception, and processing. Applications are primarily centered on intelligence, surveillance, reconnaissance (ISR), command and control, and navigation systems, with ISR accounting for a significant share due to increasing reliance on real-time data. End-users include defense agencies, aerospace organizations, and government bodies, with defense agencies dominating usage due to mission-critical communication needs. Over 70% of deployments are linked to ISR and command operations, while emerging applications such as cyber defense and space-based monitoring are gaining traction. Increasing integration of AI and software-defined systems is further refining segmentation dynamics.

Communication terminals dominate the Satellite Communication Systems for Defense Market, accounting for approximately 38% of total adoption due to their critical role in enabling real-time data transmission and connectivity across mobile and fixed military platforms. Transponders hold around 27% share, supporting signal amplification and relay functions essential for long-range communication. However, receivers are emerging as the fastest-growing segment, driven by increasing demand for advanced signal processing capabilities and expected to grow at a rate exceeding 13% annually due to integration with AI-based analytics systems. Other types, including modems and antennas, collectively contribute nearly 35% of the market, offering niche yet essential functionalities such as signal modulation and directional communication. The rising deployment of multi-band and software-defined systems is further enhancing the importance of these components.

• In 2025, a leading defense agency deployed advanced software-defined communication terminals across 120+ units, improving signal adaptability and reducing communication latency by 32% in field operations.

Intelligence, Surveillance, and Reconnaissance (ISR) leads the application segment, accounting for approximately 42% of total usage due to its reliance on real-time data transmission and continuous monitoring capabilities. Command and control applications hold around 28% share, supporting decision-making processes and operational coordination. However, navigation and tracking applications are witnessing the fastest growth, expanding at an estimated 14% annually due to increasing deployment of autonomous and unmanned systems. Other applications, including weather monitoring and disaster response, collectively account for nearly 30% of usage, reflecting growing diversification in satellite communication applications. In 2025, over 40% of defense organizations reported increased reliance on satellite systems for ISR missions, while 35% adopted satellite-enabled navigation systems for unmanned operations.

• In 2025, a global defense program deployed satellite-enabled ISR systems across 150+ operational zones, enhancing surveillance coverage by 45% and improving response times by 28%.

Defense agencies represent the leading end-user segment, accounting for approximately 55% of total adoption due to their extensive use of satellite communication systems for mission-critical operations. Aerospace organizations follow with around 25% share, focusing on satellite development, deployment, and maintenance. Government agencies account for nearly 20% of usage, supporting applications such as disaster management and national security. However, private defense contractors are emerging as the fastest-growing segment, with adoption rates increasing at approximately 15% annually due to rising outsourcing of satellite communication services. Over 60% of defense contractors have integrated satellite communication systems into their operational frameworks, reflecting growing reliance on private sector capabilities.

• In 2025, over 500 defense contractors globally adopted satellite communication platforms, improving operational coordination efficiency by 30% across multiple defense programs.

North America accounted for the largest market share at 41% in 2025 however, Asia-Pacific is expected to register the fastest growth, expanding at a CAGR of 14.2% between 2026 and 2033.

North America’s dominance is supported by over 180 active defense satellites and annual investments exceeding USD 30 billion in space-based defense systems. Europe holds approximately 26% share, driven by collaborative defense programs and increasing investments in secure communication infrastructure. Asia-Pacific accounts for nearly 22% of the market, with countries such as China and India increasing satellite deployments by over 35% in recent years. The Middle East & Africa region contributes around 7%, supported by defense modernization initiatives, while South America holds close to 4% share. Increasing geopolitical tensions and rising defense budgets across regions are further shaping demand patterns globally.

North America holds approximately 41% share of the Satellite Communication Systems for Defense Market, driven by strong defense infrastructure and high adoption of advanced communication technologies. Key industries include military intelligence, aerospace, and cybersecurity. Government initiatives supporting secure communication systems and spectrum allocation reforms are enhancing deployment efficiency. Over 65% of defense communication systems in the region rely on satellite-based networks. Technological advancements such as AI-driven communication optimization and multi-orbit satellite integration are widely implemented. A leading regional player has deployed next-generation satellite terminals improving communication efficiency by 35%. Consumer behavior reflects high enterprise adoption in defense and aerospace sectors, with increased reliance on real-time communication systems.

Europe accounts for nearly 26% of the Satellite Communication Systems for Defense Market, with major contributions from Germany, the UK, and France. Regulatory bodies emphasize secure and sustainable satellite communication systems, influencing adoption trends. Over 55% of defense programs in Europe integrate satellite-based communication technologies. The region is witnessing increased adoption of software-defined satellites and AI-enabled communication systems. A regional player has introduced advanced satellite communication platforms enhancing signal security by 30%. Consumer behavior is influenced by regulatory compliance requirements, leading to demand for transparent and secure communication systems across defense operations.

Asia-Pacific ranks as the fastest-growing region, accounting for approximately 22% of the Satellite Communication Systems for Defense Market. China, India, and Japan are key contributors, with satellite deployments increasing by over 35% in recent years. Infrastructure development and defense modernization programs are driving demand. Over 50% of defense organizations in the region are adopting satellite communication systems for ISR and navigation applications. A regional player has expanded satellite manufacturing capacity by 40%, supporting increased deployment. Consumer behavior shows strong adoption driven by mobile and digital defense technologies, with increasing reliance on real-time communication systems.

South America holds approximately 4% share of the Satellite Communication Systems for Defense Market, with Brazil and Argentina leading adoption. Infrastructure development and defense modernization initiatives are key growth drivers. Over 45% of defense communication systems in the region utilize satellite-based platforms. Government policies supporting technology adoption and international collaborations are enhancing market growth. A regional player has implemented satellite communication systems improving connectivity by 25% across defense operations. Consumer behavior is influenced by increasing demand for localized communication solutions and integration with media and language-specific applications.

The Middle East & Africa region accounts for approximately 7% of the Satellite Communication Systems for Defense Market, with key growth in the UAE and South Africa. Demand is driven by defense, oil & gas, and infrastructure sectors. Over 50% of defense modernization programs in the region include satellite communication integration. Technological advancements such as secure communication systems and anti-jamming technologies are widely adopted. A regional player has partnered with global firms to deploy advanced satellite systems, improving operational efficiency by 30%. Consumer behavior reflects increasing demand for reliable and secure communication systems in high-risk environments.

United States – 41% Market share: It is driven by high defense spending and advanced satellite infrastructure

China – 18% Market share: It is supported by rapid satellite deployment and defense modernization programs

The Satellite Communication Systems for Defense Market is moderately consolidated, with the top five companies accounting for approximately 58% of the total market share. The competitive landscape includes over 35 active global and regional players specializing in satellite manufacturing, communication systems, and defense technologies. Market leaders focus on strategic initiatives such as mergers, partnerships, and product innovation to strengthen their position. Over 60% of companies have invested in AI-enabled communication systems and software-defined satellite technologies to enhance operational efficiency.

Recent years have witnessed an increase in joint ventures between defense contractors and satellite technology firms, with over 25 collaborations announced between 2023 and 2025. Product innovation remains a key competitive factor, with nearly 45% of companies launching advanced communication systems featuring anti-jamming and encryption capabilities. Additionally, more than 50% of market players are focusing on developing multi-orbit satellite architectures to improve coverage and reduce latency. The market is also characterized by high entry barriers due to significant capital requirements and regulatory constraints, limiting the entry of new competitors.

Northrop Grumman Corporation

Boeing Defense, Space & Security

Airbus Defence and Space

Thales Group

L3Harris Technologies, Inc.

General Dynamics Corporation

Raytheon Technologies Corporation

Honeywell Aerospace

Viasat, Inc.

Inmarsat Global Limited

SES S.A.

Intelsat S.A.

Hughes Network Systems, LLC

The Satellite Communication Systems for Defense Market is undergoing rapid technological transformation driven by advancements in satellite architecture, communication protocols, and network optimization technologies. One of the most significant developments is the adoption of multi-orbit satellite systems integrating LEO, MEO, and GEO satellites, improving communication reliability by over 40% and reducing latency by nearly 50%. These systems enable seamless connectivity across diverse operational environments, supporting real-time data transmission for defense applications.

Artificial intelligence is playing a crucial role in optimizing satellite communication networks, with over 58% of defense organizations implementing AI-driven bandwidth management and predictive maintenance systems. These technologies enhance network efficiency by approximately 35% while reducing operational downtime. Software-defined satellites are also gaining traction, allowing dynamic reconfiguration of communication parameters and improving flexibility by 30% compared to traditional systems.

Advanced encryption and anti-jamming technologies are critical for ensuring secure communication, with nearly 48% of new systems incorporating these features. Quantum communication technologies are emerging as a future trend, offering enhanced security through quantum key distribution. Additionally, the integration of edge computing with satellite systems is enabling faster data processing and reducing latency in mission-critical operations. These technological advancements are shaping the future of the market, enabling more resilient and efficient communication systems for defense applications.

• In March 2025, Lockheed Martin advanced its Mobile User Objective System (MUOS) with a new reprogrammable payload processor capable of real-time updates, delivering more than a 10× increase in communication capacity compared to legacy UHF systems. Source: www.lockheedmartin.com

• In January 2025, Northrop Grumman successfully demonstrated advanced satellite communication payloads capable of improving signal reliability by 35% under contested environments, supporting next-generation defense communication systems.

• In September 2024, Airbus Defence and Space launched a new military communication satellite designed to enhance secure data transmission and support multi-domain operations across Europe and allied regions.

• In November 2024, Viasat introduced an upgraded satellite communication platform for defense applications, enabling improved network resilience and reduced latency for mission-critical operations in remote environments.

The Satellite Communication Systems for Defense Market Report provides a comprehensive analysis of key segments, technologies, applications, and regional trends shaping the industry. The report covers detailed segmentation by type, including communication terminals, transponders, receivers, modems, and antennas, highlighting their operational roles and adoption patterns. Application analysis focuses on intelligence, surveillance, reconnaissance (ISR), command and control, navigation, and emerging use cases such as cyber defense and space-based monitoring.

Geographically, the report examines key regions including North America, Europe, Asia-Pacific, South America, and the Middle East & Africa, offering insights into regional adoption patterns, infrastructure development, and defense modernization initiatives. The report also evaluates technological advancements such as multi-orbit satellite systems, AI-driven communication optimization, and advanced encryption technologies.

Additionally, the scope includes analysis of industry dynamics, including drivers, restraints, opportunities, and challenges impacting market growth. Competitive landscape insights cover major players, strategic initiatives, and innovation trends. The report further explores emerging trends such as low Earth orbit satellite constellations, software-defined satellites, and integration of edge computing in satellite communication systems. This comprehensive scope enables decision-makers to understand market structure, identify growth opportunities, and develop strategic initiatives aligned with evolving defense communication requirements.

| Report Attribute / Metric | Details |

|---|---|

| Market Revenue (2025) | USD 630.0 Million |

| Market Revenue (2033) | USD 1,628.0 Million |

| CAGR (2026–2033) | 12.6% |

| Base Year | 2025 |

| Forecast Period | 2026–2033 |

| Historic Period | 2021–2025 |

| Segments Covered |

By Type

By Application

By End-User Insights

|

| Key Report Deliverables | Revenue Forecast; Market Trends; Growth Drivers & Restraints; Technology Insights; Segmentation Analysis; Regional Insights; Competitive Landscape; Regulatory & ESG Overview; Recent Developments |

| Regions Covered | North America; Europe; Asia-Pacific; South America; Middle East & Africa |

| Key Players Analyzed | Lockheed Martin Corporation; Northrop Grumman Corporation; Boeing Defense, Space & Security; Airbus Defence and Space; Thales Group; L3Harris Technologies, Inc.; General Dynamics Corporation; Raytheon Technologies Corporation; Honeywell Aerospace; Viasat, Inc.; Inmarsat Global Limited; SES S.A.; Intelsat S.A.; Hughes Network Systems, LLC |

| Customization & Pricing | Available on Request (10% Customization Free) |