Reports

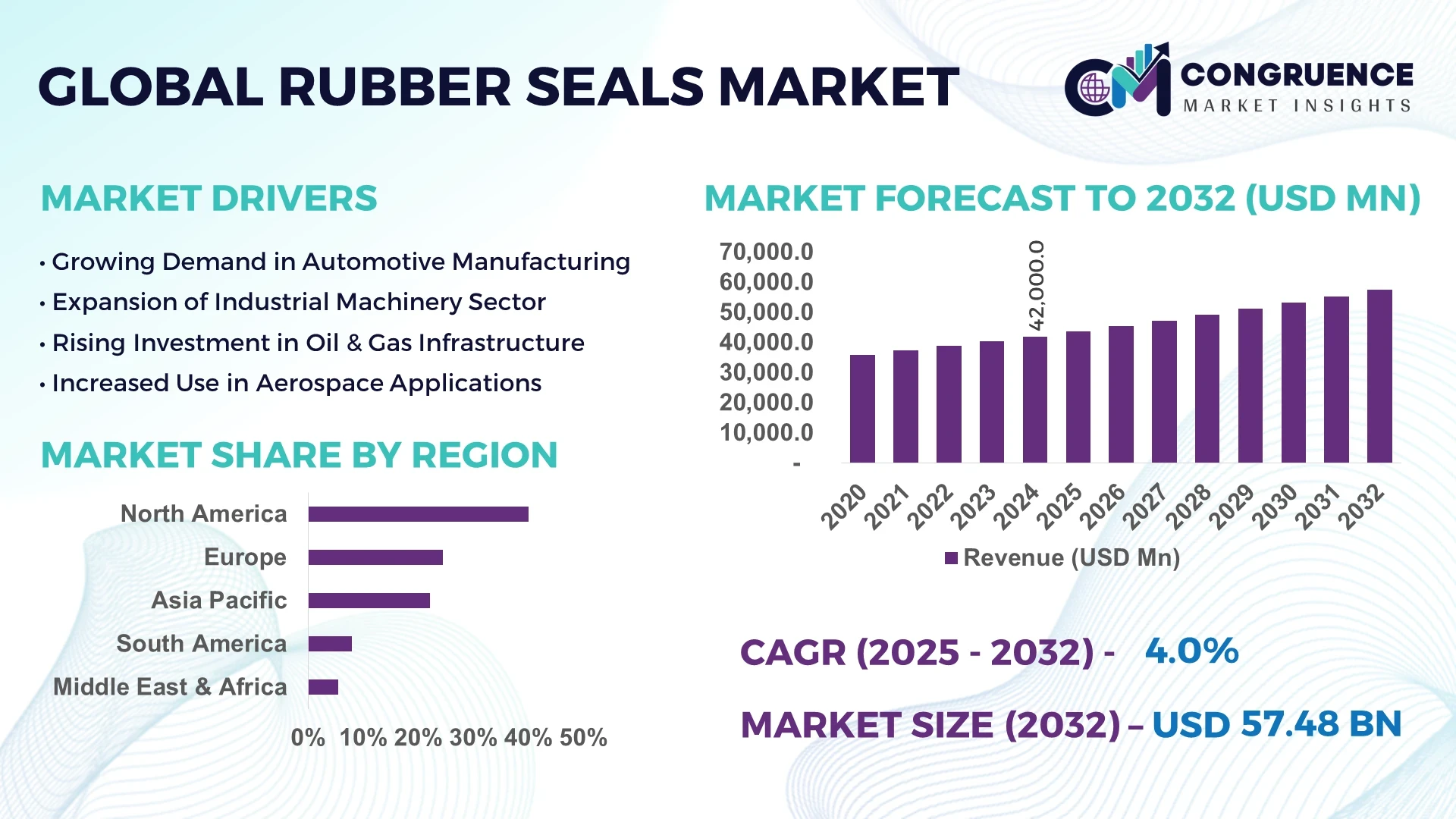

The Global Rubber Seals Market was valued at USD 42 Billion in 2024 and is anticipated to reach a value of USD 57.5 Billion by 2032, expanding at a CAGR of 4.0% between 2025 and 2032.

China dominates the global rubber seals market, accounting for over 30% of global production. The country's robust manufacturing infrastructure, paired with strategic industrial policies and rapid adoption of automation technologies, has positioned it as a global leader. Demand across its automotive, construction, and industrial equipment sectors continues to bolster market expansion, with significant investments flowing into production efficiency and export competitiveness.

The rubber seals market is increasingly shaped by developments in material science and manufacturing precision. New elastomeric compounds are enabling seals to perform under extreme temperatures and aggressive chemical exposure, expanding their application across oil & gas, aerospace, and high-voltage electrical equipment. Electric vehicles and renewable energy systems have triggered the need for custom sealing solutions, creating new revenue streams for manufacturers. However, volatility in raw materials and tightening environmental norms necessitate continuous innovation, cost optimization, and supply chain resilience to maintain competitive advantage.

Artificial Intelligence (AI) is playing a transformative role across the rubber seals industry by enabling smarter design, enhancing production efficiency, and elevating operational precision. AI-powered simulation tools are now used extensively during the R&D phase, allowing engineers to test virtual prototypes of rubber seals under high-pressure, high-temperature, and corrosive conditions. This reduces the dependency on physical trials, cuts design time, and speeds up product launches.

In manufacturing, AI enhances quality control via vision systems that detect micro-defects, dimensional deviations, or inconsistencies in seal production. Real-time analytics, driven by AI, enables predictive maintenance of molding and extrusion equipment, which reduces downtime and extends machinery lifespan. AI models are also integrated into demand forecasting and inventory management, optimizing raw material procurement and production planning. These technologies are streamlining operations and improving response time to dynamic customer requirements.

“In 2024, a major sealing technology provider collaborated with an alloy manufacturer to reduce turnaround time by up to 75% through the use of AI-driven 3D printing. By digitally designing molds with embedded gating systems and running full simulations pre-print, the development of high-precision mechanical rubber seals became faster and more efficient.”

The increasing complexity of machinery and the need for reliable sealing solutions in extreme conditions are driving the demand for high-performance rubber seals. Industries such as aerospace, automotive, and oil & gas require seals that can withstand high pressures, temperatures, and aggressive chemicals. This demand is pushing manufacturers to develop advanced materials and designs that offer superior durability and performance. The trend towards miniaturization and the integration of electronic components also necessitate seals with precise tolerances and enhanced functionality.

The rubber seals market is significantly affected by the volatility in raw material prices, particularly synthetic rubber and additives derived from petrochemicals. Price fluctuations can lead to increased production costs, affecting profit margins for manufacturers. Additionally, supply chain disruptions and geopolitical factors can exacerbate these fluctuations, making it challenging for companies to maintain stable pricing and supply. This uncertainty necessitates the development of alternative materials and more efficient production processes to mitigate the impact of raw material price volatility.

Emerging economies present significant growth opportunities for the rubber seals market. Rapid industrialization, urbanization, and infrastructure development in regions such as Asia-Pacific, Latin America, and Africa are increasing the demand for machinery and equipment that utilize rubber seals. Furthermore, the growth of the automotive and construction industries in these regions is driving the need for reliable sealing solutions. Companies that can establish a strong presence and adapt their products to meet local requirements stand to gain a competitive advantage in these burgeoning markets.

Environmental regulations concerning emissions, waste management, and the use of hazardous substances pose challenges to the rubber seals industry. Compliance with regulations requires manufacturers to invest in cleaner production technologies and develop eco-friendly materials. These regulatory requirements can increase operational costs and necessitate significant changes in manufacturing processes. Companies must balance regulatory compliance with maintaining product performance and cost-effectiveness, which can be a complex and resource-intensive endeavor.

Rise in Modular and Prefabricated Construction: The adoption of modular construction is reshaping the demand dynamics in the rubber seals market. Prefabricated building components require precise and reliable sealing solutions to ensure structural integrity and energy efficiency. This trend is driving the demand for custom-designed rubber seals that can be integrated seamlessly into modular units, reducing on-site labor and construction time.

Integration of Smart Sealing Technologies: The incorporation of sensors and IoT technologies into rubber seals is enabling real-time monitoring of seal performance. Smart seals can detect wear, temperature changes, and pressure variations, providing valuable data for predictive maintenance. This innovation enhances equipment reliability and reduces downtime, particularly in critical applications such as aerospace and industrial machinery.

Advancements in Sustainable Materials: Environmental concerns are leading to the development of rubber seals made from bio-based and recyclable materials. These sustainable alternatives aim to reduce the environmental impact of seal production and disposal. Manufacturers are exploring materials that offer comparable performance to traditional rubber while meeting sustainability goals.

Customization through Additive Manufacturing: 3D printing technologies are enabling the production of customized rubber seals with complex geometries and tailored properties. This approach allows for rapid prototyping and on-demand manufacturing, reducing lead times and inventory costs. Additive manufacturing also facilitates the creation of seals optimized for specific applications, expanding design possibilities and responsiveness to market needs.

The rubber seals market is segmented based on type, application, and end-user industry. This classification allows a better understanding of consumer demands and market behavior across various sectors. The segmentation reveals that while traditional seal types maintain steady demand, newer variants with enhanced material properties are capturing interest due to their compatibility with extreme environments. Applications in automotive, industrial machinery, aerospace, and electronics dominate the usage landscape. Among end-users, the automotive and industrial sectors are not only the largest consumers but are also leading innovation in rubber seal designs. Increasing regulatory requirements and operational precision demands are reshaping the selection criteria for sealing materials and technologies, driving both volume and value-based growth.

The rubber seals market comprises various types, including O-rings, lip seals, rotary seals, gaskets, and custom-molded seals. Among these, O-rings dominate the market due to their widespread utility, cost-effectiveness, and ease of installation. O-rings are heavily used in both static and dynamic sealing applications, particularly in automotive engines and hydraulic systems. They accounted for the largest revenue share in 2024.

However, rotary seals are emerging as the fastest-growing segment. Their ability to perform under high-speed and high-pressure environments makes them highly preferred in industrial and aerospace settings. The increased deployment of automation equipment and rotary machines in manufacturing has significantly boosted demand for these seals.

Custom-molded seals are also gaining traction in specialized industries like electronics and defense, where unique geometries and material resistance are required. The development of high-performance elastomers and advanced manufacturing techniques like injection molding and 3D printing are further enabling the growth of this niche.

The primary application areas for rubber seals include automotive, aerospace, industrial machinery, electrical & electronics, and oil & gas. Among these, the automotive sector remains the leading segment, accounting for the highest demand in 2024. Rubber seals are crucial for maintaining performance in engines, transmissions, braking systems, and HVAC systems. The continued shift toward electric vehicles and the introduction of advanced mobility solutions are expected to keep this segment dominant in the near term.

The fastest-growing segment, however, is electrical and electronics. With the rising integration of sensors, batteries, and delicate circuits in consumer electronics and electric vehicles, the need for micro-sealing solutions has surged. Rubber seals ensure protection against moisture, dust, and vibrations—vital to device reliability and lifecycle.

Meanwhile, industrial machinery continues to show steady growth due to expanding automation and process industry needs. Seals in this segment must meet higher endurance standards, especially in hydraulics and fluid power systems.

The key end-user industries in the rubber seals market include automotive, aerospace & defense, construction, oil & gas, healthcare, and industrial manufacturing. Among these, the industrial manufacturing sector led the market in 2024, accounting for a substantial share due to the extensive use of machinery and processing equipment that require durable and high-performance sealing solutions. The continual rise in automated production lines and robotics is further fueling demand in this segment.

The automotive industry remains a close second but is noted as the fastest-growing end-user segment, largely due to the EV boom and increased emphasis on energy efficiency and emission controls. Vehicles now incorporate more sealing points than ever before, from battery modules to electric drivetrains.

The healthcare sector is also seeing rising demand for hygienic and FDA-compliant rubber seals, particularly in diagnostic equipment and fluid handling systems. Meanwhile, oil & gas continues to demand high-resilience seals due to extreme operational conditions, though growth is comparatively moderate due to market volatility.

North America accounted for the largest market share at 40% in 2024; however, Asia-Pacific is expected to register the fastest growth, expanding at a CAGR of 7.0% between 2025 and 2032.

Technological Advancements Driving Demand

North America's dominance in the rubber seals market is underpinned by its robust industrial base and technological innovation. In 2024, the region's market size reached approximately USD 24.5 billion, with the United States contributing around USD 19.3 billion. The automotive sector remains a significant consumer, with increasing demand for electric vehicles necessitating advanced sealing solutions. Additionally, the aerospace and defense industries are investing in high-performance seals to meet stringent safety and performance standards. The region's focus on energy efficiency and emission reductions further propels the adoption of innovative sealing technologies.

Sustainability and Regulatory Compliance Fueling Growth

Europe's rubber seals market is characterized by a strong emphasis on sustainability and regulatory compliance. In 2024, the market size stood at approximately USD 18.4 billion, with countries like Germany and France leading in consumption. The automotive industry's shift towards electric and hybrid vehicles drives the demand for specialized seals that can withstand higher temperatures and pressures. Moreover, the region's stringent environmental regulations necessitate the use of eco-friendly materials and manufacturing processes, prompting manufacturers to innovate in developing recyclable and biodegradable sealing solutions.

Rapid Industrialization and Infrastructure Development

Asia-Pacific is emerging as the fastest-growing market for rubber seals, with a projected CAGR of 7.0% from 2025 to 2032. In 2024, the market size was approximately USD 14.1 billion, with China accounting for a significant share. The region's rapid industrialization, urbanization, and infrastructure development are key drivers of this growth. The automotive industry, particularly in China and India, is expanding rapidly, increasing the demand for high-quality sealing solutions. Additionally, the electronics and construction sectors are contributing to the rising consumption of rubber seals, necessitating products that offer durability and resistance to extreme conditions.

Growing Automotive and Energy Sectors

South America's rubber seals market is experiencing steady growth, with a market size of approximately USD 3.3 billion in 2024. Brazil and Argentina are the leading consumers, driven by the expansion of the automotive and energy sectors. The region's focus on renewable energy projects and the modernization of industrial equipment are creating opportunities for the adoption of advanced sealing technologies. However, economic fluctuations and political uncertainties may pose challenges to sustained growth in certain countries.

Infrastructure Projects and Oil & Gas Industry Driving Demand

The Middle East & Africa region's rubber seals market reached approximately USD 1.2 billion in 2024. Countries like Saudi Arabia and the United Arab Emirates are investing heavily in infrastructure projects, including transportation and construction, which require reliable sealing solutions. Additionally, the oil and gas industry's demand for high-performance seals capable of withstanding harsh environments is contributing to market growth. The region's focus on diversifying economies and developing non-oil sectors further supports the adoption of advanced rubber sealing technologies.

United States: With a market size of approximately USD 19.3 billion in 2024, the U.S. leads due to its advanced manufacturing capabilities and strong demand from automotive and aerospace sectors.

China: Accounting for a significant portion of the Asia-Pacific market, China's rapid industrialization and expansion in automotive and electronics industries drive its substantial market share.

The global rubber seals market is witnessing strong competition, with numerous global and regional players investing in innovation and geographic expansion. Companies are emphasizing the development of advanced sealing solutions that deliver high durability, resistance to chemicals, and thermal stability across critical applications such as automotive, aerospace, construction, and industrial machinery. Competitors are focusing on enhancing their production capabilities and expanding into fast-growing economies with increasing industrial activities. Additionally, partnerships and mergers are common strategies used to enter new markets and strengthen supply chain networks. Increasing demand for specialized rubber sealing solutions in electric vehicles, coupled with the shift towards environmentally sustainable products, has driven many players to adopt green manufacturing practices and materials. Digital transformation, including automation and smart manufacturing, is helping companies to boost productivity while reducing production costs and errors. The level of customization and customer service has also become a competitive differentiator, especially in markets with sophisticated engineering demands.

Trelleborg Sealing Solutions

Freudenberg Sealing Technologies

Parker Hannifin Corporation

SKF Group

NOK Corporation

ElringKlinger AG

Dana Incorporated

Saint-Gobain Performance Plastics

Hutchinson SA

Datwyler Holding Inc.

Technological advancements are significantly influencing the rubber seals market across all major sectors. Material science breakthroughs have led to the adoption of high-performance elastomers such as EPDM, FKM, and silicone rubber, known for their superior resistance to temperature extremes, chemical exposure, and pressure variations. The integration of nanotechnology has further enhanced durability, making rubber seals more efficient in critical applications like aerospace and oil & gas. CAD and simulation software allow engineers to optimize seal designs based on real-world stress conditions, minimizing development time. Automation in the manufacturing of rubber seals ensures consistent quality, reduced waste, and faster throughput.

3D printing has emerged as a transformative force in prototyping custom rubber seals. It allows manufacturers to quickly test and validate designs without incurring traditional tooling costs. Smart seals embedded with sensors are enabling predictive maintenance, especially in heavy machinery and industrial automation systems. These seals can monitor factors like wear, pressure, and temperature, sending real-time data to operators and helping to avoid system failure. Such innovations are not only improving performance but also reducing the environmental footprint by optimizing material usage and energy consumption during production.

In June 2024, LAPP introduced the ETHERLINE® FD bioP Cat.5e, its first bio-based Ethernet cable produced in series. This sustainable variant features a bio-based outer sheath composed of 43% renewable raw materials, reducing the carbon footprint by 24% compared to traditional fossil-based TPU sheaths.

In January 2024, a global sealing technology company launched a new business division dedicated to enhancing customer experience through improved logistics, service speed, and digital product support in the rubber seals market.

In August 2023, a prominent sealing systems provider acquired a South Korean precision components manufacturer to strengthen its footprint in the semiconductor and electronics sector, which increasingly demands miniature and high-performance rubber seals.

In September 2023, a tier-1 automotive supplier implemented 3D printing to produce specialized rubber gaskets for EV battery cooling systems, significantly reducing prototyping time and improving product lifecycle performance in electric vehicles.

This report provides an in-depth overview of the global rubber seals market, analyzing key trends, growth drivers, and strategic opportunities across multiple industries. The study covers detailed segmentation based on product type, applications, and end-user sectors, offering qualitative and quantitative insights into current and future market dynamics. It evaluates technological trends, such as the adoption of high-performance elastomers, sensor-enabled smart seals, and digital manufacturing techniques. Additionally, it explores competitive dynamics, showcasing leading players’ strategies, market positions, and innovation pipelines.

Geographically, the report highlights regional performance and demand drivers across North America, Europe, Asia-Pacific, South America, and the Middle East & Africa. It discusses evolving customer demands, industry-specific compliance standards, and the growing importance of sustainable manufacturing. By offering a comprehensive forecast and strategic landscape, the report helps industry stakeholders—including manufacturers, distributors, investors, and policymakers—make informed decisions and capitalize on emerging opportunities in the global rubber seals market.

| Report Attribute / Metric | Report Details |

|---|---|

| Market Name | Global Rubber Seals Market |

| Market Revenue (2024) | USD 42 Billion |

| Market Revenue (2032) | USD 57.5 Billion |

| CAGR (2025–2032) | 4.0% |

| Base Year | 2024 |

| Forecast Period | 2025–2032 |

| Historic Period | 2020–2024 |

| Segments Covered |

By Type

By Application

By End-User

|

| Key Report Deliverables | Revenue Forecast, Growth Trends, Market Dynamics, Segmental Overview, Regional and Country-wise Analysis, Competition Landscape |

| Regions Covered | North America, Europe, Asia-Pacific, South America, Middle East & Africa |

| Key Players Analyzed | Trelleborg Sealing Solutions, Freudenberg Sealing Technologies, Parker Hannifin Corporation, SKF Group, NOK Corporation, ElringKlinger AG, Dana Incorporated, Saint-Gobain Performance Plastics, Hutchinson SA, Datwyler Holding Inc. |

| Customization & Pricing | Available on Request (10% Customization is Free) |