Reports

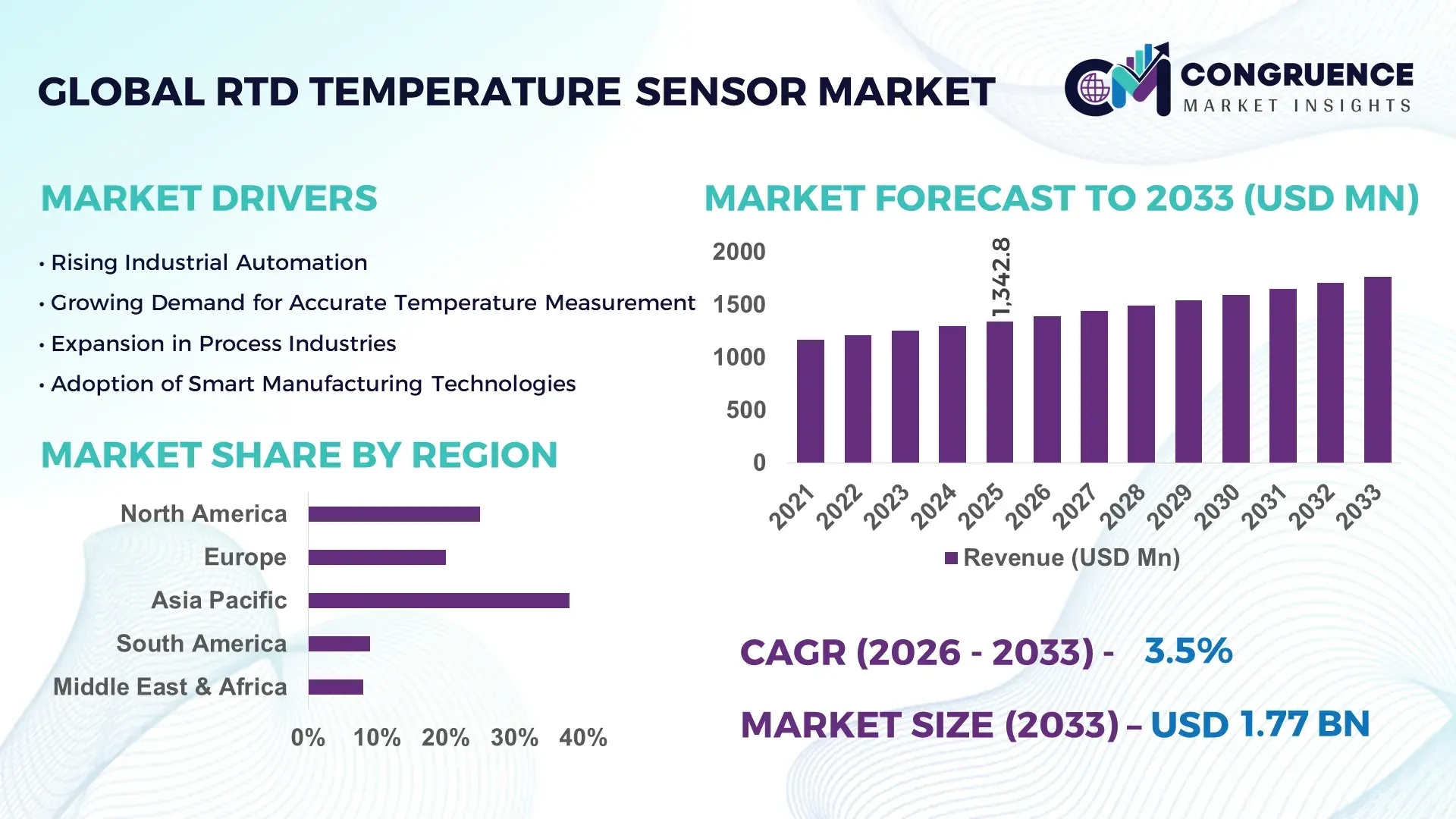

The Global RTD Temperature Sensor Market was valued at USD 1342.78 Million in 2025 and is anticipated to reach a value of USD 1768.18 Million by 2033 expanding at a CAGR of 3.5% between 2026 and 2033. Growth is supported by rising demand for high-accuracy temperature monitoring across industrial automation, energy management, and process industries.

China represents the most prominent national landscape within the RTD temperature sensor ecosystem, driven by large-scale manufacturing capacity and sustained industrial investments. The country hosts over 30% of the global sensor manufacturing facilities, with strong output from industrial hubs such as Guangdong, Jiangsu, and Zhejiang. Annual capital expenditure in industrial automation equipment exceeded USD 45 billion in 2024, accelerating RTD deployment in power generation, chemicals, and electronics manufacturing. RTD sensors are widely integrated across China’s smart factories, with industrial automation penetration surpassing 55%. Technological progress includes expanded use of thin-film platinum RTDs and automated calibration systems, while domestic production supports applications in rail infrastructure, EV battery thermal management, and semiconductor fabrication, where temperature accuracy below ±0.1°C is increasingly standardized.

Market Size & Growth: Valued at USD 1342.78 Million in 2025, projected to reach USD 1768.18 Million by 2033, expanding at a CAGR of 3.5%, driven by demand for precision temperature control in automated and safety-critical environments.

Top Growth Drivers: Industrial automation adoption at 62%, energy efficiency improvement of 18%, and predictive maintenance implementation growth of 27%.

Short-Term Forecast: By 2028, average lifecycle cost of RTD sensors is expected to decline by 12% due to material optimization and higher-volume manufacturing.

Emerging Technologies: Thin-film platinum RTDs, wireless RTD integration with IIoT platforms, and AI-enabled temperature diagnostics.

Regional Leaders: Asia-Pacific projected at USD 620 Million by 2033 with smart manufacturing adoption; Europe at USD 480 Million driven by process automation; North America at USD 410 Million supported by energy and aerospace applications.

Consumer/End-User Trends: Increased usage by power utilities, pharmaceutical manufacturers, and semiconductor fabs seeking continuous, high-accuracy thermal monitoring.

Pilot or Case Example: In 2024, an industrial automation pilot using RTDs in a chemical plant achieved a 22% reduction in unplanned downtime.

Competitive Landscape: Market leader holds approximately 18% share, followed by Emerson Electric, Siemens, Honeywell, Yokogawa, and ABB.

Regulatory & ESG Impact: Stricter industrial safety standards and energy-efficiency mandates are accelerating adoption of high-precision RTDs.

Investment & Funding Patterns: Over USD 1.2 Billion invested globally since 2023 in sensor manufacturing upgrades and smart instrumentation projects.

Innovation & Future Outlook: Integration of RTDs with digital twins, edge analytics, and smart control systems is shaping next-generation industrial monitoring.

The RTD Temperature Sensor Market serves critical industry sectors including industrial manufacturing, which contributes approximately 38% of total demand, followed by energy and utilities at 24%, oil and gas at 16%, and pharmaceuticals and food processing collectively accounting for nearly 14%. Recent innovations focus on miniaturized thin-film RTDs, improved platinum purity, and enhanced vibration resistance for harsh environments. Regulatory pressure related to industrial safety, emissions control, and process validation continues to support adoption. Regionally, Asia-Pacific leads consumption due to expanding manufacturing capacity, while Europe emphasizes precision instrumentation in regulated industries. Future growth is expected from smart factories, hydrogen energy systems, and advanced thermal management in electric mobility, reinforcing RTDs as a core component of high-accuracy temperature measurement infrastructure.

The RTD Temperature Sensor Market holds strong strategic relevance due to its role in enabling precision-driven, compliant, and data-centric industrial operations. RTD temperature sensors are increasingly embedded within automation systems across power generation, chemicals, pharmaceuticals, food processing, and advanced manufacturing, where temperature accuracy below ±0.1°C is becoming an operational standard. From a strategic perspective, thin-film platinum RTD technology delivers approximately 30% improvement in response stability and 20% longer operational life compared to traditional wire-wound RTD standards, improving asset reliability and lowering recalibration frequency.

Regionally, Asia-Pacific dominates in volume due to large-scale industrial output and infrastructure expansion, while Europe leads in adoption intensity, with over 58% of industrial enterprises integrating high-accuracy RTDs within regulated process control environments. In the short term, by 2028, AI-enabled predictive maintenance integrated with RTD sensing networks is expected to reduce unplanned equipment downtime by nearly 25% through early thermal anomaly detection.

Compliance and ESG considerations are further shaping strategic pathways. Manufacturing firms are committing to energy-efficiency improvements such as 15% reduction in thermal losses and increased sensor recyclability by 2030, aligning RTD deployments with sustainability reporting frameworks. In 2024, Germany achieved an estimated 18% improvement in industrial energy efficiency through smart factory upgrades combining RTD sensors with digital control systems. Looking ahead, the RTD Temperature Sensor Market is positioned as a foundational pillar for resilient operations, regulatory compliance, and sustainable industrial growth across global value chains.

Industrial automation is a primary driver of growth for the RTD Temperature Sensor Market, as automated systems rely heavily on precise and stable temperature data for control, safety, and efficiency. Over 60% of new industrial installations globally now incorporate closed-loop temperature monitoring, where RTDs are preferred for accuracy and drift resistance. In process industries such as chemicals and oil refining, temperature deviations as small as 1°C can impact product quality and safety, reinforcing RTD adoption. Manufacturing plants integrating robotics and programmable logic controllers increasingly deploy RTD sensors to support predictive maintenance and continuous monitoring. Additionally, smart factories using Industry 4.0 architectures report up to 20% improvement in process consistency when high-accuracy RTDs replace thermocouples in critical zones, strengthening their role across automated environments.

Despite technical advantages, higher upfront costs remain a restraint in the RTD Temperature Sensor Market, particularly for small and mid-sized industrial operators. Platinum-based RTDs can cost 25–40% more than basic thermocouples, especially when paired with protective housings and transmitters. In cost-sensitive sectors such as basic manufacturing and utilities in emerging economies, this price differential slows replacement cycles. Installation complexity and calibration requirements further add to total ownership costs, with calibration accounting for nearly 10% of lifecycle expenditure in regulated industries. These financial and operational considerations can delay adoption, especially where extreme accuracy is not mandated, limiting penetration in lower-margin applications.

The expansion of smart energy systems and electric vehicle ecosystems presents significant opportunities for the RTD Temperature Sensor Market. RTD sensors are increasingly used in battery thermal management, charging infrastructure, and grid-scale energy storage, where temperature stability directly affects performance and safety. EV battery packs require temperature accuracy within ±0.2°C to optimize charging cycles and extend lifespan, driving RTD integration. Similarly, renewable energy facilities deploying digital substations and hydrogen production units rely on RTDs for continuous monitoring. As global energy systems transition toward electrification and decentralization, demand for durable, high-precision temperature sensing creates new application spaces beyond traditional industrial uses.

Integration complexity represents a key challenge for the RTD Temperature Sensor Market, particularly as sensors become part of advanced digital and AI-enabled systems. RTDs must be correctly integrated with transmitters, control software, and analytics platforms to deliver full value, increasing system design complexity. In many regions, shortages of skilled instrumentation technicians affect installation accuracy and calibration quality, leading to performance inconsistencies. Additionally, legacy industrial systems often lack compatibility with modern smart RTD solutions, requiring costly retrofits. These technical and workforce-related challenges can slow deployment timelines and increase operational risk, especially in facilities transitioning from analog to fully digital monitoring infrastructures.

Rising Adoption in Modular and Prefabricated Construction Projects (55% Cost Efficiency Gains):

The increasing shift toward modular and prefabricated construction is reshaping demand patterns in the RTD Temperature Sensor Market. Approximately 55% of newly commissioned industrial and commercial projects report measurable cost benefits from modular construction practices. Pre-bent and pre-cut structural and mechanical components are manufactured off-site using automated systems that rely on precise temperature control, driving higher RTD deployment. In Europe and North America, over 48% of modular facilities now integrate RTD sensors for equipment thermal monitoring, enabling tighter tolerances, reduced rework rates by nearly 20%, and faster project delivery timelines by an average of 30%.

Expansion of Smart Manufacturing and Industry 4.0 Integration (60% Sensor Connectivity Growth):

Smart manufacturing environments are accelerating RTD temperature sensor integration as factories digitize operations. More than 60% of newly installed industrial temperature sensors are now connected to digital control or monitoring platforms. RTDs are increasingly preferred over thermocouples in automated lines due to stability improvements exceeding 25% in long-cycle operations. In electronics and precision engineering plants, RTD-enabled monitoring has contributed to defect rate reductions of up to 15%, supporting continuous quality control and real-time process optimization.

Increased Deployment in Energy Transition Infrastructure (40% Growth in Clean Energy Applications):

The global transition toward cleaner energy systems is driving RTD usage in power generation, energy storage, and hydrogen production facilities. Around 40% of new renewable energy and grid modernization projects now incorporate RTD temperature sensors for thermal management and safety assurance. Battery energy storage systems increasingly rely on RTDs to maintain operating temperature deviations within ±0.2°C, improving system reliability by nearly 18% and extending asset life cycles in high-load conditions.

Shift Toward Miniaturized and High-Durability RTD Designs (22% Reduction in Installation Footprint):

Manufacturers are focusing on compact, ruggedized RTD designs to meet space-constrained and harsh-environment requirements. Recent product advancements have reduced sensor installation footprints by approximately 22% while improving vibration resistance by over 30%. These developments support adoption in aerospace, rail, and heavy industrial machinery, where sensor durability directly impacts maintenance intervals. Enhanced encapsulation and material engineering are also enabling RTDs to operate reliably in temperatures exceeding 600°C without compromising measurement accuracy.

The RTD Temperature Sensor Market segmentation reflects diverse performance requirements, operating environments, and industry-specific compliance needs. Market structure is primarily shaped by sensor type, application area, and end-user industry, each influencing product specifications, adoption intensity, and integration complexity. Platinum-based RTDs dominate high-accuracy use cases, while thin-film designs are expanding into compact and automated systems. Application-wise, industrial process control remains the largest demand center due to strict temperature tolerance requirements, while emerging applications in energy storage and electric mobility are gaining traction. End-user demand is led by manufacturing and energy sectors, supported by increasing automation rates exceeding 60% in advanced economies. Regional industrial policies, safety standards, and digitalization levels further refine segmentation dynamics, making the RTD Temperature Sensor Market highly structured yet responsive to technological evolution.

The RTD Temperature Sensor Market by type is segmented into wire-wound RTDs, thin-film RTDs, and specialty RTDs designed for extreme or niche environments. Wire-wound RTDs currently account for approximately 46% of total adoption, driven by their superior accuracy, long-term stability, and suitability for critical industrial and laboratory applications. Thin-film RTDs represent around 34% of adoption and are gaining preference in compact equipment due to reduced size, faster response times, and easier integration with digital systems. However, thin-film RTDs are the fastest-growing segment, expanding at an estimated CAGR of 6.1%, supported by rising automation, miniaturization of industrial equipment, and demand from electronics and EV battery systems. Specialty RTDs, including surface-mount and high-temperature variants, collectively contribute about 20% of the market, serving aerospace, rail, and heavy engineering niches.

Application-based segmentation of the RTD Temperature Sensor Market highlights industrial process control as the leading application, accounting for nearly 41% of total usage due to stringent quality, safety, and compliance requirements. Power generation and energy management follow with approximately 23% adoption, reflecting the need for continuous thermal monitoring in turbines, transformers, and grid infrastructure. However, electric vehicle and battery thermal management applications are the fastest-growing, expanding at an estimated CAGR of 7.4%, supported by rising EV production volumes and strict battery safety thresholds requiring accuracy within ±0.2°C. Other applications such as food processing, pharmaceuticals, and HVAC systems collectively represent around 36% of demand, where hygiene, validation, and energy efficiency are key drivers.

End-user segmentation shows the manufacturing sector as the dominant consumer in the RTD Temperature Sensor Market, contributing approximately 39% of total demand due to widespread adoption in automation, quality control, and predictive maintenance systems. The energy and utilities sector holds about 26%, reflecting extensive use in power plants, renewable energy facilities, and grid infrastructure. Automotive and electric mobility end-users currently account for around 17% but represent the fastest-growing segment, expanding at an estimated CAGR of 8.2% as EV production scales and thermal safety standards tighten. Other end-users, including pharmaceuticals, food and beverage, aerospace, and rail, collectively contribute roughly 18%, with adoption rates exceeding 50% in regulated production environments.

Asia-Pacific accounted for the largest market share at 38% in 2025 however, Middle East & Africa is expected to register the fastest growth, expanding at a CAGR of 5.9% between 2026 and 2033.

Asia-Pacific leadership is supported by large-scale industrial manufacturing, accounting for over 45% of global electronics and heavy equipment output, and more than 60% deployment of automated temperature monitoring in new plants. Europe followed with nearly 27% share, driven by regulatory-led adoption in pharmaceuticals, chemicals, and food processing, where over 70% of facilities require precision temperature validation. North America held approximately 22%, supported by advanced process industries and digital transformation spending exceeding USD 120 billion annually. Middle East & Africa and South America together accounted for about 13%, with strong momentum from energy, infrastructure, and mining investments. Regional differentiation is increasingly shaped by automation intensity, regulatory stringency, and infrastructure modernization levels.

North America represents around 22% of the RTD Temperature Sensor Market, with demand concentrated in the United States and Canada. Key industries include oil & gas, pharmaceuticals, aerospace, and data center infrastructure, where temperature accuracy below ±0.1°C is increasingly mandated. Federal energy-efficiency programs and industrial safety standards have accelerated RTD integration in power plants and chemical facilities. Over 65% of large manufacturers in this region now deploy smart sensors connected to digital control platforms. Local players are investing in wireless RTD solutions and AI-enabled diagnostics to reduce maintenance downtime by nearly 20%. Regional adoption patterns show higher enterprise usage in healthcare and advanced manufacturing, reflecting strong preference for validated and compliant temperature monitoring systems.

Europe accounts for approximately 27% of global RTD temperature sensor demand, led by Germany, the United Kingdom, and France. Regulatory bodies enforcing industrial safety, emissions control, and pharmaceutical validation standards have made RTDs essential across process industries. Nearly 72% of regulated manufacturing sites in Western Europe rely on platinum RTDs for continuous monitoring. Sustainability initiatives targeting 20% energy-efficiency improvements by 2030 are also driving sensor upgrades. European manufacturers are advancing thin-film RTDs optimized for low power consumption and digital traceability. Consumer behavior in this region reflects strong preference for explainable, auditable sensing technologies aligned with compliance and ESG reporting requirements.

Asia-Pacific is the largest regional market by volume, accounting for about 38% of total demand, with China, Japan, South Korea, and India as top consumers. The region hosts more than 50% of global manufacturing capacity, supporting extensive RTD deployment in electronics, automotive, and heavy industries. Industrial automation penetration exceeds 55% in advanced economies such as Japan and South Korea. Local players are expanding production of thin-film RTDs for EV batteries and semiconductor fabs. Consumer behavior reflects strong cost-performance sensitivity, with rapid adoption driven by expanding manufacturing bases and infrastructure-led growth rather than premium compliance requirements.

South America contributes roughly 6% of global RTD temperature sensor demand, with Brazil and Argentina as primary markets. Energy, mining, and food processing are key application areas, collectively accounting for over 60% of regional usage. Government-backed infrastructure and renewable energy projects are increasing demand for durable temperature sensors capable of operating in harsh environments. Trade policies supporting local manufacturing have encouraged regional assembly of industrial sensors. Adoption behavior is closely tied to project-based investments, with buyers prioritizing ruggedness and lifecycle durability over advanced digital features.

The Middle East & Africa region holds about 7% of the RTD Temperature Sensor Market but shows the fastest expansion outlook. Demand is driven by oil & gas, petrochemicals, power generation, and large-scale construction projects in the UAE, Saudi Arabia, and South Africa. Over 50% of new energy projects now integrate continuous temperature monitoring systems to meet safety and efficiency targets. Governments are promoting industrial diversification and smart infrastructure, encouraging adoption of advanced RTDs. Regional buyers prioritize reliability in extreme temperatures, with growing interest in digital monitoring to support predictive maintenance strategies.

China: ~21% market share — Dominance driven by high industrial production capacity and extensive deployment across manufacturing, energy, and infrastructure projects.

United States: ~17% market share — Strong demand supported by advanced process industries, regulatory compliance requirements, and widespread adoption of digital automation systems.

The RTD Temperature Sensor market exhibits a moderately fragmented competitive structure, characterized by the presence of more than 40 active global and regional manufacturers competing across industrial, energy, automotive, and process automation segments. The combined share of the top five companies is estimated at approximately 55%, indicating a balance between established multinational leaders and specialized mid-sized players. Market leaders differentiate through broad product portfolios, global distribution networks, and strong integration capabilities with industrial automation platforms. Strategic initiatives increasingly focus on new product launches featuring thin-film platinum RTDs, wireless connectivity, and enhanced durability for harsh environments. Over 30% of competitive activity in the past two years has centered on technology upgrades rather than pricing strategies. Partnerships between sensor manufacturers and automation system providers have risen by nearly 25%, aimed at delivering end-to-end monitoring solutions. Mergers and acquisitions remain selective, with an emphasis on acquiring niche technology firms specializing in miniaturization or digital calibration. Innovation intensity is high, with more than 40% of competitors investing in R&D programs targeting accuracy improvements, lifecycle extension, and ESG-aligned materials. Overall, competition is driven by technological differentiation, compliance readiness, and the ability to support large-scale industrial deployments.

ABB Ltd.

Siemens AG

Honeywell International Inc.

Emerson Electric Co.

Yokogawa Electric Corporation

Schneider Electric SE

Endress+Hauser Group

Omega Engineering

WIKA Group

Amphenol Advanced Sensors

Technology advancement remains a critical driver of differentiation and performance in the RTD Temperature Sensor Market, with innovations increasingly centered on precision, connectivity, durability, and integration within digital ecosystems. Traditional platinum-based RTD elements, long valued for high accuracy and stability, are now being enhanced through thin-film deposition techniques that reduce sensor mass by roughly 22% while improving response times by up to 18% in dynamic thermal environments. These advancements are enabling precision control in sectors such as semiconductor fabrication, where temperature deviations under ±0.05°C directly impact yield quality.

Emerging digital integration trends are reshaping how RTD sensors interact within broader automated systems. Approximately 58% of new RTD deployments now include onboard digital signal processing and real-time diagnostics capabilities, enabling immediate fault detection and predictive maintenance triggers. Wireless RTD modules are also gaining traction; in some industrial facilities, the transition from wired to wireless temperature sensing has reduced installation and wiring costs by nearly 26% while maintaining measurement fidelity.

Another significant technological trend is the incorporation of artificial intelligence and edge analytics at the sensor level. Smart RTD networks equipped with edge computing can filter and preprocess temperature data, reducing network load by up to 35% and enabling faster decision-making in mission-critical environments such as power generation and pharmaceuticals. Enhanced encapsulation materials and ruggedized housings are enabling RTDs to perform reliably in extreme conditions, with operational temperature tolerances extended to exceed 650°C in metallurgy and petrochemical applications.

Miniaturization is another key technology trajectory. Micro-scale RTDs designed for compact instrumentation and consumer electronics are enabling precise thermal monitoring in battery management systems, where maintaining temperature deviations within ±0.2°C can extend service life. Interoperability standards and modular sensor architectures are also supporting rapid integration with existing industrial control systems, accelerating digital transformation efforts across manufacturing and energy sectors. Together, these technology trends highlight a shift from basic temperature measurement toward intelligent, connected, and resilient sensing solutions, positioning RTD temperature sensors as indispensable components within modern operational and monitoring frameworks.

• In February 2024, Siemens expanded its industrial temperature portfolio by introducing advanced thin-film RTD sensors designed for high-vibration environments, enabling up to 20% longer operational stability in power generation and heavy manufacturing applications through improved encapsulation and signal conditioning.

• In July 2024, Honeywell enhanced its industrial sensing lineup with digitally enabled RTD temperature sensors supporting real-time diagnostics and predictive maintenance, allowing industrial users to reduce unplanned shutdown events by approximately 18% in continuous process operations.

• In March 2025, Emerson Electric introduced a next-generation RTD assembly optimized for pharmaceutical and life-sciences environments, meeting stricter validation requirements and enabling temperature deviation control within ±0.05°C during batch manufacturing processes.

• In October 2025, Endress+Hauser expanded its global RTD production footprint with upgraded automated calibration lines, increasing output efficiency by nearly 25% while improving traceability and consistency for sensors used in regulated chemical and food processing industries.

The RTD Temperature Sensor Market Report delivers a structured and comprehensive assessment of the global market landscape, covering a wide spectrum of product types, applications, end-users, technologies, and regional dynamics. The scope includes detailed evaluation of RTD types such as wire-wound, thin-film, and specialty configurations engineered for extreme temperatures, high vibration, or hygienic environments. Application coverage spans industrial process control, power generation, energy storage systems, HVAC infrastructure, pharmaceuticals, food processing, automotive thermal management, and emerging hydrogen and battery technologies.

Geographically, the report analyzes five major regions—North America, Europe, Asia-Pacific, South America, and Middle East & Africa—capturing differences in industrial maturity, automation penetration levels exceeding 60% in developed markets, and infrastructure-led demand growth in emerging economies. End-user analysis focuses on manufacturing, energy and utilities, oil and gas, transportation, and regulated industries where temperature accuracy below ±0.1°C is operationally critical.

The report further examines technology trends including digital RTDs, wireless temperature monitoring, edge analytics integration, and smart calibration systems, along with niche segments such as EV battery thermal management and hygienic sensors for cleanroom environments. Competitive coverage evaluates market structure, innovation focus areas, and strategic positioning of key participants. Overall, the scope provides decision-makers with a precise, forward-looking framework to assess opportunities, risks, and strategic priorities within the RTD Temperature Sensor Market.

| Report Attribute/Metric | Report Details |

|---|---|

|

Market Revenue in 2025 |

USD V2025 Million |

|

Market Revenue in 2033 |

USD V2033 Million |

|

CAGR (2026 - 2033) |

3.5% |

|

Base Year |

2025 |

|

Forecast Period |

2026 - 2033 |

|

Historic Period |

2021 - 2025 |

|

Segments Covered |

By Types

By Application

By End-User

|

|

Key Report Deliverable |

Revenue Forecast, Growth Trends, Market Dynamics, Segmental Overview, Regional and Country-wise Analysis, Competition Landscape |

|

Region Covered |

North America, Europe, Asia-Pacific, South America, Middle East, Africa |

|

Key Players Analyzed |

ABB Ltd., Siemens AG, Honeywell International Inc., Emerson Electric Co., Yokogawa Electric Corporation, Schneider Electric SE, Endress+Hauser Group, Omega Engineering, WIKA Group, Amphenol Advanced Sensors |

|

Customization & Pricing |

Available on Request (10% Customization is Free) |