Reports

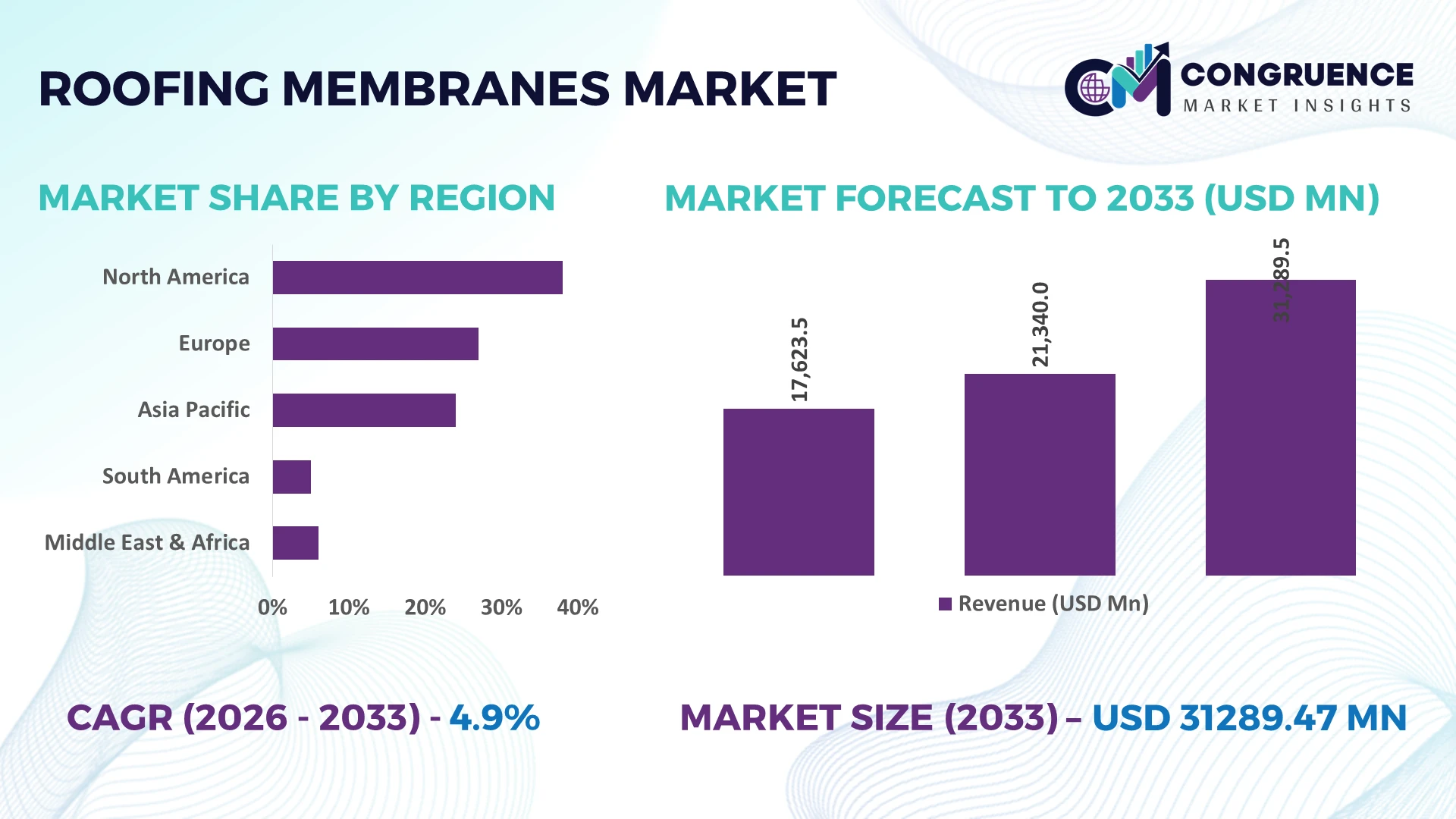

The Global Roofing Membranes Market was valued at USD 21340 Million in 2025 and is anticipated to reach a value of USD 31289.47 Million by 2033 expanding at a CAGR of 4.9% between 2026 and 2033. Growth is driven by accelerated commercial reroofing projects, stricter building energy-efficiency standards, wider adoption of cool-roof membrane technologies, and expanding industrial warehouse construction across logistics and manufacturing sectors.

The United States dominates the global roofing membranes market with approximately 28% market share, supported by sustained investments in commercial infrastructure, logistics facilities, and energy-efficient building retrofits, while over 46% of newly constructed large commercial roofs utilize single-ply membrane systems. In comparison, China continues expanding manufacturing capacity through industrial and urban development initiatives despite global trade and tariff adjustments reshaping raw material sourcing, strengthening regional production competitiveness.

Strategic investments in advanced membrane technologies, localized manufacturing, and resilient supply chains will determine long-term competitive positioning.

Market Size & Growth: USD 21,340 million (2025) to USD 31,289.47 million (2033) at 4.9% CAGR, supported by advanced roofing materials and energy-efficient construction.

Top Growth Drivers: Commercial reroofing +24%, cool-roof adoption +19%, logistics infrastructure expansion +17%.

Short-Term Forecast: By 2028, installation productivity improves 15% through prefabrication and automated membrane welding technologies.

Emerging Technologies: AI-enabled roof inspection, reflective membrane coatings, and drone-assisted installation improve maintenance efficiency by over 20%.

Regional Leaders: North America exceeds USD 9.1 billion, Asia-Pacific reaches USD 8.6 billion, Europe surpasses USD 6.8 billion, driven by sustainable building adoption.

Consumer/End-User Trends: More than 52% of commercial developers prioritize durable, energy-efficient roofing membrane systems.

Pilot/Case Example: 2026 industrial warehouse modernization reduced rooftop cooling demand by 18% using high-reflectivity membrane solutions.

Competitive Landscape: Top manufacturers control nearly 45% of global supply alongside diversified product innovation and regional expansion strategies.

Regulatory & ESG Impact: Green building compliance improves roof energy performance by approximately 16% while supporting carbon reduction objectives.

Investment & Funding: Over USD 2.3 billion supports manufacturing expansion, automation, and resilient regional supply chains.

Innovation & Future Outlook: Smart monitoring membranes, recyclable materials, and bio-based formulations accelerate next-generation roofing system development.

Roofing membranes continue gaining traction across commercial buildings, logistics centers, manufacturing plants, and institutional infrastructure where durability, waterproofing, and thermal efficiency remain operational priorities. Advanced reflective membranes and recyclable polymer formulations improve roof lifecycle performance, while installations incorporating digital inspection technologies have increased by nearly 22%. Ongoing building code modernization and regional supply-chain localization are reinforcing product innovation, setting the foundation for deeper strategic market analysis.

The roofing membranes market has become strategically important as governments, commercial developers, and industrial operators prioritize resilient building envelopes that reduce operating costs while meeting stricter energy-performance regulations. Infrastructure modernization, manufacturing reshoring, and supply-chain localization are accelerating procurement decisions, encouraging manufacturers to expand regional production and secure raw material availability. This shift is strengthening competitive differentiation through product durability, installation efficiency, and lifecycle performance rather than price alone.

Advanced thermoplastic roofing membranes deliver approximately 18% faster installation and improve solar reflectance by nearly 25% compared with conventional bituminous roofing systems, lowering maintenance requirements over long operating cycles. The United States leads large-scale commercial reroofing and logistics infrastructure deployment, while Germany emphasizes recyclable membrane technologies and circular construction practices through advanced manufacturing standards. Over the next two to three years, digital roof monitoring adoption is expected to exceed 30% across newly constructed industrial facilities, improving predictive maintenance and asset management.

A leading warehouse developer integrating reflective membrane systems with drone-based roof inspections reduced maintenance downtime by nearly 20% while extending inspection coverage across multiple facilities. Manufacturers are expanding localized production, strengthening contractor partnerships, and investing in recyclable material technologies to improve delivery reliability. Companies combining operational efficiency with sustainable product innovation will secure stronger competitive positioning in the evolving roofing membranes market.

Commercial reroofing cycles, industrial warehouse expansion, and stricter energy-efficiency regulations continue driving roofing membrane adoption. More than 52% of newly developed logistics facilities specify single-ply membrane systems due to faster installation and lower lifecycle maintenance, while reflective roofing solutions reduce cooling loads by approximately 15%. The United States continues upgrading aging commercial buildings under energy modernization initiatives, creating sustained replacement demand. Manufacturers are responding through production expansion, advanced polymer formulations, and contractor certification programs to improve installation quality. A key strategic shift is the integration of recyclable membrane technologies, enabling suppliers to strengthen long-term customer retention while aligning with evolving procurement standards and sustainable construction requirements.

Volatility in polymer feedstocks, synthetic rubber, and specialty additives continues affecting roofing membrane manufacturing economics. Raw material inputs account for nearly 60% of total production costs, while procurement prices for selected petrochemical derivatives have experienced fluctuations exceeding 18% during recent supply-chain disruptions. European manufacturers also face higher compliance costs linked to environmental regulations and imported material dependency. These pressures reduce pricing flexibility and compress operating margins for contractors managing fixed-price construction agreements. Companies are mitigating risk through localized sourcing, long-term procurement contracts, supplier diversification, and expanded recycling initiatives that recover polymer materials to stabilize production costs and improve supply resilience.

Digital asset management is creating new value opportunities beyond traditional waterproofing applications. Smart roofing membranes integrated with embedded sensors and AI-based monitoring platforms improve leak detection accuracy by approximately 35% while reducing inspection costs by nearly 22%. Japan and South Korea are expanding intelligent commercial building deployments that combine predictive maintenance with energy optimization platforms. Manufacturers are increasing investment in connected roofing solutions, advanced coatings, and recyclable composite materials through technology partnerships and product development programs. A significant strategic opportunity lies in offering roofing systems as long-term performance solutions rather than standalone construction materials, strengthening recurring service revenues and customer retention.

Maintaining consistent installation quality across increasingly complex roofing systems remains a significant execution challenge. Incorrect membrane installation contributes to nearly 30% of premature roof failures, while certified roofing specialists remain in limited supply across several industrial construction markets. Large commercial projects require precise welding, sealing, and digital inspection capabilities that many contractors are still developing. In countries including Canada and Australia, workforce shortages continue extending project schedules and increasing operational costs. Manufacturers must expand technical training, digital installation support, contractor certification, and automated quality-control technologies to ensure reliable project execution, strengthen product performance, and maintain long-term competitiveness.

Reflective Roofing Accelerates Adoption: Commercial developers are specifying high-reflectance roofing membranes at a faster pace as stricter building-energy regulations reshape procurement standards. Cool-roof installations have increased by approximately 24%, while rooftop surface temperatures decline by up to 30% under peak conditions and cooling energy demand falls nearly 15%. Large contractors are standardizing reflective membrane portfolios across logistics and retail assets, while manufacturers expand coating technologies and regional production to reduce delivery lead times amid continuing raw-material sourcing adjustments.

Digital Roof Asset Management: Building owners are integrating drones, AI-enabled inspections, and cloud-based maintenance platforms into roofing operations rather than relying on manual surveys. Digital inspection cycles shorten by nearly 40%, defect identification accuracy improves around 32%, and maintenance planning efficiency increases by approximately 20%. Enterprise facility operators are restructuring maintenance workflows around predictive asset management, prompting membrane suppliers to partner with inspection technology providers and expand lifecycle service offerings alongside traditional roofing products.

Circular Material Strategies Expand: Recycling programs for thermoplastic roofing membranes are becoming embedded within commercial construction procurement as sustainability targets influence purchasing decisions. Recycled polymer utilization has increased by roughly 18%, landfill disposal declines by nearly 12%, and manufacturing waste recovery exceeds 25% at selected facilities. Producers are investing in closed-loop material processing, redesigning product formulations, and establishing contractor collection networks to strengthen raw-material resilience while supporting environmental compliance requirements.

Prefabricated Installation Gains Momentum: Labor shortages are accelerating adoption of factory-prepared membrane systems that simplify onsite installation and improve project consistency. Prefabricated assemblies reduce installation time by nearly 20%, field labor requirements fall approximately 15%, and project scheduling reliability improves by over 18%. Construction firms are expanding modular roofing workflows, while membrane manufacturers automate fabrication processes and strengthen installer training partnerships to improve execution quality across large commercial developments.

TPO Membranes remain the leading segment because they combine strong weather resistance, weldable seams, high solar reflectivity, and competitive installation costs, making them the preferred solution for commercial and industrial roofing projects. They account for approximately 34% of total installations, supported by expanding warehouse construction and stricter energy-performance standards. PVC Membranes maintain strong demand in chemically aggressive industrial environments, while EPDM Membranes continue serving mature low-slope roofing applications where long-term durability remains the primary requirement. Bituminous Membranes retain relevance in refurbishment projects due to established installation expertise and broad contractor availability.

Liquid-Applied Membranes represent the fastest-growing segment as seamless waterproofing solutions become increasingly attractive for complex roof geometries and renovation projects. Adoption has increased by nearly 21% across refurbishment applications, while installation flexibility reduces project disruption by approximately 18%. Manufacturers are expanding liquid polymer portfolios, investing in low-VOC formulations, and strengthening contractor partnerships to capture higher-value retrofit opportunities. Competitive investment is steadily shifting toward advanced membrane chemistry, reflective technologies, and sustainable material innovation to differentiate premium product offerings.

Commercial Buildings represent the largest application segment as offices, retail centers, logistics facilities, healthcare campuses, and mixed-use developments require durable waterproofing with long service life. Nearly 46% of membrane demand originates from commercial construction, supported by replacement cycles and stricter building-performance standards. Industrial Buildings are the fastest-growing application, with adoption increasing by approximately 20% as manufacturing plants and distribution centers prioritize reflective roofing systems to reduce cooling loads and improve operational efficiency. Companies continue expanding specialized installation capabilities for large-scale industrial facilities with demanding performance requirements.

Residential Buildings maintain consistent demand through reroofing and energy-efficient housing upgrades, while Institutional Buildings increasingly specify durable membrane systems for schools and hospitals requiring predictable maintenance cycles. Infrastructure Projects continue adopting advanced waterproofing solutions for transport hubs and public assets exposed to challenging environmental conditions. Manufacturers are expanding project-specific product lines, contractor training, and digital specification support to strengthen penetration across diversified construction markets while improving installation quality and lifecycle performance.

Construction Companies remain the dominant end-user group because they manage large project pipelines across commercial, industrial, and institutional developments while influencing material specifications during project execution. They represent approximately 41% of procurement activity, supported by integrated design-build contracts and standardized roofing solutions. Facility Management is emerging as the fastest-growing end-user segment, with demand expanding by nearly 19% as organizations prioritize predictive maintenance, lifecycle optimization, and digital roof asset management across extensive property portfolios.

Real Estate Developers continue investing in premium membrane systems that improve long-term operating efficiency and enhance building sustainability credentials. Industrial Facilities increasingly procure specialized roofing solutions capable of supporting rooftop equipment and demanding operating environments, while Government agencies specify durable membrane systems for public infrastructure modernization programs. Manufacturers are responding through customized warranty programs, strategic contractor alliances, digital maintenance services, and portfolio-specific product development to strengthen customer retention and expand recurring business opportunities across major procurement channels.

North America accounted for the largest market share at 36.8% in 2025 however, Asia-Pacific is expected to register the fastest growth, expanding at a CAGR of 5.8% between 2026 and 2033.

Commercial reroofing and energy-performance upgrades sustain regional leadership

North America maintains the highest market concentration through extensive commercial reroofing programs, industrial warehouse expansion, and advanced building-performance standards. The region contributes approximately 36.8% of global demand, supported by widespread adoption of TPO and PVC membrane systems across logistics, healthcare, and retail infrastructure. More than 48% of large low-slope commercial roofing projects specify reflective membrane solutions to improve operational efficiency. Manufacturers continue investing in automated production, contractor certification, and regional distribution networks while strengthening supply resilience through localized polymer sourcing and expanded manufacturing capacity.

United States Market Outlook: The United States remains the operational center of the regional market due to extensive commercial construction activity, mature contractor ecosystems, and strong regulatory support for energy-efficient buildings. Nearly 50% of newly installed commercial roofing systems utilize reflective membrane technologies across logistics parks, educational campuses, and industrial facilities. Manufacturers continue expanding domestic production, investing in recycled polymer technologies, and strengthening partnerships with roofing contractors to improve delivery performance and installation consistency while supporting long-term infrastructure modernization.

Sustainable construction standards reshape product innovation

Europe continues strengthening its roofing membranes market through stricter building efficiency regulations, circular construction initiatives, and large-scale renovation programs. The region accounts for nearly 27% of global installations, with demand increasingly shifting toward recyclable membrane systems and low-emission production technologies. Approximately 35% of commercial refurbishment projects now prioritize high-performance roofing systems that improve thermal efficiency. Manufacturers are investing in advanced material formulations, recycling capabilities, and production modernization while aligning product portfolios with evolving environmental compliance requirements.

Germany Market Outlook: Germany leads the European market through its advanced manufacturing base, industrial modernization programs, and emphasis on sustainable construction materials. More than 40% of large commercial retrofit projects integrate high-performance roofing membrane systems designed for energy optimization and extended service life. Domestic manufacturers continue expanding recycling infrastructure, polymer innovation, and automated production capabilities, strengthening the country's position as a technology leader for premium roofing solutions across European construction markets.

Industrial expansion and manufacturing scale accelerate deployment

Asia-Pacific is the fastest-expanding regional market, supported by rapid urban development, manufacturing investment, and commercial infrastructure construction. The region represents approximately 30% of global roofing membrane consumption, with industrial facilities and logistics parks driving significant deployment volumes. Industrial roofing installations have increased by nearly 22% across major manufacturing hubs, encouraging suppliers to expand local production and strengthen regional distribution networks. Companies are also increasing investments in automated manufacturing and cost-efficient membrane technologies to support high-volume construction demand.

China Market Outlook: China dominates regional demand through large-scale industrial construction, commercial development, and integrated manufacturing capacity. Over 45% of new logistics and industrial roofing projects increasingly specify thermoplastic membrane systems because of installation speed and lifecycle efficiency. Domestic manufacturers continue expanding production capacity, investing in advanced polymer processing, and improving product quality to strengthen export competitiveness while meeting rising domestic demand for durable roofing infrastructure.

Infrastructure renewal supports steady market expansion

South America is experiencing stable roofing membrane adoption through commercial redevelopment, industrial expansion, and public infrastructure modernization. The region contributes nearly 4.8% of global market demand, with warehouse development and urban renovation projects creating consistent installation activity. Reflective roofing deployment has increased by approximately 16% across selected commercial developments as developers seek improved energy performance in warmer climates. Companies are strengthening local distribution partnerships and expanding contractor training to improve installation quality despite infrastructure and logistics constraints.

Brazil Market Outlook: Brazil remains the largest national market because of expanding logistics infrastructure, manufacturing investments, and commercial construction activity. Industrial roofing projects increasingly utilize durable membrane systems capable of handling high rainfall and elevated temperatures, while adoption across warehouse developments has increased by nearly 18%. Manufacturers are strengthening regional supply networks, expanding localized inventories, and collaborating with construction firms to improve project execution across the country's major industrial corridors.

Mega infrastructure investment transforms roofing demand

The Middle East & Africa market continues expanding through large-scale urban development, transport infrastructure, and industrial diversification projects. The region represents approximately 6.4% of global roofing membrane demand, with premium waterproofing systems increasingly specified for airports, commercial districts, and mixed-use developments. High-reflectivity membrane adoption has increased by nearly 20% within large infrastructure projects to improve thermal performance under extreme climatic conditions. Manufacturers are expanding regional partnerships, technical support services, and localized inventories to improve project delivery efficiency.

Saudi Arabia Market Outlook: Saudi Arabia leads regional demand through major infrastructure development, industrial diversification initiatives, and large commercial construction programs. Large mixed-use developments increasingly specify advanced roofing membrane systems that deliver long-term waterproofing and heat-reflective performance, while deployment across major construction projects has expanded by approximately 21%. Suppliers continue investing in local partnerships, technical training, and regional distribution capabilities to support complex infrastructure programs and improve execution across rapidly expanding project pipelines.

Global leaders including Carlisle Companies, Sika AG, Holcim, SOPREMA, and GAF compete directly with regional membrane manufacturers and cost-focused suppliers, while specialty polymer innovators challenge traditional bituminous roofing providers through differentiated performance. The top five companies collectively control approximately 44% of the global market, creating a moderately consolidated competitive structure. Competition centers on product durability, installation speed, manufacturing scale, and supply-chain resilience rather than pricing alone. Reflective membrane technologies reduce building cooling demand by nearly 15%, while automated production improves manufacturing efficiency by approximately 18% and localized sourcing shortens delivery times by around 20%. Companies are expanding manufacturing capacity, forming contractor partnerships, integrating recycled materials, and strengthening vertical control over polymer processing to secure procurement advantages. Competitive momentum is shifting toward sustainable membrane technologies and digital roof lifecycle services, increasing pressure on suppliers dependent on conventional products. High certification requirements, technical installation expertise, and established distribution networks remain key entry barriers. Winning requires continuous product innovation, localized manufacturing, contractor loyalty, and superior lifecycle performance.

Carlisle Companies Inc.

Sika AG

Holcim Ltd.

SOPREMA Group

GAF

Johns Manville

Owens Corning

BMI Group

Firestone Building Products

IKO Industries Ltd.

Derbigum

Polyglass S.p.A.

Advanced thermoplastic membranes, high-reflectivity coatings, and reinforced polymer composites are defining current technology adoption across commercial and industrial roofing systems. Approximately 48% of new large low-slope commercial installations now specify high-performance single-ply membranes because they improve thermal efficiency and simplify maintenance. Automated hot-air welding enhances seam consistency by nearly 22%, while advanced UV-resistant formulations extend service life by approximately 18%, reducing long-term operating costs for facility owners and contractors.

Emerging technologies combine embedded moisture sensors, drone-assisted inspections, AI-based defect detection, and digital asset management platforms to improve lifecycle performance. Smart monitoring systems reduce inspection time by nearly 35% and increase leak detection accuracy by approximately 30% compared with conventional manual inspections. Liquid-applied hybrid membranes integrated with recycled polymers also improve waterproofing continuity, while digital project documentation streamlines contractor workflows. Large commercial developers and industrial facility operators benefit most because predictive maintenance minimizes unexpected repair disruptions and extends roof replacement intervals.

Between 2026 and 2028, recyclable membrane technologies, factory-prefabricated roofing assemblies, and bio-based polymer formulations will reshape competitive differentiation. Prefabricated systems complete installation nearly 20% faster than conventional roofing methods while reducing onsite labor dependency by around 15%. Manufacturers investing in automation, circular material processing, and intelligent roofing solutions will strengthen operational efficiency, secure premium project specifications, and establish stronger long-term positions in performance-driven construction markets.

March 2025 Sika completed the acquisition of Cromar Building Products, expanding its roofing and waterproofing solutions portfolio across the UK. The transaction added more than 100 product lines, strengthening Sika's distribution network and accelerating growth in roofing membrane applications across Europe. Source: https://www.sika.com/

July 2024 Dow introduced its bio-based NORDEL™ REN EPDM technology at DKT 2024, delivering equivalent material performance while reducing product carbon footprint through certified renewable feedstocks. The innovation enables up to 100% bio-based attributed feedstock via mass balance, supporting sustainable roofing membrane manufacturing. Source: https://www.dow.com/

February 2025 Sika launched the SikaShield® HB79 Hybrid membrane in the United States, combining APAO and SBS technologies into a single roofing solution. The hybrid design integrates 2 modified-bitumen technologies, improving installation flexibility, weather resistance, and contractor productivity across commercial roofing projects. Source: https://usa.sika.com/

September 2025 GAF created its new Specialty Products and Services business unit by integrating SGI, Glass Mat, and Standard Logistics operations into one organization. The restructuring consolidated 3 operating businesses, improving manufacturing coordination, supply-chain efficiency, and customer service across roofing product operations. Source: https://www.gaf.com/

The report provides a comprehensive assessment of the global roofing membranes market by evaluating competitive positioning, technology evolution, procurement strategies, and operational trends across the value chain. It covers five major product categories, five application segments, and five key end-user groups, supported by detailed analysis across North America, Europe, Asia-Pacific, South America, and the Middle East & Africa. More than 40% of the assessment emphasizes technology adoption, product differentiation, deployment patterns, and enterprise purchasing behavior shaping market competitiveness.

The study delivers strategic insights for manufacturers, contractors, investors, distributors, and infrastructure developers through detailed regional benchmarking, competitive landscape evaluation, technology assessment, and segmentation analysis. It highlights manufacturing expansion, digital roof management, sustainable membrane innovation, supply-chain localization, and emerging refurbishment opportunities expected to influence business strategies between 2026 and 2033. The report also supports investment prioritization, portfolio optimization, partnership planning, and expansion decisions by identifying high-adoption segments, evolving customer requirements, and operational shifts across mature and emerging construction markets.

| Report Attribute/Metric | Report Details |

|---|---|

|

Market Revenue in 2025 |

USD 21340 Million |

|

Market Revenue in 2033 |

USD 31289.47 Million |

|

CAGR (2026 - 2033) |

4.9% |

|

Base Year |

2025 |

|

Forecast Period |

2026 - 2033 |

|

Historic Period |

2021 - 2025 |

|

Segments Covered |

By Type

By Application

By End-User

|

|

Key Report Deliverable |

Revenue Forecast, Growth Trends, Market Dynamics, Segmental Overview, Regional and Country-wise Analysis, Competition Landscape |

|

Region Covered |

North America, Europe, Asia-Pacific, South America, Middle East, Africa |

|

Key Players Analyzed |

Carlisle Companies Inc., Sika AG, Holcim Ltd., SOPREMA Group, GAF, Johns Manville, Owens Corning, BMI Group, Firestone Building Products, IKO Industries Ltd., Derbigum, Polyglass S.p.A. |

|

Customization & Pricing |

Available on Request (10% Customization is Free) |