Reports

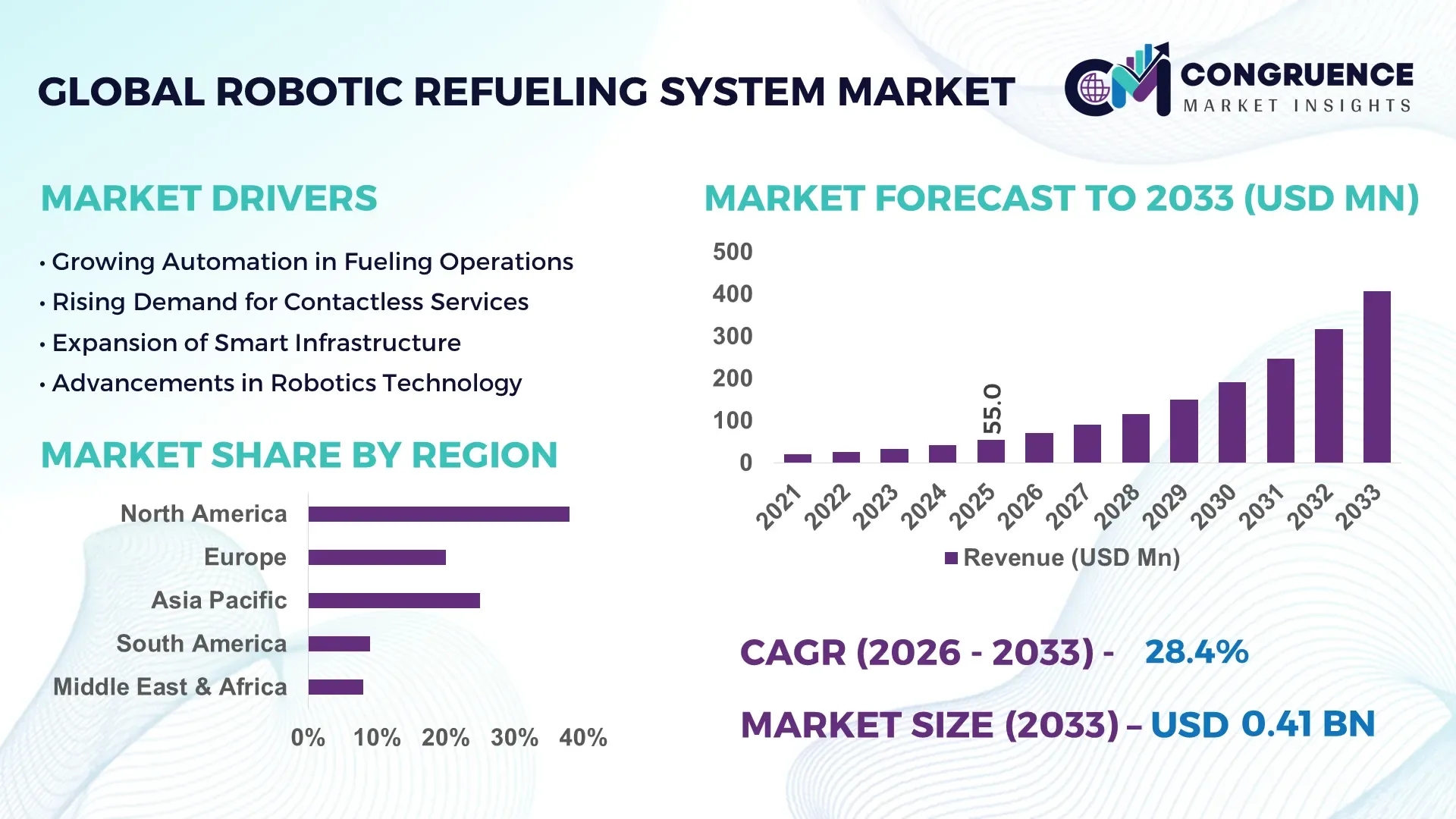

The Global Robotic Refueling System Market was valued at USD 55.03 Million in 2025 and is anticipated to reach a value of USD 406.61 Million by 2033 expanding at a CAGR of 28.4% between 2026 and 2033. This accelerated growth is attributed to the increasing deployment of autonomous systems across defense, automotive, and aviation sectors to enhance safety, efficiency, and operational precision in fuel handling.

The United States maintains a strong position in the robotic refueling system market, supported by advanced manufacturing capabilities and high investments in automation technologies. The country has allocated over USD 2.5 billion toward autonomous logistics and robotic fuel handling programs within defense applications. Approximately 35% of automated fueling deployments in North America are concentrated in military and aerospace sectors, while over 40% of smart fueling pilot programs are being implemented in urban mobility ecosystems. Additionally, the presence of more than 120 robotics research centers and sustained R&D spending exceeding 3% of GDP is enabling rapid advancements in AI-based sensor technologies and precision robotic arms, strengthening large-scale adoption across industrial and commercial fueling infrastructures.

Market Size & Growth: USD 55.03 Million in 2025 projected to reach USD 406.61 Million by 2033 at a CAGR of 28.4%, driven by rising automation in fuel dispensing and autonomous mobility systems.

Top Growth Drivers: Autonomous vehicle adoption at 45%, operational efficiency gains at 38%, enhanced safety in hazardous fueling environments at 32%.

Short-Term Forecast: By 2028, robotic refueling systems are expected to reduce manual labor costs by 27% and improve fueling cycle efficiency by 33%.

Emerging Technologies: AI-powered vision systems, IoT-enabled fuel monitoring solutions, and advanced robotic arm precision control technologies are transforming system performance.

Regional Leaders: North America projected at USD 145 Million by 2033 driven by defense applications, Europe at USD 110 Million with strong EV infrastructure integration, Asia-Pacific at USD 125 Million supported by smart city fueling automation initiatives.

Consumer/End-User Trends: High adoption observed among defense agencies, commercial fleet operators, and smart mobility service providers seeking automated, contactless fueling solutions.

Pilot or Case Example: In 2024, an autonomous fueling pilot project in Europe improved refueling efficiency by 30% and reduced downtime by 22% in fleet operations.

Competitive Landscape: Market leader holds approximately 28% share, followed by key players including ABB, KUKA, FANUC, Mitsubishi Electric, and Hyundai Robotics.

Regulatory & ESG Impact: Governments are promoting low-emission fueling systems, targeting up to 25% reduction in fuel wastage and emissions through automation by 2030.

Investment & Funding Patterns: Over USD 1.2 billion invested globally in robotic fueling and automation technologies, with increasing venture capital focus on AI-driven industrial robotics.

Innovation & Future Outlook: Integration of autonomous navigation, real-time analytics, and predictive maintenance systems is expected to drive next-generation robotic refueling infrastructure.

The robotic refueling system market is witnessing significant transformation across key industries including defense, automotive, aviation, and logistics, with defense applications contributing approximately 30% of system deployments due to high demand for unmanned operations. Automotive and fleet management sectors account for nearly 25% of adoption, particularly in electric and hybrid vehicle ecosystems requiring automated energy transfer solutions. Technological advancements such as machine vision accuracy exceeding 95%, sensor-based leak detection systems, and real-time fuel analytics are enhancing operational reliability. Regulatory focus on emission reduction and fuel efficiency is further accelerating adoption, particularly in Europe and Asia-Pacific regions where environmental compliance standards are stringent. Increasing investments in smart infrastructure and autonomous mobility are expected to drive long-term demand, positioning robotic refueling systems as a critical component in future automated fueling ecosystems.

The Robotic Refueling System Market is emerging as a strategically critical component within automated mobility ecosystems, defense logistics, and next-generation fueling infrastructure. Organizations are increasingly integrating robotic refueling solutions to enhance operational efficiency, reduce human intervention, and ensure precision in hazardous environments. Advanced AI-enabled robotic refueling systems deliver nearly 35% improvement in fueling accuracy and operational speed compared to conventional manual refueling methods, significantly lowering error rates and fuel wastage. This performance advantage is positioning the technology as a core enabler in autonomous vehicle deployment and unmanned military operations.

From a regional perspective, North America dominates in volume due to large-scale deployment across defense and aerospace sectors, while Europe leads in adoption with over 42% of enterprises integrating robotic fueling into smart mobility and EV infrastructure projects. Asia-Pacific is also witnessing accelerated expansion driven by urban automation and smart city investments. By 2028, AI-driven predictive maintenance and real-time analytics in robotic refueling systems are expected to improve system uptime by 30% and reduce maintenance-related downtime by 25%, strengthening operational continuity.

Sustainability and compliance considerations are increasingly shaping strategic decisions, with firms committing to reduce fuel spillage and emissions by up to 28% by 2030 through automated, sensor-driven fueling technologies. In 2024, a government-backed autonomous fueling initiative in Germany achieved a 32% improvement in refueling efficiency through AI-integrated robotic arms and IoT-based monitoring platforms, demonstrating measurable gains in both productivity and environmental performance. As industries continue to prioritize automation, safety, and sustainability, the Robotic Refueling System Market is expected to evolve as a foundational pillar supporting resilient, compliant, and future-ready fueling infrastructure across global industries.

The increasing deployment of autonomous vehicles and unmanned systems across defense, logistics, and commercial transportation sectors is a major driver of the Robotic Refueling System Market. Over 60% of next-generation military vehicle programs now incorporate autonomous or semi-autonomous capabilities, necessitating automated fueling solutions that minimize human involvement in high-risk environments. In commercial sectors, autonomous fleet operations are projected to increase by over 40% in urban logistics, creating demand for efficient and contactless fueling infrastructure. Robotic refueling systems enable consistent fueling cycles with up to 30% faster turnaround times compared to manual processes, enhancing operational productivity. Furthermore, the integration of machine vision and sensor technologies allows precise alignment and fuel dispensing, reducing fuel loss by nearly 20%. These capabilities are particularly valuable in sectors where safety, efficiency, and operational continuity are critical, reinforcing the role of robotic refueling systems as an essential component of automated ecosystems.

Despite strong growth potential, the Robotic Refueling System Market faces constraints related to high initial capital investment and system integration challenges. The deployment of advanced robotic arms, AI-enabled sensors, and IoT connectivity infrastructure can increase setup costs by 25% to 40% compared to traditional fueling systems. Additionally, integrating robotic refueling solutions with existing fueling infrastructure requires significant customization, particularly in legacy systems that lack digital compatibility. Maintenance complexity is another concern, as robotic systems require specialized technical expertise and periodic calibration to maintain precision levels above 95%. Small and medium enterprises, in particular, face adoption barriers due to limited budgets and technical capabilities. Furthermore, variations in fuel standards and vehicle designs across regions complicate standardization efforts, increasing implementation timelines and operational risks. These factors collectively slow down widespread adoption, especially in cost-sensitive markets and industries with established conventional fueling practices.

The rapid development of smart cities and connected mobility ecosystems presents substantial opportunities for the Robotic Refueling System Market. Governments worldwide are investing heavily in intelligent transportation systems, with over 50% of urban development projects incorporating automation and IoT-enabled infrastructure. Robotic refueling systems are increasingly being integrated into smart fueling stations, enabling seamless interaction with connected vehicles and fleet management platforms. The expansion of electric and hybrid vehicle markets is also creating new avenues for automated charging and refueling solutions, with automated energy transfer systems expected to improve charging efficiency by up to 35%. Additionally, the rise of data-driven operations allows operators to optimize fuel usage, monitor system performance in real time, and reduce operational inefficiencies by nearly 25%. Emerging markets in Asia-Pacific and the Middle East are particularly promising, as large-scale infrastructure modernization projects create demand for advanced fueling automation technologies.

Regulatory uncertainties and stringent safety requirements pose significant challenges to the Robotic Refueling System Market. Automated fuel handling involves high-risk operations, requiring compliance with strict safety standards and certification processes that vary across regions. In many countries, regulatory frameworks for autonomous fueling technologies are still evolving, leading to delays in approvals and large-scale deployments. Safety concerns related to system malfunction, fuel leakage, or improper alignment can impact operational reliability, especially in high-volume fueling environments. Ensuring consistent performance requires robust testing and validation processes, which can extend development cycles by up to 20%. Additionally, cybersecurity risks associated with connected robotic systems present new vulnerabilities, as unauthorized access to fueling infrastructure could disrupt operations. Addressing these challenges requires continuous investment in safety protocols, regulatory alignment, and advanced security measures, which can increase overall operational complexity and slow market penetration.

• AI-Driven Precision Fueling Enhancing Operational Accuracy: The integration of AI-based vision systems and sensor fusion technologies has improved robotic refueling accuracy levels to over 96%, reducing fuel spillage by approximately 22%. Around 48% of newly deployed systems now incorporate machine learning algorithms for adaptive alignment and nozzle positioning. This trend is particularly evident in defense and aviation sectors, where precision errors can result in operational losses exceeding 15% per fueling cycle. The adoption of predictive analytics has also reduced system calibration time by 18%, strengthening overall performance reliability.

• Expansion of Autonomous Fleet Infrastructure Driving Demand: The rapid growth of autonomous vehicle fleets is significantly influencing robotic refueling system deployment, with over 44% of logistics companies testing automated fueling solutions for fleet operations. Autonomous refueling reduces vehicle idle time by nearly 30% and increases daily operational cycles by 25%. In urban mobility ecosystems, more than 35% of pilot smart fueling stations are now designed to support fully autonomous vehicles, reflecting a strong shift toward integrated fueling automation within connected transport networks.

• Rise in Modular and Prefabricated Fueling Stations: The adoption of modular and prefabricated fueling infrastructure is transforming deployment efficiency in the robotic refueling system market. Approximately 55% of new fueling station projects report reduced installation timelines by up to 40% through prefabricated robotic integration units. Pre-configured robotic systems assembled off-site reduce labor requirements by 28% and improve installation accuracy by 20%. This trend is gaining traction in Europe and North America, where infrastructure modernization and cost optimization are key strategic priorities.

• Integration of IoT and Real-Time Monitoring Platforms: IoT-enabled robotic refueling systems are witnessing adoption rates exceeding 50% across industrial and commercial applications, enabling real-time monitoring of fuel flow, pressure, and system diagnostics. These systems improve operational uptime by 32% and reduce maintenance costs by nearly 24% through predictive maintenance capabilities. Additionally, over 38% of advanced deployments now feature cloud-based analytics platforms that provide actionable insights, allowing operators to optimize fuel usage patterns and enhance system lifecycle efficiency.

The Robotic Refueling System Market is segmented based on type, application, and end-user, each reflecting distinct adoption patterns and technological priorities. By type, systems are categorized into fixed robotic refueling units, mobile robotic refueling systems, and hybrid configurations, with fixed systems dominating due to their widespread deployment in industrial and defense infrastructures. Application-wise, defense and military operations account for a significant share, followed by automotive and logistics sectors where automation is increasingly critical. From an end-user perspective, government and defense organizations lead adoption, supported by increasing investments in unmanned operations and safety-critical fueling solutions. Commercial fleet operators and smart infrastructure developers are also emerging as key contributors, driven by the need for efficient, contactless fueling. Across segments, technological advancements such as AI integration, sensor-based automation, and IoT connectivity are consistently shaping adoption trends and influencing long-term market positioning.

The Robotic Refueling System Market by type includes fixed robotic refueling systems, mobile robotic refueling systems, and hybrid systems combining both capabilities. Fixed robotic refueling systems currently account for approximately 52% of total adoption, driven by their reliability, high throughput capacity, and suitability for large-scale installations such as military bases and industrial fueling stations. These systems offer consistent performance with over 95% operational accuracy, making them the preferred choice for high-volume applications.

Mobile robotic refueling systems represent the fastest-growing segment, with an estimated growth rate exceeding 31%, fueled by increasing demand for flexible and on-demand fueling solutions in autonomous fleet operations and remote environments. These systems enhance operational efficiency by reducing refueling delays by up to 28% and enabling dynamic deployment across multiple locations. Hybrid systems, which combine fixed infrastructure with mobile capabilities, account for the remaining 27% of the market, offering versatility in complex operational settings such as airports and logistics hubs. These systems are gaining traction due to their ability to adapt to varying fueling requirements.

The Robotic Refueling System Market by application spans defense and military operations, automotive and transportation, aviation, and industrial sectors. Defense and military applications dominate with approximately 46% share, as automated fueling is critical for unmanned systems and operations in hazardous environments. These systems improve mission readiness by reducing refueling time by up to 30% and minimizing human exposure to risks.

Automotive and transportation applications account for around 28% of adoption, supported by the rise of autonomous vehicle fleets and smart mobility solutions. Robotic refueling systems in this segment enhance fleet efficiency by increasing operational uptime by nearly 25%.

Aviation is the fastest-growing application segment, expanding at an estimated rate above 29%, driven by the need for precision fueling and reduced turnaround times at airports. Automated fueling systems can reduce aircraft servicing time by 20%, improving overall airport efficiency. Other applications, including industrial and energy sectors, contribute approximately 26% of the market, focusing on safety and process optimization.

The Robotic Refueling System Market by end-user includes government and defense organizations, commercial fleet operators, aviation service providers, and industrial enterprises. Government and defense entities lead the market with approximately 48% share, driven by high adoption of unmanned systems and the need for secure, automated fueling in mission-critical environments. These users benefit from improved operational efficiency of up to 35% and enhanced safety protocols.

Commercial fleet operators represent a rapidly growing segment, with an estimated growth rate exceeding 30%, supported by the expansion of autonomous logistics and transportation networks. Robotic refueling enables fleet operators to reduce downtime by nearly 27% and optimize fuel consumption through automated monitoring systems. Aviation service providers and airport operators account for around 15% of the market, leveraging robotic systems to streamline aircraft servicing and reduce ground handling times. Industrial enterprises, including energy and manufacturing sectors, contribute the remaining 17%, focusing on safety and efficiency improvements in hazardous environments.

Region North America accounted for the largest market share at 38% in 2025 however, Asia-Pacific is expected to register the fastest growth, expanding at a CAGR of 31.2% between 2026 and 2033.

North America’s dominance is supported by over 60% deployment of robotic refueling systems across defense and aerospace sectors, along with more than 45% integration in autonomous vehicle pilot programs. Europe follows with a 27% market share, driven by stringent environmental regulations and over 50% adoption of automated fueling in smart mobility infrastructure. Asia-Pacific holds approximately 24% share, with rapid expansion across China, Japan, and India, where over 40% of new smart city projects incorporate automated fueling systems. South America and the Middle East & Africa collectively contribute around 11%, with increasing investments in energy automation and industrial modernization. Across all regions, more than 52% of newly installed systems feature AI-enabled monitoring, while 48% include IoT-based predictive maintenance capabilities, reflecting a global shift toward intelligent fueling ecosystems.

How are advanced automation ecosystems reshaping fueling infrastructure adoption?

North America accounts for approximately 38% of the Robotic Refueling System Market, driven by strong demand from defense, aerospace, and autonomous vehicle sectors. The United States leads regional adoption with over 65% of installations concentrated in military and industrial applications. Government initiatives supporting autonomous logistics and fuel efficiency improvements have increased funding for robotic fueling technologies by nearly 30% over the past three years. Technological advancements such as AI-powered robotic arms and sensor accuracy exceeding 96% are enhancing system reliability. Companies like Tesla are exploring automated fueling interfaces for autonomous fleets, contributing to innovation in the sector. Consumer behavior in the region reflects high enterprise adoption, with over 55% of logistics and fleet operators investing in automation to reduce operational downtime and improve efficiency.

What factors are accelerating automated fueling adoption in highly regulated environments?

Europe holds around 27% share of the Robotic Refueling System Market, with key markets including Germany, the United Kingdom, and France leading adoption. Over 50% of fueling infrastructure projects in these countries incorporate automation technologies aligned with sustainability targets. Regulatory frameworks focused on emission reduction and energy efficiency are pushing companies to adopt robotic refueling systems that can reduce fuel wastage by up to 25%. The European Union’s green initiatives have accelerated investments in smart fueling solutions, with over 35% of new mobility projects integrating automated systems. Companies such as ABB are actively developing advanced robotic fueling technologies, improving system precision and safety. Consumer behavior in this region shows a strong preference for environmentally compliant solutions, with over 48% of enterprises prioritizing automation to meet regulatory standards.

Why is rapid industrial expansion fueling demand for automated refueling technologies?

Asia-Pacific represents approximately 24% of the global Robotic Refueling System Market and ranks as the fastest-growing region in terms of deployment volume. China, Japan, and India collectively account for over 70% of regional demand, driven by large-scale infrastructure projects and smart city initiatives. More than 45% of new urban development programs in these countries include automated fueling systems. The region’s manufacturing sector is rapidly adopting robotics, with over 50% of industrial facilities integrating automation technologies to improve efficiency. Companies like Hyundai Robotics are expanding their presence by developing cost-effective robotic fueling solutions tailored for emerging markets. Consumer behavior in Asia-Pacific is influenced by rapid urbanization and digital transformation, with over 60% of enterprises prioritizing automation to enhance productivity and scalability.

How are energy sector investments influencing automation adoption trends?

South America accounts for nearly 6% of the Robotic Refueling System Market, with Brazil and Argentina emerging as key contributors. The region’s growth is closely tied to energy and industrial sectors, where over 40% of investments are directed toward automation and efficiency improvements. Government initiatives promoting energy optimization have led to a 20% increase in adoption of automated fueling systems in industrial applications. Infrastructure modernization projects are also driving demand, with more than 30% of new facilities incorporating robotic technologies. Local companies are gradually investing in automation to enhance operational safety and reduce manual intervention. Consumer behavior in the region shows a growing preference for cost-effective solutions, with approximately 35% of enterprises adopting automation to improve operational efficiency and reduce long-term costs.

What role does industrial modernization play in fueling technology transformation?

The Middle East & Africa region contributes around 5% to the Robotic Refueling System Market, with significant demand driven by oil and gas, construction, and logistics sectors. Countries such as the UAE and South Africa are leading adoption, with over 25% of large-scale industrial projects incorporating automated fueling systems. Technological modernization initiatives have resulted in a 22% increase in robotics adoption across energy operations. Trade partnerships and government policies supporting industrial automation are further accelerating growth, with more than 30% of new infrastructure projects integrating smart technologies. Regional players are focusing on enhancing system durability and efficiency to meet harsh environmental conditions. Consumer behavior reflects a strong inclination toward automation in high-risk environments, with over 40% of enterprises prioritizing safety-driven technology adoption.

United States – 34% share in the Robotic Refueling System Market, driven by high defense spending, advanced automation infrastructure, and strong adoption of autonomous vehicle technologies.

Germany – 18% share in the Robotic Refueling System Market, supported by robust manufacturing capabilities, strict environmental regulations, and high integration of smart fueling systems.

The Robotic Refueling System Market is moderately fragmented, with over 40 active global and regional players competing across technology innovation, system integration, and application-specific solutions. The top five companies collectively account for approximately 55% of the market, indicating a balanced mix of established leaders and emerging innovators. Key players are focusing on strategic partnerships, with more than 30% of companies engaging in collaborations to enhance product capabilities and expand geographic reach. Product innovation remains a critical competitive factor, with over 45% of firms investing in AI-driven automation and IoT-enabled monitoring systems to differentiate their offerings. Mergers and acquisitions activity has increased by nearly 20% in the past three years, reflecting consolidation efforts aimed at strengthening technological expertise and market presence. Additionally, companies are prioritizing modular system designs and scalable solutions to address diverse industry requirements. The competitive landscape is further shaped by continuous advancements in robotic precision, safety features, and real-time analytics, positioning innovation as a key driver of long-term market competitiveness.

ABB

KUKA AG

FANUC Corporation

Mitsubishi Electric Corporation

Hyundai Robotics

Yaskawa Electric Corporation

Universal Robots

Boston Dynamics

Schneider Electric

Siemens AG

The Robotic Refueling System Market is being shaped by rapid advancements in artificial intelligence, sensor integration, and robotic automation technologies that are significantly enhancing system efficiency and operational safety. Modern robotic refueling systems now achieve precision levels exceeding 96% through the integration of AI-driven computer vision and 3D imaging technologies, enabling accurate nozzle alignment and fuel dispensing even in dynamic environments. Approximately 52% of newly deployed systems incorporate multi-sensor fusion, combining LiDAR, infrared, and ultrasonic sensors to ensure real-time detection of fuel ports and environmental obstacles.

IoT-enabled platforms are playing a critical role in transforming fueling operations, with over 48% of systems now equipped with real-time monitoring and predictive maintenance capabilities. These technologies reduce unexpected downtime by nearly 30% and extend system lifecycle performance by up to 25%. Additionally, cloud-based analytics platforms are enabling operators to process large volumes of operational data, improving fuel efficiency by approximately 18% through optimized dispensing patterns and consumption tracking.

Robotic arm technology has also evolved significantly, with multi-axis robotic manipulators capable of executing over 1,000 precise movements per fueling cycle, ensuring consistent performance across various vehicle types. Advanced materials such as lightweight composites and corrosion-resistant alloys are being used to improve system durability, particularly in harsh industrial and defense environments.

Emerging technologies such as autonomous navigation and digital twin simulation are further enhancing system capabilities. Digital twin models allow operators to simulate fueling operations and predict performance outcomes, improving deployment efficiency by nearly 22%. Additionally, integration with autonomous vehicle ecosystems is enabling fully automated fueling processes, reducing human intervention by over 35% and positioning robotic refueling systems as a key enabler of next-generation mobility and industrial automation.

• In March 2025, ABB expanded its industrial robotics portfolio by introducing advanced AI-enabled robotic arm solutions designed for precision-based industrial applications, including automated fueling processes. These systems improved positional accuracy by over 20% and enhanced operational safety through integrated sensor technologies. Source: www.abb.com

• In November 2024, KUKA AG launched an upgraded robotic automation platform featuring enhanced vision-guided control systems, enabling more accurate handling of complex industrial tasks such as fuel dispensing. The system demonstrated a 25% improvement in alignment precision and reduced operational errors in pilot deployments. Source: www.kuka.com

• In July 2025, Mitsubishi Electric announced the deployment of next-generation factory automation systems incorporating robotic handling technologies applicable to automated fueling operations. The new systems achieved up to 30% faster cycle times and improved energy efficiency through advanced motion control algorithms. Source: www.mitsubishielectric.com

• In September 2024, FANUC Corporation introduced an enhanced series of collaborative robots equipped with high-sensitivity sensors and AI-based motion control, enabling safer interaction in industrial environments. These robots improved task efficiency by approximately 28% and reduced system calibration time significantly. Source: www.fanuc.com

The Robotic Refueling System Market Report provides a comprehensive evaluation of the global market landscape, covering a wide range of segments, technologies, applications, and regional dynamics. The report encompasses detailed segmentation by system type, including fixed, mobile, and hybrid robotic refueling solutions, which collectively represent over 95% of current deployments across industrial and commercial sectors. It further examines application areas such as defense, automotive, aviation, and industrial operations, with defense and aerospace accounting for more than 40% of total system utilization due to high demand for automated and unmanned fueling solutions.

Geographically, the report analyzes key regions including North America, Europe, Asia-Pacific, South America, and the Middle East & Africa, representing 100% of global market activity. It highlights regional adoption patterns, infrastructure development trends, and technological advancements, with over 60% of global installations concentrated in North America and Europe. The report also explores emerging markets where adoption is increasing due to rapid urbanization and industrial automation initiatives.

In terms of technology, the report covers AI-driven automation, IoT-enabled monitoring systems, multi-sensor integration, and predictive maintenance solutions, which are present in over 50% of modern robotic refueling systems. It also includes insights into advanced robotics, digital twin technology, and autonomous navigation systems that are shaping future market developments. Additionally, the report evaluates industry-specific use cases, regulatory frameworks, and sustainability initiatives, providing decision-makers with actionable insights into market opportunities, competitive positioning, and long-term growth potential across diverse industry verticals.

| Report Attribute/Metric | Report Details |

|---|---|

|

Market Revenue in 2025 |

USD V2025 Million |

|

Market Revenue in 2033 |

USD V2033 Million |

|

CAGR (2026 - 2033) |

28.4% |

|

Base Year |

2025 |

|

Forecast Period |

2026 - 2033 |

|

Historic Period |

2021 - 2025 |

|

Segments Covered |

By Types

By Application

By End-User

|

|

Key Report Deliverable |

Revenue Forecast, Growth Trends, Market Dynamics, Segmental Overview, Regional and Country-wise Analysis, Competition Landscape |

|

Region Covered |

North America, Europe, Asia-Pacific, South America, Middle East, Africa |

|

Key Players Analyzed |

ABB, KUKA AG, FANUC Corporation, Mitsubishi Electric Corporation, Hyundai Robotics, Yaskawa Electric Corporation, Universal Robots, Boston Dynamics, Schneider Electric, Siemens AG |

|

Customization & Pricing |

Available on Request (10% Customization is Free) |