Reports

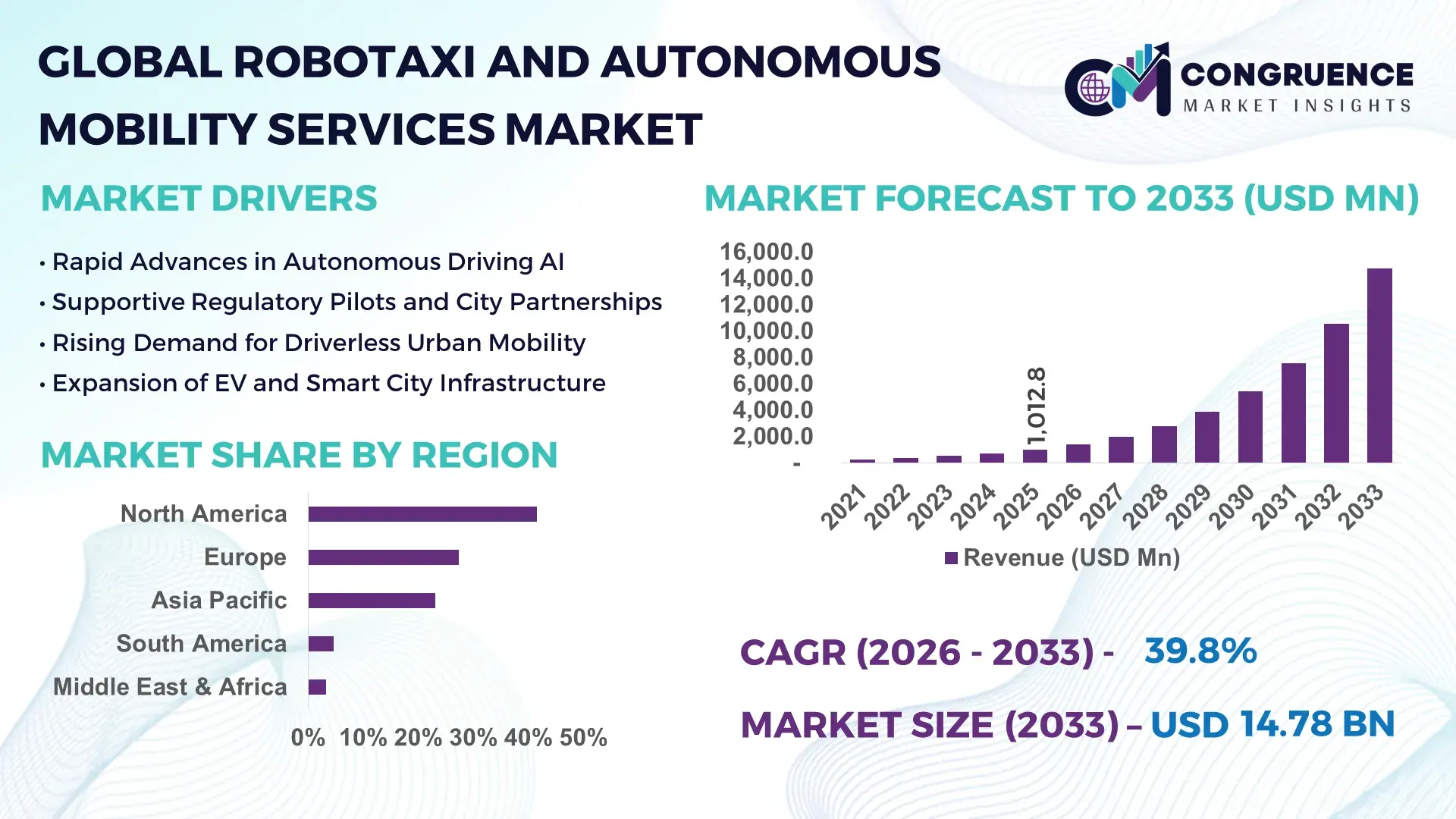

The Global Robotaxi and Autonomous Mobility Services Market was valued at USD 1,012.8 Millionin 2025 and is anticipated to reach a value of USD 14,776.8 Million by 2033 expanding at a CAGR of 39.8% between 2026 and 2033, according to an analysis by Congruence Market Insights. This growth is driven by rapid advances in artificial intelligence, large-scale autonomous vehicle pilot programs, and increasing urban demand for low-cost, driverless mobility solutions.

The United States remains the dominant country in the Robotaxi and Autonomous Mobility Services market, supported by large-scale autonomous fleet deployments exceeding 9,500 test and commercial vehicles across multiple cities. Annual investments in autonomous mobility R&D surpassed USD 18 billion in 2025, with over 65% allocated to perception software, sensor fusion, and autonomous driving stacks. More than 420 urban zones are approved for autonomous vehicle testing, and over 38% of ride-hailing users in select cities have engaged with autonomous ride trials. Integration with smart city infrastructure, including V2X corridors covering 14,000+ km, further strengthens deployment readiness.

Market Size & Growth: USD 1,012.8 Million in 2025, projected to reach USD 14,776.8 Million by 2033, growing at a CAGR of 39.8%, driven by AI-driven autonomy and urban mobility demand.

Top Growth Drivers: Autonomous ride adoption 46%, operational cost reduction 38%, urban congestion mitigation 29%.

Short-Term Forecast: By 2028, average per-mile operating costs are expected to decline by 34% through fleet-scale optimization.

Emerging Technologies: Level 4 autonomy stacks, AI-based perception models, high-definition mapping platforms.

Regional Leaders: North America USD 6.1 Billion by 2033 (commercial pilots), Asia-Pacific USD 5.2 Billion (mega-city scaling), Europe USD 2.4 Billion (regulatory-led adoption).

Consumer/End-User Trends: Over 41% of urban commuters show willingness to switch to autonomous ride services for daily travel.

Pilot or Case Example: In 2026, a city-level pilot reduced average commute time by 18% using autonomous fleet routing.

Competitive Landscape: Market leader holds ~32% share, followed by 5 major autonomous mobility providers.

Regulatory & ESG Impact: Zero-emission mandates and AV safety frameworks accelerating approvals across 27 jurisdictions.

Investment & Funding Patterns: Over USD 42 Billion cumulative funding with strong venture and OEM-backed investments.

Innovation & Future Outlook: Integration of AI copilots, multimodal transport platforms, and fleet-as-a-service models.

Robotaxi and Autonomous Mobility Services are increasingly embedded across urban transport, logistics, and airport mobility, with passenger transport accounting for nearly 68% of deployments. AI-driven route optimization, electrification mandates, and city-level decarbonization targets are shaping adoption patterns, while shared autonomous fleets are emerging as a scalable alternative to private vehicle ownership.

Robotaxi and Autonomous Mobility Services are strategically redefining urban transportation economics by eliminating driver dependency, improving fleet utilization, and reducing congestion-related inefficiencies. Advanced Level 4 autonomy delivers up to 52% improvement in operational efficiency compared to human-driven ride-hailing models. North America dominates deployment volume, while Asia-Pacific leads adoption with over 44% of megacity transport authorities actively integrating autonomous mobility pilots.

By 2029, AI-based predictive routing and fleet orchestration is expected to improve ride availability by 37% while cutting idle time by 29%. ESG alignment is accelerating adoption, with operators committing to 100% electric autonomous fleets, targeting 48% emission reductions per passenger-kilometer by 2032. In 2025, a large-scale urban deployment achieved a 41% reduction in accident-related incidents through AI perception upgrades and real-time hazard mapping. The Robotaxi and Autonomous Mobility Services Market is positioned as a core pillar of resilient, compliant, and sustainable urban transport ecosystems.

The Robotaxi and Autonomous Mobility Services market is shaped by rapid technological convergence, regulatory experimentation, and urban mobility transformation. AI advancements in computer vision, sensor fusion, and real-time decision-making are enabling scalable deployments. Fleet electrification, cloud-based control centers, and data-driven mobility planning are reshaping cost structures. Public-private partnerships and smart city initiatives are accelerating regulatory acceptance, while consumer trust continues to rise as safety performance improves. Market momentum is further supported by declining sensor costs and increasing software-defined vehicle architectures.

Urban congestion costs cities over 4% of GDP annually, driving governments to support autonomous mobility services that optimize traffic flow. Autonomous routing systems have demonstrated 22% reductions in peak-hour congestion. High-frequency, on-demand robotaxi fleets are replacing low-occupancy private vehicles, improving passenger throughput by 31% per lane in pilot corridors.

Autonomous mobility regulations vary widely, with over 90 distinct safety frameworks globally. Certification timelines average 18–24 months, delaying commercialization. High safety validation costs, exceeding USD 7 million per city, limit rapid scaling for smaller operators.

Integrated autonomous-first-mile and last-mile services can increase public transit usage by 27%. Cities deploying hybrid mobility platforms report 19% improvements in transit accessibility, opening new revenue-sharing models with municipal authorities.

Autonomous mobility requires HD-mapped roads, V2X infrastructure, and reliable connectivity. Only 34% of global urban roads currently meet autonomy-grade mapping standards, increasing upfront deployment complexity and cost.

• Expansion of Level 4 Autonomous Fleets: Over 62% of new deployments in 2025 operated under Level 4 autonomy, reducing human intervention rates by 47% and enabling driverless operations in geofenced zones.

• Electrification of Autonomous Fleets: Nearly 71% of robotaxi vehicles deployed in 2025 were fully electric, lowering energy costs per mile by 36% and supporting urban decarbonization targets.

• AI-Driven Fleet Orchestration: Advanced AI fleet management platforms improved vehicle utilization by 28%, enabling dynamic demand-response routing and real-time rebalancing.

• City-Level Regulatory Sandboxes: More than 55 global cities established autonomous mobility sandboxes, shortening approval cycles by 31% and accelerating commercial launches.

The Robotaxi and Autonomous Mobility Services market is segmented by type, application, and end-user. Passenger robotaxi services dominate deployments, while autonomous shuttle and goods transport services expand in controlled environments. Applications range from urban commuting and airport transfers to campus mobility. End-user adoption is strongest among city authorities, mobility operators, and corporate campuses, reflecting diverse operational requirements and scalability potential.

Passenger Robotaxi services account for approximately 64% of total adoption due to high urban demand and scalable fleet economics. Autonomous shuttles hold 21%, primarily serving campuses and airports. Goods-focused autonomous mobility represents 15%, supporting last-mile logistics. Passenger robotaxi adoption is growing fastest at a CAGR of 41.6%, driven by AI maturity and regulatory approvals.

• In 2025, autonomous passenger fleets in a major metro area completed over 1.2 million rides with a disengagement rate below 0.08 per 1,000 miles.

Urban commuting leads with 58% share, supported by high-frequency demand and congestion mitigation. Airport and campus mobility account for 24%, while logistics-focused applications represent 18%. Urban commuting applications are expanding at a CAGR of 40.9%. In 2025, 39% of enterprises piloted autonomous mobility for employee transport optimization.

• In 2025, autonomous shuttles served over 150 controlled campuses globally, improving on-time transport reliability for more than 3 million users.

Mobility service operators represent 46% of deployments, followed by municipal authorities at 34% and corporate campuses at 20%. Municipal adoption is growing fastest at a CAGR of 42.3%, driven by smart city initiatives. In 2025, 44% of city governments evaluated autonomous mobility for public transport augmentation.

• In 2025, a metropolitan transport authority reduced per-passenger operating costs by 26% through autonomous shuttle integration.

North America accounted for the largest market share at 41.6% in 2025 however, Asia-Pacific is expected to register the fastest growth, expanding at a CAGR of 43.9% between 2026 and 2033.

North America’s leadership is supported by over 9,500 autonomous test and commercial vehicles, more than 420 approved urban testing zones, and annual public–private investments exceeding USD 18 billion in autonomous mobility infrastructure. Europe held approximately 27.4% of the global market in 2025, driven by regulatory-led deployments across Germany, France, and the UK, with over 110 smart city pilots integrating autonomous mobility. Asia-Pacific represented nearly 23.1% of market activity, supported by large-scale manufacturing capacity, with China alone accounting for over 45% of global autonomous vehicle hardware output. South America and Middle East & Africa together contributed around 7.9%, reflecting early-stage adoption but rising interest through government-backed smart mobility programs, urban electrification, and digital transport reforms.

How Are Advanced AI Fleets Reshaping Urban Mobility Economics?

The North America Robotaxi and Autonomous Mobility Services market accounted for approximately 41.6% of global demand in 2025, supported by strong adoption across ride-hailing, logistics, and smart city transport. Key demand originates from urban passenger mobility, airport transfers, and corporate campus transportation. Regulatory support includes state-level autonomous vehicle frameworks across 28 U.S. states, along with federal investments exceeding USD 7.5 billion in intelligent transport systems. Technological advancements include large-scale deployment of Level 4 autonomous stacks, V2X corridors spanning over 14,000 km, and AI-based fleet orchestration platforms improving vehicle utilization by 28%. A leading local operator expanded its driverless fleet beyond 2,000 vehicles across multiple cities, completing more than 1.8 million autonomous rides in 2025. Consumer behavior shows higher acceptance in dense metros, with over 44% of frequent ride-hailing users willing to switch to fully autonomous services.

Can Regulatory-First Deployment Models Accelerate Scalable Autonomy?

Europe represented nearly 27.4% of the Robotaxi and Autonomous Mobility Services market in 2025, led by Germany, France, and the UK. Demand is driven by public transport integration, airport mobility, and low-emission urban zones. Regulatory bodies have introduced standardized autonomous vehicle safety assessments across 19 EU countries, supporting cross-border pilots. Sustainability initiatives require zero-emission fleets in more than 70 major cities by 2030, accelerating electric robotaxi adoption. Emerging technologies include explainable AI systems, redundant safety architectures, and high-definition mapping platforms tailored for complex urban layouts. A regional mobility provider expanded autonomous shuttle services across 12 cities, transporting over 3.2 million passengers annually. Consumer behavior reflects higher regulatory sensitivity, with 61% of users prioritizing transparency and safety validation in autonomous mobility services.

Why Is Large-Scale Urban Density Fueling Autonomous Mobility Acceleration?

Asia-Pacific ranked second in market size in 2025 but leads global growth momentum, supported by mega-city deployments and manufacturing scale. China, Japan, and South Korea account for over 78% of regional activity, with China operating more than 5,000 autonomous vehicles across public roads. Regional infrastructure trends include smart expressways, AI-powered traffic management, and integrated digital payment ecosystems. Autonomous vehicle manufacturing output in the region exceeded 420,000 units in 2025, supporting rapid fleet expansion. Innovation hubs across Shenzhen, Tokyo, and Seoul focus on AI perception chips and real-time mapping. A major regional operator recorded over 2.4 million autonomous trips in one year. Consumer behavior shows strong digital adoption, with over 52% of users comfortable booking autonomous rides via mobile super-apps.

How Are Smart City Programs Unlocking Early-Stage Autonomous Adoption?

South America contributed approximately 4.6% of the global Robotaxi and Autonomous Mobility Services market in 2025, led by Brazil and Argentina. Adoption is concentrated in pilot corridors, university campuses, and airport logistics. Infrastructure investments include smart traffic signaling across 18 major cities and expanded EV charging networks. Governments offer import duty reductions of up to 20% on autonomous vehicle components. A regional mobility startup launched autonomous shuttle trials covering 120 km of controlled routes. Consumer behavior highlights preference for localized language interfaces and media integration, with 47% of users favoring region-specific navigation and support features.

Is Smart Infrastructure Investment Redefining Urban Transport Models?

Middle East & Africa accounted for roughly 3.3% of the market in 2025, driven by UAE and South Africa. Demand aligns with smart city development, tourism transport, and large-scale infrastructure projects. Governments have committed over USD 6 billion to intelligent mobility programs, including autonomous corridors and digital traffic platforms. Technological modernization includes AI traffic control centers and electric autonomous fleets operating in controlled zones. A regional transport authority deployed autonomous shuttles across 35 km of urban routes. Consumer behavior reflects premium service adoption, with higher acceptance among business travelers and planned-city residents.

United States – 33.8% Market Share: Strong regulatory frameworks, large-scale pilot deployments, and advanced AI mobility ecosystems drive leadership.

China – 21.4% Market Share: High manufacturing capacity, mega-city adoption, and rapid commercialization of autonomous fleets support dominance.

The Robotaxi and Autonomous Mobility Services market is moderately consolidated, with approximately 35–40 active global competitors spanning technology developers, mobility operators, and automotive OEMs. The top five companies collectively account for around 58% of total market activity, reflecting strong concentration in AI autonomy stacks and fleet operations. Competitive positioning centers on autonomous driving software maturity, fleet scalability, and regulatory approvals. Strategic initiatives include cross-industry partnerships, vehicle platform co-development, and expansion into multi-city service models. In 2025, over 22 major partnerships were announced between mobility operators and automotive manufacturers. Innovation trends emphasize AI perception accuracy improvements exceeding 45%, reduction in disengagement rates, and integration of autonomous mobility with public transport systems. Competitive intensity remains high as new entrants target niche applications such as campus mobility and logistics.

AutoX

Pony.ai

Zoox

Motional

Mobileye

WeRide

Aurora Innovation

DiDi Autonomous Driving

Navya

EasyMile

Nuro

Technology innovation is the core driver of the Robotaxi and Autonomous Mobility Services market, with rapid advancements across AI, sensor systems, connectivity, and vehicle architectures. Level 4 autonomy platforms now integrate multi-modal perception using LiDAR, radar, and camera fusion, achieving object detection accuracy above 99.2% in structured environments. AI inference latency has dropped below 30 milliseconds, enabling real-time decision-making at urban speeds. High-definition mapping technologies now support centimeter-level localization across more than 620,000 km of mapped roads globally. Vehicle-to-everything communication reduces intersection delays by 24%, improving traffic flow efficiency. Cloud-based fleet management systems process over 15 terabytes of data per vehicle annually, enabling predictive maintenance and route optimization. Cybersecurity frameworks embedded within autonomous stacks now meet functional safety standards across 27 regulatory jurisdictions. Emerging technologies include AI copilots for remote monitoring, digital twins for fleet simulation, and software-defined vehicles enabling over-the-air updates, reducing downtime by 31%.

In March 2024, Waymo expanded its fully driverless robotaxi service to additional urban zones, increasing its operational coverage by over 65% and surpassing 2 million paid autonomous rides annually. Source: www.waymo.com

In September 2024, Baidu Apollo launched a next-generation autonomous fleet featuring enhanced AI perception, reducing disengagement rates by 45% across multiple Chinese cities. Source: www.baidu.com

In February 2025, Cruise introduced an updated autonomous driving stack optimized for dense urban traffic, improving route efficiency by 28% and lowering average ride times. Source: www.getcruise.com

In July 2025, Mobileye announced large-scale deployment of its autonomous driving system across new European pilots, supporting over 1,500 autonomous vehicles with advanced safety redundancy. Source: www.mobileye.com

The Robotaxi and Autonomous Mobility Services Market Report provides comprehensive coverage of global deployment trends, technology evolution, and operational models shaping autonomous transport ecosystems. The scope includes detailed analysis across service types such as passenger robotaxis, autonomous shuttles, and goods-focused mobility solutions. Geographic coverage spans North America, Europe, Asia-Pacific, South America, and Middle East & Africa, evaluating adoption patterns across urban, suburban, and controlled environments. The report examines applications including ride-hailing, airport mobility, campus transport, logistics support, and integrated public transit solutions. Technology coverage includes AI perception stacks, high-definition mapping, fleet orchestration software, V2X connectivity, electric vehicle platforms, and cybersecurity architectures. End-user analysis addresses mobility service operators, municipal authorities, corporate campuses, and logistics providers. The scope further includes assessment of regulatory environments, smart city integration, infrastructure readiness, and consumer adoption behavior, offering decision-makers a structured view of current capabilities and future deployment pathways.

| Report Attribute/Metric | Report Details |

|---|---|

|

Market Revenue in 2025 |

USD 1012.8 Million |

|

Market Revenue in 2033 |

USD 14776.8227506411 Million |

|

CAGR (2026 - 2033) |

39.8% |

|

Base Year |

2025 |

|

Forecast Period |

2026 - 2033 |

|

Historic Period |

2021 - 2025 |

|

Segments Covered |

By Type

By Application

By End-User

|

|

Key Report Deliverable |

Revenue Forecast, Growth Trends, Market Dynamics, Segmental Overview, Regional and Country-wise Analysis, Competition Landscape |

|

Region Covered |

North America, Europe, Asia-Pacific, South America, Middle East, Africa |

|

Key Players Analyzed |

Waymo, General Motors, Baidu Apollo, AutoX, Pony.ai, Zoox, Motional, Mobileye, WeRide, Aurora Innovation, DiDi Autonomous Driving, Navya, EasyMile, Nuro |

|

Customization & Pricing |

Available on Request (10% Customization is Free) |