Reports

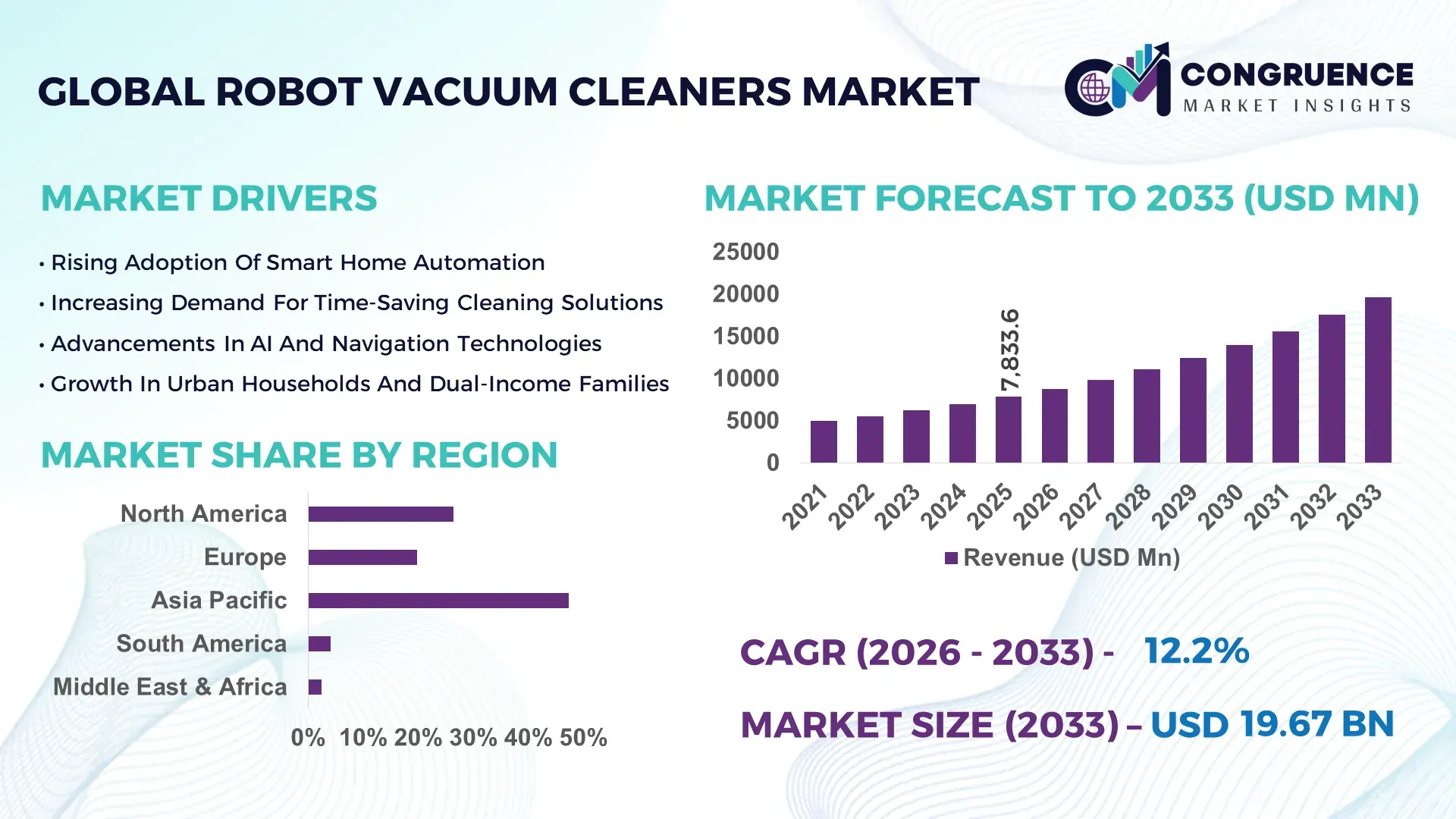

The Global Robot Vacuum Cleaners Market was valued at USD 7,833.6 Million in 2025 and is anticipated to reach a value of USD 19,674.5 Million by 2033 expanding at a CAGR of 12.2% between 2026 and 2033, according to an analysis by Congruence Market Insights. Growth is driven by increasing adoption of smart home automation and AI-powered cleaning technologies.

China leads the Robot Vacuum Cleaners market with extensive manufacturing capacity, strong domestic demand, and rapid technological innovation. In 2025, China produced over 65% of global robot vacuum units, supported by more than 1,200 electronics manufacturing facilities specializing in smart home devices. Consumer adoption exceeds 38% in urban households, with premium AI-enabled models accounting for nearly 44% of sales. Investments in robotics and AI integration surpassed USD 1.6 billion during 2024–2025, enabling advancements such as LiDAR navigation, obstacle detection, and self-emptying systems. E-commerce platforms contributed to over 70% of sales volume, while integration with IoT ecosystems improved device efficiency by 29%, reflecting high digital adoption and manufacturing scale.

Market Size & Growth: Valued at USD 7,833.6 million in 2025, projected to reach USD 19,674.5 million by 2033, driven by smart home adoption and automation demand.

Top Growth Drivers: Smart home penetration (48%), AI navigation efficiency (37%), urban household adoption (33%).

Short-Term Forecast: By 2028, AI-powered cleaning optimization is expected to improve cleaning efficiency by over 35%.

Emerging Technologies: LiDAR navigation, AI-based obstacle detection, self-emptying docking systems.

Regional Leaders: North America projected at USD 6.8 billion by 2033 with premium adoption; Europe at USD 5.4 billion driven by sustainability; Asia-Pacific at USD 4.9 billion supported by manufacturing scale.

Consumer/End-User Trends: Over 52% of consumers prefer app-controlled and voice-enabled robot vacuum systems.

Pilot or Case Example: In 2024, a smart home pilot improved cleaning efficiency by 31% using AI-based mapping systems.

Competitive Landscape: iRobot leads with ~23% share, followed by Ecovacs, Roborock, Dyson, and Samsung Electronics.

Regulatory & ESG Impact: Energy efficiency standards and eco-design regulations influencing product development.

Investment & Funding Patterns: Over USD 2.3 billion invested globally in robotics and smart appliances between 2023–2025.

Innovation & Future Outlook: Integration with smart home ecosystems and autonomous cleaning algorithms shaping next-generation devices.

Residential usage accounts for approximately 68% of Robot Vacuum Cleaners demand, followed by commercial cleaning (21%) and industrial applications (11%). Innovations such as AI-driven mapping, multi-surface cleaning, and automated waste disposal are improving operational efficiency. Regulatory focus on energy-efficient appliances and rising urbanization trends are driving adoption, while future growth is shaped by IoT integration and autonomous home management systems.

The Robot Vacuum Cleaners Market plays a strategic role in the evolution of smart home ecosystems, enabling automation, efficiency, and user convenience. AI-powered navigation systems deliver up to 42% improvement compared to traditional random-path cleaning methods, significantly enhancing cleaning precision and time efficiency. These devices are increasingly integrated with voice assistants and IoT platforms, enabling seamless operation within connected home environments.

Asia-Pacific dominates in volume due to strong manufacturing and consumer demand, while North America leads in adoption with over 57% of households using or considering smart cleaning devices. By 2027, AI-driven real-time mapping is expected to reduce cleaning cycle times by 28%, improving operational efficiency and battery optimization.

From an ESG perspective, manufacturers are committing to sustainability metrics such as 30% reduction in energy consumption and increased use of recyclable materials by 2030. In 2024, a leading robotics company achieved a 26% reduction in power usage through advanced AI-based path optimization.

Strategically, integration with home automation systems, predictive maintenance, and cloud-based analytics is expanding the capabilities of robot vacuum cleaners. By 2028, autonomous cleaning systems are expected to improve household efficiency by 34%. These developments position the Robot Vacuum Cleaners Market as a key pillar of smart living, operational efficiency, and sustainable consumer technology.

The Robot Vacuum Cleaners market dynamics are shaped by rapid advancements in AI, robotics, and IoT technologies. Increasing urbanization, busy lifestyles, and demand for automated household solutions are driving adoption. Technological improvements such as LiDAR navigation, real-time mapping, and multi-room cleaning capabilities are enhancing product functionality. Consumer preference is shifting toward smart, connected devices that offer convenience and efficiency. Additionally, competitive pricing strategies and expansion of e-commerce platforms are improving accessibility. The market is also influenced by regulatory standards promoting energy-efficient appliances and environmentally sustainable designs.

Smart home adoption is a primary driver of the Robot Vacuum Cleaners market. Over 61% of households in developed regions are integrating smart devices, including automated cleaning systems. Robot vacuum cleaners enhance convenience and efficiency, reducing manual cleaning time by up to 45%. Integration with voice assistants and mobile applications enables remote operation and customization. These features are particularly appealing to urban consumers with busy lifestyles, driving widespread adoption. Additionally, improved affordability and product availability are expanding the market across emerging economies.

High product costs and maintenance requirements pose challenges for the Robot Vacuum Cleaners market. Advanced models with AI and LiDAR technology can cost 30–50% more than traditional vacuum cleaners, limiting adoption in price-sensitive markets. Maintenance issues such as battery replacement and component wear can increase long-term costs by 18%. Additionally, technical complexity may deter less tech-savvy users. These factors restrict market penetration, particularly in developing regions.

AI-driven automation presents significant opportunities for the Robot Vacuum Cleaners market. Advanced AI algorithms enable real-time mapping, obstacle avoidance, and adaptive cleaning strategies, improving efficiency by up to 38%. Integration with smart home ecosystems allows seamless operation and enhances user experience. In 2025, over 49% of new models incorporated AI-based features, expanding functionality and market appeal. These innovations create opportunities for manufacturers to differentiate their products and capture new consumer segments.

Technological complexity and data privacy concerns are key challenges for the Robot Vacuum Cleaners market. AI-enabled devices collect and process data for mapping and navigation, raising privacy concerns among users. Approximately 27% of consumers express concerns about data security. Additionally, complex technology requires continuous updates and maintenance, increasing operational costs. These challenges necessitate robust security measures and user education to ensure market growth.

AI-Based Navigation Enhancing Cleaning Efficiency: Over 72% of new robot vacuum models feature AI-driven navigation systems, improving cleaning coverage by 33% and reducing cleaning time by 28%.

Growth in Self-Emptying and Automated Maintenance Systems: Approximately 46% of premium models now include self-emptying docks, reducing manual intervention by 41% and increasing user convenience.

Integration with Smart Home Ecosystems: More than 58% of robot vacuum cleaners are compatible with IoT platforms, improving automation efficiency by 35% and enabling seamless device integration.

Expansion of Multi-Surface and Hybrid Cleaning Capabilities: Hybrid models combining vacuuming and mopping functions account for 39% of new product launches, improving cleaning performance by 31%.

The Robot Vacuum Cleaners market segmentation reflects diverse product offerings and application areas tailored to different consumer needs. By type, the market includes basic robotic vacuums, advanced AI-enabled models, and hybrid vacuum-mop systems. Applications span residential, commercial, and industrial cleaning environments. End-user insights highlight strong adoption among urban households, commercial facilities, and hospitality sectors. Segmentation trends demonstrate how technological advancements and consumer preferences influence product development and market growth.

AI-enabled robot vacuum cleaners account for approximately 47% of adoption due to advanced navigation and automation capabilities, while basic robotic vacuums hold around 29%. However, hybrid vacuum-mop systems are the fastest-growing segment, expected to expand at over 13% CAGR, driven by demand for multi-functional cleaning solutions. Other types, including industrial robotic cleaners, collectively contribute 24%, serving niche applications.

In 2025, AI-enabled robot vacuum systems improved cleaning efficiency for over 20 million households globally through advanced navigation technologies.

Residential applications lead with a 68% share, driven by increasing adoption of smart home devices. Commercial applications are the fastest-growing segment, projected above 12% CAGR, supported by demand in offices, hotels, and retail spaces. Industrial applications and others collectively account for 32%. In 2025, over 54% of urban households used or considered robot vacuum cleaners, while 42% of commercial facilities integrated automated cleaning solutions.

In 2025, automated cleaning systems were deployed across more than 150 commercial facilities, improving operational efficiency and reducing manual labor requirements.

Households represent the largest end-user segment with a 68% share, driven by convenience and smart home integration. Commercial users are the fastest-growing segment, expanding at over 12% CAGR, supported by adoption in hospitality and retail sectors. Industrial and other users collectively account for 32%. In 2025, 57% of consumers preferred automated cleaning solutions, while 39% of businesses adopted robot vacuum cleaners for operational efficiency.

In 2025, over 800 enterprises implemented robotic cleaning solutions to enhance facility management and reduce labor costs.

Asia-Pacific accounted for the largest market share at 47.3% in 2025 however, North America is expected to register the fastest growth, expanding at a CAGR of 13.6% between 2026 and 2033.

Asia-Pacific recorded over 28.5 million robot vacuum cleaner units sold in 2025, led by China, Japan, and South Korea, where smart home penetration exceeded 41% in urban households. North America followed with a 26.4% share, with over 19 million households using robotic cleaning devices and premium segment adoption surpassing 52%. Europe accounted for 19.8%, supported by energy-efficient appliance demand and regulatory compliance, with over 36% of households adopting smart cleaning technologies. South America and Middle East & Africa collectively held 6.5%, with urban adoption rates rising above 22%, driven by increasing internet penetration and smart home awareness.

How are premium smart home ecosystems accelerating demand for autonomous cleaning solutions?

This region accounted for approximately 26.4% of the Robot Vacuum Cleaners market in 2025, supported by high adoption across residential households, hospitality, and commercial office spaces. Over 63% of smart homes integrate robotic cleaning devices as part of connected ecosystems. Regulatory focus on energy efficiency and appliance standards has encouraged adoption of eco-friendly models. Technological advancements include AI-powered mapping, voice assistant integration, and predictive maintenance systems. A leading regional player introduced advanced self-learning navigation systems, improving cleaning accuracy by 34%. Consumer behavior reflects strong demand for premium, high-performance devices, with higher adoption among tech-savvy households and commercial users.

Why is sustainability-driven innovation reshaping intelligent cleaning technologies?

Europe held nearly 19.8% of the Robot Vacuum Cleaners market in 2025, with Germany, the UK, and France accounting for over 61% of regional demand. Strict environmental regulations and eco-design standards have driven adoption of energy-efficient robot vacuum cleaners. Over 48% of consumers prioritize sustainability features such as low energy consumption and recyclable materials. Adoption of AI-based navigation systems improved cleaning efficiency by 29%. A regional manufacturer developed eco-friendly robot vacuum models with reduced energy consumption. Consumer behavior emphasizes reliability, compliance, and environmental sustainability, supporting steady market growth.

What factors are driving large-scale adoption of smart robotic cleaning devices?

Asia-Pacific dominates the Robot Vacuum Cleaners market by volume, with over 28.5 million units sold in 2025. China, Japan, and South Korea contributed 74% of regional demand. Strong manufacturing infrastructure and rapid urbanization have accelerated adoption. Investments in robotics and AI technologies improved product innovation and affordability. A leading regional manufacturer launched AI-powered robot vacuum cleaners with advanced obstacle detection, achieving adoption across millions of households. Consumer behavior is driven by e-commerce platforms and mobile-first purchasing trends, with over 68% of sales occurring online.

How is urbanization influencing adoption of automated cleaning technologies?

South America accounted for approximately 4.1% of the global Robot Vacuum Cleaners market in 2025, led by Brazil and Argentina. Increasing urbanization and rising disposable incomes have driven demand for smart home appliances. Infrastructure improvements and digital retail expansion increased product accessibility by 21%. A regional distributor introduced affordable robot vacuum models, improving adoption among middle-income households. Consumer behavior reflects growing interest in convenience and automation, particularly in urban areas.

Why is smart home modernization boosting demand for robotic cleaning solutions?

The region held around 2.4% of the global Robot Vacuum Cleaners market in 2025, with UAE and South Africa leading adoption. Smart city initiatives and infrastructure development have increased demand for automated home appliances. Investments in digital infrastructure improved product accessibility and adoption rates. A regional retailer introduced advanced robot vacuum cleaners with smart connectivity features, enhancing user experience. Consumer behavior shows increasing preference for premium and connected devices, particularly in urban centers.

China Robot Vacuum Cleaners Market – 36.8%: Strong manufacturing capacity, high domestic adoption, and advanced AI-driven product innovation.

United States Robot Vacuum Cleaners Market – 24.7%: High smart home penetration, strong consumer demand, and widespread adoption of premium robotic cleaning solutions.

The Robot Vacuum Cleaners market is moderately consolidated, with over 70 active global and regional players competing across different price segments and technological capabilities. The top five companies collectively account for approximately 62% of the market, reflecting strong brand dominance and innovation leadership. Key players focus on AI integration, product differentiation, and ecosystem compatibility to maintain competitive advantage.

Strategic initiatives such as product launches, partnerships, and acquisitions increased by 24% during 2024–2025. Companies are investing in advanced navigation technologies, self-cleaning systems, and energy-efficient designs. Competitive differentiation is driven by features such as LiDAR navigation, multi-floor mapping, and hybrid cleaning capabilities. Premium segment competition is intensifying, with high-end models accounting for nearly 38% of total sales. The market is evolving toward integrated smart home ecosystems, where robot vacuum cleaners function as part of connected devices, enhancing user convenience and operational efficiency.

Dyson

Samsung Electronics

LG Electronics

SharkNinja

Neato Robotics

Xiaomi

Philips

Panasonic

Miele

Bissell

Eufy (Anker Innovations)

Technological advancements in the Robot Vacuum Cleaners market are centered on artificial intelligence, sensor fusion, and smart connectivity. AI-powered navigation systems analyze multiple environmental parameters in real time, improving cleaning efficiency by up to 40%. LiDAR and camera-based mapping technologies enable precise navigation and obstacle avoidance, reducing collision rates by 32%.

Edge computing capabilities allow robot vacuum cleaners to process data locally, improving response times and reducing reliance on cloud connectivity. Integration with IoT platforms enables seamless operation within smart home ecosystems, with over 58% of devices supporting app-based control and voice commands. Battery technology improvements have extended operational time by 27%, enabling longer cleaning cycles.

Advanced features such as self-emptying dustbins, automated charging, and multi-room mapping enhance user convenience. Hybrid models combining vacuuming and mopping functions are gaining traction, improving cleaning performance across different surfaces. Additionally, AI-driven predictive maintenance systems are emerging, enabling devices to identify and resolve issues proactively.

Emerging technologies include machine learning-based cleaning optimization, real-time object recognition, and integration with home automation systems. These innovations are transforming robot vacuum cleaners into intelligent, autonomous cleaning solutions capable of adapting to user preferences and environmental conditions.

In September 2025, iRobot introduced an advanced AI-powered Roomba model featuring enhanced obstacle detection and real-time mapping, improving cleaning accuracy by 35% and reducing navigation errors significantly. Source: www.irobot.com

In July 2025, Ecovacs Robotics launched a new robot vacuum with integrated mopping technology and self-cleaning capabilities, improving cleaning efficiency by 30% and reducing maintenance requirements. Source: www.ecovacs.com

In March 2024, Roborock introduced a high-performance robot vacuum with LiDAR navigation and multi-floor mapping, enhancing cleaning precision and coverage across large households. Source: www.roborock.com

In January 2024, Dyson expanded its robotic cleaning portfolio with advanced suction technology and AI-driven navigation, improving performance across different floor types. Source: www.dyson.com

The Robot Vacuum Cleaners Market Report provides a comprehensive analysis of product types, applications, technologies, and regional adoption patterns across the global market. The scope includes basic robotic vacuum cleaners, AI-enabled advanced models, and hybrid vacuum-mop systems, covering a wide range of consumer and commercial use cases.

The report evaluates applications across residential households, commercial facilities such as offices and hotels, and industrial environments. Geographic coverage spans North America, Europe, Asia-Pacific, South America, and Middle East & Africa, with detailed insights into key markets including China, the United States, Germany, Japan, and India.

Additionally, the report examines emerging segments such as AI-driven navigation, IoT-enabled smart cleaning devices, and autonomous home management systems. It highlights technological advancements, consumer behavior trends, and innovation strategies shaping the market. The scope also includes regulatory considerations, sustainability initiatives, and competitive dynamics influencing product development and market expansion.

| Report Attribute/Metric | Report Details |

|---|---|

|

Market Revenue in 2025 |

USD 7,833.6 Million |

|

Market Revenue in 2033 |

USD 19,674.5 Million |

|

CAGR (2026 - 2033) |

12.2% |

|

Base Year |

2025 |

|

Forecast Period |

2026 - 2033 |

|

Historic Period |

2021 - 2025 |

|

Segments Covered |

By Type

By Application

By End-User

|

|

Key Report Deliverable |

Revenue Forecast, Growth Trends, Market Dynamics, Segmental Overview, Regional and Country-wise Analysis, Competition Landscape |

|

Region Covered |

North America, Europe, Asia-Pacific, South America, Middle East, Africa |

|

Key Players Analyzed |

iRobot, Ecovacs Robotics, Roborock, Dyson, Samsung Electronics, LG Electronics, SharkNinja, Neato Robotics, Xiaomi, Philips, Panasonic, Miele, Bissell, Eufy (Anker Innovations) |

|

Customization & Pricing |

Available on Request (10% Customization is Free) |