Reports

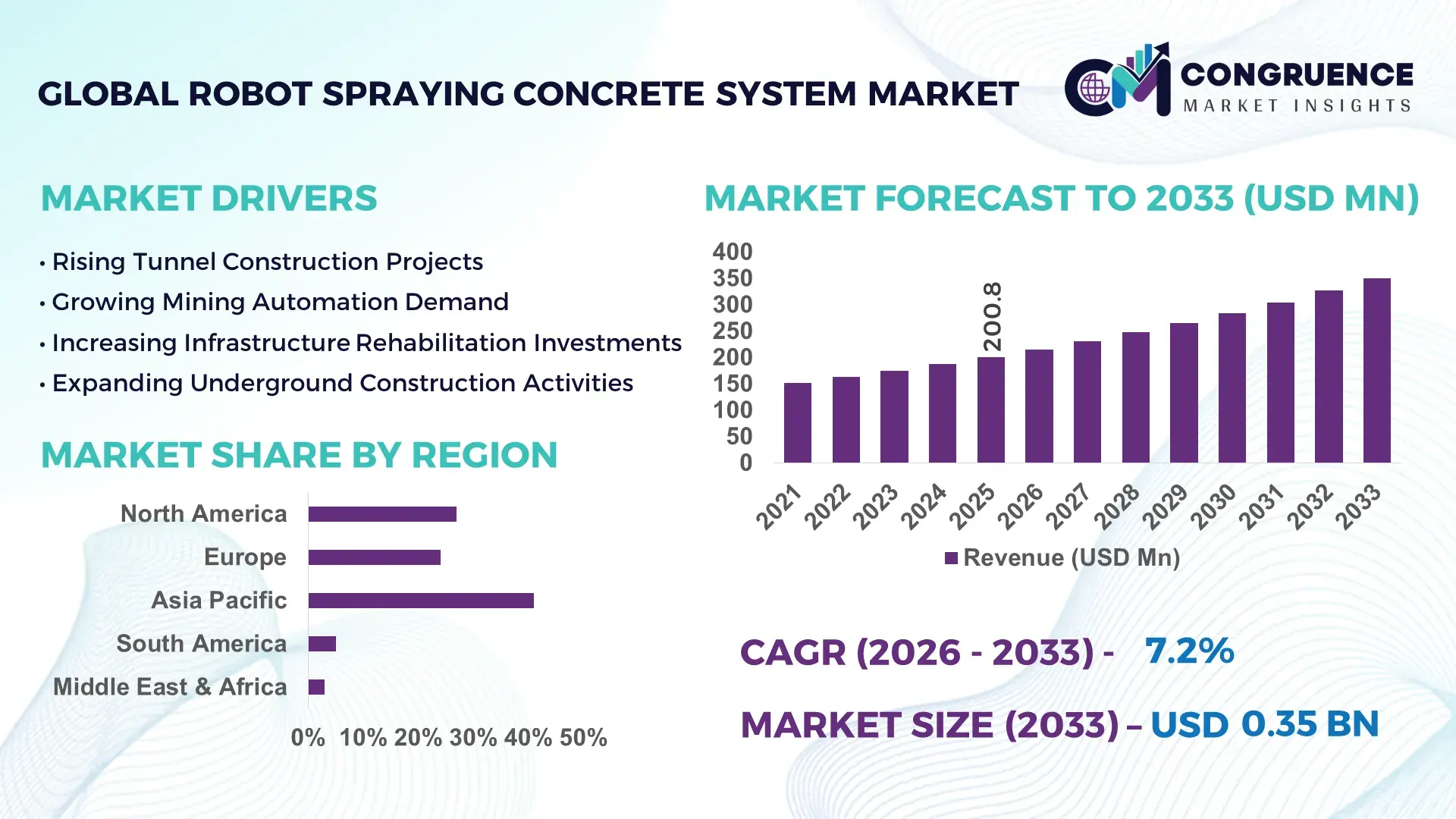

The Global Robot Spraying Concrete System Market was valued at USD 200.8 Million in 2025 and is anticipated to reach a value of USD 350.2 Million by 2033 expanding at a CAGR of 7.2% between 2026 and 2033. Rising labor shortages across large-scale infrastructure and underground construction projects are accelerating automated shotcrete deployment, with robotic systems improving material utilization by nearly 28% while reducing application time by over 35% compared to conventional manual spraying operations. Between 2024 and 2026, stricter worker safety mandates, tunnel modernization projects, and growing investment in smart infrastructure across Asia and Europe have intensified demand for high-precision robotic concrete spraying systems, particularly amid ongoing global supply chain restructuring and rising urban transit investments.

China dominates the global Robot Spraying Concrete System Market with approximately 31% market share, supported by aggressive railway tunnel expansion, mining automation programs, and high-speed infrastructure development exceeding 4,000 km annually. More than 45% of newly commissioned underground construction projects in China integrated semi-automated or fully automated shotcrete systems during 2025, compared to below 22% adoption across several developing regions. Government-backed smart construction initiatives and domestic robotics manufacturing capacity have reduced operational deployment costs by nearly 18%, strengthening China’s execution advantage over North America and Europe in large-volume infrastructure applications.

This dominance is reshaping supplier strategies, forcing manufacturers to prioritize automation scalability, localized production, and high-efficiency spraying technologies to remain globally competitive.

Market Size & Growth: USD 200.8 million in 2025 reaches USD 350.2 million by 2033, driven by tunnel automation and 35% faster shotcrete deployment efficiency.

Top Growth Drivers: Labor shortages contribute 38% demand acceleration, infrastructure automation 34%, and mining modernization 28% globally.

Short-Term Forecast: By 2028, robotic spraying systems are projected to reduce material waste by 22% and labor dependency by 31%.

Emerging Technologies: AI-guided spraying, LiDAR positioning, and automated nozzle calibration improve precision rates by over 27%.

Regional Leaders: Asia-Pacific exceeds USD 118 million demand, Europe strengthens ESG adoption, while North America expands mining automation deployment.

Consumer/End-User Trends: Nearly 49% of underground infrastructure contractors now prioritize automated shotcrete systems for safety compliance.

Pilot/Case Example: In 2025, a Scandinavian tunnel project improved spraying consistency by 33% and reduced rebound waste by 24%.

Competitive Landscape: Top players control nearly 42% market share, led by Putzmeister, Normet, Sika, CIFA, and Epiroc.

Regulatory & ESG Impact: Automated spraying systems reduce concrete wastage by 20% while supporting stricter occupational safety compliance targets.

Investment & Funding: Over USD 90 million was allocated toward robotic construction automation partnerships and underground equipment expansion projects.

Innovation & Future Outlook: Autonomous fleet integration and digital twin-enabled spraying optimization are redefining high-efficiency infrastructure execution globally.

Underground infrastructure projects account for nearly 44% of global Robot Spraying Concrete System demand, followed by mining operations at 29% and transportation infrastructure at 18%. Manufacturers are increasingly integrating AI-assisted nozzle positioning and sensor-based thickness monitoring systems, improving application precision by over 25%. Asia-Pacific continues dominating deployment volume due to rapid tunnel construction, while Europe is accelerating adoption through stricter worker safety and sustainability mandates. Rising localization of robotic construction equipment manufacturing amid global supply chain diversification is further reshaping procurement strategies. These shifts are positioning automation-driven concrete spraying systems as a long-term strategic infrastructure investment priority.

The Robot Spraying Concrete System Market is rapidly transforming into a critical automation segment within global infrastructure, mining, and underground construction ecosystems as contractors aggressively shift toward labor-efficient, precision-driven execution models. Escalating urban transit investments, tunnel expansion programs, and worker safety enforcement are accelerating demand for robotic shotcrete systems capable of optimizing material utilization while reducing human exposure in hazardous environments. Construction firms are increasingly prioritizing automation-led productivity models as project delays, labor shortages, and operational inefficiencies intensify competitive pressure across high-value infrastructure contracts.

Global infrastructure supply chains are simultaneously shifting toward localized equipment sourcing and digitally integrated construction operations, forcing manufacturers to accelerate automation-focused capital allocation strategies. AI-assisted robotic spraying technology improves application consistency by nearly 32% while reducing rebound material waste by approximately 24% compared to legacy manual spraying systems. Europe leads in innovation-focused adoption, with automated safety-compliant deployments increasing above 41%, while Asia-Pacific dominates global deployment volume due to large-scale tunnel and railway infrastructure expansion.

Over the next three years, robotic spraying integration across underground infrastructure projects is projected to increase operational productivity by more than 29%, while reducing dependency on skilled manual spraying labor by nearly 34%. ESG positioning is also becoming a competitive advantage, as automated systems reduce concrete overuse and lower dust exposure, improving environmental compliance and workforce safety metrics simultaneously. In 2025, a large Nordic tunnel modernization project using AI-guided robotic spraying systems improved structural coating precision by 30% while shortening execution timelines by 19%.

Major construction equipment manufacturers are now shifting investment toward autonomous fleet coordination, sensor-based spraying analytics, and modular robotic deployment systems to capture high-growth infrastructure contracts. Companies prioritizing automation scalability, predictive maintenance integration, and digital construction ecosystems are strengthening long-term competitive positioning as infrastructure modernization accelerates globally.

The Robot Spraying Concrete System Market is being reshaped by rapid automation adoption across underground construction, mining, and transportation infrastructure sectors. Rising pressure to improve worker safety, reduce project delays, and optimize material efficiency is accelerating deployment of robotic shotcrete systems across high-risk environments. Automated spraying technologies now improve spraying consistency by nearly 30% while lowering rebound material losses by more than 20%, making them increasingly attractive for large-scale infrastructure contractors. Tunnel modernization projects, railway expansion, and mining automation initiatives across Asia-Pacific and Europe are intensifying procurement activity. Simultaneously, stricter workplace safety regulations and labor shortages are forcing construction firms to replace manual spraying operations with digitally controlled robotic systems. Manufacturers are responding through AI-enabled spraying automation, localized production expansion, and integrated monitoring technologies, reshaping competitive dynamics and long-term infrastructure execution models.

Severe shortages of skilled construction labor and rising infrastructure execution pressure are forcing rapid adoption of robotic spraying concrete systems across tunnels, mining operations, and underground transit projects. Automated spraying systems reduce labor dependency by nearly 31% while improving application speed by over 35%, enabling contractors to maintain project timelines despite workforce constraints. Large-scale railway tunnel investments across China, India, and the Middle East have intensified demand for automated shotcrete equipment capable of continuous high-volume operation. Simultaneously, stricter occupational safety standards are accelerating replacement of hazardous manual spraying activities. More than 46% of newly commissioned underground infrastructure projects now include semi-automated spraying technologies as contractors prioritize efficiency and compliance. In response, leading manufacturers are expanding regional production facilities, accelerating AI-integrated equipment launches, and forming strategic partnerships with infrastructure engineering firms to capture high-growth automation demand.

High upfront equipment costs, operational calibration complexity, and dependence on advanced maintenance infrastructure remain major barriers restricting widespread Robot Spraying Concrete System adoption. Fully automated robotic spraying units can increase initial project equipment expenditure by nearly 25% compared to conventional manual systems, limiting penetration among mid-sized contractors. In several developing markets, inconsistent power infrastructure and limited access to specialized robotic maintenance services are increasing operational downtime risks by approximately 18%. Supply concentration for precision sensors, hydraulic components, and automation software is also creating procurement bottlenecks, particularly amid ongoing global industrial supply chain realignment. These challenges directly impact scalability and deployment consistency across cost-sensitive regions. To mitigate risks, companies are increasingly diversifying supplier networks, developing modular robotic systems with simplified maintenance requirements, and offering long-term service contracts to reduce operational uncertainty and improve adoption confidence.

AI-enabled robotic spraying systems and smart infrastructure modernization initiatives are creating high-impact growth opportunities across the Robot Spraying Concrete System Market. Advanced sensor-guided spraying platforms improve application precision by nearly 27% while reducing concrete wastage by over 20%, generating measurable cost advantages for infrastructure contractors. Emerging economies are accelerating tunnel construction, metro rail expansion, and underground mining automation programs, creating new deployment opportunities beyond traditional mature markets. More than 39% of infrastructure automation investments announced during 2025 included robotic construction technologies as governments prioritize long-term operational efficiency and workforce safety. Autonomous nozzle adjustment systems, digital twin integration, and real-time thickness monitoring are redefining operational performance standards. In response, manufacturers are expanding R&D spending, developing cloud-connected monitoring ecosystems, and building regional partnerships to secure long-term infrastructure automation contracts and strengthen competitive differentiation.

Long-term scalability within the Robot Spraying Concrete System Market is increasingly constrained by integration complexity, workforce training gaps, and inconsistent operational standardization across infrastructure projects. Nearly 29% of contractors deploying robotic spraying technologies report implementation delays linked to inadequate operator training and digital integration challenges. Variability in tunnel geometries, environmental conditions, and concrete material composition also affects spraying consistency, increasing recalibration requirements by approximately 17% during complex underground operations. Rising pressure to comply with stricter infrastructure safety regulations and environmental standards is simultaneously increasing equipment certification costs and deployment timelines. These operational barriers threaten long-term execution consistency, particularly for contractors transitioning from conventional spraying systems. To remain competitive, companies must strengthen technical training ecosystems, invest in adaptive automation technologies, and establish strategic engineering partnerships capable of supporting scalable, multi-project robotic deployment models.

32% Increase in AI-Guided Spraying Deployment Across Tunnel Projects Infrastructure contractors are rapidly integrating AI-assisted nozzle positioning and sensor-based thickness monitoring into robotic spraying systems. Automated calibration deployment increased by 32% during 2025, while spraying precision improved by nearly 26%. Companies are restructuring equipment portfolios toward digitally connected systems to reduce rework cycles and optimize underground project execution speed.

27% Reduction in Material Waste Reshaping Operational Priorities Advanced robotic spraying systems are significantly reducing rebound concrete waste and overspray losses across mining and transportation infrastructure projects. Material optimization rates improved by 27%, while labor-intensive correction work declined by 21%. Rising cement cost volatility and tighter ESG compliance requirements are forcing contractors to prioritize high-efficiency spraying technologies with real-time monitoring capabilities.

41% Growth in Asia-Pacific Infrastructure Automation Deployment Asia-Pacific is witnessing accelerated deployment of robotic concrete spraying systems due to high-speed railway, metro tunnel, and mining expansion projects. Localized equipment production increased by 24%, reducing procurement lead times and improving regional project scalability. Manufacturers are expanding strategic partnerships with domestic construction firms to capture fast-moving infrastructure demand and strengthen execution capacity.

35% Shift Toward Service-Based Robotic Equipment Models Construction equipment providers are increasingly offering leasing, remote diagnostics, and predictive maintenance services instead of traditional one-time equipment sales. Subscription-based support contracts expanded by 35% during 2025 as contractors sought lower upfront costs and faster deployment flexibility. This operational shift is redefining procurement strategies and strengthening long-term supplier-client integration across infrastructure automation ecosystems.

The Robot Spraying Concrete System Market is segmented by type, application, and end-user, with demand increasingly concentrated around high-efficiency underground infrastructure and mining automation projects. Automated and semi-automated systems collectively account for over 68% of deployment volume due to rising pressure for operational precision and labor optimization. Tunnel construction and mining applications dominate global demand, together contributing nearly 61% of system utilization as infrastructure modernization accelerates across Asia-Pacific and Europe. Demand is steadily shifting toward AI-enabled spraying systems capable of improving material efficiency and reducing rebound losses by over 20%. Large infrastructure contractors remain the primary buyers, although mining operators and industrial engineering firms are rapidly increasing procurement activity to strengthen operational safety and project scalability. Companies are responding through product specialization, regional manufacturing expansion, and digitally integrated spraying technologies targeting execution efficiency and long-term infrastructure automation.

Automated robotic spraying systems dominate the Robot Spraying Concrete System Market with approximately 46% share due to superior spraying precision, lower labor dependency, and scalable integration across large underground infrastructure projects. These systems improve application consistency by nearly 30% while reducing material wastage by over 22%, making them highly preferred in tunnel construction and mining operations. Semi-automated systems represent the fastest-growing segment, expanding deployment adoption by approximately 18% as mid-sized contractors seek lower-cost automation alternatives without fully replacing manual operational control. Compared to fully automated systems, semi-automated solutions offer lower upfront implementation complexity while still improving operational productivity significantly. Manual-assisted robotic systems and compact mobile spraying units collectively account for nearly 28% share, maintaining niche relevance in small-scale infrastructure repair and regional mining operations where deployment flexibility remains critical. Demand is clearly shifting toward intelligent automation platforms integrated with AI-guided nozzle control and sensor-driven monitoring systems. Manufacturers are accelerating modular product development, localized assembly expansion, and predictive maintenance integration to strengthen scalability and capture high-volume infrastructure contracts globally. Strategic investment is increasingly concentrating on automation-focused platforms with long-term operational efficiency advantages.

Tunnel construction remains the leading application segment within the Robot Spraying Concrete System Market, accounting for nearly 38% of total deployment demand due to massive global investments in railway, metro, and underground transportation infrastructure. High-volume tunnel projects increasingly require robotic spraying systems capable of reducing execution time by over 30% while maintaining consistent structural coating precision under complex underground conditions. Mining operations represent the fastest-growing application segment, with deployment activity increasing by approximately 21% as mining companies accelerate automation strategies to improve workforce safety and operational continuity. Compared to mature tunnel infrastructure applications, mining environments demand more rugged and adaptive robotic spraying technologies capable of operating under extreme environmental conditions. Infrastructure rehabilitation, slope stabilization, and industrial concrete reinforcement applications collectively contribute nearly 34% market share, maintaining strategic importance in aging urban infrastructure modernization programs. Companies are repositioning deployment strategies toward AI-enabled monitoring systems, mobile robotic units, and integrated spraying analytics to optimize project execution efficiency. Demand is rapidly shifting toward high-productivity automation platforms that improve structural durability while lowering long-term operational costs.

Large infrastructure contractors dominate the Robot Spraying Concrete System Market with nearly 43% demand share due to their extensive involvement in tunnel construction, railway modernization, and urban transit expansion projects. These organizations prioritize automated spraying systems to improve execution consistency, reduce workforce dependency, and strengthen compliance with evolving safety regulations. Mining companies represent the fastest-growing end-user group, with robotic spraying system adoption increasing by approximately 24% as underground mining operations intensify automation investment to reduce hazardous labor exposure and improve operational continuity. Compared to traditional construction contractors, mining operators show stronger preference for ruggedized, sensor-integrated systems optimized for continuous deployment in harsh operating environments. Government infrastructure agencies, industrial engineering firms, and specialized underground construction service providers collectively account for nearly 36% market share, supported by rising public infrastructure investment and rehabilitation activity. Buying behavior is increasingly shifting toward long-term service agreements, predictive maintenance integration, and modular automation platforms. Manufacturers are targeting these end-users through customized deployment models, financing partnerships, and region-specific automation solutions designed to improve operational scalability and long-term infrastructure performance.

Asia-Pacific accounted for the largest market share at 41% in 2025 however, Europe is expected to register the fastest growth, expanding at a CAGR of 7.8% between 2026 and 2033.

Asia-Pacific dominates global demand due to aggressive railway tunnel construction, mining automation programs, and rapid urban infrastructure expansion across China, India, and Southeast Asia. North America holds approximately 27% share, supported by underground mining modernization and advanced construction automation adoption, while Europe contributes nearly 24% through safety-driven infrastructure upgrades and ESG-focused construction practices. Latin America and the Middle East & Africa collectively account for 8% share, driven by selective mining and transportation infrastructure projects. Rising localization of robotic equipment manufacturing and global supply chain diversification are reshaping regional procurement strategies. Companies are increasingly prioritizing Asia-Pacific for scale, Europe for innovation-led compliance, and North America for advanced automation deployment.

North America accounts for nearly 27% of the global Robot Spraying Concrete System Market, driven by expanding underground mining automation, transportation tunnel rehabilitation, and labor optimization initiatives. The United States and Canada are accelerating adoption of AI-assisted spraying systems to address rising workforce shortages and improve operational safety compliance. More than 44% of large underground infrastructure contractors in the region now prioritize automated shotcrete systems with digital monitoring capabilities. Stricter workplace safety standards and rising infrastructure modernization spending are reshaping procurement strategies across mining and transit sectors. Manufacturers expanded regional service and maintenance capacity by approximately 18% during 2025 to support faster deployment cycles. Enterprise buyers increasingly favor predictive maintenance integration and modular robotic systems, strengthening North America’s position as a strategic market for advanced infrastructure automation investment.

Europe represents approximately 24% of the global Robot Spraying Concrete System Market, led by Germany, Switzerland, and the Nordic countries where underground infrastructure modernization and worker safety compliance remain strategic priorities. Tightening ESG regulations and carbon reduction mandates are accelerating adoption of robotic spraying systems capable of reducing concrete wastage by over 20%. Automated thickness monitoring and AI-guided spraying technologies are increasingly replacing manual operations across tunnel rehabilitation and railway expansion projects. More than 39% of newly approved underground infrastructure programs in Western Europe now integrate automated spraying requirements. Construction firms are prioritizing digitally controlled spraying systems to strengthen compliance efficiency and long-term operational sustainability. This regulatory-driven transformation is forcing manufacturers to accelerate product innovation, precision engineering, and eco-efficient deployment strategies across the European infrastructure ecosystem.

Asia-Pacific dominates the Robot Spraying Concrete System Market with approximately 41% global share, supported by aggressive infrastructure expansion across China, India, Japan, and Southeast Asia. China alone contributes nearly 31% of global deployment demand due to high-speed railway tunnels, metro expansion, and mining automation initiatives. Regional manufacturers increased localized robotic equipment production by approximately 26% during 2025, significantly improving supply chain responsiveness and reducing deployment lead times. Infrastructure contractors increasingly prioritize high-speed automated spraying systems capable of improving project productivity by over 30%. Large-scale government-backed transportation investments and rapid urbanization continue accelerating adoption of advanced construction automation technologies. Enterprise buyers across the region strongly favor scalable, cost-efficient robotic systems optimized for mass infrastructure execution, positioning Asia-Pacific as the primary global expansion hub for robotic spraying equipment manufacturers.

South America accounts for nearly 5% of the global Robot Spraying Concrete System Market, with Brazil and Chile leading regional demand due to mining infrastructure modernization and transportation tunnel development projects. Underground mining operations are increasingly adopting robotic spraying technologies to improve workforce safety and operational continuity, particularly across copper and lithium extraction projects. However, equipment import dependency and fluctuating infrastructure investment cycles continue constraining broader regional deployment scalability. More than 22% of regional mining contractors expanded automation investment during 2025 despite ongoing capital expenditure pressure. Buyers remain highly price-sensitive, favoring modular and semi-automated systems that balance operational efficiency with lower upfront costs. This combination of rising automation demand and structural economic constraints positions South America as both a strategic expansion opportunity and a selective execution-risk market.

The Middle East & Africa region contributes approximately 3% of the global Robot Spraying Concrete System Market, driven by large-scale transportation, mining, and smart city infrastructure projects across the UAE, Saudi Arabia, and South Africa. Government-backed infrastructure modernization programs and underground transit expansion are accelerating demand for automated spraying technologies capable of improving execution speed and worker safety. Deployment of robotic shotcrete systems across major regional infrastructure projects increased by nearly 19% during 2025. Construction firms are increasingly partnering with global equipment manufacturers to strengthen technical expertise and deployment efficiency. Enterprise buyers prioritize durable, high-productivity systems suited for large-scale infrastructure environments and harsh operational conditions. The region is steadily emerging as a strategic long-term infrastructure automation market supported by investment-driven modernization and industrial diversification initiatives.

China – 31% Market share: dominates due to massive tunnel infrastructure expansion, high-speed railway construction, and strong domestic robotic equipment manufacturing capacity.

United States – 19% Market share: leads advanced robotic spraying adoption through mining automation, underground infrastructure rehabilitation, and rapid integration of AI-enabled construction technologies.

The Robot Spraying Concrete System Market is dominated by global automation leaders such as Putzmeister, Normet, Epiroc, Sika, and CIFA, competing aggressively against regional underground equipment manufacturers and low-cost Asian system integrators. The top five players collectively control nearly 58% of the global market, with competition intensifying between premium automation-focused OEMs and cost-optimized regional suppliers targeting mid-scale infrastructure projects.

Competition is increasingly defined by spraying precision, automation capability, digital diagnostics, and deployment speed rather than pricing alone. AI-assisted robotic spraying systems improve operational consistency by nearly 30%, while advanced low-pulsation pumping technologies reduce material rebound losses by over 22%. Leading manufacturers are expanding through regional assembly facilities, mining partnerships, and integrated service ecosystems to secure long-term infrastructure contracts.

The competitive landscape is rapidly shifting toward intelligent automation platforms and vertically integrated underground construction solutions. Companies with proprietary control software, predictive maintenance systems, and localized support infrastructure are strengthening market control. High capital requirements, certification complexity, and specialized engineering expertise remain major entry barriers. Winning in this market increasingly requires scalable automation technology, regional execution capability, and continuous innovation aligned with infrastructure modernization demand.

Normet

Epiroc

Sika AG

CIFA S.p.A.

Zoomlion Heavy Industry Science & Technology Co., Ltd.

XCMG Group

SANY Heavy Industry Co., Ltd.

MacLean Engineering

Junjin Heavy Industry Co., Ltd.

REED Concrete Pumps & Shotcrete Equipment

Thiessen Team

Aliva Equipment

GHH Fahrzeuge GmbH

The Robot Spraying Concrete System Market is rapidly transitioning from hydraulically controlled spraying equipment toward AI-enabled, sensor-integrated automation platforms optimized for underground infrastructure execution. Automated nozzle positioning systems combined with LiDAR-based tunnel mapping now improve spraying precision by nearly 28% while reducing overspray losses by over 20%. More than 46% of newly deployed robotic spraying systems during 2025 integrated digital diagnostics and remote monitoring capabilities, reflecting the market’s accelerating shift toward intelligent construction automation.

Advanced low-pulsation pumping technology and closed-loop accelerator dosing systems are redefining operational efficiency across mining and tunnel construction projects. Compared to conventional manual spraying operations, modern robotic shotcrete systems reduce labor dependency by approximately 31% while improving coating consistency by over 30%. Premium OEMs and large infrastructure contractors benefit most from these technologies due to their ability to scale automation across high-volume underground projects while lowering long-term maintenance costs.

Emerging technologies between 2026 and 2028 include autonomous spraying path optimization, digital twin-enabled structural monitoring, and predictive maintenance ecosystems connected through cloud-based construction platforms. Remote-controlled spraying systems equipped with AI-assisted calibration are expected to accelerate deployment adoption across hazardous underground environments where workforce exposure reduction is becoming operationally critical. Companies investing early in intelligent automation integration, modular robotic architectures, and real-time performance analytics are strengthening long-term competitive positioning as infrastructure execution standards continue transforming globally.

March 2025 – Normet launched the Spraymec 4100 and Spraymec 5100 robotic concrete sprayers featuring synchronized dosing systems and vertical spray reach up to 14 meters, significantly improving underground spraying precision and productivity for tunnel projects. The launch strengthened Normet’s high-performance tunnelling portfolio expansion strategy. [Tunnel Automation Push] Source: www.normet.com

May 2025 – Normet unveiled the Spraymec 9100 at the World Tunnelling Congress with a 19.5-meter vertical spraying reach and 28-meter spraying width, targeting large-scale tunnel and cavern projects. The system enhanced high-output underground spraying capability and reinforced Normet’s leadership in advanced infrastructure automation. [Large Tunnel Expansion]

December 2024 – Normet introduced a new underground equipment range for India’s rapidly expanding infrastructure market, accelerating localization and deployment flexibility. The initiative strengthened regional manufacturing responsiveness and aligned with rising automated tunnelling and mining equipment demand across South Asia. [India Localization Drive]

September 2025 – Putzmeister Underground introduced the Wetkret 2 Narrow Vein robotic shotcrete system designed for mining sections as small as 2.5 × 2.5 meters, significantly improving operator safety and deployment flexibility in confined underground environments. The innovation expanded robotic shotcrete applicability across narrow-vein mining operations. [Compact Mining Innovation]

The Robot Spraying Concrete System Market Report provides comprehensive analysis across automated, semi-automated, and specialized robotic spraying system types used in tunnel construction, mining operations, infrastructure rehabilitation, and industrial underground applications. The report evaluates demand patterns across major end-user groups including infrastructure contractors, mining operators, engineering firms, and government transportation agencies. Geographic coverage spans North America, Europe, Asia-Pacific, South America, and the Middle East & Africa, with detailed assessment of regional deployment trends, infrastructure investments, and automation adoption shifts. The study also examines emerging technologies such as AI-guided spraying systems, LiDAR-enabled tunnel mapping, predictive maintenance integration, and sensor-based thickness monitoring platforms.

The report delivers deep strategic intelligence through analysis of over 10 major market participants, multiple application categories, and evolving procurement behaviors shaping infrastructure automation demand. More than 46% of recent underground infrastructure projects now integrate automated spraying technologies, while AI-assisted systems improve operational precision by nearly 28%. The study further evaluates niche growth areas including compact robotic systems for confined mining environments and digitally connected underground construction ecosystems. Forward-looking coverage between 2026 and 2033 highlights execution-level technology transformation, regional manufacturing localization, sustainability-driven equipment adoption, and competitive positioning strategies critical for investment planning, capacity expansion, partnership decisions, and long-term infrastructure automation leadership.

| Report Attribute / Metric | Details |

|---|---|

| Market Revenue (2025) | USD 200.8 Million |

| Market Revenue (2033) | USD 350.2 Million |

| CAGR (2026–2033) | 7.2% |

| Base Year | 2025 |

| Forecast Period | 2026–2033 |

| Historic Period | 2021–2025 |

| Segments Covered |

By Type

By Application

By End-User Insights

|

| Key Report Deliverables | Revenue Forecast; Market Trends; Growth Drivers & Restraints; Technology Insights; Segmentation Analysis; Regional Insights; Competitive Landscape; Regulatory & ESG Overview; Recent Developments |

| Regions Covered | North America; Europe; Asia-Pacific; South America; Middle East & Africa |

| Key Players Analyzed | Putzmeister; Normet; Epiroc; Sika AG; CIFA S.p.A.; Zoomlion Heavy Industry Science & Technology Co., Ltd.; XCMG Group; SANY Heavy Industry Co., Ltd.; MacLean Engineering; Junjin Heavy Industry Co., Ltd.; REED Concrete Pumps & Shotcrete Equipment; Thiessen Team; Aliva Equipment; GHH Fahrzeuge GmbH |

| Customization & Pricing | Available on Request (10% Customization Free) |