Reports

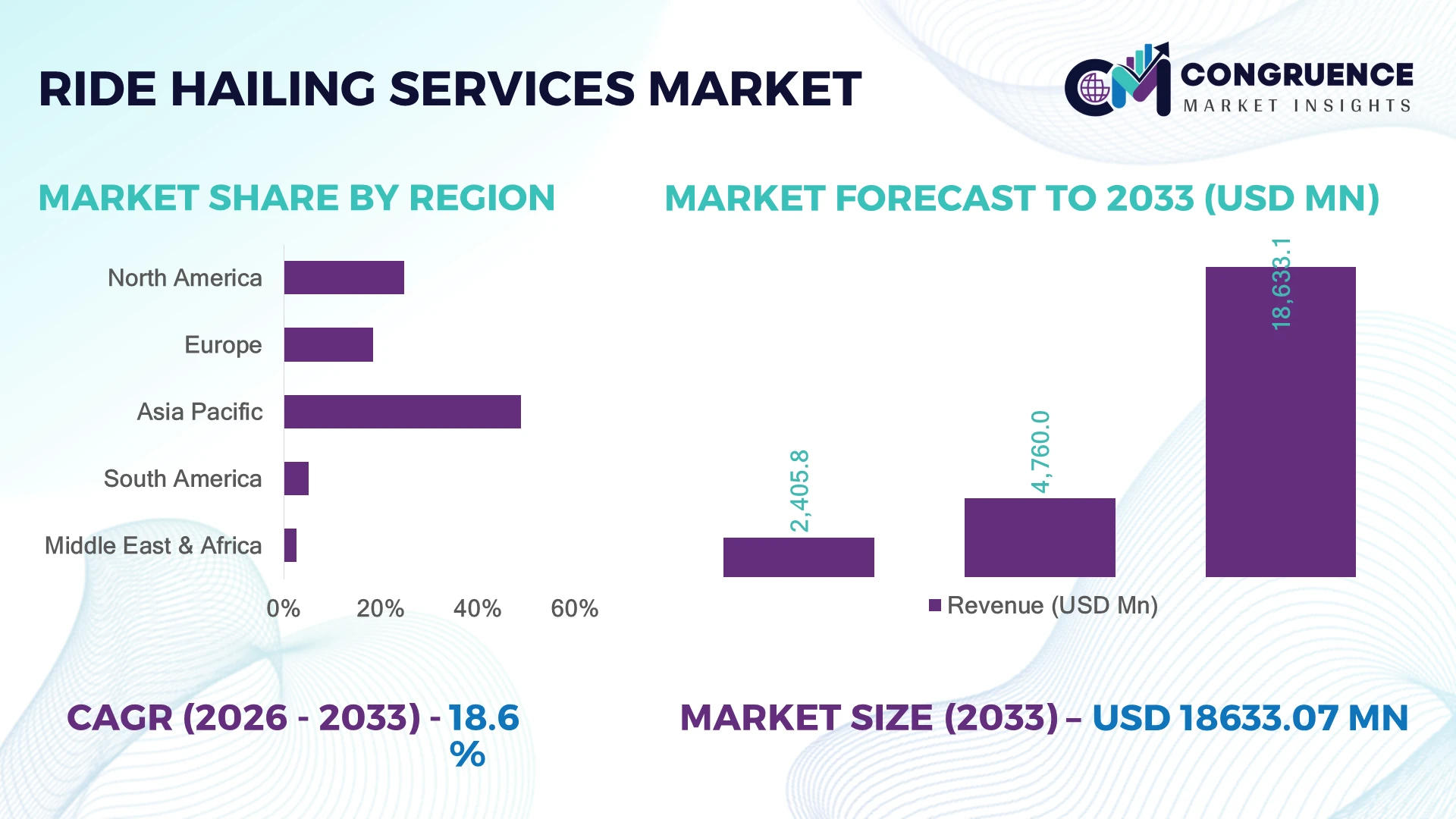

The Global Ride Hailing Services Market was valued at USD 4,760.0 Million in 2025 and is anticipated to reach a value of USD 18,633.1 Million by 2033 expanding at a CAGR of 18.6% between 2026 and 2033. Growth is being accelerated by AI-powered dispatch optimization, expanding electric mobility fleets, digital payment integration, and government-backed urban mobility initiatives that improve fleet utilization and passenger convenience.

China remains the dominant country, accounting for approximately 41% of global ride hailing activity, supported by over 500 major cities with app-based mobility services, rapid EV fleet deployment, and strong digital payment penetration. Compared with the United States, China processes substantially higher daily ride volumes due to dense urban populations and smart-city investments, while national transport digitalization policies continue strengthening operational efficiency and platform scalability.

As urban mobility ecosystems evolve, companies prioritizing intelligent fleet management, localized partnerships, and regulatory compliance will secure stronger competitive positioning across high-growth metropolitan markets.

Market Size & Growth: USD 4,760.0 Million (2025) to USD 18,633.1 Million (2033) at 18.6% CAGR, driven by AI-based fleet optimization and expanding digital mobility ecosystems.

Top Growth Drivers: EV fleet adoption (+32%), digital payment penetration (+28%), and AI route optimization (+24%) continue reshaping global operations.

Short-Term Forecast: By 2028, average passenger wait times decline by nearly 18% while fleet utilization improves by over 20% through intelligent dispatching.

Emerging Technologies: AI dispatch engines, predictive demand analytics, autonomous mobility pilots, and connected vehicle platforms enhance operational efficiency.

Regional Leaders: Asia Pacific (~USD 8.2 Billion), North America (~USD 4.6 Billion), and Europe (~USD 3.4 Billion) benefit from smart-city investments and regional mobility expansion.

Consumer/End-User Trends: More than 65% of urban riders prefer app-based transportation integrated with digital wallets and real-time ride tracking.

Pilot/Case Example: In 2024, AI-powered routing deployments reduced idle driving by approximately 15% while improving driver allocation efficiency across major metropolitan networks.

Competitive Landscape: Uber leads with roughly 26% global market share alongside Lyft, Didi Global, Grab, and Bolt amid regional platform expansion.

Regulatory & ESG Impact: Zero-emission fleet mandates support over 30% EV integration targets while urban transport policies accelerate cleaner mobility networks.

Investment & Funding: More than USD 8 Billion in strategic investments supports platform expansion, AI capabilities, EV partnerships, and autonomous mobility development.

Innovation & Future Outlook: Super-app integration, autonomous ride services, multimodal transportation, and advanced analytics strengthen long-term competitive differentiation across global markets.

Ride Hailing Services Market demand continues expanding across urban commuting, airport transfers, corporate mobility, and last-mile transportation as operators enhance platform intelligence and service personalization. AI-enabled pricing engines, electric vehicle integration, and predictive demand forecasting are improving fleet efficiency, while EV-based ride volumes have surpassed 25% in several leading cities. Regulatory support for sustainable transportation and expanding charging infrastructure are reinforcing long-term operational transformation across major metropolitan networks.

Ride hailing services have become a strategic pillar of modern urban transportation as cities prioritize digital mobility, congestion management, and low-emission travel. Platform operators are strengthening competitive positions through AI-driven dispatch systems, integrated payment ecosystems, and partnerships with electric vehicle manufacturers. Simultaneously, evolving transport regulations and investments in smart-city infrastructure are accelerating the transition toward more connected and efficient mobility networks.

Compared with conventional taxi dispatch systems, AI-enabled ride matching reduces passenger wait times by approximately 20% while lowering fleet idle time by nearly 15%, delivering measurable operational efficiency. Asia Pacific leads global deployment through dense urban populations and extensive mobile payment adoption, whereas North America emphasizes premium mobility services, autonomous vehicle pilots, and enterprise transportation solutions. Over the next two to three years, connected fleet management platforms and EV integration are expected to significantly increase digitally managed ride volumes across leading metropolitan markets.

Companies are expanding through strategic fleet electrification programs, regional partnerships, and investments in predictive analytics that improve driver allocation and customer experience. For example, several operators now combine AI-based demand forecasting with dynamic pricing to optimize fleet deployment during peak travel periods while reducing unnecessary vehicle movement. Organizations that align technology investment, regulatory compliance, and sustainable mobility strategies will establish stronger competitive differentiation and long-term operational resilience in the evolving global transportation ecosystem.

Artificial intelligence is fundamentally improving ride hailing efficiency through real-time demand forecasting, dynamic pricing, and intelligent driver allocation. AI-enabled dispatch platforms have reduced average passenger wait times by nearly 20%, while predictive routing lowers idle driving by approximately 15% and improves fleet utilization by over 22%. China continues accelerating digital mobility through smart-city investments and expanding EV charging infrastructure, encouraging platform operators to transition toward electric fleets. This structural shift reduces operating costs while supporting urban emission targets. Leading companies are investing in AI-powered mobility platforms, expanding EV partnerships, and integrating connected vehicle analytics to strengthen driver productivity, enhance customer experience, and create scalable urban transportation ecosystems with higher operational resilience.

Evolving labor regulations and increasing compliance requirements continue challenging platform profitability and operational flexibility. In several developed markets, labor-related expenses account for over 35% of operating costs, while mandatory driver benefits can increase platform expenditure by approximately 15%. The United Kingdom and parts of Europe have introduced stricter worker classification frameworks that require additional employment protections, creating operational complexity for mobility platforms. These regulatory changes directly affect pricing strategies, fleet scalability, and service availability. Companies are responding through localized operating models, diversified driver engagement programs, long-term insurance partnerships, and greater investment in automated compliance management systems that reduce administrative overhead while maintaining regulatory alignment across multiple jurisdictions.

Autonomous driving technologies and integrated mobility ecosystems are opening new strategic opportunities beyond traditional ride hailing services. Connected mobility platforms combining ride sharing, micro-mobility, and public transport integration can improve urban transportation efficiency by nearly 25%, while AI-enabled demand prediction increases fleet productivity by approximately 18%. The United States continues expanding autonomous vehicle pilot programs supported by advanced mapping and connected infrastructure initiatives. Companies are strengthening innovation through strategic R&D investments, autonomous technology partnerships, and digital ecosystem expansion that connects payment platforms, charging infrastructure, and mobility services. An emerging opportunity lies in subscription-based urban mobility packages that increase customer retention while diversifying recurring revenue streams and reducing dependence on single-trip demand.

Maintaining consistent service quality across expanding digital mobility ecosystems remains a major long-term execution challenge. Cybersecurity incidents targeting transportation platforms have increased by nearly 30%, while real-time data processing requirements continue growing alongside millions of daily ride requests. Large metropolitan areas in India face infrastructure disparities that affect GPS precision, traffic prediction, and driver routing efficiency during peak demand periods. These operational constraints influence customer satisfaction, deployment consistency, and platform competitiveness. Companies must strengthen cloud infrastructure, cybersecurity frameworks, and edge-based analytics while investing in high-availability digital architecture, intelligent mapping technologies, and resilient telecommunications partnerships to sustain secure, scalable, and uninterrupted mobility operations across increasingly complex transportation networks.

AI-Powered Dispatch Optimization: Ride hailing operators are rapidly deploying AI-driven dispatch engines that improve driver-passenger matching and reduce average wait times by nearly 20%, while predictive routing lowers idle mileage by approximately 15%. Increased smartphone penetration and expanding cloud-based fleet management platforms are streamlining real-time operations. Companies are scaling machine learning capabilities, automating demand forecasting, and integrating dynamic pricing engines to improve fleet productivity and customer retention across densely populated urban corridors.

Electric Fleet Transformation: Electric vehicles are becoming integral to ride hailing operations as government emission regulations and lower operating costs reshape fleet strategies. EV participation within ride hailing fleets has exceeded 25% in several leading cities, while maintenance expenses decline by nearly 30% compared with conventional vehicles. Companies are expanding charging partnerships, introducing dedicated EV financing programs for drivers, and restructuring fleet procurement to accelerate low-emission mobility while reducing long-term operating expenditures.

Super-App Mobility Integration: Ride hailing platforms are evolving into comprehensive mobility ecosystems by integrating ride booking, food delivery, digital payments, and micro-mobility services. Cross-platform customer engagement has increased by approximately 35%, while bundled mobility subscriptions improve repeat usage by nearly 18%. Growing consumer preference for unified digital services is encouraging operators to strengthen strategic partnerships, consolidate platform capabilities, and deploy integrated customer loyalty programs that improve lifetime user value and operational efficiency.

Enterprise Mobility Expansion: Corporate transportation is becoming an increasingly important operational segment as businesses prioritize employee mobility, travel visibility, and automated expense management. Enterprise ride bookings have grown by over 22%, while digital fleet reporting reduces administrative processing time by nearly 30%. Hybrid work models and stricter travel compliance requirements are encouraging companies to deploy centralized mobility management platforms, expand business partnerships, and introduce customized transportation solutions that improve workforce mobility and operational transparency.

The market is segmented into E-Hailing, Car Sharing, Car Rental, and Station-Based Mobility Services. E-Hailing remains the leading segment, accounting for approximately 62% of total market demand owing to instant booking convenience, GPS-enabled route optimization, and extensive smartphone adoption. The segment benefits from scalable cloud infrastructure, integrated digital payments, and AI-powered dispatch systems that maximize fleet utilization. Major operators continue expanding platform capabilities through subscription programs, driver incentive models, and intelligent pricing algorithms. Meanwhile, Car Sharing is emerging as the fastest-growing segment, supported by increasing urban congestion, sustainability initiatives, and changing vehicle ownership preferences. Car Rental maintains strong relevance for long-distance and business travel, while Station-Based Mobility Services continue serving regulated transportation hubs and multimodal transit integration. Companies are diversifying mobility portfolios through strategic acquisitions, EV deployment, and connected fleet technologies. Around 35% of newly launched mobility platforms now integrate multiple transportation modes within a single application, reflecting shifting investment priorities toward comprehensive urban mobility ecosystems.

The market is segmented into Daily Commuting, Airport Transportation, Outstation Travel, and Corporate Transportation. Daily Commuting represents the dominant application, contributing nearly 58% of ride demand due to increasing urbanization, rising smartphone usage, and growing reliance on app-based transportation. Frequent travel patterns enable operators to optimize dynamic pricing and maximize vehicle utilization throughout peak demand periods. Corporate Transportation is the fastest-growing application as organizations increasingly digitize employee travel management and integrate automated billing, compliance monitoring, and centralized booking platforms. Airport Transportation remains strategically important due to premium ride demand and predictable passenger flows, while Outstation Travel continues expanding through intercity mobility offerings and scheduled ride services. Companies are strengthening these segments through AI-based scheduling, corporate partnerships, and integrated travel management solutions. Approximately 28% of enterprise customers now prefer centralized digital mobility platforms that simplify transportation administration while improving travel visibility and operational efficiency.

The market is segmented into Individual Consumers, Corporate Enterprises, Government Organizations, and Tourism & Hospitality. Individual Consumers remain the largest end-user group with nearly 68% of platform usage, supported by increasing digital payment adoption, mobile application penetration, and demand for convenient urban transportation. Operators continue enhancing customer retention through loyalty programs, subscription offerings, and AI-driven personalization. Corporate Enterprises represent the fastest-growing end-user segment as businesses standardize employee mobility, automate travel expense management, and improve transportation visibility across distributed workforces. Tourism & Hospitality continues expanding through partnerships with hotels, airports, and travel platforms that provide seamless mobility experiences for domestic and international travelers. Government Organizations are increasingly adopting regulated ride services for official transportation and smart-city mobility initiatives. More than 40% of leading ride hailing companies are introducing enterprise-focused mobility solutions that combine analytics, compliance management, and centralized billing to strengthen long-term commercial relationships and competitive differentiation.

Asia-Pacific accounted for the largest market share at 48.9% in 2025 however, Middle East & Africa is expected to register the fastest growth, expanding at a CAGR of 21.4% between 2026 and 2033.

North America accounted for approximately 24.8% of the global Ride Hailing Services Market in 2025, supported by mature digital infrastructure, high smartphone penetration, and extensive app-based mobility adoption. Enterprise transportation, airport mobility, and subscription-based ride services continue expanding as businesses digitize workforce travel management. More than 70% of ride bookings are completed through integrated digital payment platforms, while AI-powered dispatch systems improve fleet utilization and reduce passenger wait times. Platform operators are strengthening partnerships with EV manufacturers, charging providers, and autonomous technology companies to improve operational efficiency. Continued investment in intelligent transportation systems and connected mobility ecosystems reinforces the region's leadership in premium urban mobility services.

United States Market Outlook: The United States remains the largest contributor to regional demand through extensive urban transportation networks, strong technology innovation, and widespread enterprise mobility adoption. Cities including New York, Los Angeles, Chicago, and San Francisco continue expanding digital transportation ecosystems supported by AI-driven fleet management and connected vehicle technologies. More than 75% of urban consumers regularly use app-based transportation services, while leading mobility providers continue investing in autonomous vehicle testing, EV fleet expansion, and integrated multimodal transportation platforms to strengthen long-term operational competitiveness.

Europe represented nearly 18.5% of global market activity in 2025, driven by strong sustainability policies, widespread electric mobility adoption, and increasingly digital public transportation ecosystems. Urban congestion policies and low-emission zones are encouraging operators to deploy electric vehicles and optimize ride-sharing utilization. Approximately 32% of newly registered ride hailing vehicles in major European cities are fully electric, improving fleet sustainability while reducing operating expenses. Platform providers continue expanding mobility partnerships with municipalities, charging infrastructure operators, and public transit agencies to deliver integrated transportation services across metropolitan markets.

United Kingdom Market Outlook: The United Kingdom leads regional platform innovation through advanced digital payment adoption, regulatory modernization, and high urban mobility demand. London remains one of Europe's largest ride hailing markets, supported by intelligent traffic management systems and extensive multimodal transportation integration. Fleet operators continue investing in electric vehicle adoption and digital compliance platforms, while enterprise transportation demand continues expanding through corporate mobility agreements and automated travel management solutions that improve operational transparency.

Asia-Pacific remains the largest regional market, accounting for approximately 48.9% of global demand due to rapid urbanization, expanding middle-class populations, and exceptional smartphone penetration. High-density metropolitan areas generate significant ride volumes supported by digital payment ecosystems and advanced AI-based dispatch technologies. More than 60% of ride bookings across leading metropolitan markets are completed through integrated super-app ecosystems combining transportation, payments, and digital commerce. Platform operators continue investing heavily in electric vehicle deployment, cloud-based fleet management, and predictive demand analytics to maximize operating efficiency and customer retention.

China Market Outlook: China dominates the regional market through unmatched urban mobility demand, smart-city development, and extensive digital infrastructure. Hundreds of cities operate large-scale ride hailing ecosystems supported by high mobile payment penetration and expanding EV charging networks. More than 40% of active ride hailing vehicles in several major metropolitan areas are electrified, while technology companies continue integrating AI-powered dispatch, autonomous mobility pilots, and intelligent transportation platforms to strengthen nationwide operational scalability.

South America contributes approximately 5.2% of global market demand, supported by rising smartphone adoption, increasing digital financial inclusion, and expanding urban transportation requirements. Ride hailing adoption continues increasing across major metropolitan centers where public transport capacity remains constrained during peak travel periods. Digital payment transactions have increased by nearly 30%, enabling broader customer participation and reducing cash dependency. Platform providers are strengthening regional operations through localized pricing strategies, driver incentive programs, and partnerships with financial technology providers that improve accessibility while addressing infrastructure limitations.

Brazil Market Outlook: Brazil represents the largest ride hailing market in South America due to its large urban population, expanding digital economy, and extensive metropolitan transportation demand. São Paulo and Rio de Janeiro continue serving as major deployment hubs supported by high smartphone usage and increasing adoption of cashless payment platforms. Mobility providers are investing in fleet expansion, AI-driven routing technologies, and integrated financial services that enhance driver earnings while improving customer convenience across densely populated urban centers.

The Middle East & Africa accounts for approximately 2.6% of global market activity but demonstrates the strongest long-term expansion potential through rapid smart-city development and transportation modernization initiatives. Governments continue investing in intelligent mobility infrastructure, digital payment ecosystems, and connected transportation platforms. Ride hailing penetration has increased by nearly 25% across several major metropolitan areas, supported by expanding internet connectivity and favorable digital transformation policies. Companies are entering strategic partnerships with local mobility providers, infrastructure developers, and electric vehicle ecosystem participants to strengthen long-term market positioning.

United Arab Emirates Market Outlook: The United Arab Emirates leads regional innovation through advanced digital infrastructure, supportive mobility regulations, and ambitious smart-city initiatives. Dubai continues deploying integrated transportation platforms that combine ride hailing, autonomous mobility trials, and intelligent traffic management systems. More than 90% of residents have access to high-speed mobile connectivity, enabling seamless app-based transportation adoption. Operators continue expanding premium mobility offerings, EV fleet deployment, and strategic technology collaborations that reinforce the country's position as a regional hub for next-generation urban transportation.

Competition is led by Uber Technologies, DiDi Global, Lyft, Grab Holdings, and Bolt, while regional platforms such as Ola and Rapido challenge global operators through localized pricing and stronger driver networks. The top five players collectively control approximately 68% of the global market, creating a concentrated but innovation-driven landscape. Global leaders compete on AI-powered dispatch, multimodal ecosystems, and autonomous mobility, whereas regional players emphasize affordability, regulatory alignment, and market-specific customization. Dynamic pricing algorithms improve fleet utilization by nearly 20%, AI-based route optimization reduces idle mileage by approximately 15%, and digital payment integration exceeds 80% across mature markets. Companies are expanding through EV partnerships, autonomous vehicle collaborations, super-app integration, and strategic acquisitions rather than price competition alone. The competitive shift is increasingly driven by autonomous mobility and platform ecosystems instead of conventional ride aggregation. High regulatory compliance costs, network-scale requirements, and driver acquisition remain significant entry barriers. Winning requires superior technology, localized execution, scalable operations, and trusted mobility ecosystems.

Lyft Inc.

Grab Holdings Limited

DiDi Global Inc.

Bolt Technology OÜ

Ola Consumer

Rapido

Gojek

Cabify

Yandex Go

inDrive

FREE NOW

Careem

Artificial intelligence has become the core operating technology across ride hailing platforms. AI-powered dispatch engines, predictive demand forecasting, and dynamic pricing continuously optimize driver allocation while reducing passenger waiting times by nearly 20%. More than 70% of leading platforms now utilize cloud-native analytics and machine learning for real-time marketplace balancing. Connected telematics further improve fleet visibility, enabling operators to lower idle mileage and increase vehicle productivity through automated decision-making.

Emerging technologies are reshaping competitive differentiation. Autonomous driving systems, computer vision, high-definition mapping, and edge computing are moving from pilot deployments toward commercial integration. Compared with traditional rule-based dispatch systems, AI-enabled optimization improves fleet efficiency by approximately 18% while reducing operational costs by nearly 12%. Companies investing in autonomous mobility, digital twins, and intelligent fleet orchestration gain measurable advantages through faster matching, improved customer experience, and better asset utilization. Large technology-driven operators benefit most because existing platform scale accelerates algorithm performance and deployment efficiency.

Between 2026 and 2028, robotaxi integration, vehicle-to-everything communication, generative AI customer support, and predictive maintenance platforms are expected to expand rapidly across major metropolitan markets. Increasing adoption of multimodal mobility ecosystems and intelligent charging management for electric fleets will strengthen operational resilience, enabling leading mobility providers to improve service consistency, reduce operating complexity, and establish sustainable long-term competitive advantages.

July 2025 – Lyft announced a partnership with Benteler's Holon division to deploy autonomous electric shuttles beginning in 2026, with plans to scale to thousands of vehicles following initial airport and city deployments, significantly strengthening its autonomous mobility strategy. Source: www.techcrunch.com

July 2025 – Uber Technologies partnered with Lucid and Nuro to launch a robotaxi fleet, targeting deployment of at least 20,000 autonomous vehicles over six years. The collaboration accelerates commercial autonomous ride-hailing while expanding Uber's next-generation mobility platform.

May 2026 – Rapido secured USD 240 million in fresh funding at a USD 3 billion valuation to expand its driver network, strengthen technology capabilities, and accelerate multimodal mobility expansion across high-growth Indian markets.

March 2026 – Uber Technologies and Zoox entered a multi-year partnership to deploy custom-built robotaxis on Uber's platform, with commercial service launching in Las Vegas during summer 2026 and expansion planned for Los Angeles, advancing autonomous ride deployment.

The report delivers comprehensive analysis of the global Ride Hailing Services Market across four major service types, four application segments, four end-user categories, and five geographic regions, providing detailed evaluation of evolving competitive dynamics and operational developments. It assesses digital platform adoption, electric fleet deployment, AI-enabled dispatch systems, autonomous mobility, connected vehicle technologies, and multimodal transportation integration. The study also examines deployment intensity, enterprise mobility adoption, consumer behavior, regulatory developments, and strategic investment priorities influencing market evolution.

The analysis supports business expansion, investment evaluation, competitive benchmarking, and product positioning by profiling major industry participants, technology adoption patterns, deployment strategies, and regional demand variations. It highlights emerging mobility ecosystems, enterprise transportation solutions, urban digitalization initiatives, and sustainable transportation trends expected to reshape competitive positioning between 2026 and 2033, enabling stakeholders to identify high-potential opportunities, optimize operational strategies, and strengthen long-term market participation.

| Report Attribute / Metric | Details |

|---|---|

| Market Revenue (2025) | USD 4,760.0 Million |

| Market Revenue (2033) | USD 18,633.1 Million |

| CAGR (2026–2033) | 18.6% |

| Base Year | 2025 |

| Forecast Period | 2026–2033 |

| Historic Period | 2021–2025 |

| Segments Covered |

By Type

By Application

By End-User

|

| Key Report Deliverables | Revenue Forecast; Market Trends; Growth Drivers & Restraints; Technology Insights; Segmentation Analysis; Regional Insights; Competitive Landscape; Regulatory & ESG Overview; Recent Developments |

| Regions Covered | North America; Europe; Asia-Pacific; South America; Middle East & Africa |

| Key Players Analyzed | Uber Technologies Inc.; Lyft Inc.; Grab Holdings Limited; DiDi Global Inc.; Bolt Technology OÜ; Ola Consumer; Rapido; Gojek; Cabify; Yandex Go; inDrive; FREE NOW; Careem |

| Customization & Pricing | Available on Request (10% Customization Free) |