Reports

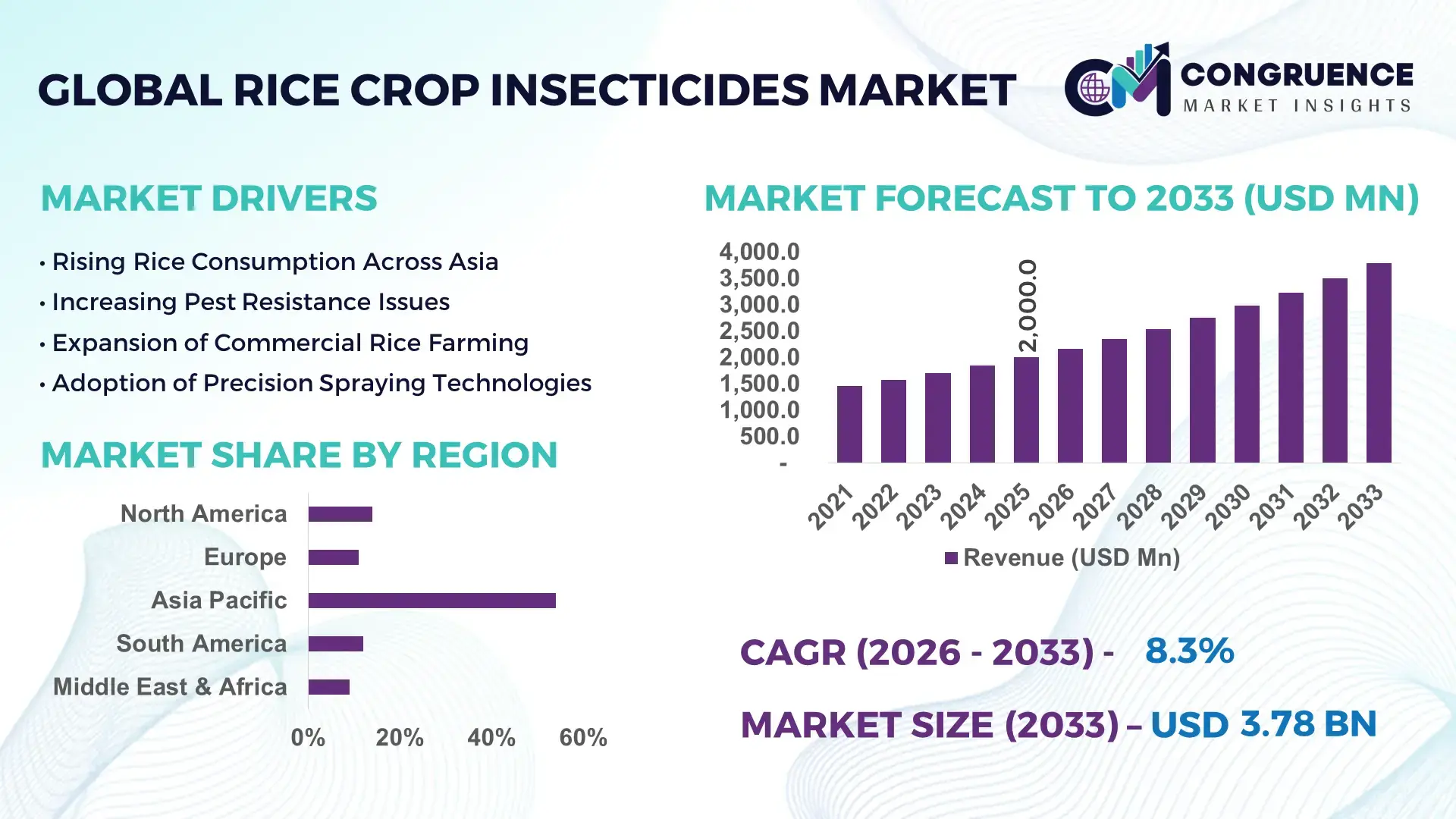

The Global Rice Crop Insecticides Market was valued at USD 2,000 Million in 2025 and is anticipated to reach a value of USD 3,784.9 Million by 2033 expanding at a CAGR of 8.3% between 2026 and 2033, according to an analysis by Congruence Market Insights. The growth is primarily driven by increasing pest resistance, rising rice consumption across Asia-Pacific, and the accelerated adoption of integrated pest management (IPM) programs in high-yield cultivation zones.

China represents the dominant country in the Rice Crop Insecticides Market in terms of production capacity and large-scale application. The country cultivates over 29 million hectares of rice annually and produces more than 210 million metric tons of paddy rice, creating substantial demand for crop protection inputs. China’s domestic agrochemical manufacturing capacity exceeds 2.5 million tons annually, with several large-scale technical-grade insecticide plants supplying both domestic and export markets. Over 70% of large rice farms in eastern provinces deploy drone-based spraying systems, covering more than 120 million hectares cumulatively per year. Government-backed smart agriculture programs have enabled precision-application technologies that reduce chemical usage by nearly 15% while maintaining yield performance above 6.8 tons per hectare in intensive farming clusters.

Market Size & Growth: Valued at USD 2,000 Million in 2025 and projected to reach USD 3,784.9 Million by 2033 at 8.3% CAGR, supported by rising pest incidence affecting over 30% of global rice acreage annually.

Top Growth Drivers: 42% adoption of hybrid rice varieties; 35% increase in drone-based spraying efficiency; 28% rise in pest resistance cases driving chemical rotation demand.

Short-Term Forecast: By 2028, precision spraying technologies are expected to reduce insecticide wastage by 18% and improve field efficiency by 22%.

Emerging Technologies: AI-based pest detection platforms, nano-formulated insecticides, and drone-enabled ultra-low volume spraying systems.

Regional Leaders: Asia-Pacific projected at USD 2,100 Million by 2033 with 65% intensive cultivation adoption; North America at USD 620 Million driven by high-mechanization rates; Latin America at USD 480 Million supported by export-oriented rice farming.

Consumer/End-User Trends: Over 60% of large commercial rice farms integrate IPM models; smallholders increasingly adopt low-residue formulations.

Pilot or Case Example: In 2024, a Jiangsu drone-spraying pilot improved pest mortality rates by 27% while cutting chemical use by 14%.

Competitive Landscape: Syngenta holds approximately 18% share, followed by Bayer, BASF, Corteva Agriscience, and FMC Corporation.

Regulatory & ESG Impact: Over 40 countries tightened residue limits, accelerating shift toward low-toxicity and bio-based formulations.

Investment & Funding Patterns: More than USD 750 Million invested globally in crop protection R&D and smart spraying technologies between 2022–2025.

Innovation & Future Outlook: Expansion of nano-encapsulation, biological insecticide blends, and digital advisory platforms enhancing sustainable rice protection models.

The Rice Crop Insecticides Market is segmented into synthetic pyrethroids (38%), organophosphates (24%), neonicotinoids (18%), and bio-insecticides (20%). Commercial farms account for nearly 58% of total demand, driven by mechanized spraying systems and compliance-driven residue standards. Innovations in nano-formulations and drone-compatible liquid concentrates are improving target accuracy by over 20%. Regulatory tightening on high-toxicity molecules and rising export-quality standards are accelerating the transition toward low-residue chemistries, particularly across Asia-Pacific and Latin America.

The Rice Crop Insecticides Market holds strategic importance in ensuring food security for more than 3.5 billion people who rely on rice as a staple food. With global rice cultivation spanning over 165 million hectares, pest-induced yield losses can reach 30% annually without structured crop protection programs. Modern precision-application systems are reshaping operational strategies; for instance, AI-enabled drone spraying delivers 25% higher deposition efficiency compared to conventional knapsack sprayers.

Asia-Pacific dominates in volume due to its extensive rice-growing acreage, while North America leads in technology adoption with over 72% of commercial rice enterprises using GPS-guided or drone-assisted spraying systems. By 2028, AI-driven pest surveillance platforms are expected to reduce scouting time by 35% and improve targeted chemical usage efficiency by 20%.

From an ESG perspective, firms are committing to measurable sustainability goals, including 25% reduction in chemical runoff and 30% recyclable packaging integration by 2030. In 2024, China achieved a 15% reduction in insecticide usage per hectare through digital advisory and drone-application initiatives in large rice clusters.

Strategically, stakeholders are focusing on bio-based actives, resistance-management rotation programs, and data-driven crop advisory ecosystems. As regulatory standards tighten and export markets demand lower residue levels, the Rice Crop Insecticides Market is positioning itself as a pillar of resilience, regulatory compliance, and sustainable agricultural growth worldwide.

The Rice Crop Insecticides Market dynamics are shaped by rising pest resistance, climate variability, and the increasing need for high-yield crop protection strategies. Brown planthopper, stem borers, and leaf folders account for yield losses exceeding 25% in major rice-producing belts. Technological modernization has enabled over 50% of commercial farms in developed regions to adopt mechanized or drone-based spraying systems, improving uniform coverage and reducing labor dependency by nearly 30%. Regulatory frameworks across more than 40 countries have restricted certain high-toxicity compounds, accelerating innovation in low-residue and biological formulations. Additionally, growing export requirements and traceability mandates are influencing product selection, formulation improvements, and compliance-oriented pest management strategies across Asia-Pacific and emerging Latin American markets.

Pest resistance has emerged as a critical growth catalyst in the Rice Crop Insecticides Market. Field studies indicate that resistance to conventional organophosphates has increased by over 30% in key Asian rice belts over the past decade. Brown planthopper outbreaks alone affect nearly 12 million hectares annually across Asia. Farmers are increasingly rotating active ingredients, leading to a 25% increase in multi-mode-of-action insecticide adoption. Hybrid rice varieties covering approximately 42% of cultivated area demand higher protection precision due to their input sensitivity. This shift is driving adoption of advanced formulations and combination products capable of improving pest mortality rates by 20–28% under intensive cultivation systems.

Environmental and residue compliance regulations are imposing operational constraints on the Rice Crop Insecticides Market. More than 40 importing nations have revised maximum residue limits (MRLs), leading to the phase-out of several high-toxicity molecules. Compliance testing costs for exporters have increased by nearly 18% in the past five years. In addition, environmental monitoring programs report that improper pesticide application contributes to 12–15% runoff contamination in certain river basins. Such regulatory tightening limits product portfolios and increases reformulation costs for manufacturers. Smaller producers face elevated certification expenses and technology adaptation challenges, slowing market penetration in highly regulated regions.

Precision agriculture technologies present significant expansion opportunities in the Rice Crop Insecticides Market. Drone-assisted spraying can cover up to 20 hectares per day, improving operational efficiency by 40% compared to manual methods. AI-driven pest detection tools enhance early infestation identification accuracy by 30%, reducing unnecessary chemical application. In Asia-Pacific, over 120 million hectares are now serviced annually through agricultural drones. Demand for ultra-low volume formulations compatible with automated systems is rising steadily. These advancements enable chemical savings of 15–20% per hectare while maintaining optimal pest control performance, offering scalable and technology-driven growth prospects.

Volatile raw material prices and climatic variability present structural challenges to the Rice Crop Insecticides Market. Active ingredient production costs have fluctuated by up to 22% due to supply chain disruptions. Erratic monsoon patterns affect more than 35% of Asian rice acreage, altering pest lifecycles and increasing unpredictability in application schedules. Flooding and drought conditions reduce effective spraying windows by nearly 15% in certain regions. Additionally, smallholder farmers—who represent over 50% of rice producers globally—often face limited access to advanced application technologies, constraining uniform adoption and operational efficiency.

27% Increase in Drone-Based Spraying Adoption: Drone-assisted insecticide application now covers over 120 million hectares annually in Asia, improving spray precision by 25% and reducing labor requirements by nearly 30%. Adoption rates among large commercial farms exceed 60%, enhancing uniformity and minimizing chemical wastage by 18%.

20% Shift Toward Bio-Based and Low-Residue Formulations: Bio-insecticides now account for approximately 20% of total product usage in regulated export-oriented markets. Field trials indicate residue reduction of 35% compared to traditional chemistries, supporting compliance with stricter international MRL standards.

22% Improvement in Nano-Formulation Efficiency: Nano-encapsulated insecticides demonstrate 22% higher active ingredient stability and 18% longer field persistence, enabling reduced dosage per hectare. Adoption in high-intensity farming zones has grown by over 15% year-on-year.

30% Expansion in AI-Driven Pest Monitoring Systems: AI-based pest detection platforms have improved early infestation identification accuracy by 30%, reducing scouting time by 35%. Over 45% of technologically advanced rice clusters in China and Japan integrate digital advisory systems to optimize application timing and improve yield stability by nearly 12%.

The Rice Crop Insecticides Market is segmented by type, application, and end-user, reflecting differentiated demand patterns across cultivation intensity, pest profiles, and regulatory environments. Product segmentation highlights a gradual transition from conventional synthetic chemistries toward integrated and bio-based formulations, particularly in export-oriented rice economies where residue compliance is critical. Application-wise, foliar spray remains the dominant method due to its rapid knockdown effect against brown planthopper and stem borers, which collectively affect over 25% of Asia’s rice acreage annually. However, seed treatment and soil application methods are gaining structured adoption in mechanized farming clusters to improve early-stage crop protection.

From an end-user perspective, large commercial farms account for the majority of organized procurement, supported by mechanization rates exceeding 65% in developed rice-producing regions. Meanwhile, smallholder farmers—representing more than 50% of global rice growers—are increasingly participating in cooperative-based purchasing models, improving access to advanced formulations and drone-based services. Regulatory shifts toward low-toxicity molecules and precision agriculture integration continue to shape the segmentation landscape.

The Rice Crop Insecticides Market by type includes synthetic pyrethroids, organophosphates, neonicotinoids, diamides, insect growth regulators (IGRs), and bio-insecticides. Synthetic pyrethroids currently account for approximately 38% of total adoption due to their rapid knockdown efficacy and cost efficiency in large-scale foliar spraying. Organophosphates hold about 24%, primarily used in regions where resistance management rotation is essential. Neonicotinoids represent nearly 18%, widely applied in seed treatment for early-stage protection. However, bio-insecticides are the fastest-growing segment, expanding at an estimated CAGR of 11.2%, driven by tightening residue regulations and export compliance standards. Bio-based formulations currently account for around 20% of usage in regulated markets and are projected to expand significantly as integrated pest management adoption rises. Diamides and IGRs together contribute roughly 15% combined share, often used in rotation programs to mitigate resistance.

By application, foliar spray dominates with approximately 52% share, as it provides immediate pest control against planthoppers and leaf folders during peak infestation periods. Seed treatment accounts for about 26% of total adoption, particularly in mechanized farming regions where pre-sowing chemical coating improves early-stage plant vigor and reduces initial pest damage by up to 18%. Soil treatment represents around 12%, mainly used in intensive farming systems targeting root-zone pests. Drone-based ultra-low volume spraying applications currently account for nearly 10% but are expanding rapidly with an estimated CAGR of 12.5%, supported by precision agriculture programs. Commercial rice clusters report that more than 45% of large farms now use GPS-guided or drone-assisted spraying systems. In 2025, approximately 40% of organized rice farming enterprises in Asia-Pacific reported piloting AI-enabled pest surveillance systems to optimize application timing.

Large commercial rice farms represent the leading end-user segment, accounting for nearly 58% of structured insecticide procurement due to mechanized spraying systems and compliance-driven export production. Contract farming enterprises hold around 22%, benefiting from centralized purchasing and technical advisory services. Smallholder farmers collectively contribute approximately 20% of formal market demand but dominate in volume terms across emerging economies. While commercial farms lead adoption, agricultural cooperatives are the fastest-growing end-user segment, expanding at an estimated CAGR of 10.4%, driven by pooled procurement, shared drone services, and government-subsidized precision agriculture initiatives. Over 65% of organized rice exporters now mandate residue-compliant insecticide programs aligned with international standards. In 2025, nearly 38% of mid-sized rice enterprises in Southeast Asia reported transitioning to integrated pest management frameworks to reduce chemical intensity.

Asia-Pacific accounted for the largest market share at 54% in 2025; however, North America is expected to register the fastest growth, expanding at a CAGR of 9.6% between 2026 and 2033.

Asia-Pacific’s dominance is supported by more than 145 million hectares of harvested rice area, representing over 85% of global rice cultivation acreage. China and India together account for nearly 50% of global paddy production, driving high-volume insecticide consumption for brown planthopper and stem borer control. North America, while representing only 14% market share, demonstrates higher per-hectare insecticide intensity, averaging 18–22% greater application efficiency due to precision spraying systems. Europe contributes approximately 11% share, driven by residue-compliant formulations and regulatory-driven product innovation. South America holds close to 12%, supported by Brazil’s export-oriented rice clusters exceeding 1.6 million hectares. The Middle East & Africa region collectively accounts for nearly 9%, with modernization programs increasing chemical input usage by over 15% in irrigated rice zones over the past five years.

North America accounts for approximately 14% of the global Rice Crop Insecticides Market, supported primarily by the United States, which cultivates nearly 1.1 million hectares of rice annually. The region demonstrates high mechanization levels, with over 75% of commercial rice farms utilizing GPS-guided or drone-assisted spraying systems. Demand is driven by export-quality compliance, contract farming operations, and high-yield hybrid rice programs averaging 8.5 tons per hectare. Regulatory oversight under strict environmental frameworks has accelerated adoption of low-residue and EPA-approved active ingredients. Digital transformation is prominent, with nearly 70% of large rice enterprises integrating farm management software for spray optimization. FMC Corporation actively invests in next-generation diamide insecticides tailored for resistance management in southern U.S. rice belts. Consumer behavior reflects enterprise-led procurement, with cooperative-based purchasing influencing nearly 60% of total volume contracts.

Europe represents roughly 11% of the global Rice Crop Insecticides Market, with Italy, Spain, and France serving as major rice-producing economies. Italy alone accounts for over 50% of Europe’s rice cultivation area, covering approximately 220,000 hectares. Regulatory frameworks emphasizing reduced chemical load and strict maximum residue levels are influencing formulation shifts toward bio-insecticides, which now represent nearly 28% of product usage in certain EU rice clusters. Precision spraying systems are implemented across more than 40% of mechanized farms, improving dosage accuracy by 15–20%. Sustainability initiatives targeting 25% reduction in chemical pesticide usage by 2030 are accelerating demand for innovative actives. BASF and Bayer have expanded integrated pest management programs tailored to Mediterranean rice systems. Regional buyer behavior reflects strong compliance-driven procurement, with over 65% of exporters prioritizing residue-certified insecticide programs.

Asia-Pacific dominates in volume, accounting for nearly 54% of the global Rice Crop Insecticides Market. China, India, Indonesia, Vietnam, and Japan collectively cultivate more than 140 million hectares of rice annually. China alone produces over 210 million metric tons of rice, while India exceeds 180 million metric tons, sustaining extensive insecticide demand cycles. Manufacturing infrastructure in China surpasses 2.5 million tons of agrochemical production capacity annually, ensuring steady regional supply. Drone-assisted spraying now services over 120 million hectares across the region, improving coverage efficiency by approximately 25%. Syngenta and several regional agrochemical firms are expanding nano-formulation facilities to address resistance challenges. Consumer behavior varies significantly, with smallholder farmers accounting for more than 50% of volume consumption, while organized agribusiness clusters adopt digital pest surveillance at rates exceeding 45%.

South America contributes approximately 12% of the global Rice Crop Insecticides Market, led by Brazil and Argentina. Brazil cultivates nearly 1.6 million hectares of rice, with Rio Grande do Sul accounting for over 70% of national production. Export-driven farming requires strict compliance with international residue standards, increasing adoption of low-toxicity insecticides by nearly 20% over the past five years. Infrastructure modernization and irrigation expansion have improved yield averages to 7.0 tons per hectare. Government-backed agricultural financing programs support chemical input procurement for commercial farms. Ourofino Agrociência is expanding crop protection portfolios to address regional pest resistance trends. Consumer behavior reflects strong cooperative structures, with more than 55% of rice growers participating in collective procurement agreements to negotiate input pricing.

The Middle East & Africa region accounts for approximately 9% of the global Rice Crop Insecticides Market, supported by Egypt, Nigeria, and parts of West Africa. Egypt cultivates over 600,000 hectares of rice, with irrigation-driven systems requiring structured pest control programs. Government food security strategies have increased rice production capacity in several African nations by nearly 18% over the last five years, indirectly expanding insecticide demand. Technological modernization remains gradual; however, drone trials have expanded by 12% annually in select commercial farms. Trade partnerships facilitating agrochemical imports have improved product availability. Regional consumer behavior shows mixed adoption patterns, with smallholder farms representing over 65% of end-user volume, often relying on government-supported extension services for pest management guidance.

China – 29% Market Share: High agrochemical production capacity exceeding 2.5 million tons annually and extensive rice cultivation above 29 million hectares support dominant positioning in the Rice Crop Insecticides Market.

India – 21% Market Share: Large-scale paddy cultivation above 45 million hectares and strong smallholder demand for pest control inputs drive significant contribution to the Rice Crop Insecticides Market.

The Rice Crop Insecticides Market is moderately consolidated, with the top five multinational agrochemical companies accounting for approximately 58–62% of total global market share. More than 120 active agrochemical manufacturers and formulators operate globally, including regional generic producers and specialty biological firms. Tier-1 players maintain strong positioning through patented active ingredients, integrated pest management (IPM) portfolios, and digital agronomy platforms.

Strategic initiatives between 2023 and 2025 have included over 25 new product registrations for rice-specific insecticide formulations across Asia-Pacific and Latin America. Leading firms are expanding nano-formulation R&D pipelines, with nearly 15% of new product launches incorporating controlled-release or encapsulation technologies. Partnerships between agrochemical companies and agri-tech drone service providers have grown by more than 30%, enhancing precision-application compatibility.

Competitive differentiation increasingly centers on resistance management, residue-compliant chemistries, and digital farm advisory integration. Several global leaders allocate more than 8% of annual operating budgets to R&D, targeting next-generation diamides and bio-insecticides. Regional manufacturers in China and India collectively account for over 35% of technical-grade insecticide output, intensifying pricing competition in emerging markets. The market structure reflects strong multinational leadership alongside a vibrant base of domestic producers, particularly in Asia-Pacific.

Corteva Agriscience

FMC Corporation

UPL Limited

Sumitomo Chemical Co., Ltd.

Nufarm Limited

ADAMA Ltd.

Mitsui Chemicals Agro, Inc.

Nissan Chemical Corporation

PI Industries Ltd.

Rallis India Limited

Indofil Industries Limited

American Vanguard Corporation

Shandong Weifang Rainbow Chemical Co., Ltd.

Technological transformation in the Rice Crop Insecticides Market is centered on precision agriculture, formulation science, and digital integration. Drone-based ultra-low volume (ULV) spraying systems now cover over 120 million hectares annually in Asia-Pacific, improving spray uniformity by up to 25% and reducing chemical drift by nearly 18% compared to conventional boom sprayers. GPS-guided variable rate technology (VRT) systems are deployed across more than 70% of large commercial rice farms in North America, enabling site-specific dosage control.

Nano-encapsulation and controlled-release technologies are enhancing active ingredient stability by 20–22%, extending residual activity while reducing total chemical load per hectare. Microbial and botanical bio-insecticides now represent nearly 20% of regulated market applications, driven by environmental compliance and export quality standards. AI-based pest detection tools leveraging satellite imagery and field sensors improve early infestation identification accuracy by approximately 30%, reducing scouting time by 35%.

Digital farm management platforms integrate weather analytics and pest lifecycle modeling, improving application timing precision by nearly 15%. Robotics-assisted spraying systems are being piloted in high-density rice clusters, demonstrating labor cost reductions of up to 28%. Additionally, biodegradable packaging innovations targeting 30% recyclability improvement by 2030 are gaining adoption, aligning product innovation with sustainability mandates. These technologies collectively enhance productivity, compliance, and operational efficiency for rice producers worldwide.

• In August 2025, Insecticides (India) Limited announced the launch of “SPARCLE”, a broad-spectrum insecticide developed in collaboration with Corteva Agriscience, specifically formulated to help paddy farmers control brown plant hopper (BPH) pests and improve rice yields in major Indian rice belts. Source: www.insecticidesindia.com

• In February 2025, BASF SE introduced its new rice-focused insecticide Valexio in India, powered by the novel Prexio Active mode of action designed to target all four major rice hopper species with resistance-breaking chemistry.

• In October 2025, Syngenta announced the launch of SEGURIS™ Evo and VESTORIA™ Pro, enhanced protection solutions developed to bolster pest and disease defense in rice systems across Asia-Pacific agricultural markets.

• In 2025, Corteva Agriscience expanded its portfolio with new sustainable pest management solutions including a bioinsecticide offering broad control against sap-feeding and chewing insects, marking Corteva’s first bioinsecticide innovation for broad crop protection. Source: www.agribusinessglobal.com

The Rice Crop Insecticides Market Report provides a comprehensive evaluation of product types, application techniques, end-user segments, regional performance, and technological advancements shaping industry development. The scope covers synthetic insecticides—including pyrethroids, organophosphates, neonicotinoids, and diamides—as well as biological and nano-formulated alternatives. Application coverage spans foliar spraying (over 50% usage share), seed treatment (approximately 25%), soil treatment, and drone-based ultra-low volume systems.

Geographically, the report assesses five key regions—Asia-Pacific, North America, Europe, South America, and the Middle East & Africa—analyzing cultivation acreage, production intensity, regulatory frameworks, and technology penetration levels. It evaluates over 120 active manufacturers and formulators, examining innovation pipelines, resistance management strategies, and sustainability initiatives.

The scope further incorporates precision agriculture integration, AI-enabled pest monitoring, and digital advisory ecosystems influencing application efficiency improvements of up to 30% in advanced farming systems. It also addresses compliance-driven product reformulations, export-oriented residue standards, and cooperative-based procurement models affecting more than 50% of smallholder rice growers globally.

By combining segmentation analytics, regional performance metrics, competitive benchmarking, and technology assessment, the report equips decision-makers with actionable insights into operational optimization, regulatory alignment, and long-term strategic positioning within the Rice Crop Insecticides Market.

| Report Attribute / Metric | Details |

|---|---|

| Market Revenue (2025) | USD 2,000 Million |

| Market Revenue (2033) | USD 3,784.9 Million |

| CAGR (2026–2033) | 8.3% |

| Base Year | 2025 |

| Forecast Period | 2026–2033 |

| Historic Period | 2021–2025 |

| Segments Covered |

By Type

By Application

By End-User Insights

|

| Key Report Deliverables | Revenue Forecast; Market Trends; Growth Drivers & Restraints; Technology Insights; Segmentation Analysis; Regional Insights; Competitive Landscape; Regulatory & ESG Overview; Recent Developments |

| Regions Covered | North America; Europe; Asia-Pacific; South America; Middle East & Africa |

| Key Players Analyzed | Syngenta; Bayer AG; BASF SE; Corteva Agriscience; FMC Corporation; UPL Limited; Sumitomo Chemical Co., Ltd.; Nufarm Limited; ADAMA Ltd.; Mitsui Chemicals Agro, Inc.; Nissan Chemical Corporation; PI Industries Ltd.; Rallis India Limited; Indofil Industries Limited; American Vanguard Corporation; Shandong Weifang Rainbow Chemical Co., Ltd. |

| Customization & Pricing | Available on Request (10% Customization Free) |