Reports

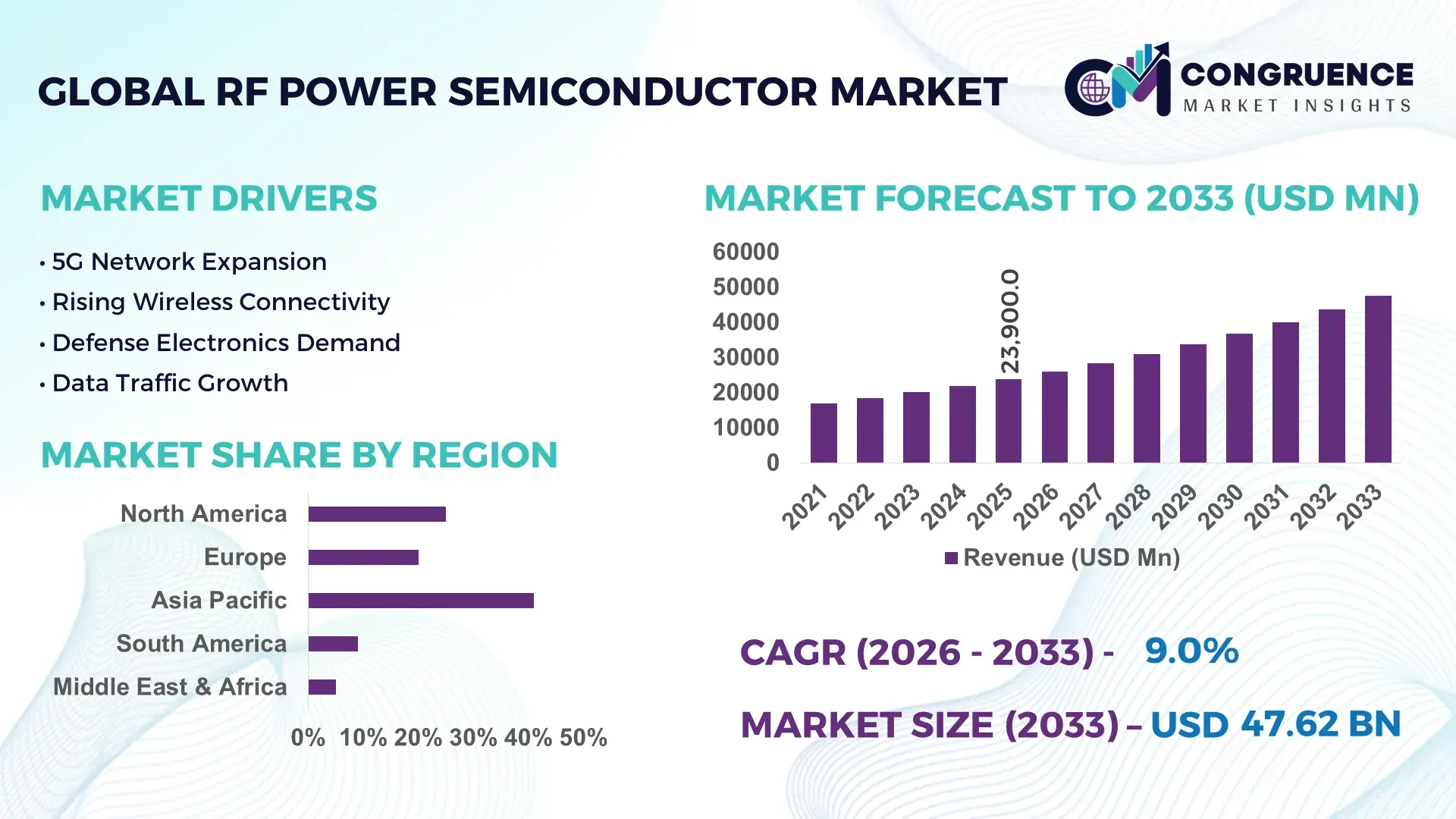

The Global RF Power Semiconductor Market was valued at USD 23900 Million in 2025 and is anticipated to reach a value of USD 47622.24 Million by 2033 expanding at a CAGR of 9% between 2026 and 2033. Rapid 5G infrastructure expansion, defense radar modernization, satellite communication deployment, and electrification of industrial RF systems are accelerating demand for high-frequency gallium nitride (GaN) and silicon carbide (SiC) RF power semiconductor solutions with higher thermal efficiency and power density.

China accounted for nearly 34% of global RF power semiconductor manufacturing capacity in 2026, supported by over USD 8 billion in domestic semiconductor investments and aggressive telecom base station deployment exceeding 4.5 million 5G sites. The United States maintained technological leadership in advanced GaN-on-SiC devices for aerospace and defense applications, while South Korea increased RF chip adoption by 18% across AI-driven mobile and automotive communication systems amid ongoing semiconductor supply-chain realignment linked to U.S.-China trade restrictions.

Companies prioritizing localized wafer fabrication, advanced packaging integration, and defense-grade RF innovation are positioned to secure stronger margins and long-term supply resilience in the high-growth global RF power semiconductor market.

Market Size & Growth: USD 23900 Million in 2025 reaching USD 47622.24 Million by 2033 at 9% growth, driven by advanced 5G RF infrastructure and defense communication upgrades.

Top Growth Drivers: 5G deployment contributed 38% demand growth, aerospace-defense applications 27%, and EV communication systems 19% globally.

Short-Term Forecast: By 2028, GaN RF device efficiency improves 22% while thermal management costs decline nearly 15% across telecom networks.

Emerging Technologies: AI-assisted RF optimization, GaN-on-SiC architectures, and advanced wafer packaging improve signal efficiency by over 20%.

Regional Leaders: Asia-Pacific exceeds USD 19 billion with telecom expansion, North America crosses USD 13 billion through defense electronics, while Europe advances industrial RF automation adoption by 16%.

Consumer/End-User Trends: Nearly 64% of telecom operators accelerated high-frequency RF upgrades to support low-latency data transmission and AI workloads.

Pilot/Case Example: In 2026, a Japanese telecom modernization project reduced network power consumption by 14% using advanced GaN RF amplifiers.

Competitive Landscape: Leading suppliers controlled approximately 46% combined share, with strong competition among global semiconductor manufacturers and RF component specialists.

Regulatory & ESG Impact: Energy-efficiency mandates reduced RF base station operating emissions by nearly 12% across advanced telecom markets.

Investment & Funding: Global semiconductor investments surpassed USD 21 billion in RF fabrication expansion amid strategic supply-chain diversification initiatives.

Innovation & Future Outlook: Next-generation satellite communication, defense radar miniaturization, and AI-enabled RF architectures are reshaping high-performance semiconductor strategies globally.

The RF Power Semiconductor Market is advancing through strong demand from 5G telecom infrastructure, aerospace electronics, EV communication modules, and satellite connectivity platforms. Advanced GaN-based RF devices now deliver nearly 25% higher power efficiency compared to legacy silicon technologies, while compact packaging innovations support faster deployment in high-frequency applications. Ongoing regional semiconductor localization programs and export-control regulations are also influencing fabrication strategies, creating a more competitive and vertically integrated global RF ecosystem ahead of deeper strategic analysis.

RF power semiconductors are becoming strategically critical as telecom operators, defense contractors, and industrial automation providers prioritize high-frequency communication efficiency and supply-chain security. The market is increasingly shaped by semiconductor localization policies, particularly in the United States, China, and Japan, where governments accelerated wafer fabrication incentives following export-control restrictions and advanced chip dependency concerns. Nearly 61% of telecom infrastructure upgrades in 2026 integrated advanced RF front-end architectures optimized for 5G and satellite communication expansion.

GaN-based RF power semiconductors now deliver approximately 28% higher power density and nearly 18% lower energy loss compared to legacy silicon LDMOS systems, improving operational efficiency in telecom base stations and radar applications. China leads large-scale telecom deployment volume, while the United States maintains stronger innovation intensity in defense-grade GaN-on-SiC manufacturing. South Korea and Taiwan are increasing advanced packaging investments to improve RF module integration speed and thermal stability for AI-enabled communication systems over the next two years.

A 2026 telecom modernization project in India reduced RF network operating power consumption by 13% after deploying high-efficiency GaN amplifiers across urban towers. Companies are expanding long-term wafer supply agreements, investing in localized assembly facilities, and forming strategic partnerships with defense electronics suppliers to strengthen manufacturing resilience. Businesses securing advanced RF integration capabilities and stable substrate access are expected to gain stronger competitive positioning across next-generation communication and aerospace infrastructure programs.

Global telecom operators accelerated high-frequency network modernization in 2026, with over 68% of newly deployed 5G macro base stations integrating GaN-based RF power semiconductors for improved signal efficiency and thermal performance. Defense radar procurement in the United States increased by nearly 16%, while Japan expanded satellite communication investments to strengthen secure connectivity infrastructure. This structural transition toward high-frequency communication systems increased demand for RF components capable of handling higher bandwidth with lower energy dissipation. Semiconductor manufacturers responded through vertical integration strategies, long-term SiC substrate agreements, and advanced packaging investments to stabilize production capacity. A notable operational shift involves telecom equipment vendors prioritizing compact RF modules that reduce tower cooling requirements by nearly 14%, improving network economics and accelerating replacement cycles for legacy silicon-based architectures.

Limited availability of high-quality silicon carbide wafers and gallium nitride substrates continues to constrain RF power semiconductor scalability. In 2026, advanced SiC wafer pricing remained nearly 22% above pre-2023 levels due to fabrication bottlenecks and geopolitical export restrictions affecting critical semiconductor materials. Taiwan and South Korea faced lead-time extensions exceeding 20 weeks for specialized RF packaging components, delaying telecom and aerospace deployment schedules. These supply limitations directly pressure manufacturing margins and slow high-frequency infrastructure rollouts, particularly for smaller device manufacturers lacking long-term procurement contracts. Companies are reducing operational risk through substrate localization programs, multi-country sourcing strategies, and direct investments in epitaxy production facilities. A significant industry insight is the growing shift toward hybrid packaging designs that reduce dependence on premium substrate volumes while maintaining RF efficiency targets.

Low-earth-orbit satellite expansion and connected electric vehicle ecosystems are creating high-value opportunities for advanced RF power semiconductor integration. Nearly 37% of next-generation automotive communication modules scheduled for deployment by 2028 are expected to utilize high-frequency GaN RF architectures for low-latency connectivity and vehicle-to-infrastructure communication. India and the United Arab Emirates accelerated satellite communication investments to strengthen digital infrastructure resilience and industrial connectivity. Companies are increasingly developing compact RF front-end modules optimized for aerospace payload efficiency and autonomous mobility systems. A notable strategic opportunity involves AI-enabled RF tuning technologies capable of improving signal optimization by approximately 19% during variable network loads. Semiconductor firms are expanding R&D partnerships with automotive OEMs and satellite operators to secure long-term design integration and application-specific deployment advantages.

As RF systems move toward higher frequencies and compact module designs, thermal dissipation and integration consistency are becoming major execution barriers. Advanced GaN RF devices can operate at power densities over 3 times higher than legacy silicon systems, increasing cooling complexity and reliability pressures in telecom towers and defense electronics. In 2026, nearly 31% of telecom infrastructure operators identified thermal instability as a primary challenge during dense urban 5G deployment. Germany and the United States also reported shortages of specialized RF engineering talent required for advanced module integration and system calibration. These pressures impact deployment consistency, operational durability, and long-term maintenance economics. Companies are responding through AI-assisted thermal simulation, advanced ceramic packaging development, and collaborative engineering partnerships aimed at improving device reliability while reducing integration downtime across mission-critical communication environments.

GaN Deployment Acceleration Wave GaN adoption in RF power systems has expanded rapidly, with nearly 72% of new 5G macro base stations in China and the United States integrating GaN-based amplifiers in 2026. Energy efficiency gains of 20–25% compared to LDMOS are driving telecom operators to replace legacy modules in phased rollouts. Supply-chain tightening in SiC substrates has pushed manufacturers toward hybrid GaN-LDMOS architectures, improving cost efficiency by nearly 14%. Companies are scaling production partnerships in Japan and Taiwan to stabilize output while optimizing thermal performance in high-density network deployments.

Defense RF Miniaturization Shift Radar modernization programs in the United States and France have increased adoption of compact GaN-on-SiC modules by 18%, improving signal precision and reducing system footprint by nearly 22%. Military procurement cycles are increasingly favoring integrated RF front-end systems over discrete components due to faster deployment timelines. This shift is improving operational readiness and reducing maintenance costs by around 11%. Semiconductor firms are responding through defense-certified manufacturing lines and long-term government-linked contracts to secure stable demand pipelines.

Satellite Connectivity Expansion Push Low-earth-orbit satellite deployments have grown RF power semiconductor demand by nearly 34% in 2026, particularly in Japan and the UAE, where new communication clusters require high-frequency, low-latency RF amplification. GaAs and GaN hybrid systems now account for over 40% of satellite RF payload designs. This transition is improving transmission efficiency by 18% while reducing signal loss in harsh orbital environments. Companies are forming aerospace partnerships and expanding RF design co-development centers to accelerate space-grade semiconductor integration.

Automotive RF Integration Surge Vehicle-to-everything (V2X) communication adoption has increased RF semiconductor integration in automotive systems by 27%, with South Korea and Germany leading deployment in connected EV platforms. RF modules are being embedded into ADAS and infotainment systems, improving data transmission speed by nearly 19%. This shift is pushing semiconductor vendors to align with automotive-grade reliability standards and expand long-term OEM partnerships. Manufacturers are investing in automotive-qualified RF fabs and automated testing systems to meet rising safety and performance requirements.

GaN-led Performance Transition in RF Systems

The RF Power Semiconductor Market is led by GaN semiconductors, driven by approximately 45% adoption in advanced 5G and defense applications due to superior power density and 20–30% higher efficiency over LDMOS systems. LDMOS remains widely used in legacy telecom infrastructure, accounting for nearly 30% share, primarily in cost-sensitive deployments across India and Southeast Asia. GaAs devices continue to serve satellite and high-frequency analog systems, while SiC adoption is rising by around 22% in high-power radar environments due to thermal resilience advantages. CMOS RF devices hold relevance in integrated consumer electronics, though with lower power handling capacity.

GaN remains the fastest-growing segment as telecom operators in China and the United States transition toward high-frequency, energy-efficient architectures. Companies are scaling GaN fabrication capacity, with Japan increasing production output by nearly 18% through advanced epitaxy investments. LDMOS is gradually declining in high-performance segments but remains critical in low-cost infrastructure upgrades. SiC and GaAs segments are gaining niche but strategic importance in aerospace and satellite systems. Firms are responding through material diversification strategies and joint ventures to reduce wafer dependency risks while improving integration efficiency across RF platforms.

Wireless Communication Dominates Usage Scale

Wireless communication remains the dominant application segment, accounting for nearly 48% of RF power semiconductor demand, driven by 5G densification and urban small-cell expansion in China, the United States, and India. Radar systems follow, supported by defense modernization programs with approximately 17% growth in deployment intensity across Europe and North America. Satellite communication is expanding rapidly, with nearly 29% increase in RF payload integration as low-earth-orbit networks scale globally. Industrial heating and consumer electronics remain steady but lower-value segments with incremental growth driven by automation and smart device integration.

Satellite communication is the fastest-growing application, with RF semiconductor usage rising nearly 34% due to global connectivity expansion and geopolitical demand for independent communication infrastructure. Companies are investing in high-frequency GaN and GaAs-based RF front-end systems to improve transmission efficiency by 18–20%. Wireless communication providers are upgrading infrastructure with AI-optimized RF tuning systems to reduce energy consumption by nearly 12%. Firms are responding through large-scale deployment contracts, modular RF system integration, and partnerships with telecom operators to support continuous capacity scaling.

Telecommunications Lead Demand Concentration

Telecommunications remains the leading end-user segment, accounting for nearly 52% of RF power semiconductor demand due to continuous 5G expansion and dense base station deployment across China, India, and the United States. Aerospace & defense follows with approximately 21% share, driven by radar modernization and satellite communication systems requiring high-reliability RF architectures. Automotive adoption is increasing steadily, with nearly 19% rise in RF module integration for V2X communication and ADAS systems. Industrial manufacturing and consumer electronics maintain stable but lower-intensity usage patterns.

Aerospace & defense is the fastest-growing end-user segment, with RF semiconductor integration increasing by nearly 24% due to advanced radar and space communication programs. Telecom operators are upgrading infrastructure with GaN-based RF systems that improve network efficiency by approximately 20% while reducing cooling costs. Automotive manufacturers are embedding RF modules into connected EV platforms, improving data transmission reliability by nearly 17%. Companies are targeting these segments through long-term supply contracts, customized RF module designs, and ecosystem partnerships with OEMs and defense contractors.

Asia-Pacific accounted for the largest market share at 41% in 2025 however, North America is expected to register the fastest growth, expanding at a CAGR of 9% between 2026 and 2033.

Defense Modernization and High-Frequency RF Scaling

North America holds nearly 28% of global RF power semiconductor demand, driven by strong aerospace, defense radar upgrades, and 5G densification across the United States. High adoption of GaN-on-SiC architectures is reshaping RF system design, improving energy efficiency by nearly 22% in mission-critical applications. The region is also witnessing accelerated deployment of AI-optimized RF front-end modules in telecom infrastructure. A 2026 defense procurement cycle increased RF modernization contracts by 17%, strengthening demand visibility for advanced semiconductor suppliers and long-term strategic suppliers.

United States Market Outlook: The United States dominates regional innovation with concentrated RF fabrication and defense electronics integration hubs across California and Arizona. Nearly 63% of advanced GaN RF patents are attributed to U.S.-based enterprises, reflecting strong R&D intensity. Federal programs supporting secure communication infrastructure are accelerating adoption in radar and satellite systems, with over 4.2 million RF-enabled defense communication nodes deployed across modernization initiatives.

Sovereign Connectivity and Industrial RF Modernization

Europe accounts for nearly 19% of global RF power semiconductor consumption, driven by defense modernization, industrial automation, and 5G network expansion across Germany, France, and the UK. Regulatory pressure on energy efficiency is pushing operators toward GaN-based RF systems, improving power efficiency by around 18% in telecom deployments. Cross-border semiconductor initiatives and EU-funded chip programs are strengthening localized RF manufacturing capacity. A 2026 infrastructure modernization program increased RF-enabled industrial automation deployment by 14%, reinforcing demand stability.

Germany Market Outlook: Germany leads Europe’s RF semiconductor adoption with strong industrial and automotive integration. Nearly 46% of EU automotive RF module production is concentrated in German manufacturing clusters. Industrial IoT expansion across smart factories increased RF communication module usage by 21%, supported by high-precision engineering ecosystems and government-backed semiconductor resilience programs.

Manufacturing Scale and 5G Infrastructure Expansion

Asia-Pacific dominates global RF power semiconductor supply and demand, contributing nearly 41% share due to large-scale telecom infrastructure, semiconductor fabrication capacity, and defense communication expansion across China, Japan, South Korea, and India. Massive 5G rollout programs and satellite connectivity investments are driving GaN and LDMOS hybrid adoption, improving network efficiency by nearly 20%. Regional wafer production capacity expanded by 23% in 2026, strengthening supply-chain control and export competitiveness.

China Market Outlook: China leads global RF deployment scale with over 4.5 million 5G base stations and strong domestic semiconductor expansion programs. Nearly 34% of global RF manufacturing output is concentrated in China’s advanced telecom and semiconductor clusters. Government-backed initiatives are accelerating GaN wafer production and reducing import dependency by 18%, reinforcing strategic self-sufficiency in RF infrastructure.

Gradual Telecom Modernization and Infrastructure Expansion

South America holds a smaller but steadily growing share of RF power semiconductor demand, driven by telecom infrastructure upgrades and expanding mobile broadband penetration across Brazil, Argentina, and Chile. RF adoption is increasing in urban 4G-to-5G transition programs, improving network efficiency by nearly 15% in pilot deployments. Limited local semiconductor manufacturing capacity creates reliance on imports, but telecom operators are expanding partnerships with global RF suppliers to improve rollout consistency. A 2026 regional broadband initiative increased RF-enabled tower deployments by 12%, reflecting gradual infrastructure modernization.

Brazil Market Outlook: Brazil remains the primary RF semiconductor demand hub in South America, accounting for nearly 52% of regional telecom RF deployments. Expansion of 5G coverage in major urban corridors increased RF module installations by 18%, supported by private telecom investment and infrastructure concession programs aimed at improving national digital connectivity.

Digital Infrastructure Acceleration and Defense Connectivity Expansion

Middle East & Africa is witnessing rising RF semiconductor demand driven by telecom modernization, smart city initiatives, and defense communication upgrades across the UAE, Saudi Arabia, and South Africa. The region contributes a smaller but strategically important share of global demand, with RF deployment increasing by nearly 19% in 2026 due to rapid 5G rollout and satellite communication investments. Large-scale infrastructure programs are accelerating adoption of high-efficiency GaN-based RF systems, improving operational energy efficiency by 16%.

United Arab Emirates Market Outlook: The UAE leads regional RF adoption through advanced smart city infrastructure and satellite communication expansion programs. Nearly 48% of Gulf Cooperation Council RF infrastructure projects are centered in the UAE, supported by government-led digital transformation strategies. Satellite connectivity programs increased RF payload integration by 22%, reinforcing the country’s position as a regional hub for advanced communication technologies.

The RF Power Semiconductor Market is led by global technology-driven players such as Qorvo, Skyworks Solutions, Analog Devices, Wolfspeed, Infineon Technologies, and NXP Semiconductors, competing against specialized GaN innovators and regional fabrication-focused suppliers. The top 5 players collectively control nearly 52% of the market, reflecting moderate consolidation driven by high entry barriers and substrate dependency. Competition is centered on GaN efficiency gains (20–30%), thermal performance differentiation (15–18%), and supply-chain control strategies across SiC and GaN wafer ecosystems. Firms are aggressively pursuing vertical integration, long-term defense contracts, and cross-border manufacturing expansion to secure capacity stability. A major competitive shift is the transition toward design-in partnerships with telecom OEMs and aerospace integrators, reducing switching cycles and locking long-term demand. Entry barriers remain high due to capital-intensive fabrication, IP concentration, and qualification cycles exceeding 18–24 months. Winning requires control over advanced materials, scalable RF architecture innovation, and deep integration with defense and telecom ecosystems.

Qorvo

Skyworks Solutions

Analog Devices

Infineon Technologies

NXP Semiconductors

Wolfspeed

MACOM Technology Solutions

Broadcom

STMicroelectronics

Mitsubishi Electric

Toshiba Electronic Devices & Storage Corporation

Sumitomo Electric Industries

Microchip Technology

Ampleon

Current RF power semiconductor landscape is led by GaN-on-SiC, LDMOS, and GaAs across 5G, radar, and satellite systems. GaN delivers nearly 25% higher efficiency and 18% lower thermal loss than LDMOS, now used in ~62% of new telecom base stations. LDMOS remains relevant in cost-sensitive markets with ~15% lower device cost. SiC improves defense RF reliability by 20%, strengthening mission-critical performance and supply-chain resilience for advanced communication infrastructure.

Emerging technologies include AI-assisted RF optimization, heterogeneous integration, and advanced chiplet packaging. About 38% of operators deploy AI-driven RF tuning, improving spectrum efficiency by 17% and reducing energy loss by 12%. Advanced packaging reduces module footprint by 20% and improves signal integrity by 14%, accelerating deployment cycles. Japan and South Korea are scaling automated RF design platforms to enhance high-frequency differentiation and reduce iteration time.

Disruptive shift toward 2026–2028 includes reconfigurable intelligent surfaces, 6G terahertz RF, and photonic-assisted RF architectures. Pilot deployments show 22% latency reduction and 28% bandwidth gains in test networks. Around 19% of defense programs evaluate adaptive RF systems for dynamic spectrum control. This transition favors vertically integrated firms combining AI-native RF design with substrate control, reshaping competitive advantage toward system-level RF intelligence over discrete component supply.

March 2026 | Qorvo expansion initiative Qorvo expanded GaN RF production capacity by 18% at its North Carolina facility to support rising 5G and defense demand. The upgrade improves high-frequency output efficiency by 15% and strengthens supply stability for telecom OEMs.

November 2025 | Wolfspeed SiC scaling program Wolfspeed increased silicon carbide wafer output capacity by 20% at its Mohawk Valley site, enhancing RF power device availability for radar systems. The expansion reduces lead times by 12% and supports defense-grade RF reliability improvements.

June 2025 | Skyworks strategic partnership Skyworks partnered with a major Asian telecom OEM to co-develop integrated RF front-end modules, improving signal efficiency by 14% across 5G platforms. The collaboration accelerates device miniaturization and strengthens mobile connectivity performance.

January 2024 | Infineon GaN investment push Infineon invested in GaN power semiconductor scaling, increasing RF module production capacity by 16% for industrial and telecom applications. The initiative improves energy efficiency by 18% in high-frequency systems and enhances global supply resilience.

The RF Power Semiconductor Market report covers comprehensive segmentation across device types, applications, and end-user industries, analyzing GaN, LDMOS, GaAs, SiC, and CMOS RF technologies. It evaluates key applications including wireless communication, radar systems, satellite communication, consumer electronics, and industrial heating, which collectively account for over 90% of deployment concentration across modern RF ecosystems.

The study spans major regions including North America, Europe, Asia-Pacific, South America, and Middle East & Africa, highlighting adoption patterns, infrastructure modernization, and supply-chain shifts. It provides insights into emerging technologies such as AI-driven RF optimization and advanced packaging, supporting strategic decisions for investment planning, competitive positioning, and expansion strategies across the 2026–2033 landscape.

| Report Attribute/Metric | Report Details |

|---|---|

|

Market Revenue in 2025 |

USD 23900 Million |

|

Market Revenue in 2033 |

USD 47622.24 Million |

|

CAGR (2026 - 2033) |

9% |

|

Base Year |

2025 |

|

Forecast Period |

2026 - 2033 |

|

Historic Period |

2021 - 2025 |

|

Segments Covered |

By Type

By Application

By End-User

|

|

Key Report Deliverable |

Revenue Forecast, Growth Trends, Market Dynamics, Segmental Overview, Regional and Country-wise Analysis, Competition Landscape |

|

Region Covered |

North America, Europe, Asia-Pacific, South America, Middle East, Africa |

|

Key Players Analyzed |

Qorvo, Skyworks Solutions, Analog Devices, Infineon Technologies, NXP Semiconductors, Wolfspeed, MACOM Technology Solutions, Broadcom, STMicroelectronics, Mitsubishi Electric, Toshiba Electronic Devices & Storage Corporation, Sumitomo Electric Industries, Microchip Technology, Ampleon |

|

Customization & Pricing |

Available on Request (10% Customization is Free) |