Reports

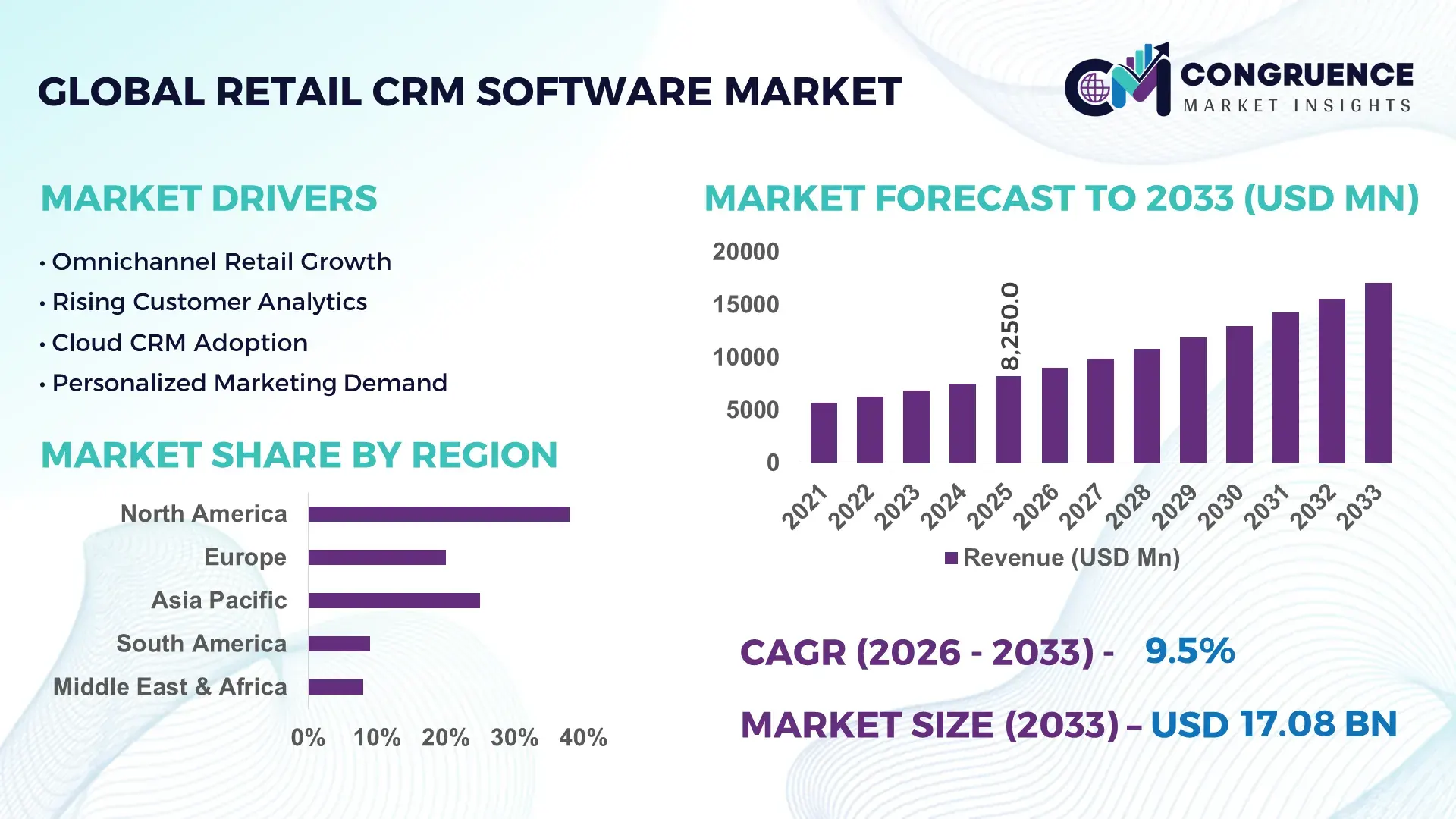

The Global Retail CRM Software Market was valued at USD 8250 Million in 2025 and is anticipated to reach a value of USD 17076.6 Million by 2033 expanding at a CAGR of 9.52% between 2026 and 2033. Growth is being accelerated by AI-powered customer analytics, omnichannel engagement platforms, loyalty program digitization, and real-time personalization capabilities adopted across large retail chains and e-commerce ecosystems.

The United States remains the dominant country, accounting for approximately 34% of global retail CRM software adoption, supported by over USD 15 billion in annual retail technology investments and widespread deployment across grocery, fashion, and specialty retail segments. Compared with Germany, where adoption penetration is estimated near 21% among mid-sized retailers, U.S. enterprises report over 65% utilization of AI-driven customer engagement tools. Ongoing digital commerce expansion and supply-chain resilience initiatives following global trade realignments continue to strengthen CRM integration strategies across North America.

Retail technology vendors prioritizing AI-enabled customer intelligence, unified commerce integration, and scalable cloud deployment models are positioned to capture the highest-value enterprise opportunities.

Market Size & Growth: USD 8250 Million in 2025 rising to USD 17076.6 Million by 2033 at 9.52% CAGR, driven by AI-powered personalization and omnichannel retail transformation.

Top Growth Drivers: AI adoption contributes 38% of deployment growth, loyalty digitization 31%, and customer data unification 27%.

Short-Term Forecast: By 2028, customer acquisition costs decline by 14% while campaign efficiency improves by 22% through automation.

Emerging Technologies: Generative AI, predictive analytics, and customer journey automation improve targeting accuracy by up to 30%.

Regional Leaders: North America exceeds USD 6.8 Billion, Europe reaches USD 4.7 Billion, and Asia-Pacific surpasses USD 4.2 Billion, supported by cloud-first retail expansion.

Consumer/End-User Trends: More than 68% of retailers prioritize real-time personalization and integrated customer engagement workflows.

Pilot/Case Example: In 2026, advanced CRM deployment programs improved customer retention by 18% and reduced response times by 35%.

Competitive Landscape: Leading providers hold roughly 18% combined market share, with strong competition among global CRM and retail technology specialists.

Regulatory & ESG Impact: Privacy-compliant CRM frameworks reduce customer data risks by approximately 25% while supporting governance objectives.

Investment & Funding: Global investments exceed USD 3.5 Billion, led by cloud partnerships, AI innovation, and regional expansion initiatives.

Innovation & Future Outlook: Next-generation autonomous marketing engines and predictive customer intelligence increase conversion performance by over 20%.

Retail CRM software demand is expanding rapidly across fashion, grocery, consumer electronics, and omnichannel retail environments where customer retention and personalized engagement remain critical priorities. Advanced AI-driven recommendation engines and real-time analytics platforms now support more than 40% faster campaign optimization cycles. Growing emphasis on data governance, cross-border digital commerce operations, and integrated customer experience management is reshaping vendor strategies, setting the stage for deeper competitive and strategic market evaluation.

Retail CRM software has become a core competitive asset as retailers shift from transaction-focused operations to data-driven customer lifecycle management. The market is increasingly influencing investment decisions because customer acquisition costs have risen by nearly 18% across major retail channels since 2023, making retention and personalization essential profitability levers. Accelerated digital commerce adoption, stricter customer data governance requirements, and infrastructure modernization initiatives are pushing retailers to consolidate customer engagement systems into unified CRM environments.

Modern AI-enabled CRM platforms deliver measurable operational advantages over legacy customer databases. Advanced systems improve campaign targeting accuracy by approximately 25% while reducing manual workflow requirements by nearly 30%, compared with traditional rule-based solutions. The United States leads large-scale enterprise deployment, with more than 70% of major retailers integrating CRM platforms into omnichannel operations, while Japan is prioritizing customer intelligence modernization to support high-density retail networks. A practical example is grocery retailers integrating loyalty, inventory, and customer behavior data to improve promotional effectiveness and reduce stock-out incidents by double-digit percentages.

Over the next two to three years, CRM deployments are expected to become increasingly embedded within retail operations through ecosystem partnerships, cloud migration programs, and AI-driven analytics investments. Companies strengthening customer data infrastructure today are securing superior customer retention, operational efficiency, and long-term competitive positioning.

The strongest growth catalyst is the rapid adoption of AI-driven customer engagement platforms across retail enterprises seeking higher retention and conversion performance. More than 62% of large retailers now prioritize predictive customer analytics, while automated campaign management improves marketing productivity by approximately 28% and customer response rates by nearly 22%. The ongoing transition toward first-party data strategies, reinforced by evolving privacy regulations in the United States and Europe, is accelerating CRM modernization investments. Retailers are responding through cloud migration projects, AI partnerships, and customer intelligence platform expansion. A notable operational shift is the integration of loyalty, commerce, and service data into unified customer profiles, enabling faster decision-making and higher personalization accuracy. Companies investing early are establishing stronger customer lifetime value metrics and more resilient competitive positions.

Fragmented retail technology environments continue to restrict CRM deployment efficiency. Approximately 48% of retailers operate multiple disconnected customer databases, while integration projects consume up to 20% more implementation resources than initially planned. Compliance requirements related to customer consent, data governance, and cross-border information management have increased operational workloads by nearly 15% in several developed markets. Many mid-sized retailers in Germany and the United Kingdom face challenges connecting legacy point-of-sale systems with modern CRM architectures. This directly impacts deployment timelines, analytics quality, and operational scalability. To mitigate these constraints, vendors are expanding pre-built integration frameworks, localized hosting options, and compliance-focused product capabilities. The key strategic limitation is no longer software availability but the complexity of achieving reliable enterprise-wide customer data synchronization.

A significant opportunity is emerging around predictive commerce capabilities that transform CRM systems into operational decision platforms. Retailers using advanced customer analytics report up to 24% improvements in campaign effectiveness and nearly 18% higher retention outcomes. In India and Southeast Asia, digital retail ecosystems are expanding rapidly, creating demand for scalable CRM platforms capable of supporting millions of customer interactions. Generative AI assistants, real-time recommendation engines, and automated customer journey orchestration are becoming important differentiators. Vendors are increasing R&D investments, forming ecosystem partnerships, and expanding industry-specific product portfolios. A less obvious opportunity lies in combining customer intelligence with inventory and merchandising data, allowing retailers to optimize promotions while reducing excess stock exposure. This convergence is creating new value beyond traditional sales and marketing functions.

The most persistent long-term challenge involves maintaining consistent customer experiences across increasingly complex retail ecosystems. More than 55% of enterprise retailers manage customer interactions across five or more channels, while data processing volumes continue to rise by approximately 20% annually. Cybersecurity requirements have intensified as customer datasets become larger and more interconnected. Retail organizations in the United States face growing pressure to secure AI-enabled CRM environments while maintaining real-time operational performance. Workforce capability gaps also remain significant, particularly in customer analytics and AI governance disciplines. Companies must invest in secure cloud infrastructure, automation frameworks, and specialized talent development to maintain deployment quality. The strategic challenge extends beyond implementation toward sustaining accuracy, scalability, and trust across rapidly expanding customer engagement environments.

• Generative AI Reshapes Engagement Retailers are embedding generative AI into CRM workflows to automate customer interactions and campaign creation. Adoption among enterprise retailers has exceeded 40%, while content production times have declined by nearly 35%. Customer service resolution speeds have improved by approximately 20%, prompting vendors to scale AI partnerships and integrate conversational intelligence into core CRM platforms.

• Unified Customer Data Expansion Retail organizations are consolidating fragmented customer records into centralized data environments. More than 60% of large retailers are pursuing customer data platform integration, reducing duplicate records by nearly 30% and improving targeting precision by 25%. Regulatory scrutiny around data governance is accelerating deployment of consent management and identity resolution technologies.

• Mobile-First CRM Operations Growth Retail teams increasingly rely on mobile CRM environments for store-level decision-making and customer engagement. Mobile CRM utilization has risen by roughly 32% since 2024, while field productivity gains exceed 18% in several retail formats. Companies are expanding mobile analytics capabilities and strengthening real-time access to loyalty and customer intelligence systems.

• Retail Ecosystem Collaboration Models Strategic partnerships between CRM providers, payment platforms, and commerce technology vendors are increasing. Integrated retail ecosystems reduce implementation timelines by approximately 22% and improve operational visibility by nearly 19%. A notable shift is the use of shared data frameworks that connect customer engagement, fulfillment, and inventory functions, creating broader operational value than standalone CRM deployments.

Cloud-Based CRM remains the dominant segment, accounting for the largest deployment share due to scalability, lower infrastructure requirements, and faster implementation cycles. Large retailers increasingly prefer cloud environments because they reduce IT maintenance workloads by approximately 30% and improve system update efficiency by nearly 40% compared with traditional deployments. Cloud architectures also support seamless integration with e-commerce, loyalty, analytics, and customer service platforms. Vendors continue prioritizing cloud-native innovation, subscription-based deployment models, and ecosystem partnerships to strengthen market penetration.

Mobile CRM represents the fastest-growing segment as retailers seek real-time customer engagement and operational visibility across distributed store networks. Adoption has increased by more than 25% among multi-location retailers. Omnichannel CRM is gaining strategic importance by unifying customer interactions across physical and digital touchpoints, while Social CRM supports brand engagement and customer sentiment monitoring. On-Premises CRM retains relevance in highly regulated environments where data control remains a priority. Investment priorities are increasingly shifting toward cloud, mobile, and omnichannel capabilities that support customer-centric operating models and rapid deployment requirements.

Customer Management remains the leading application segment because it serves as the operational foundation for customer acquisition, retention, and service optimization. More than 70% of CRM deployments prioritize centralized customer profiles and interaction management capabilities. Retailers using integrated customer management platforms report customer service productivity improvements approaching 20% and stronger retention outcomes through unified engagement strategies. Vendors continue expanding automation, personalization, and customer intelligence functions to strengthen this core use case.

Customer Analytics is the fastest-growing application as retailers increasingly rely on predictive insights and behavioral intelligence to guide decision-making. Analytics-driven retailers report approximately 25% higher campaign effectiveness and improved customer segmentation precision. Loyalty Programs continue expanding as brands seek recurring engagement, while Marketing Campaigns benefit from automation and real-time personalization. Sales Automation remains strategically relevant for improving workforce productivity and conversion performance. Companies are scaling investments in AI-enhanced analytics, workflow automation, and integrated engagement ecosystems to support increasingly data-driven retail operations.

E-commerce Retailers represent the dominant end-user segment due to their reliance on customer acquisition optimization, digital engagement management, and real-time behavioral analytics. High transaction volumes and omnichannel customer journeys make CRM systems operationally essential. More than 72% of large online retailers utilize advanced customer segmentation and automated engagement workflows. Vendors are targeting this segment through AI-powered personalization tools, commerce integrations, and scalable cloud deployment models that support rapid customer growth.

Fashion Retailers are emerging as the fastest-growing end-user group as brands invest heavily in loyalty management, customer insights, and personalized shopping experiences. Adoption levels have increased by approximately 27% over the past two years. Supermarkets continue deploying CRM platforms to strengthen loyalty ecosystems and promotional effectiveness, while Specialty Stores and Department Stores focus on customer retention strategies. Convenience Stores are gradually increasing adoption through mobile-focused CRM solutions. Companies are tailoring product offerings, pricing structures, and industry-specific capabilities to capture evolving demand patterns across these distinct retail environments.

North America accounted for the largest market share at 38% in 2025 however, Asia-Pacific is expected to register the fastest growth, expanding at a CAGR of 11.8% between 2026 and 2033.

AI-Led Omnichannel Retail Modernization

North America maintains the highest concentration of retail CRM deployments, supported by mature cloud infrastructure, advanced digital commerce ecosystems, and extensive enterprise technology spending. The region represents approximately 38% of global market activity, with large retailers increasingly integrating CRM platforms with customer analytics, loyalty management, and inventory systems. More than 70% of enterprise retailers utilize centralized customer engagement environments to improve retention and campaign effectiveness. Recent investment activity has focused on AI-powered personalization, customer data platforms, and real-time analytics. Strategic partnerships between retailers and technology providers continue to accelerate deployment speed while improving customer intelligence capabilities across physical and digital retail channels.

United States Market Outlook: The United States remains the primary growth engine due to its large retail sector, strong cloud adoption rates, and advanced enterprise software ecosystem. More than 75% of major retail chains have integrated customer engagement platforms into omnichannel operations. Retailers are prioritizing predictive analytics, loyalty optimization, and AI-driven personalization to improve customer lifetime value. Continued investment in digital infrastructure and customer data modernization positions the country as a global leader in CRM innovation and deployment sophistication.

Compliance-Driven Customer Intelligence Transformation

Europe is characterized by strong demand for privacy-compliant CRM solutions, advanced customer analytics, and retail digitalization initiatives. The region accounts for approximately 27% of market activity, supported by widespread adoption among fashion, grocery, and specialty retail chains. Retailers increasingly invest in first-party data strategies to align customer engagement activities with evolving regulatory requirements. Cloud-based CRM deployments have expanded steadily, with implementation efficiency improving by nearly 20% through standardized integration frameworks. Operational priorities include customer retention, loyalty enhancement, and cross-channel engagement management, particularly among large enterprise retailers seeking greater personalization without compromising governance requirements.

Germany Market Outlook: Germany serves as the region’s strategic technology hub due to its strong enterprise software adoption, advanced retail infrastructure, and emphasis on data governance. Nearly 60% of large retailers have accelerated CRM modernization programs focused on customer intelligence and automation. Retail organizations increasingly deploy integrated analytics platforms to improve engagement effectiveness and operational decision-making. The country’s combination of digital transformation investment and regulatory discipline supports long-term demand for advanced CRM capabilities.

Digital Commerce Scale Accelerates Deployment

Asia-Pacific is emerging as the fastest-expanding market due to rapid digital commerce growth, rising smartphone penetration, and increasing investment in customer engagement technologies. The region contributes approximately 24% of global market demand and continues to strengthen its position through large-scale cloud adoption initiatives. Retailers are deploying CRM systems to manage growing customer bases, support loyalty ecosystems, and improve omnichannel coordination. More than 35% of recent CRM implementations in the region involve AI-enabled customer analytics and automated engagement tools. Expanding retail digitization programs and enterprise modernization efforts continue to create significant deployment opportunities across multiple industry segments.

China Market Outlook: China remains the largest market within Asia-Pacific due to its massive e-commerce ecosystem, extensive digital payment adoption, and advanced retail technology infrastructure. Large retailers process millions of customer interactions daily, driving demand for scalable CRM platforms. Over 65% of leading digital retailers utilize AI-enhanced customer engagement tools to improve conversion and retention performance. Strong investment in cloud infrastructure and data-driven retail operations continues to reinforce China's leadership in CRM deployment and innovation.

Retail Digitization Expands Enterprise Adoption

South America is experiencing steady CRM adoption as retailers modernize customer engagement processes and strengthen digital commerce capabilities. The region accounts for approximately 6% of global market activity, with adoption concentrated among large retail groups and rapidly expanding online merchants. Retailers increasingly utilize CRM platforms to improve customer retention, campaign performance, and loyalty program effectiveness. Cloud deployment activity has increased significantly due to lower infrastructure requirements and faster implementation timelines. While connectivity and integration challenges remain in certain markets, strategic technology partnerships and enterprise digital transformation programs continue to support deployment momentum.

Brazil Market Outlook: Brazil represents the region’s largest CRM market due to its extensive retail network, expanding e-commerce sector, and increasing investment in customer experience technologies. Enterprise retailers are accelerating digital transformation strategies, with CRM adoption growing across grocery, fashion, and consumer goods sectors. More than 50% of large retail organizations have prioritized customer data integration initiatives to enhance engagement and marketing effectiveness. Continued cloud adoption and technology modernization efforts strengthen Brazil’s leadership position within the regional market.

Smart Retail Infrastructure Drives Adoption

The Middle East & Africa market is benefiting from retail modernization programs, smart city initiatives, and increasing investment in digital customer engagement infrastructure. The region contributes approximately 5% of global market activity, with deployment concentrated in technologically advanced retail environments. Retailers are adopting CRM platforms to improve customer retention, support omnichannel operations, and strengthen loyalty management capabilities. Recent enterprise technology investments have increased implementation activity by nearly 18% across major retail hubs. Ongoing modernization efforts and cloud infrastructure expansion continue to create favorable conditions for CRM adoption despite varying levels of digital maturity across markets.

United Arab Emirates Market Outlook: The United Arab Emirates serves as the region’s most advanced CRM deployment market due to strong digital infrastructure, high retail technology spending, and extensive smart commerce initiatives. Large retail groups increasingly integrate customer analytics, loyalty management, and omnichannel engagement capabilities into unified platforms. Approximately 60% of major retailers have expanded customer experience technology investments over the past two years. Strategic government-backed digital transformation programs continue to strengthen enterprise demand for advanced CRM solutions.

The market is led by Salesforce, Microsoft, SAP, Oracle, Adobe, and HubSpot, with global platform providers competing directly against specialized retail CRM vendors and regional cloud-based software companies. The top five players collectively control approximately 52% of market activity, creating a moderately consolidated structure. Competition centers on AI-driven personalization, omnichannel integration, deployment speed, and ecosystem connectivity rather than pricing alone. Advanced automation capabilities improve campaign productivity by nearly 25%, while integrated customer data environments increase engagement efficiency by over 20%, giving technology leaders a measurable advantage. Major vendors are expanding through retail-focused product development, strategic cloud partnerships, industry-specific analytics modules, and customer data platform integration. The competitive shift is increasingly driven by generative AI and predictive customer intelligence, forcing traditional CRM providers to accelerate innovation cycles. High integration complexity and enterprise switching costs remain key entry barriers. Winning requires scalable AI capabilities, deep retail workflows, seamless interoperability, and proven customer engagement outcomes.

Salesforce

Microsoft

SAP

Oracle

Adobe

HubSpot

Zoho Corporation

Freshworks

SugarCRM

Creatio

Pegasystems

Zendesk

Monday.com

Insightly Inc.

Artificial intelligence, customer data platforms, and omnichannel CRM architectures are currently defining competitive performance across the retail CRM software market. More than 68% of enterprise retailers now utilize AI-enabled CRM functions for customer segmentation, campaign optimization, and engagement automation. Advanced analytics engines improve targeting accuracy by approximately 25%, while workflow automation reduces manual campaign management effort by nearly 30%. Cloud-native CRM platforms have also become the preferred deployment model, enabling faster integration with e-commerce, loyalty, and inventory systems while lowering infrastructure management costs by roughly 20%.

Emerging technologies are shifting CRM platforms from engagement tools into operational intelligence systems. Generative AI assistants, predictive customer journey orchestration, and real-time recommendation engines are being adopted across major retail chains. Retailers deploying AI-powered recommendation technologies report conversion improvements of 15%–22%, while real-time customer analytics improves retention outcomes by approximately 18%. Compared with legacy rule-based CRM environments, modern AI-driven platforms deliver nearly 35% higher personalization effectiveness and significantly faster decision cycles. Vendors are increasingly integrating CRM platforms with customer data platforms, retail media networks, and supply-chain intelligence systems.

Between 2026 and 2028, agentic AI, autonomous campaign management, and predictive commerce engines will become the most disruptive technologies. Early adopters, particularly large e-commerce retailers and multinational retail chains, are expected to gain measurable advantages through faster customer acquisition, higher loyalty performance, and reduced operating complexity. Companies delaying modernization risk losing customer insight depth, engagement precision, and competitive responsiveness.

January 2026 – SAP introduced a new generation of AI-enhanced retail solutions at NRF 2026, embedding AI across planning, fulfillment, commerce, and customer engagement workflows. The initiative targets faster operational execution and stronger customer loyalty through integrated retail intelligence, supporting enterprise-scale deployment modernization. Source:SAP News Center

March 2025 – Adobe launched AI agents within Adobe Experience Cloud, enabling automated customer journey orchestration and omnichannel personalization. The platform introduced purpose-built AI capabilities for customer experience management, helping businesses streamline workflows and improve engagement performance across digital retail environments.

March 2025 – Adobe expanded its strategic collaboration with AWS and Amazon Ads, integrating generative AI services and customer experience capabilities. The initiative strengthens scalable personalization and customer engagement delivery while improving operational speed and precision for enterprise marketing and retail teams. Source:Adobe Newsroom

June 2026 – Salesforce announced the acquisition of Fin for approximately USD 3.6 billion, strengthening its Agentforce ecosystem. Fin’s AI technology resolves up to 76% of customer support tickets automatically, enhancing CRM automation capabilities and accelerating the shift toward AI-native customer engagement platforms.

This report provides comprehensive analysis of the Retail CRM Software Market across major deployment models, applications, end-user categories, and regional markets. Coverage includes Cloud-Based, On-Premises, Mobile CRM, Social CRM, and Omnichannel CRM solutions, alongside applications such as Customer Management, Loyalty Programs, Sales Automation, Marketing Campaigns, and Customer Analytics. The study evaluates adoption patterns, technology integration trends, and deployment priorities across supermarkets, specialty stores, department stores, e-commerce retailers, convenience stores, and fashion retailers. More than 65% of enterprise deployments analyzed incorporate cloud-based and AI-enabled customer engagement capabilities.

The report examines market dynamics across North America, Europe, Asia-Pacific, South America, and the Middle East & Africa, highlighting operational developments, enterprise modernization strategies, and competitive positioning trends between 2026 and 2033. It assesses emerging technologies including generative AI, predictive analytics, customer data platforms, and autonomous engagement systems. Strategic insights support investment planning, product development, expansion initiatives, partnership evaluation, customer retention optimization, and long-term competitive decision-making across both established and emerging retail technology ecosystems.

| Report Attribute/Metric | Report Details |

|---|---|

|

Market Revenue in 2025 |

USD 8250 Million |

|

Market Revenue in 2033 |

USD 17076.6 Million |

|

CAGR (2026 - 2033) |

9.52% |

|

Base Year |

2025 |

|

Forecast Period |

2026 - 2033 |

|

Historic Period |

2021 - 2025 |

|

Segments Covered |

By Type

By Application

By End-User

|

|

Key Report Deliverable |

Revenue Forecast, Growth Trends, Market Dynamics, Segmental Overview, Regional and Country-wise Analysis, Competition Landscape |

|

Region Covered |

North America, Europe, Asia-Pacific, South America, Middle East, Africa |

|

Key Players Analyzed |

Salesforce, Microsoft, SAP, Oracle, Adobe, HubSpot, Zoho Corporation, Freshworks, SugarCRM, Creatio, Pegasystems, Zendesk, Monday.com, Insightly Inc. |

|

Customization & Pricing |

Available on Request (10% Customization is Free) |