Reports

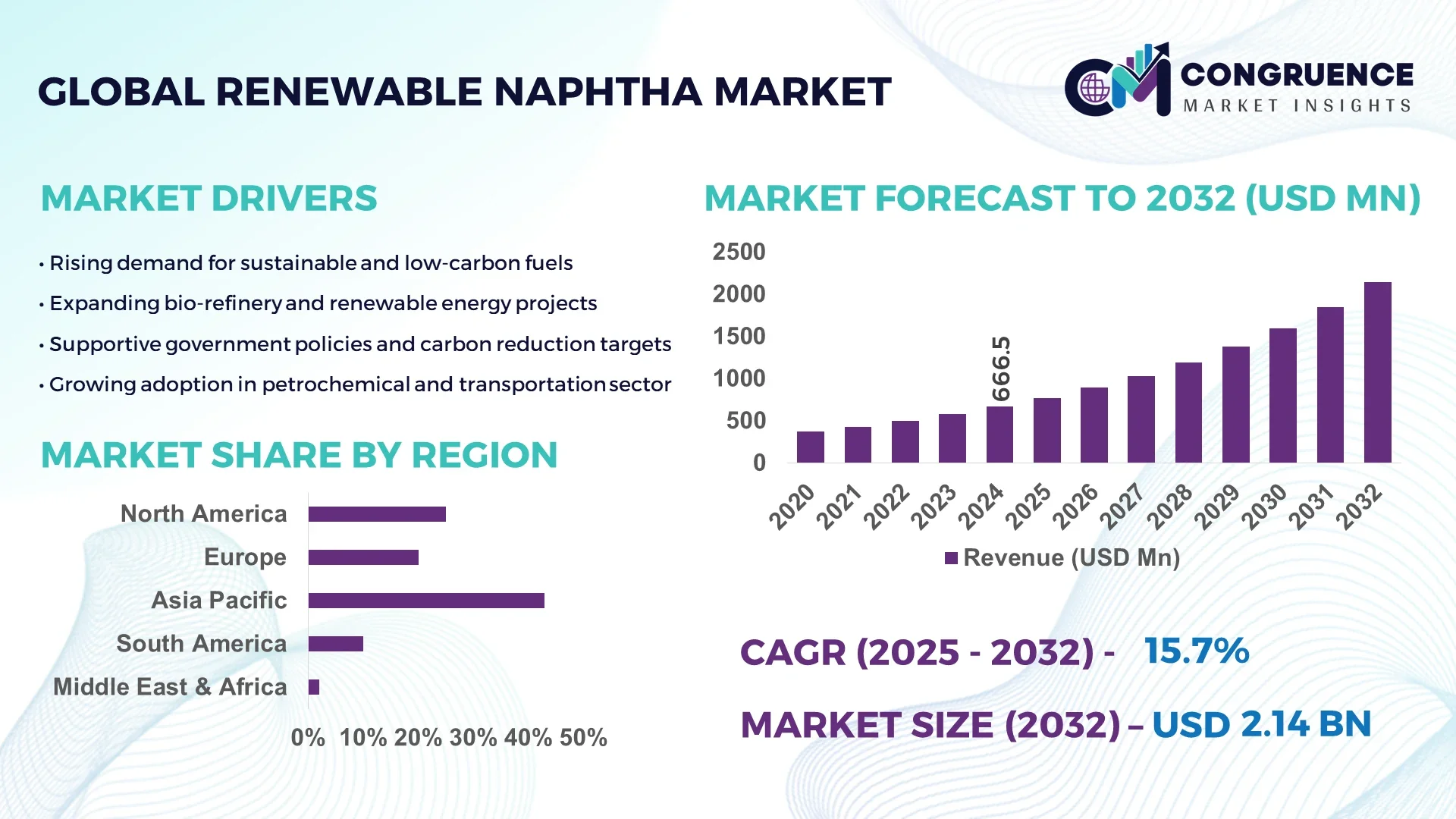

The Global Renewable Naphtha Market was valued at USD 666.51 Million in 2024 and is anticipated to reach a value of USD 2,140.3 Million by 2032 expanding at a CAGR of 15.7% between 2025 and 2032. The market’s growth is driven by increasing renewable fuel integration across petrochemical, transportation, and energy sectors.

Japan leads the global renewable naphtha market with advanced refinery infrastructure and significant investments in bio-based fuel technologies. The country’s renewable naphtha production capacity surpassed 120 kilotons in 2024, supported by continuous R&D in hydrotreated vegetable oil (HVO) and waste-based feedstocks. Major Japanese energy firms have expanded their renewable fuel blending facilities, while applications in plastics and green hydrogen sectors are accelerating adoption. Government-backed decarbonization programs have further strengthened domestic production ecosystems, ensuring stable supply to downstream industries.

• Market Size & Growth: The market was valued at USD 666.51 Million in 2024 and is projected to reach USD 2,140.3 Million by 2032, expanding at a CAGR of 15.7%, driven by rising demand for sustainable alternatives in petrochemicals and transportation fuels.

• Top Growth Drivers: 48% increase in renewable fuel adoption, 35% efficiency improvement in feedstock conversion, and 41% rise in downstream applications across chemical manufacturing.

• Short-Term Forecast: By 2028, production efficiency is expected to improve by 22%, while operational costs may decline by up to 18% due to optimized refinery processes.

• Emerging Technologies: Advancements in hydroprocessing catalysts, co-processing techniques, and biomass gasification are shaping production scalability and cost efficiency.

• Regional Leaders: Asia-Pacific projected to reach USD 970 Million by 2032 with strong industrial adoption; Europe to hit USD 680 Million led by regulatory mandates; North America expected to reach USD 310 Million with rapid refinery upgrades.

• Consumer/End-User Trends: High uptake observed in petrochemical, automotive, and aviation sectors due to compatibility with existing infrastructure and regulatory alignment with low-carbon initiatives.

• Pilot or Case Example: In 2024, Neste launched a pilot renewable naphtha co-processing project achieving a 27% carbon reduction in feedstock utilization.

• Competitive Landscape: Neste Corporation leads with approximately 31% market share, followed by Honeywell UOP, ENEOS Corporation, TotalEnergies, and Repsol.

• Regulatory & ESG Impact: Stringent carbon reduction mandates and renewable fuel blending targets across Europe and Asia are accelerating production transitions and technology investments.

• Investment & Funding Patterns: Over USD 1.8 Billion invested in 2023–2024 across bio-refinery expansions and technology partnerships, emphasizing sustainable energy diversification.

• Innovation & Future Outlook: The market is witnessing integration of AI-driven process optimization, modular refinery designs, and expanding circular economy collaborations aimed at reducing lifecycle emissions.

The renewable naphtha market is increasingly influenced by advancements in feedstock flexibility, catalytic upgrading, and bio-refining technologies across key sectors including petrochemicals, automotive, and aviation. Innovations in process efficiency and reduced lifecycle emissions are improving cost-competitiveness and environmental performance. Regional consumption growth is led by Asia-Pacific and Europe, driven by industrial decarbonization mandates and increased consumer demand for sustainable materials. The market outlook remains robust, supported by regulatory incentives, corporate sustainability goals, and expanding R&D investments targeting next-generation bio-based fuels and green chemical applications.

The strategic relevance of the Renewable Naphtha Market lies in its capacity to redefine the global energy and chemical supply chains by enabling a sustainable substitute for fossil-derived naphtha. As industries accelerate decarbonization, renewable naphtha provides a critical pathway to achieving circular economy goals through low-carbon feedstock integration. Advanced hydroprocessing technology delivers up to 35% improvement in conversion efficiency compared to traditional refining processes, substantially reducing lifecycle emissions. Asia-Pacific dominates in production volume, while Europe leads in adoption with over 52% of enterprises actively integrating renewable naphtha in downstream operations.

By 2028, AI-enabled process automation and predictive refinery analytics are expected to improve operational efficiency by 24% and reduce feedstock waste by 18%. Firms are committing to ESG metrics targeting a 40% reduction in carbon emissions and 25% recycling of by-products by 2030. In 2024, Finland’s Neste Corporation achieved a 32% reduction in production-related CO₂ emissions through an AI-optimized hydrotreatment system. Such advancements highlight the sector’s transition toward a data-driven, technology-centric growth framework.

Looking forward, the Renewable Naphtha Market will evolve as a central pillar of industrial resilience, compliance alignment, and sustainable growth. Its role in bridging renewable energy inputs with circular production systems positions it as a cornerstone of global low-carbon transformation.

The expansion of bio-refinery infrastructure is a major driver propelling the Renewable Naphtha Market. Global capacity additions reached approximately 6 million tons in 2024, led by new projects in Japan, the Netherlands, and the United States. These facilities employ hydrotreated vegetable oil (HVO) and advanced waste-to-fuel technologies, enabling higher output efficiency and broader feedstock flexibility. As a result, production efficiency has improved by nearly 28% compared to conventional refinery setups. Governments are incentivizing large-scale integration through renewable blending mandates and carbon credit programs. The development of modular and scalable bio-refineries is further enabling decentralized production, reducing logistics costs and enhancing accessibility across industrial sectors such as plastics, coatings, and green fuels.

High production costs and inconsistent feedstock quality remain critical restraints in the Renewable Naphtha Market. The average cost of producing renewable naphtha remains 20–30% higher than that of conventional petroleum-based alternatives due to limited economies of scale and expensive hydrogen processing systems. Moreover, the variability in feedstock—ranging from used cooking oil to algae—impacts yield consistency and process stability. Supply chain complexities, including limited access to sustainable biomass and the high cost of feedstock transportation, add to financial pressure. Additionally, refining technologies such as hydro-deoxygenation and catalytic cracking require continuous maintenance investments, further affecting profitability. These cost disparities challenge market competitiveness, especially in regions with weaker renewable policy incentives or limited biofuel infrastructure.

Technological innovation and global decarbonization policies are unlocking substantial opportunities in the Renewable Naphtha Market. Advancements in catalytic hydroprocessing and co-processing techniques now allow renewable naphtha to be produced with up to 40% lower carbon intensity compared to fossil-based alternatives. By 2030, several nations aim to integrate at least 10% renewable feedstock into petrochemical operations, creating long-term demand stability. The emergence of bio-based circular economy projects, particularly in Europe and Asia, provides new pathways for product diversification. Growing alignment between industrial decarbonization targets and renewable fuel incentives encourages public-private collaborations, spurring innovation funding and infrastructure modernization. These opportunities are expected to foster sustainable value creation across end-use sectors including automotive, aviation, and polymers.

Complex certification procedures and inconsistent regulatory frameworks across regions present major challenges to the Renewable Naphtha Market. Producers face difficulties aligning with multiple sustainability standards such as ISCC, RED II, and ASTM guidelines, leading to extended compliance timelines and higher administrative costs. Disparities between regional carbon credit valuation and renewable blending targets create uncertainty in investment returns. In 2024, nearly 37% of renewable fuel producers reported delays in project execution due to regulatory bottlenecks. Moreover, cross-border trade barriers and varying bio-content verification requirements hinder market fluidity. To sustain growth, uniform certification systems and global recognition of renewable naphtha standards are essential to streamline operations and attract broader industrial participation.

• Expansion of Co-Processing Technologies in Refineries: Global refineries are increasingly integrating co-processing technologies that allow renewable and fossil feedstocks to be treated simultaneously. By 2024, over 60% of newly commissioned refineries incorporated co-processing systems, achieving an average carbon reduction of 28%. This shift is significantly improving production flexibility while minimizing feedstock dependency, particularly across Asian and European markets where refining efficiency and low-emission mandates are key priorities.

• Growth in Waste-to-Naphtha Conversion Initiatives: The utilization of waste-derived feedstocks for renewable naphtha production has risen sharply, with waste-based inputs accounting for nearly 35% of total production volume in 2024. Advanced pyrolysis and gasification units have enabled up to 40% yield efficiency improvement compared to first-generation biofuel methods. North America and Japan are leading in the deployment of these technologies, which align with national recycling and waste valorization goals.

• Increased Adoption of Digital Refinery Management Systems: The integration of digital monitoring and AI-driven optimization tools has grown by 47% among major renewable naphtha producers. Predictive analytics and process automation are helping reduce operational downtime by 22% and energy consumption by 15%. These digital solutions enhance production reliability and ensure compliance with stringent emission regulations across refineries in Europe and Southeast Asia.

• Shift Toward Renewable Feedstock Diversification: Feedstock diversification has become a strategic focus, with second-generation biomass, algae, and used cooking oil now comprising 48% of renewable naphtha inputs. Producers are expanding partnerships with agricultural and industrial sectors to secure sustainable supply chains. This diversification has contributed to a 30% reduction in production volatility and increased resilience against price fluctuations, reinforcing long-term market stability.

The Renewable Naphtha Market is segmented based on type, application, and end-user, reflecting its growing integration into multiple industrial value chains. In terms of type, the market is divided into hydrotreated vegetable oil (HVO)-based naphtha, Fischer-Tropsch (FT) naphtha, and waste-derived naphtha, each demonstrating distinct feedstock efficiencies and emission profiles. By application, renewable naphtha finds increasing use in petrochemicals, fuel blending, and hydrogen production, driven by the transition toward circular and low-carbon manufacturing processes. End-user segmentation reveals strong participation from the chemical, automotive, and energy industries, where demand for sustainable feedstocks and regulatory compliance are key adoption motivators. This diversified segmentation ensures balanced growth across upstream and downstream markets, enhancing overall resilience and innovation potential.

HVO-based renewable naphtha dominates the market, accounting for approximately 46% of total production in 2024, attributed to its high compatibility with existing refinery infrastructure and its low sulfur content. Fischer-Tropsch naphtha holds around 31% share, benefiting from steady advancements in synthetic fuel technology. However, waste-derived naphtha represents the fastest-growing segment, projected to expand at a 16.4% CAGR due to rising circular economy initiatives and technological progress in waste-to-fuel conversion. Collectively, other emerging types—including algae-based and lignocellulosic naphtha—contribute around 23% share, primarily serving niche applications in bio-based plastics and specialty chemicals.

Petrochemical feedstock applications dominate the Renewable Naphtha Market, representing nearly 52% of total consumption in 2024, supported by robust demand for sustainable inputs in ethylene and propylene production. Fuel blending applications account for 28% and are expected to rise as renewable naphtha gains acceptance in aviation and marine fuels. Hydrogen production applications currently hold 20% but are expanding fastest, growing at an estimated 17.1% CAGR as nations scale low-emission hydrogen infrastructure.

Other emerging uses, including packaging materials and renewable solvents, together contribute around 10% of demand. This trend reflects increasing interest in replacing fossil-based intermediates across industrial chemistry chains.

The chemical industry leads the Renewable Naphtha Market, accounting for approximately 49% of total end-user adoption in 2024, driven by strong demand for renewable raw materials in polymer and olefin production. The energy sector follows with 33%, primarily leveraging renewable naphtha for sustainable fuel blending and green hydrogen production. The automotive industry, representing around 18%, is the fastest-growing segment, projected to expand at a 15.8% CAGR as electric vehicle manufacturers and OEMs integrate low-carbon materials in production chains.

Other end-users, including packaging, construction, and coatings sectors, collectively contribute about 12%, with growing interest in bio-based inputs to meet ESG commitments.

Asia-Pacific accounted for the largest market share at 43% in 2024; however, Europe is expected to register the fastest growth, expanding at a CAGR of 16.2% between 2025 and 2032.

Asia-Pacific’s dominance stems from robust refinery capacity exceeding 4.2 million tons and significant investments in renewable energy projects across Japan, China, and India. Europe follows with 31% share, driven by strict emission regulations and advanced R&D programs supporting sustainable fuels. North America held a 17% share, bolstered by technological innovations in bio-refinery automation. South America and the Middle East & Africa collectively represented 9% share, supported by emerging waste-to-fuel projects and green policy initiatives. The regional landscape reflects rising government-backed decarbonization targets, growing feedstock diversity, and expansion of renewable fuel blending mandates across industrial and transportation sectors.

North America held approximately 17% of the global Renewable Naphtha Market in 2024, supported by strong adoption in petrochemicals, aviation, and automotive sectors. The U.S. and Canada have implemented renewable fuel standards and carbon reduction initiatives, spurring demand across integrated refineries. Technological advancements such as AI-based refinery optimization and feedstock traceability platforms have enhanced process efficiency by nearly 18%. Local players like Chevron are investing in renewable hydrocarbon facilities that produce naphtha from biogenic sources. Consumer behavior in the region shows higher enterprise adoption in energy, logistics, and construction sectors, reflecting a strong focus on sustainability and carbon accountability.

Europe accounted for around 31% of the Renewable Naphtha Market in 2024, with major contributors including Germany, France, and the United Kingdom. The European Commission’s decarbonization frameworks and renewable energy directives have accelerated the replacement of fossil-based naphtha with sustainable alternatives. Advanced catalytic conversion and co-processing systems are increasingly adopted in refineries, enabling a 26% improvement in energy efficiency. Leading companies such as TotalEnergies and Repsol are investing in dedicated renewable fuel complexes. European consumers are particularly responsive to ESG compliance, with over 58% of industrial buyers prioritizing low-carbon raw materials in procurement, further reinforcing market maturity and innovation adoption.

Asia-Pacific dominated the Renewable Naphtha Market in 2024, with a total consumption volume exceeding 2.3 million tons. Japan, China, and India are the top consuming nations, leveraging strong petrochemical and automotive manufacturing bases. The region’s rapid investment in digitalized bio-refineries and AI-integrated hydroprocessing units has improved feedstock conversion efficiency by 32%. Japanese and South Korean producers are leading pilot projects integrating circular waste feedstocks. Regional consumer behavior reflects growing sustainability awareness and preference for locally produced renewable fuels. Infrastructure expansion, supported by national decarbonization targets, continues to position Asia-Pacific as the innovation hub for renewable naphtha deployment.

South America accounted for nearly 6% of the global Renewable Naphtha Market in 2024, led by Brazil and Argentina. Expanding bio-refinery capacities, particularly those processing sugarcane and agricultural residues, are improving regional fuel self-sufficiency. Brazil’s renewable blending mandates and Argentina’s green energy tax incentives have strengthened local investment in advanced hydrotreated naphtha facilities. Regional players are focusing on waste valorization technologies, achieving up to 21% yield efficiency improvement. Consumer adoption patterns reveal strong support from industrial sectors, especially in transportation and energy, aligning with broader sustainability transitions within the Latin American energy ecosystem.

The Middle East & Africa accounted for 3% of the Renewable Naphtha Market in 2024, primarily driven by UAE, Saudi Arabia, and South Africa. Demand is growing within the petrochemical and construction sectors, supported by renewable integration in refinery modernization projects. The region has witnessed an 18% increase in public-private partnerships focusing on bio-refinery development and waste-to-fuel initiatives. Companies in the UAE are piloting solar-assisted hydroprocessing systems to reduce operational emissions by 20%. Consumer behavior reflects gradual but steady acceptance of low-carbon industrial feedstocks, particularly in export-oriented manufacturing and downstream energy industries.

• Japan – 24% Market Share: Dominance attributed to advanced refinery infrastructure, significant investments in hydrogen-integrated naphtha production, and early adoption of bio-feedstock conversion technologies.

• Germany – 18% Market Share: Strong regulatory backing for renewable fuel use in chemical and transport industries, coupled with industry-wide implementation of carbon reduction technologies in refineries.

The competitive environment in the Renewable Naphtha Market is moderately consolidated yet rapidly evolving, with around 35 to 40 active global competitors engaged in production, feedstock integration, and downstream distribution. The top 5 companies collectively hold approximately 63% of the global market share, reflecting a high concentration of capacity and technological expertise. Leading players have pursued strategic initiatives such as refinery conversions, joint ventures, co-processing licensing, and long-term supply agreements to expand their renewable portfolios.

Innovation remains a core competitive differentiator, with firms investing in advanced hydroprocessing of waste and bio-feedstocks, digital refinery optimization, and certification systems for renewable content tracking. For instance, several participants are scaling modular bio-refinery platforms and forming alliances with catalyst technology providers to enhance process efficiency. Moreover, ongoing mergers and acquisitions indicate a shift toward vertical integration, enabling companies to secure sustainable raw materials and expand into downstream petrochemical applications.

Overall, the market reflects a balance between established energy leaders and emerging biofuel specialists, where cost optimization, scalability, and feedstock flexibility are shaping competitive positioning. Decision-makers should expect intensified rivalry as new entrants capitalize on regional policy incentives, circular-economy initiatives, and low-carbon fuel mandates driving renewable naphtha adoption globally.

Chevron Corporation

UPM Biofuels

ENI S.p.A.

Technological advancements are playing a decisive role in transforming the Renewable Naphtha Market, with innovations targeting feedstock flexibility, process efficiency, and carbon footprint reduction. The most widely adopted production technologies include hydrotreated vegetable oil (HVO) refining, biomass-to-liquid (BTL) conversion, and co-processing technologies that allow bio-feedstocks to be processed alongside fossil feedstocks in existing refineries. Approximately 68% of operational renewable naphtha capacity in 2024 utilized hydroprocessing routes due to their compatibility with conventional refinery infrastructure and cost-effective scalability.

Emerging technologies are increasingly focused on bio-waste valorization and synthetic fuel synthesis. Pyrolysis and gasification technologies are now enabling conversion of municipal solid waste, agricultural residues, and algae biomass into renewable naphtha precursors, cutting lifecycle greenhouse gas emissions by up to 80% compared to fossil alternatives. Meanwhile, advancements in carbon capture integration and catalyst optimization have improved yield efficiency by nearly 12–15%, reducing production costs and improving sustainability metrics across the supply chain.

Digitalization is another major technology trend, with over 45% of top manufacturers adopting AI-driven process controls, predictive maintenance, and real-time analytics to optimize throughput and energy use. Furthermore, modular biorefinery systems and electrolysis-based synthesis routes are gaining traction, enabling decentralized production models that align with circular economy goals. These technologies collectively enhance operational flexibility, allowing producers to adapt to variable feedstock availability and evolving environmental standards. For decision-makers, technological readiness and digital integration are emerging as key differentiators defining long-term competitiveness in the renewable naphtha landscape.

The Renewable Naphtha Market Report provides a comprehensive evaluation of the industry landscape, encompassing segmentation by type, application, and end-user, along with in-depth regional and technological analyses. The study covers both conventional and emerging renewable naphtha production pathways, including hydrotreated vegetable oil (HVO), biomass-to-liquid (BTL), and co-processing technologies that collectively account for over 90% of global output in 2024.

Geographically, the report examines five major regions—North America, Europe, Asia-Pacific, South America, and the Middle East & Africa—capturing both mature markets with established biorefinery infrastructure and rapidly industrializing economies driving biofuel adoption. It highlights varying market dynamics, such as high bio-feedstock utilization in Europe and rapid capacity expansions in Asia-Pacific.

In terms of applications, the scope extends across plastics, petrochemical feedstocks, transportation fuels, and specialty chemicals, representing the primary demand drivers for renewable naphtha integration. The report further outlines the competitive environment, featuring over 25 active industry participants, and details technological progress in catalyst innovation, feedstock optimization, and digital monitoring systems.

Additionally, the analysis explores niche segments, such as waste-to-naphtha conversion and bio-aromatic synthesis, emphasizing their role in circular economy transitions. Overall, the report offers a holistic assessment of the market’s strategic direction, focusing on sustainability targets, production efficiency, and global regulatory frameworks shaping the renewable naphtha industry’s evolution through 2032.

| Report Attribute/Metric | Report Details |

|---|---|

Market Revenue in 2024 | USD 666.51 Million |

Market Revenue in 2032 | USD 2140.3 Million |

CAGR (2025 - 2032) | 15.7% |

Base Year | 2024 |

Forecast Period | 2025 - 2032 |

Historic Period | 2020 - 2024 |

Segments Covered | By Types

By Application

By End-User

|

Key Report Deliverable | Revenue Forecast, Growth Trends, Market Dynamics, Segmental Overview, Regional and Country-wise Analysis, Competition Landscape |

Region Covered | North America, Europe, Asia-Pacific, South America, Middle East, Africa |

Key Players Analyzed | Neste Oyj, TotalEnergies SE, Repsol S.A., Chevron Corporation, UPM Biofuels, ENI S.p.A. |

Customization & Pricing | Available on Request (10% Customization is Free) |