Reports

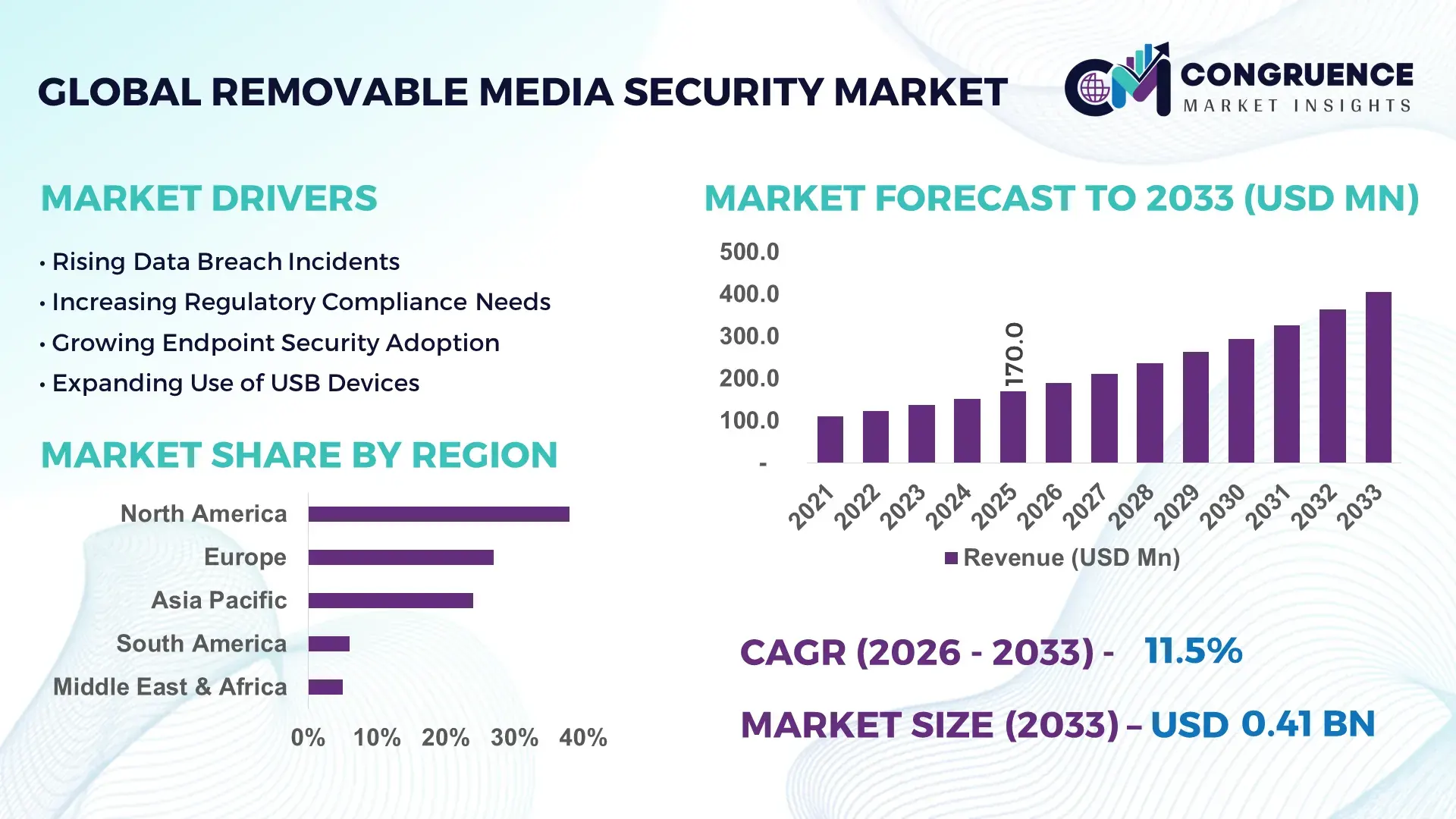

The Global Removable Media Security Market was valued at USD 170.0 Million in 2025 and is anticipated to reach a value of USD 406.1 Million by 2033 expanding at a CAGR of 11.5% between 2026 and 2033, according to an analysis by Congruence Market Insights. This growth is primarily driven by increasing cybersecurity threats linked to unauthorized data transfer via USB devices and external storage media.

The United States leads the removable media security landscape with over 42% enterprise-level adoption of endpoint data loss prevention tools integrated with removable media controls. More than 68% of Fortune 500 companies have implemented USB port control and encryption enforcement solutions. The country has witnessed over USD 2.5 billion cumulative investments in endpoint security technologies between 2022 and 2025. Key industries such as defense, BFSI, and healthcare account for nearly 55% of total deployment, with government agencies enforcing strict removable media policies under federal cybersecurity mandates. Advanced solutions leveraging AI-based anomaly detection have improved threat identification accuracy by over 35%, while cloud-managed removable media security platforms are adopted by 47% of large enterprises.

Market Size & Growth: USD 170.0 Million in 2025, projected to reach USD 406.1 Million by 2033 at 11.5% CAGR, driven by rising endpoint security risks.

Top Growth Drivers: 72% increase in USB-based cyber threats, 64% enterprise compliance adoption, 58% growth in remote workforce usage.

Short-Term Forecast: By 2028, organizations are expected to reduce unauthorized data transfer incidents by 38%.

Emerging Technologies: AI-driven threat detection, zero-trust endpoint security, blockchain-based device authentication.

Regional Leaders: North America (~USD 150M by 2033), Europe (~USD 110M), Asia-Pacific (~USD 95M), with varying regulatory-driven adoption.

Consumer/End-User Trends: BFSI and healthcare sectors contribute over 48% usage due to sensitive data handling requirements.

Pilot or Case Example: In 2025, a healthcare provider reduced data breach incidents by 41% using AI-enabled removable media monitoring tools.

Competitive Landscape: Leader holds ~18% share, followed by 4–5 key players maintaining strong global presence.

Regulatory & ESG Impact: Data protection laws drive over 62% adoption in regulated industries.

Investment & Funding Patterns: Over USD 900M invested in endpoint security startups between 2023–2025.

Innovation & Future Outlook: Integration with cloud security and zero-trust architectures will define next-gen solutions.

Key industry sectors such as BFSI (28%), healthcare (20%), and government (18%) dominate demand, driven by strict compliance requirements. Innovations in AI-based anomaly detection and encrypted USB management systems have improved threat response efficiency by over 35%. Regulatory mandates and rising remote work trends continue to accelerate adoption globally, while Asia-Pacific is witnessing over 40% enterprise digitization, shaping future demand and innovation pathways.

The Removable Media Security Market holds strong strategic importance in modern cybersecurity frameworks, particularly as organizations increasingly rely on portable storage devices for data transfer across distributed work environments. With over 65% of enterprises reporting at least one removable media-related security incident annually, the need for robust control mechanisms has intensified. Advanced endpoint protection solutions now integrate AI-powered monitoring tools that analyze user behavior, improving threat detection efficiency by over 40%.

Zero-trust security frameworks are becoming a foundational strategy, where removable media access is granted only after strict verification protocols. Compared to traditional signature-based detection systems, AI-driven behavioral analytics delivers 37% improvement in identifying anomalous activities. North America dominates in volume, while Asia-Pacific leads in adoption with over 52% of enterprises actively implementing next-generation endpoint security solutions.

By 2028, AI-integrated removable media security platforms are expected to reduce insider threat incidents by nearly 33%, significantly improving data governance metrics. Firms are committing to ESG targets, including reducing electronic waste by 25% through controlled device lifecycle management and secure disposal protocols by 2030.

In 2025, a major US-based defense contractor achieved a 45% reduction in unauthorized data transfers by deploying AI-enabled USB control systems with real-time monitoring. Such micro-level implementations demonstrate measurable efficiency gains and regulatory compliance adherence.

Looking ahead, the Removable Media Security Market is set to become a critical pillar of enterprise resilience, ensuring compliance, enhancing data protection, and supporting sustainable digital transformation across industries.

The Removable Media Security Market is influenced by the rapid rise in data mobility, increasing cyber threats, and strict regulatory frameworks governing data protection. Over 70% of organizations now allow some form of external device usage, increasing the attack surface significantly. This has led to a surge in demand for advanced endpoint security solutions that monitor and control data flow through USB devices, external hard drives, and other portable storage mediums. The market is also witnessing increased integration with cloud security platforms, enabling centralized management across distributed enterprise environments. Furthermore, industries such as healthcare, BFSI, and government are prioritizing removable media security to safeguard critical information assets, driving continuous innovation and adoption of intelligent monitoring systems.

The increasing frequency of cyberattacks originating from removable media devices is a primary driver of market growth. Studies indicate that nearly 72% of malware infections in isolated or air-gapped systems originate from USB devices. Additionally, over 60% of organizations have reported data leakage incidents linked to unauthorized use of removable storage. Industries such as defense and energy, where air-gapped systems are common, are particularly vulnerable. The growing sophistication of threats, including ransomware and insider attacks, has pushed enterprises to deploy advanced removable media control solutions with real-time monitoring and encryption capabilities. Furthermore, compliance mandates such as data protection regulations have forced organizations to strengthen endpoint security, contributing significantly to increased adoption rates.

Despite growing demand, the complexity associated with deploying and managing removable media security solutions remains a key restraint. Around 48% of small and medium enterprises report challenges in integrating these solutions with existing IT infrastructure. Compatibility issues with legacy systems, high configuration requirements, and the need for continuous monitoring create operational challenges. Additionally, over 35% of IT teams face difficulties in managing policy enforcement across diverse endpoints, especially in hybrid work environments. User resistance due to restricted device access further complicates adoption. These factors collectively slow down implementation, particularly in cost-sensitive industries, limiting widespread deployment despite increasing security concerns.

The integration of artificial intelligence into removable media security solutions presents significant growth opportunities. AI-based systems can analyze user behavior patterns and detect anomalies with over 40% higher accuracy compared to traditional methods. Approximately 57% of enterprises are exploring AI-driven endpoint security solutions to enhance threat detection capabilities. The rise of remote work and cloud-based operations has further increased demand for intelligent, scalable solutions. Additionally, the adoption of zero-trust architectures is creating new opportunities for vendors to develop advanced authentication and access control mechanisms. Emerging markets, particularly in Asia-Pacific, are witnessing rapid digital transformation, providing a strong foundation for future market expansion.

The rapid evolution of cyber threats poses a significant challenge to the removable media security market. Advanced persistent threats (APTs) and fileless malware are increasingly bypassing traditional security controls, with over 45% of attacks now using sophisticated evasion techniques. Organizations must continuously update their security frameworks to counter these threats, leading to increased operational costs and complexity. Additionally, the lack of skilled cybersecurity professionals—affecting nearly 52% of organizations globally—further exacerbates the challenge. Maintaining real-time monitoring and response capabilities across multiple endpoints requires significant investment in technology and expertise, making it difficult for smaller organizations to keep pace with evolving threats.

AI-driven anomaly detection adoption exceeds 60% across enterprises: Organizations are rapidly adopting AI-based removable media monitoring tools, with over 60% of large enterprises implementing behavioral analytics to detect abnormal data transfer patterns. These solutions have improved threat detection accuracy by nearly 38%, significantly reducing response times and enhancing endpoint visibility across distributed networks.

Zero-trust security frameworks implemented by over 55% organizations: The shift toward zero-trust architectures has led to over 55% of enterprises enforcing strict access control policies for removable devices. This approach has reduced unauthorized USB usage incidents by approximately 42%, ensuring stronger data protection and compliance across regulated industries.

Cloud-based management platforms adopted by 47% enterprises: Cloud-managed removable media security solutions are gaining traction, with 47% of organizations deploying centralized monitoring systems. These platforms enable real-time policy enforcement across multiple endpoints, improving operational efficiency by nearly 33% while reducing infrastructure dependency.

Encryption-enabled USB device usage rises by 50%: The use of hardware-encrypted USB devices has increased by 50%, particularly in BFSI and healthcare sectors. These devices provide enhanced data protection, reducing data leakage risks by approximately 36%, while supporting compliance with stringent data protection regulations.

The Removable Media Security Market is segmented based on type, application, and end-user industries, each contributing uniquely to overall market dynamics. By type, solutions such as device control, encryption, and monitoring dominate deployment strategies, reflecting diverse security requirements across organizations. Application-wise, data protection and compliance management lead adoption, driven by increasing regulatory mandates. End-user segmentation highlights strong demand from BFSI, healthcare, and government sectors, collectively accounting for over 60% of total usage due to sensitive data handling requirements. Additionally, growing digital transformation in manufacturing and IT sectors is contributing to expanded adoption, particularly in emerging economies where enterprise digitization rates exceed 40%.

Device Control solutions dominate the market, accounting for approximately 38% of total adoption due to their ability to restrict unauthorized device access and enforce policy-based controls. Encryption solutions follow with around 27% share, offering enhanced data protection through secure storage and transfer mechanisms. Monitoring and auditing tools contribute nearly 20%, enabling real-time tracking of data movement. Device Control remains the leading segment due to its critical role in preventing unauthorized access and ensuring compliance with data protection regulations. Encryption solutions are the fastest-growing segment, expanding at a CAGR of approximately 13%, driven by increasing demand for secure data transfer and compliance with stringent regulations. The integration of hardware-based encryption and advanced key management systems is further accelerating adoption. Other types, including data loss prevention integration and removable media scanning tools, collectively account for around 15% of the market, serving niche but critical use cases.

• In 2025, a national cybersecurity agency reported that implementing USB device control policies reduced unauthorized data access incidents by over 40% across government networks.

Data Protection & Compliance applications lead the market with approximately 44% share, driven by strict regulatory requirements across industries such as BFSI and healthcare. Threat Detection & Prevention accounts for around 29%, leveraging advanced analytics to identify potential risks. Threat detection is the fastest-growing application segment, expanding at a CAGR of nearly 12.5%, supported by rising cyber threats and increasing adoption of AI-based monitoring tools. Other applications, including device management and auditing, collectively contribute about 27% of the market. In 2025, more than 42% of enterprises globally reported deploying removable media security solutions specifically for compliance management. Additionally, over 58% of IT leaders indicated increased investment in threat detection capabilities.

• In 2025, a global healthcare network implemented AI-driven removable media monitoring across 120+ facilities, improving data breach detection efficiency by over 35%.

The BFSI sector leads with approximately 32% market share due to high sensitivity of financial data and strict compliance requirements. Healthcare follows with around 24%, driven by increasing digitization of patient records and regulatory mandates. Government and defense sectors contribute nearly 18%, focusing on national security and data protection. Healthcare is the fastest-growing end-user segment, expanding at a CAGR of approximately 13.2%, fueled by rising adoption of electronic health records and increased cybersecurity investments. Other sectors, including IT & telecom and manufacturing, collectively account for about 26% of the market. In 2025, over 60% of financial institutions reported implementing advanced removable media controls, while 48% of healthcare organizations increased spending on endpoint security solutions.

• In 2025, a national healthcare authority deployed removable media encryption systems across public hospitals, reducing unauthorized data access incidents by 37%.

North America accounted for the largest market share at 38% in 2025 however, Asia-Pacific is expected to register the fastest growth, expanding at a CAGR of 12.8% between 2026 and 2033.

Europe holds approximately 27% share, driven by stringent regulatory frameworks, while Asia-Pacific accounts for nearly 24% with rapid enterprise digitization. South America and Middle East & Africa collectively contribute around 11%, supported by increasing cybersecurity investments. Over 65% of enterprises in developed regions have implemented removable media controls, compared to 38% in emerging economies, indicating strong growth potential. Adoption rates are particularly high in BFSI and healthcare sectors globally, exceeding 50% in regulated industries.

North America holds approximately 38% of the global market share, driven by high adoption across BFSI, healthcare, and defense sectors. Over 70% of enterprises have implemented endpoint security solutions with removable media control capabilities. Regulatory frameworks such as data protection mandates have accelerated adoption. Advanced technologies, including AI-driven monitoring and zero-trust architectures, are widely deployed. A leading regional player has developed AI-based USB control solutions that improved threat detection rates by 40%. Consumer behavior shows higher adoption among large enterprises compared to SMEs.

Europe accounts for around 27% of the market, with Germany, the UK, and France leading adoption. Over 62% of organizations comply with stringent data protection laws, driving demand for removable media security solutions. Adoption of encryption technologies is particularly strong, with over 50% usage across enterprises. Regional initiatives focusing on cybersecurity resilience further support market growth. A European cybersecurity firm has introduced encrypted USB solutions, reducing data leakage risks by 30%. Consumer behavior reflects strong preference for compliance-driven security systems.

Asia-Pacific represents approximately 24% of the market, with China, India, and Japan leading consumption. Over 45% of enterprises in the region are investing in endpoint security solutions due to increasing cyber threats. Rapid industrialization and digital transformation are key growth drivers. Technology hubs are focusing on AI-based security solutions, improving efficiency by over 35%. A regional company has implemented cloud-based monitoring systems across enterprises, enhancing security compliance. Consumer behavior indicates strong growth in SMEs adopting cost-effective solutions.

South America holds around 6% of the market, with Brazil and Argentina as key contributors. Increasing digitalization in banking and government sectors is driving demand. Government initiatives promoting cybersecurity awareness have improved adoption rates by over 28%. Infrastructure development is supporting deployment of advanced security solutions. A local firm has introduced cost-effective USB security tools, improving adoption among SMEs. Consumer behavior shows growing demand for localized and affordable solutions.

The Middle East & Africa account for approximately 5% of the market, with UAE and South Africa leading growth. Increasing investments in oil & gas and construction sectors are driving demand for data protection solutions. Over 40% of enterprises are adopting endpoint security tools. Technological modernization initiatives are supporting market expansion. A regional cybersecurity provider has deployed advanced monitoring systems, improving data security by 32%. Consumer behavior indicates rising awareness of cybersecurity risks.

United States – 34% Market share: Strong enterprise adoption and high investment in cybersecurity infrastructure

Germany – 12% Market share: Strict regulatory framework and strong industrial demand

The Removable Media Security Market is moderately fragmented, with over 40 active global and regional players competing across different solution categories. The top five companies collectively account for approximately 52% of the market share, indicating a semi-consolidated structure. Leading players focus on strategic initiatives such as product innovation, partnerships, and acquisitions to strengthen their market presence. Over 65% of vendors have introduced AI-integrated security solutions to enhance threat detection capabilities. Additionally, around 48% of companies are investing in cloud-based platforms to offer scalable and centralized management solutions.

Competitive differentiation is largely driven by technological capabilities, regulatory compliance features, and integration with broader cybersecurity ecosystems. The market is also witnessing increased collaboration between cybersecurity firms and cloud service providers, enabling comprehensive endpoint protection strategies. Emerging players are focusing on niche segments such as encrypted USB devices and specialized monitoring tools, intensifying competition and driving continuous innovation.

McAfee LLC

Trend Micro Incorporated

Sophos Group plc

Kaspersky Lab

Check Point Software Technologies Ltd.

Cisco Systems, Inc.

Digital Guardian

Forcepoint

CoSoSys Ltd.

Ivanti, Inc.

Endpoint Protector

ManageEngine

Palo Alto Networks, Inc.

Technological advancements are playing a critical role in shaping the Removable Media Security Market, with a strong focus on automation, artificial intelligence, and cloud integration. AI-driven behavioral analytics solutions are now capable of identifying anomalous device usage patterns with over 40% higher accuracy compared to traditional methods. These systems analyze user activity in real time, enabling faster threat detection and response.

Zero-trust architecture has become a key technological trend, with over 55% of enterprises implementing strict verification protocols for removable media access. This approach ensures that every device and user interaction is authenticated, significantly reducing the risk of unauthorized data transfers. Additionally, encryption technologies are evolving, with hardware-based encrypted USB devices gaining popularity, particularly in regulated industries.

Cloud-based management platforms are transforming how organizations monitor and control removable media usage. Approximately 47% of enterprises have adopted centralized cloud solutions, allowing real-time policy enforcement across multiple endpoints. These platforms improve operational efficiency by nearly 33% and enable seamless integration with other cybersecurity tools.

Another significant advancement is the integration of removable media security with data loss prevention (DLP) systems. Over 60% of organizations are deploying integrated solutions to enhance data protection capabilities. Emerging technologies such as blockchain-based device authentication and automated compliance reporting are expected to further strengthen security frameworks, providing robust protection against evolving cyber threats.

• In March 2026, Cisco Systems updated its Secure Client compliance modules to enhance endpoint posture validation, enabling improved control over device access including external media integration and compliance checks across Windows, macOS, and Linux environments. Source: www.cisco.com

• In 2025, Broadcom (Symantec Enterprise Division) continued enhancements to Symantec Endpoint Security, integrating advanced AI-driven behavioral analysis and device control capabilities to monitor and restrict removable media usage across hybrid and cloud environments.

• In 2025, Trend Micro expanded its Vision One platform with enhanced third-party log ingestion and endpoint telemetry integration, enabling improved visibility into removable media activity and cross-platform threat correlation through centralized monitoring systems.

• In March 2026, ThreatDown (Malwarebytes division) introduced advanced vulnerability and patch management features in OneView, allowing administrators to remotely remove unauthorized or risky applications from endpoints, strengthening control over devices interacting with removable media.

The Removable Media Security Market Report provides a comprehensive analysis of the global market landscape, covering key segments such as device control, encryption, monitoring, and data loss prevention integration. It includes detailed insights into application areas such as data protection, compliance management, and threat detection, highlighting their significance across industries. The report evaluates end-user segments including BFSI, healthcare, government, IT & telecom, and manufacturing, offering a detailed understanding of adoption patterns and demand drivers.

Geographically, the report covers major regions including North America, Europe, Asia-Pacific, South America, and the Middle East & Africa, providing region-specific insights into market trends, adoption rates, and technological advancements. It also examines emerging markets where digital transformation and increasing cybersecurity awareness are driving demand.

The report further explores technological developments such as AI-driven monitoring, zero-trust security frameworks, cloud-based management platforms, and encryption technologies. It highlights the role of these innovations in enhancing endpoint security and improving operational efficiency. Additionally, the report analyzes competitive dynamics, profiling key market players and their strategic initiatives.

Overall, the scope of the report is designed to provide decision-makers with actionable insights, enabling them to understand market trends, identify growth opportunities, and develop effective strategies in the evolving Removable Media Security Market.

| Report Attribute / Metric | Details |

|---|---|

| Market Revenue (2025) | USD 170.0 Million |

| Market Revenue (2033) | USD 406.1 Million |

| CAGR (2026–2033) | 11.5% |

| Base Year | 2025 |

| Forecast Period | 2026–2033 |

| Historic Period | 2021–2025 |

| Segments Covered |

By Type

By Application

By End-User Insights

|

| Key Report Deliverables | Revenue Forecast; Market Trends; Growth Drivers & Restraints; Technology Insights; Segmentation Analysis; Regional Insights; Competitive Landscape; Regulatory & ESG Overview; Recent Developments |

| Regions Covered | North America; Europe; Asia-Pacific; South America; Middle East & Africa |

| Key Players Analyzed | Broadcom (Symantec Enterprise Division); McAfee LLC; Trend Micro Incorporated; Sophos Group plc; Kaspersky Lab; Check Point Software Technologies Ltd.; Cisco Systems, Inc.; Digital Guardian; Forcepoint; CoSoSys Ltd.; Ivanti, Inc.; Endpoint Protector; ManageEngine; Palo Alto Networks, Inc. |

| Customization & Pricing | Available on Request (10% Customization Free) |