Reports

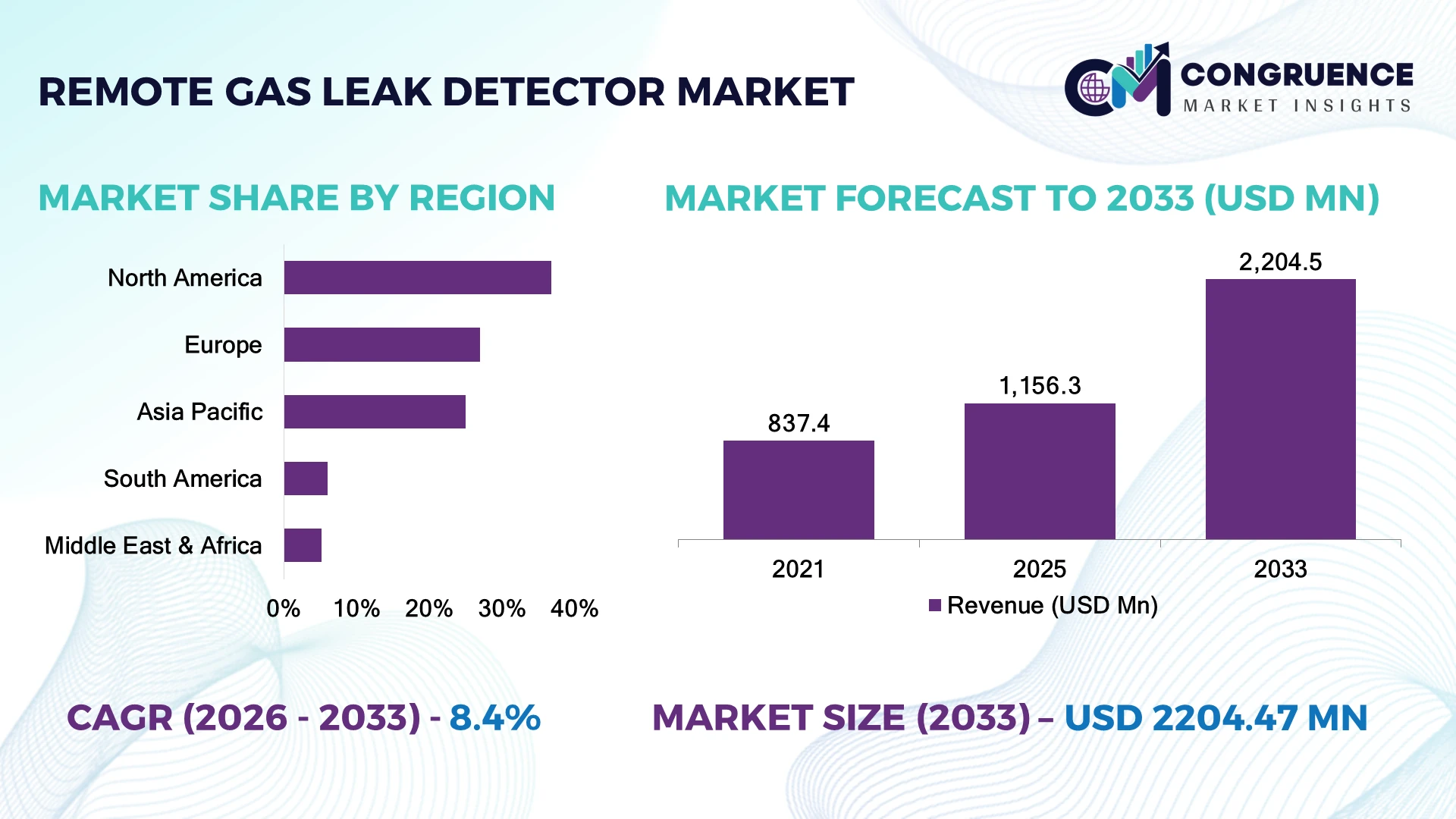

The Global Remote Gas Leak Detector Market was valued at USD 1,156.3 Million in 2025 and is anticipated to reach a value of USD 2,204.5 Million by 2033 expanding at a CAGR of 8.4% between 2026 and 2033. Growth is being driven by stricter industrial methane emission regulations, expansion of hydrogen infrastructure, and increasing deployment of AI-enabled optical gas detection systems across energy and process industries.

The United States accounts for approximately 31% of the global market, supported by extensive oil & gas infrastructure, LNG investments, and advanced industrial safety standards. More than 64% of newly commissioned upstream monitoring projects incorporate remote gas leak detection technologies, while Norway is expanding offshore optical monitoring for carbon capture and hydrogen facilities. Geopolitical emphasis on energy security and methane emission reduction is accelerating deployment across critical infrastructure, strengthening global demand for high-performance detection systems.

Companies investing in intelligent sensing platforms, regulatory compliance, and integrated industrial monitoring solutions will strengthen long-term market leadership.

Market Size & Growth: USD 1,156.3 million in 2025, projected to reach USD 2,204.5 million by 2033 at 8.4% CAGR, driven by stricter industrial emission monitoring.

Top Growth Drivers: Methane monitoring (+24%), hydrogen infrastructure (+19%), industrial automation (+17%).

Short-Term Forecast: By 2028, inspection response time is expected to improve by approximately 22% through AI-assisted monitoring.

Emerging Technologies: AI analytics, laser spectroscopy, and drone-integrated gas sensing improve operational visibility.

Regional Leaders: North America (~USD 430 million), Europe (~USD 350 million), Asia-Pacific (~USD 610 million) expand through industrial safety modernization.

Consumer/End-User Trends: Nearly 66% of energy operators prioritize continuous remote gas monitoring over manual inspections.

Pilot/Case Example: In 2026, automated leak monitoring reduced emergency inspection requirements by approximately 27% at large industrial facilities.

Competitive Landscape: Leading suppliers collectively control nearly 56% of global demand through sensing innovation and industrial integration.

Regulatory & ESG Impact: Methane reduction initiatives lowered fugitive emission events by approximately 18% across monitored assets.

Investment & Funding: More than USD 950 million has been committed toward industrial safety digitization and gas monitoring infrastructure.

Innovation & Future Outlook: Edge analytics, autonomous inspection, and cloud-connected monitoring platforms continue reshaping industrial safety operations.

Remote gas leak detectors are increasingly deployed across oil & gas facilities, hydrogen infrastructure, chemical plants, and utility networks where continuous monitoring improves operational safety and regulatory compliance. AI-assisted optical sensing increases leak detection accuracy by approximately 23%, while industrial operators continue strengthening digital monitoring capabilities amid tighter methane emission requirements and resilient infrastructure investments. These operational trends establish the foundation for the strategic assessment that follows.

Remote gas leak detection has become strategically important as industrial operators prioritize continuous emissions monitoring, predictive maintenance, and workforce safety across energy, chemical, and utility infrastructure. Regulatory tightening surrounding methane emissions, combined with modernization of industrial assets and digital safety systems, is accelerating investment in intelligent monitoring platforms capable of identifying leaks before operational disruptions occur.

Compared with conventional handheld inspections, fixed and remote optical gas detection systems reduce inspection time by approximately 35% while improving leak localization accuracy by nearly 28%. North America leads deployment through advanced energy infrastructure and regulatory enforcement, whereas Asia-Pacific is rapidly expanding adoption across refineries, LNG terminals, and large-scale manufacturing facilities. Over the next two to three years, more than 42% of newly commissioned industrial monitoring projects are expected to integrate AI-enabled remote gas detection with centralized asset management platforms.

A practical example is the deployment of autonomous gas monitoring systems at LNG terminals, where continuous sensing minimizes manual inspection frequency while improving operational reliability. Companies are expanding investments in laser-based sensing, cloud-connected monitoring platforms, and strategic partnerships with industrial automation providers to strengthen integrated safety solutions. Organizations combining high-precision sensing, digital analytics, and scalable industrial integration will establish durable competitive advantages as intelligent emissions monitoring becomes an operational standard.

Stricter methane emission regulations and industrial safety requirements are driving large-scale adoption of remote gas leak detectors across oil & gas, petrochemical, and LNG facilities. Approximately 69% of newly commissioned upstream energy assets now integrate continuous gas monitoring systems, while AI-enabled optical detection reduces leak response time by nearly 30%. In the United States, expanding methane reporting requirements are encouraging operators to replace periodic inspections with continuous remote surveillance. This regulatory shift improves environmental compliance, minimizes unplanned shutdowns, and lowers operational risk. Manufacturers are responding through laser-based sensing innovation, cloud-enabled monitoring platforms, and strategic partnerships with industrial automation providers, strengthening long-term service contracts and integrated safety solutions for critical infrastructure operators.

Remote gas leak detection systems require significant upfront investment in optical sensors, communication infrastructure, and software integration, limiting adoption among smaller industrial facilities. Installation and commissioning expenses account for nearly 36% of total deployment costs, while integration with legacy control systems increases project timelines by approximately 18%. Aging industrial infrastructure in several developing markets further complicates implementation because existing SCADA and plant automation systems often lack compatibility with advanced monitoring platforms. These structural limitations reduce deployment flexibility and extend return-on-investment periods. Companies are addressing these issues through modular detector architectures, localized system integration services, and long-term maintenance agreements that improve affordability while simplifying deployment across brownfield industrial sites.

Artificial intelligence, autonomous inspection platforms, and digital industrial ecosystems are opening new growth avenues beyond conventional fixed monitoring. Nearly 34% of new industrial digitalization projects now evaluate AI-assisted gas analytics integrated with drones, robotic inspection systems, and edge computing platforms. Japan is accelerating hydrogen infrastructure investments, creating demand for high-precision remote gas detection technologies capable of continuous monitoring in complex operating environments. Automated analytics improve leak classification accuracy by approximately 26%, reducing unnecessary field inspections and maintenance costs. Companies are increasing investments in AI algorithms, autonomous sensing platforms, and strategic collaborations with industrial software providers to develop intelligent monitoring ecosystems that deliver predictive operational insights alongside safety compliance.

Expanding remote gas monitoring across geographically dispersed industrial assets requires secure data transmission, standardized communication protocols, and reliable interoperability between sensing devices and industrial control platforms. Nearly 43% of industrial operators identify cybersecurity and network resilience as primary concerns during remote monitoring deployment, while over 21% of projects require additional integration engineering for multi-vendor environments. Increasing digital connectivity also raises exposure to operational disruptions affecting continuous monitoring reliability. Companies must strengthen encrypted communications, edge-based processing, resilient network infrastructure, and cybersecurity partnerships while investing in workforce training and standardized industrial protocols to maintain dependable monitoring performance across increasingly connected industrial operations.

AI-Powered Leak Analytics Industrial operators are integrating AI-driven analytics with optical gas detection to automate leak prioritization and reduce false alarms. Detection accuracy has improved by approximately 24%, while manual verification requirements have declined by nearly 19%. Stricter methane regulations are accelerating adoption, prompting suppliers to expand software capabilities and cloud-based monitoring partnerships.

Drone-Based Inspection Growth Energy companies are increasingly combining remote gas detectors with unmanned aerial systems for pipeline, refinery, and LNG inspections. Drone-assisted monitoring reduces inspection time by approximately 32% and lowers field personnel exposure by nearly 27%. Companies are scaling autonomous inspection programs and strengthening collaborations with industrial drone solution providers to improve operational efficiency.

Edge Computing Integration Remote detection platforms are shifting toward edge-based processing to enable faster incident response and reduce network dependence. Local data processing shortens alert latency by approximately 21% while decreasing bandwidth utilization by nearly 17%. Industrial enterprises are modernizing monitoring infrastructure through intelligent edge devices and integrated operational technology architectures.

Hydrogen Safety Monitoring Expansion Growing hydrogen production and transportation projects are increasing demand for specialized remote leak detection systems with enhanced sensitivity. More than 29% of newly planned hydrogen facilities include continuous remote gas monitoring during project design, while advanced laser sensors improve low-concentration detection performance by approximately 18%. Manufacturers are expanding product portfolios and engineering partnerships to address emerging hydrogen infrastructure requirements.

Fixed remote gas leak detectors accounted for approximately 64% of the market in 2025, supported by their continuous monitoring capability, seamless integration with distributed control systems (DCS), and suitability for high-risk industrial facilities. Oil & gas operators, LNG terminals, and petrochemical plants increasingly deploy fixed optical gas detectors to comply with emission monitoring regulations while reducing manual inspections. Around 71% of newly commissioned process facilities integrate fixed detection systems during plant construction, reflecting their operational reliability and lower lifecycle maintenance costs. Manufacturers continue enhancing long-range laser sensing, wireless connectivity, and AI-assisted diagnostics to improve monitoring performance across complex industrial environments.

Portable remote gas leak detectors represent the fastest-growing segment as maintenance teams, emergency responders, and utility operators demand flexible inspection solutions for pipelines and remote assets. Vehicle-mounted and drone-compatible systems are also expanding, supporting rapid infrastructure inspections without permanent installation. Nearly 29% of recent product launches emphasize portable and mobile detection platforms with cloud connectivity and real-time analytics. Companies are expanding product portfolios, forming technology partnerships, and investing in lightweight sensor architectures to address evolving field inspection requirements.

A 2026 industrial safety assessment reported that continuous fixed gas monitoring systems are increasingly being specified for new energy and process facilities to strengthen regulatory compliance and reduce unplanned operational interruptions.

Oil & gas accounted for approximately 43% of total market demand in 2025 due to extensive pipeline networks, upstream production sites, refineries, and LNG infrastructure requiring continuous gas monitoring. Remote gas leak detectors are widely deployed to improve operational safety, minimize methane emissions, and support automated facility management. Nearly 68% of newly upgraded upstream monitoring programs incorporate remote optical detection technologies as operators replace manual inspections with continuous surveillance. Suppliers continue strengthening industrial integration, remote diagnostics, and predictive maintenance capabilities to support large-scale energy infrastructure.

Hydrogen infrastructure represents the fastest-growing application as governments and industrial enterprises accelerate hydrogen production, storage, and transportation projects requiring highly sensitive leak detection systems. Chemical processing, utilities, mining, and power generation remain strategically important as digital safety modernization expands across industrial sectors. Approximately 26% of enterprise investments in industrial gas monitoring now target hydrogen-compatible sensing technologies. Companies are increasing deployment partnerships, integrating AI-enabled analytics, and scaling advanced monitoring platforms to address evolving operational safety requirements across emerging industrial applications.

According to enterprise findings published during 2025, industrial operators implementing continuous gas monitoring reported broader deployment of remote sensing technologies across energy, chemical, and hydrogen facilities to strengthen environmental compliance and operational resilience.

Oil & gas companies held approximately 46% of market demand in 2025, driven by extensive upstream, midstream, and downstream infrastructure requiring continuous gas monitoring across geographically dispersed assets. Their large-scale operations, stringent safety requirements, and regulatory obligations make remote gas leak detectors a critical operational technology investment. Around 63% of enterprise procurement programs within the sector now prioritize integrated monitoring platforms capable of combining gas detection with centralized asset management. Vendors are responding through customized monitoring solutions, long-term service agreements, and integrated industrial automation partnerships.

Chemical and petrochemical companies represent the fastest-growing end-user group as process safety modernization and hazardous gas monitoring become increasingly automated. Utilities, mining operators, and manufacturing facilities continue expanding deployment as workforce safety and environmental compliance gain greater operational importance. Nearly 31% of solution providers have increased investment in industry-specific software, customized sensing platforms, and predictive maintenance capabilities to address evolving customer requirements. Companies are strengthening ecosystem partnerships and flexible deployment models to improve competitiveness across multiple industrial sectors.

A 2026 enterprise industrial safety survey found that organizations operating continuous-process facilities are increasingly prioritizing remote gas monitoring platforms integrated with centralized operational control systems to improve response speed and asset visibility.

North America accounted for the largest market share at 36.8% in 2025 however, Asia-Pacific is expected to register the fastest growth, expanding at a CAGR of 9.3% between 2026 and 2033.

Advanced Emissions Monitoring Becomes Operational Standard

North America maintains market leadership through extensive oil & gas infrastructure, stringent industrial safety regulations, and rapid adoption of continuous emissions monitoring technologies. The region contributes approximately 37% of global demand, supported by widespread deployment across upstream production, LNG terminals, petrochemical complexes, and pipeline networks. Nearly 61% of newly upgraded industrial monitoring projects integrate remote gas leak detectors with centralized asset management systems, improving operational visibility and incident response. Companies continue expanding AI-enabled sensing platforms, cloud-connected monitoring networks, and long-term service partnerships with energy operators to strengthen predictive maintenance and regulatory compliance. These investments reinforce North America's position as the primary commercial market for advanced remote gas detection technologies.

United States Market Outlook: The United States leads regional deployment through its extensive natural gas pipeline network, LNG export infrastructure, and advanced industrial automation ecosystem. More than 67% of newly commissioned methane monitoring installations are concentrated within large energy and petrochemical facilities. Industrial operators continue investing in laser-based remote sensing, autonomous monitoring platforms, and integrated environmental compliance systems to improve operational efficiency while supporting stricter emissions management requirements.

Decarbonization Policies Accelerate Smart Safety Infrastructure

Europe accounts for approximately 27% of the global market, supported by strict methane reduction targets, industrial modernization, and expanding hydrogen infrastructure. Energy producers and process industries are replacing periodic inspections with continuous remote monitoring systems to improve operational reliability and environmental performance. Nearly 46% of large industrial emission control upgrades now incorporate intelligent gas detection integrated with digital asset management platforms. Technology providers are expanding partnerships with automation companies while introducing advanced optical sensing solutions designed for hydrogen, carbon capture, and petrochemical applications.

Germany Market Outlook: Germany serves as Europe's leading industrial market due to its advanced chemical manufacturing base, hydrogen investments, and engineering expertise. Approximately 39% of regional hydrogen demonstration facilities utilize remote gas monitoring during commissioning and operations. Companies continue integrating intelligent sensing with industrial control platforms while investing in high-precision monitoring technologies for process safety and emission compliance.

Industrial Expansion Strengthens Intelligent Monitoring Adoption

Asia-Pacific is rapidly expanding through industrial infrastructure development, refinery modernization, LNG investments, and growing adoption of digital industrial safety technologies. The region represents approximately 25% of global demand, with increasing deployment across petrochemical complexes, power generation facilities, and city gas distribution networks. Around 33% of recently commissioned industrial safety projects include AI-enabled remote gas leak detection integrated with centralized monitoring systems. Equipment manufacturers are strengthening regional production capabilities, expanding distribution networks, and investing in localized engineering support to meet rising enterprise demand.

China Market Outlook: China remains the region's largest market owing to large-scale refinery expansion, chemical manufacturing capacity, and accelerated hydrogen infrastructure projects. More than 41% of newly commissioned heavy industrial facilities incorporate intelligent gas detection during plant construction. Domestic manufacturers are increasing production capacity, improving laser sensing technologies, and expanding industrial automation partnerships to support national industrial safety modernization initiatives.

Energy Infrastructure Modernization Supports Safety Investments

South America contributes approximately 6% of global demand, driven by upstream oil production, mining operations, and expanding natural gas infrastructure. Industrial operators increasingly deploy remote gas leak detectors to strengthen operational safety across pipelines, offshore facilities, and processing plants. Nearly 24% of recent industrial modernization projects include digital gas monitoring solutions as enterprises reduce manual inspections and improve maintenance planning. Limited local manufacturing capacity continues to create import dependency, encouraging suppliers to strengthen regional distribution partnerships and technical support capabilities.

Brazil Market Outlook: Brazil leads the regional market through offshore oil production, expanding natural gas processing infrastructure, and increasing investment in industrial automation. Approximately 44% of large-scale energy monitoring deployments within South America are concentrated in Brazil. Companies are expanding service networks, improving system integration capabilities, and supporting digital safety upgrades across upstream and downstream energy facilities.

Energy Infrastructure Investments Expand Intelligent Monitoring

The Middle East & Africa accounts for approximately 5.2% of global demand, supported by ongoing investments in oil & gas infrastructure, LNG developments, and industrial safety modernization. Large energy operators increasingly deploy remote gas leak detectors to improve continuous emissions monitoring and reduce operational risk across high-value assets. Around 29% of newly approved hydrocarbon processing projects include advanced optical gas detection within integrated plant safety systems. Technology providers are expanding regional partnerships, localized engineering services, and industrial training programs to strengthen deployment efficiency and long-term operational support.

Saudi Arabia Market Outlook: Saudi Arabia represents the region's most influential market through large-scale hydrocarbon infrastructure, refinery expansion, and hydrogen development initiatives. Nearly 48% of major energy infrastructure modernization projects within the Gulf incorporate intelligent gas monitoring technologies. Companies continue investing in integrated safety platforms, digital industrial control systems, and advanced optical sensing solutions to enhance operational resilience across strategically important energy assets.

Honeywell, Teledyne FLIR, Siemens, Pergam, and Opgal lead competition, while specialized laser-sensing innovators increasingly challenge diversified industrial automation companies. The top five players collectively account for approximately 58% of global market activity. Honeywell and Siemens compete through integrated industrial safety ecosystems, whereas Teledyne FLIR, Opgal, and Pergam differentiate through optical gas imaging, long-range laser detection, and remote inspection capabilities. Competition depends on sensing accuracy, software intelligence, deployment speed, and lifecycle support rather than equipment pricing. AI-assisted analytics improve leak identification by approximately 24%, optical imaging extends inspection productivity by nearly 30%, and cloud-connected diagnostics reduce maintenance intervention by around 18%. Companies are expanding industrial automation partnerships, integrating edge analytics, and strengthening service networks while investing in autonomous monitoring technologies. Qualification for hazardous environments, regulatory certification, and advanced optical engineering remain significant entry barriers. Winning requires superior sensing precision, intelligent analytics, industrial integration expertise, and dependable lifecycle support.

Honeywell International Inc.

Teledyne FLIR LLC

Siemens AG

ABB Ltd.

Emerson Electric Co.

Drägerwerk AG & Co. KGaA

MSA Safety Incorporated

Opgal Optronic Industries Ltd.

Pergam Suisse AG

Heath Consultants Incorporated

Sensia LLC

Tokyo Gas Engineering Solutions Corporation

Remote gas leak detection is rapidly evolving through tunable diode laser absorption spectroscopy (TDLAS), optical gas imaging (OGI), AI-enabled analytics, and cloud-connected industrial monitoring platforms. More than 62% of newly deployed industrial monitoring projects now integrate intelligent remote sensing with centralized asset management systems. AI-assisted leak recognition improves detection accuracy by approximately 24%, while edge computing reduces alert latency by nearly 19%, enabling faster operational decisions and improved facility safety.

Compared with conventional handheld inspections, fixed optical monitoring systems increase inspection coverage by approximately 35% while reducing manual field interventions by nearly 28%. Integration with drones, robotics, and autonomous inspection platforms enables continuous monitoring across pipelines, LNG terminals, and petrochemical complexes. Honeywell, Teledyne FLIR, and Opgal benefit from these technology shifts through advanced sensing capabilities, whereas automation providers strengthen competitiveness by embedding gas monitoring into broader industrial digitalization platforms.

Between 2026 and 2028, hydrogen-specific sensing, AI-driven plume analytics, multispectral infrared imaging, and predictive industrial monitoring will redefine competitive positioning. Nearly 45% of planned industrial safety upgrades are expected to include intelligent remote gas monitoring integrated with digital twins and predictive maintenance systems. Organizations investing now will improve operational resilience, regulatory compliance, maintenance efficiency, and long-term infrastructure performance.

May 2025 Honeywell launched its Hydrogen Leak Detector capable of identifying hydrogen leaks as small as 50 parts per million, supporting industrial equipment and hydrogen-powered systems while improving operational safety. Business impact: accelerates hydrogen infrastructure deployment. Source: Honeywell

May 2025 Teledyne FLIR OEM and AerialOGI introduced the AerialOGI-N optical gas imaging module, supporting detection of more than 25 greenhouse gases from handheld and drone platforms. Business impact: improves inspection productivity and remote emissions monitoring. Source: Teledyne FLIR OEM

March 2026 Honeywell introduced its 4-Series NDIR Hydrocarbon Gas Sensor featuring infrared technology with lower power consumption and enhanced resistance to sensor poisoning for fixed and portable detectors. Business impact: extends detector operating life and improves industrial reliability. Source: Honeywell

January 2026 Teledyne FLIR's GF77a optical gas imaging system was deployed at South Korea's Boryeong LNG Terminal with AI-assisted methane monitoring for unmanned facilities. Business impact: strengthens continuous leak detection and operational safety across LNG infrastructure. Source: FLIR

The report delivers comprehensive analysis of the Remote Gas Leak Detector market across detector types, industrial applications, end-user industries, and major geographic markets. It evaluates fixed, portable, vehicle-mounted, and drone-integrated systems deployed across oil & gas, petrochemicals, hydrogen infrastructure, utilities, mining, manufacturing, and other industrial environments. The assessment covers North America, Europe, Asia-Pacific, South America, and the Middle East & Africa, supported by country-level operational and competitive insights. More than 60% of the analysis focuses on intelligent monitoring technologies and industrial digitalization trends influencing purchasing decisions.

The report further examines optical gas imaging, tunable diode laser sensing, AI-powered analytics, cloud connectivity, edge computing, and autonomous inspection technologies shaping next-generation industrial safety. It provides competitive benchmarking, deployment trends, technology adoption patterns, and strategic company positioning to support investment planning, product development, market expansion, supply-chain optimization, and long-term business strategy across the global remote gas leak detection ecosystem between 2026 and 2033.

| Report Attribute/Metric | Report Details |

|---|---|

|

Market Revenue in 2025 |

USD 1,156.3 Million |

|

Market Revenue in 2033 |

USD 2,204.5 Million |

|

CAGR (2026 - 2033) |

8.4% |

|

Base Year |

2025 |

|

Forecast Period |

2026 - 2033 |

|

Historic Period |

2021 - 2025 |

|

Segments Covered |

By Type

By Application

By End-User

|

|

Key Report Deliverable |

Revenue Forecast, Growth Trends, Market Dynamics, Segmental Overview, Regional and Country-wise Analysis, Competition Landscape |

|

Region Covered |

North America, Europe, Asia-Pacific, South America, Middle East, Africa |

|

Key Players Analyzed |

Honeywell International Inc., Teledyne FLIR LLC, Siemens AG, ABB Ltd., Emerson Electric Co., Drägerwerk AG & Co. KGaA, MSA Safety Incorporated, Opgal Optronic Industries Ltd., Pergam Suisse AG, Heath Consultants Incorporated, Sensia LLC, Tokyo Gas Engineering Solutions Corporation |

|

Customization & Pricing |

Available on Request (10% Customization is Free) |