Reports

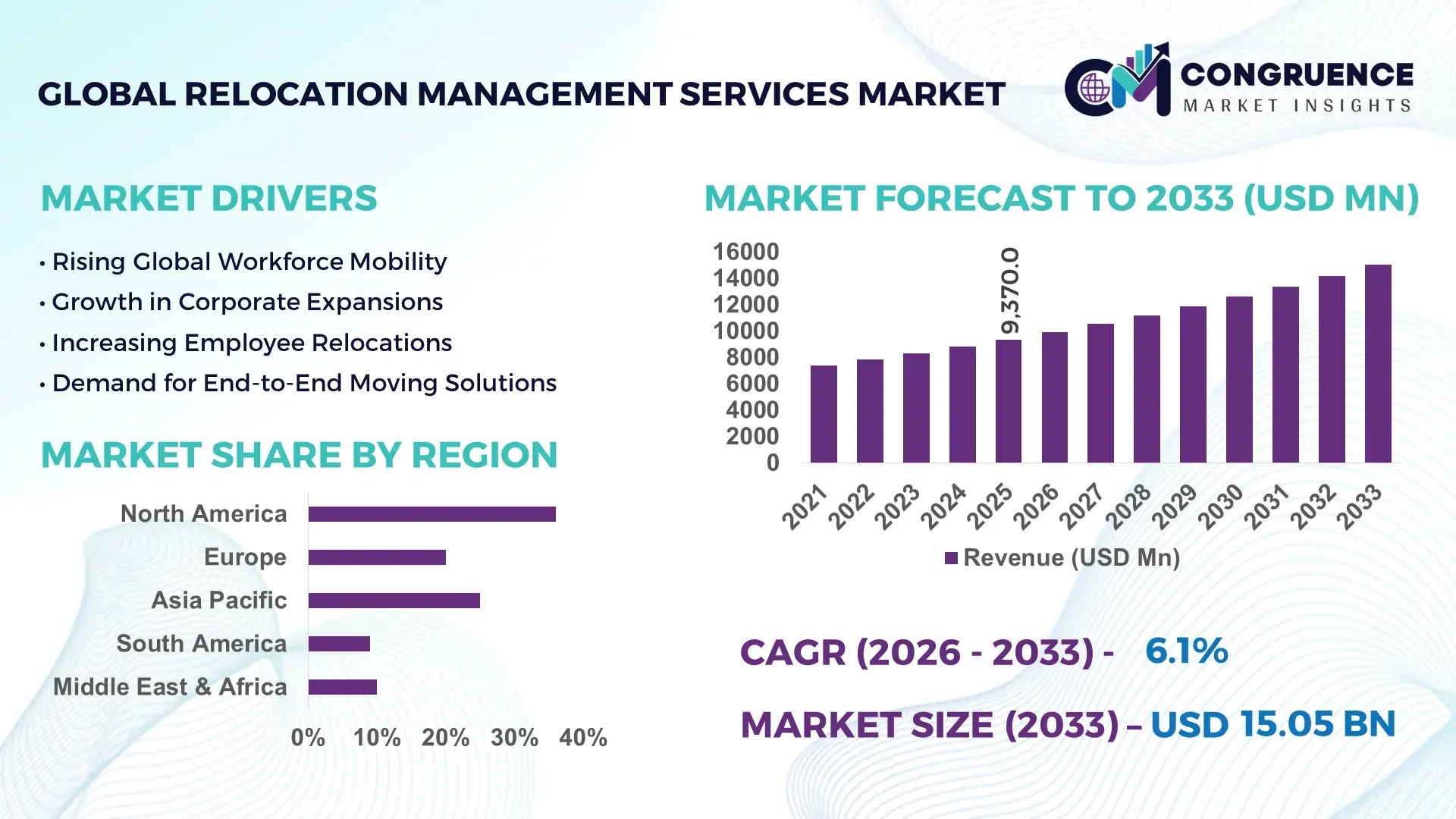

The Global Relocation Management Services Market was valued at USD 9370 Million in 2025 and is anticipated to reach a value of USD 15047.44 Million by 2033 expanding at a CAGR of 6.1% between 2026 and 2033. Cross-border workforce mobility expansion, hybrid assignment models, and rising multinational hiring across technology, healthcare, and manufacturing sectors are accelerating demand for integrated relocation management platforms with automated compliance tracking and destination support services.

The United States continues to dominate the global relocation management services market with nearly 34% share, supported by over USD 18 billion in annual corporate mobility spending and strong deployment across financial services, aerospace, semiconductors, and digital infrastructure industries. More than 62% of Fortune 500 enterprises adopted AI-enabled relocation workflow systems by early 2026, improving employee onboarding efficiency by 28% compared to conventional relocation coordination models. Rising geopolitical supply chain diversification after the Red Sea shipping disruption and continued Asia-Pacific manufacturing expansion increased executive and skilled-worker transfers across North America by over 17% year-on-year. Compared with Europe, U.S.-based enterprises execute higher-volume domestic-to-international workforce transitions, supported by stronger enterprise mobility budgets and cloud-based HR integration capabilities.

Organizations prioritizing scalable relocation ecosystems with immigration analytics, vendor consolidation, and digital employee experience optimization are strengthening workforce continuity and reducing assignment failure risks in high-growth international markets.

Market Size & Growth: USD 9370 million in 2025 reaching USD 15047.44 million by 2033 at 6.1% growth, driven by AI-enabled workforce mobility and multinational expansion.

Top Growth Drivers: Cross-border hiring rose 21%, remote-to-office relocation demand increased 18%, and immigration compliance outsourcing expanded 24% globally.

Short-Term Forecast: By 2027, automated relocation workflows are projected to reduce processing costs by 19% and improve assignment efficiency by 27%.

Emerging Technologies: AI-based mobility analytics, cloud HR integration, and predictive expense automation improved relocation tracking accuracy by 31%.

Regional Leaders: North America exceeds USD 5.4 billion, Europe reaches USD 3.1 billion, and Asia-Pacific crosses USD 4 billion with rising manufacturing relocation activity.

Consumer/End-User Trends: Over 58% of multinational firms shifted toward flexible employee relocation packages with digital self-service mobility tools.

Pilot/Case Example: In 2025, a global technology enterprise reduced relocation approval timelines by 42% through centralized mobility automation deployment.

Competitive Landscape: Market leaders control nearly 38% share, with enterprise expansion led by advanced mobility specialists and integrated HR service providers.

Regulatory & ESG Impact: ESG-linked relocation policies reduced temporary housing emissions by 16% while stricter immigration frameworks increased compliance spending by 22%.

Investment & Funding: Corporate mobility technology investments surpassed USD 2.3 billion through SaaS expansion, strategic partnerships, and regional workforce integration programs.

Innovation & Future Outlook: Predictive workforce planning, AI-driven destination intelligence, and digital immigration management are reshaping high-growth global relocation ecosystems.

Technology, healthcare, financial services, and advanced manufacturing collectively account for more than 61% of enterprise relocation demand, driven by skilled labor redistribution and international expansion projects. AI-powered mobility dashboards, automated immigration documentation, and employee experience platforms are improving assignment visibility and reducing processing delays across multinational operations. North America maintains leadership, while Asia-Pacific records the fastest enterprise mobility adoption due to semiconductor and industrial supply chain repositioning. Increasing regulatory scrutiny around labor mobility and data compliance is pushing enterprises toward centralized relocation ecosystems with integrated analytics and vendor consolidation capabilities. This operational shift is expected to intensify strategic investments in scalable workforce mobility infrastructure through the next phase of global expansion.

The relocation management services market is becoming strategically critical as multinational enterprises restructure workforce distribution to support supply-chain diversification, semiconductor expansion, and regional manufacturing localization. Increasing immigration compliance complexity and hybrid workforce mobility are pushing corporations toward centralized mobility ecosystems with integrated HR, tax, and housing coordination capabilities. By 2026, over 54% of large enterprises are expected to consolidate relocation vendors into unified digital mobility platforms to improve assignment visibility and reduce administrative fragmentation. Countries including the United States, Germany, and Singapore are accelerating skilled-worker relocation programs to strengthen industrial competitiveness in advanced manufacturing and technology sectors.

AI-enabled relocation workflow systems are reducing employee onboarding timelines by nearly 32% compared to legacy manual coordination models while lowering documentation processing errors by 26%. The United States leads in enterprise-scale deployment through cloud-integrated mobility suites, whereas Japan and the UAE are prioritizing high-touch executive relocation supported by immigration automation and destination intelligence platforms. Over the next two to three years, enterprise demand for predictive mobility analytics and employee experience optimization is projected to accelerate as global labor redistribution intensifies across logistics, healthcare, and digital infrastructure industries.

A major technology consulting enterprise in 2025 integrated AI-driven relocation expense management with immigration tracking across 40 countries, reducing assignment disruption rates by 21% and improving vendor coordination efficiency. Relocation providers are expanding partnerships with HR software vendors, temporary housing operators, and compliance specialists to build scalable workforce mobility ecosystems. Companies that combine digital mobility infrastructure with localized compliance execution are expected to secure stronger enterprise retention, operational continuity, and long-term competitive positioning.

Rising cross-border workforce mobility and distributed talent acquisition are accelerating enterprise investment in advanced relocation management services. More than 63% of multinational corporations increased international employee transfers in 2025, while AI-enabled mobility workflow adoption improved relocation processing efficiency by 29%. U.S.-based technology and pharmaceutical companies are expanding relocation partnerships to support semiconductor manufacturing, clinical research, and cloud infrastructure projects. Tightening immigration documentation standards in Germany and Canada are further increasing demand for centralized compliance management platforms. In response, relocation providers are integrating predictive analytics, digital expense automation, and employee experience dashboards into unified mobility ecosystems. A notable operational shift involves enterprises consolidating fragmented relocation vendors into strategic long-term partnerships to improve assignment continuity and reduce workforce deployment delays.

Escalating housing costs, immigration compliance burdens, and fragmented tax regulations are constraining operational scalability across the relocation management services market. Temporary accommodation expenses in major business hubs such as London, Singapore, and New York increased by over 18% between 2024 and 2026, directly impacting corporate mobility budgets. Nearly 41% of multinational firms reported extended relocation approval cycles due to evolving visa documentation requirements and labor policy revisions. Supply shortages in premium short-term housing are also increasing assignment disruption risks for executive transfers. To reduce operational exposure, companies are diversifying housing networks, renegotiating vendor contracts, and expanding regional compliance partnerships. A significant business impact is the shift toward flexible relocation packages and hybrid assignment structures designed to control deployment costs without reducing workforce mobility capabilities.

Digital relocation ecosystems and emerging workforce migration corridors are creating high-value expansion opportunities for mobility service providers. AI-enabled relocation platforms are improving policy compliance accuracy by 34% while reducing manual coordination workloads by nearly 30%. India, Vietnam, and Poland are attracting rising volumes of technology, engineering, and semiconductor-related workforce transfers due to industrial expansion and competitive labor availability. Enterprises are increasingly deploying predictive mobility analytics, multilingual onboarding tools, and digital immigration processing to accelerate deployment consistency. A notable strategic opportunity is the integration of sustainability-focused relocation models, including low-emission temporary housing and optimized travel coordination. Providers are responding through HR technology alliances, regional expansion strategies, and cloud-based mobility service development targeting high-growth industrial and digital infrastructure clusters.

Relocation management providers face increasing execution complexity as enterprises demand seamless integration between mobility platforms, payroll systems, immigration databases, and employee experience applications. More than 46% of global enterprises identified interoperability limitations as a major barrier to scalable mobility deployment, while cybersecurity incidents linked to HR and employee data systems increased by 23% in 2025. Large-scale international assignments require synchronized coordination across tax advisors, housing vendors, logistics operators, and compliance teams, creating operational fragmentation risks. Japan and the United States are witnessing growing pressure to strengthen employee data governance frameworks due to expanding AI-based workforce analytics adoption. Companies are investing in encrypted cloud infrastructure, API-based mobility integration, and cybersecurity partnerships to improve deployment consistency. Solving cross-platform synchronization and data protection challenges remains essential for sustaining enterprise trust and long-term operational competitiveness.

AI Mobility Workflow Expansion Enterprises are accelerating AI-enabled relocation orchestration to reduce assignment processing delays and improve workforce visibility. More than 57% of multinational firms deployed automated relocation tracking systems in 2025, while document processing accuracy improved by 33% compared to manual workflows. U.S.-based HR technology providers are integrating relocation analytics with payroll and immigration platforms following stricter labor compliance monitoring. Companies are responding through software partnerships, centralized mobility operations, and predictive employee support systems that reduce relocation-related administrative workloads and improve deployment consistency.

Flexible Assignment Models Rising Corporate relocation structures are shifting from long-term expatriate deployments toward short-duration and hybrid mobility programs. Nearly 46% of global enterprises expanded rotational assignment policies to control housing and travel expenses, while temporary accommodation utilization increased by 28% across technology and consulting sectors. Germany and Singapore recorded rising demand for project-based mobility tied to semiconductor and digital infrastructure expansion. Relocation providers are restructuring service portfolios with modular housing, digital onboarding, and flexible compliance support designed for shorter workforce transition cycles.

Immigration Compliance Digitization Accelerates Tightening visa documentation requirements and cross-border employment regulations are increasing enterprise investment in digital immigration support tools. More than 39% of relocation providers integrated automated compliance verification systems during 2025, reducing documentation errors by 24%. Canada and the United Kingdom strengthened skilled-worker verification frameworks, pushing corporations toward centralized compliance management. Companies are scaling cloud-based immigration coordination platforms and expanding partnerships with legal advisory firms to improve relocation continuity and reduce assignment disruption risks.

Sustainable Mobility Practices Expanding Enterprises are integrating sustainability metrics into relocation operations as ESG-linked workforce policies gain operational relevance. Low-emission temporary housing adoption increased by 21%, while digitally coordinated relocation logistics reduced unnecessary transportation costs by 17%. Japanese and Nordic corporations are prioritizing carbon-conscious mobility programs tied to internal ESG reporting frameworks. A non-obvious industry shift involves relocation providers using occupancy analytics and localized vendor networks to minimize idle housing inventory. Companies are investing in green accommodation partnerships and centralized travel optimization systems to improve operational efficiency while aligning with evolving corporate sustainability mandates.

International Relocation remains the dominant segment due to rising multinational workforce deployment, immigration compliance requirements, and global project expansion across technology, healthcare, and industrial manufacturing sectors. Nearly 43% of enterprise relocation contracts in 2026 involve cross-border assignments requiring integrated visa processing, housing coordination, and tax compliance support. Employee Relocation is emerging as the fastest-growing segment as corporations increasingly adopt flexible talent redistribution models and hybrid assignment structures, particularly across the United States, India, and Germany. Domestic Relocation continues to hold strategic relevance for manufacturing decentralization and regional office expansion, while Office Relocation demand is strengthening through corporate restructuring and infrastructure modernization initiatives. Mobility Consulting is gaining traction among large enterprises seeking centralized workforce planning and predictive relocation analytics. Relocation providers are expanding cloud-based mobility platforms, compliance partnerships, and destination service capabilities to improve scalability, assignment continuity, and employee experience optimization across diversified workforce mobility programs.

Workforce Mobility represents the leading application segment as multinational enterprises prioritize centralized employee deployment, talent redistribution, and assignment continuity across expanding operational networks. More than 48% of enterprise mobility spending is concentrated in workforce mobility coordination due to rising demand for integrated relocation tracking, immigration management, and employee onboarding support. Immigration Support is the fastest-growing application segment, supported by stricter visa processing frameworks and increasing regulatory oversight in countries including Canada, Australia, and the United Kingdom. Corporate Transfers continue to maintain high deployment volume across financial services and consulting sectors, while Temporary Housing and Logistics Coordination are evolving through digital vendor integration and occupancy optimization systems. Household Relocation demand remains stable for executive and long-duration assignments requiring premium support services. Companies are scaling AI-enabled coordination platforms, cloud-based compliance systems, and flexible relocation ecosystems to improve deployment speed, reduce administrative inefficiencies, and strengthen workforce mobility resilience.

Corporate Enterprises account for the largest share of relocation management services demand due to large-scale workforce mobility requirements, international expansion programs, and high employee transfer volumes across technology, manufacturing, consulting, and logistics industries. Nearly 52% of enterprise mobility contracts in 2026 are linked to multinational corporate restructuring and cross-border talent deployment initiatives. The Healthcare Sector is emerging as the fastest-growing end-user group as hospitals, clinical research organizations, and biotechnology firms accelerate international hiring to address specialized workforce shortages. IT and Telecom companies continue expanding relocation spending through global cloud infrastructure and semiconductor projects, while Financial Services institutions are increasing executive mobility support for regulatory and operational realignment. Government Organizations and Educational Institutions maintain stable demand through diplomatic assignments, academic exchange programs, and research collaborations. Relocation providers are responding through customized mobility packages, sector-specific compliance services, and integrated employee experience platforms designed to strengthen retention and deployment efficiency across high-volume enterprise environments.

North America accounted for the largest market share at 36% in 2025 however, Asia-Pacific is expected to register the fastest growth, expanding at a CAGR of 7.4% between 2026 and 2033.

Enterprise Mobility Consolidation Accelerating Across Strategic Industries

North America maintains leadership in the relocation management services market through high multinational workforce mobility, advanced HR technology integration, and large-scale corporate transfer operations. The region accounts for nearly 36% of global deployment activity, supported by strong enterprise demand across technology, aerospace, healthcare, and financial services sectors. More than 64% of Fortune 500 companies operating in the United States adopted centralized relocation management platforms by 2026 to improve compliance visibility and employee retention efficiency. Supply-chain diversification and semiconductor infrastructure expansion are increasing skilled-worker transfers across the United States and Mexico. Relocation providers are strengthening partnerships with immigration specialists, temporary housing operators, and digital HR platforms to support complex workforce deployment requirements with faster assignment coordination and improved operational scalability.

United States Market Outlook: The United States leads regional demand through high enterprise mobility intensity, large-scale multinational operations, and rapid adoption of AI-enabled relocation coordination systems. Technology, healthcare, and semiconductor industries are driving rising employee transfer volumes linked to domestic manufacturing expansion and cloud infrastructure investment. More than 62% of large U.S. corporations integrated relocation analytics into workforce planning systems during 2026, improving assignment visibility and reducing onboarding disruptions. Immigration compliance complexity and hybrid workforce redistribution are further accelerating demand for centralized mobility ecosystems with integrated tax, housing, and destination support services.

Regulatory Alignment and Workforce Localization Reshaping Mobility Operations

Europe remains a strategically important market due to complex labor regulations, cross-border workforce mobility, and growing demand for centralized compliance management. The region contributes nearly 28% of global relocation deployment activity, supported by strong enterprise mobility demand across Germany, the United Kingdom, France, and the Netherlands. Stricter immigration verification standards and ESG-focused corporate policies are accelerating digital relocation workflow adoption. In 2025, several multinational enterprises expanded regional mobility hubs to reduce relocation approval delays and improve workforce coordination efficiency by over 24%. Industrial modernization projects and skilled-worker shortages across advanced manufacturing and engineering sectors are increasing demand for integrated relocation and immigration support services. Companies are prioritizing localized vendor networks and cloud-based compliance management to improve operational consistency across multiple jurisdictions.

Germany Market Outlook: Germany leads the European relocation management services market through industrial manufacturing strength, engineering workforce mobility, and large-scale enterprise expansion projects. Automotive, industrial automation, and semiconductor sectors are driving increased cross-border employee deployment requirements. More than 41% of multinational employers operating in Germany expanded relocation partnerships during 2026 to manage stricter labor compliance procedures and rising skilled-worker shortages. Enterprise demand is also increasing for multilingual onboarding support, tax coordination, and digital immigration processing integrated with centralized HR infrastructure.

Industrial Expansion and Talent Redistribution Driving Rapid Deployment

Asia-Pacific is witnessing the fastest operational expansion due to accelerating manufacturing investment, technology workforce migration, and multinational supply-chain realignment. The region accounts for nearly 31% of global workforce mobility deployment activity, with rising relocation demand across India, China, Singapore, Vietnam, and Australia. Semiconductor investments, digital infrastructure projects, and industrial decentralization initiatives are significantly increasing skilled labor transfers. In 2026, enterprise relocation automation adoption across major Asia-Pacific business hubs increased by 33%, improving assignment processing speed and compliance coordination efficiency. Companies are expanding regional mobility service networks, cloud-based relocation platforms, and destination management partnerships to support growing international workforce movement tied to industrial and technology expansion.

India Market Outlook: India is emerging as a high-priority relocation management services hub due to rapid technology sector expansion, global capability center growth, and increasing cross-border talent mobility. IT services, engineering, and pharmaceutical industries are driving sustained enterprise relocation demand across Bengaluru, Hyderabad, Pune, and Chennai. More than 48% of multinational corporations expanding operations in India increased investment in integrated workforce mobility support during 2026. Digital onboarding systems, immigration coordination platforms, and flexible employee relocation programs are becoming operationally critical for enterprises scaling high-volume skilled workforce deployment.

Corporate Expansion and Infrastructure Modernization Supporting Mobility Demand

South America is experiencing steady relocation management services expansion through rising multinational investment, infrastructure development, and regional workforce redistribution across energy, mining, logistics, and agribusiness sectors. The region contributes approximately 7% of global enterprise relocation activity, with Brazil and Chile leading deployment concentration. Industrial expansion and nearshoring strategies are increasing demand for cross-border employee transfers and immigration support services. However, operational scalability remains constrained by inconsistent regulatory frameworks and uneven digital infrastructure maturity. In 2025, several relocation providers expanded partnerships with regional housing and logistics operators to improve workforce deployment continuity and reduce assignment delays by nearly 18%. Companies are increasingly adopting centralized mobility coordination to manage compliance complexity and workforce retention across geographically dispersed operations.

Brazil Market Outlook: Brazil dominates the South American relocation management services market through industrial scale, infrastructure modernization initiatives, and expanding multinational business activity. Energy, mining, manufacturing, and logistics industries are increasing workforce mobility requirements linked to operational expansion and supply-chain restructuring. More than 37% of enterprise mobility providers operating in Brazil strengthened digital compliance and relocation coordination capabilities during 2026 to address administrative inefficiencies and immigration processing delays. Large urban business centers including São Paulo and Rio de Janeiro continue attracting regional headquarters expansion and executive relocation activity.

Mega Infrastructure Investment Accelerating Workforce Mobility Systems

The Middle East & Africa market is strengthening through infrastructure megaprojects, economic diversification programs, and rising international workforce deployment across construction, energy, aviation, and digital infrastructure sectors. The region accounts for nearly 6% of global relocation management deployment activity, led by the UAE and Saudi Arabia. Large-scale industrial and smart-city investments are increasing demand for integrated workforce relocation, immigration processing, and temporary housing coordination services. In 2026, enterprise demand for digital relocation management systems across Gulf Cooperation Council countries increased by over 27% as organizations accelerated expatriate workforce expansion. Companies are investing in localized compliance support, multilingual onboarding platforms, and strategic partnerships with housing and logistics providers to improve assignment continuity and workforce integration efficiency.

United Arab Emirates Market Outlook: The United Arab Emirates leads the regional market through aggressive infrastructure modernization, multinational business concentration, and large expatriate workforce dependency. Financial services, aviation, construction, and technology sectors are driving continuous employee mobility demand across Dubai and Abu Dhabi. More than 53% of multinational enterprises operating in the UAE expanded relocation and immigration management partnerships during 2026 to support large-scale workforce deployment linked to smart infrastructure and digital economy initiatives. Advanced digital government systems and streamlined business regulations continue strengthening the country’s operational advantage for enterprise mobility coordination.

The relocation management services market is led by global mobility specialists competing against regional destination-service providers, HR outsourcing firms, and digital workforce mobility platforms. Cartus, Graebel, SIRVA, Aires, and Altair Global collectively control nearly 38% of enterprise relocation contracts, competing through compliance integration, assignment speed, technology automation, and multinational service coverage. Large global players are targeting Fortune 500 clients with AI-enabled mobility dashboards and centralized immigration coordination, while regional operators compete aggressively on localized housing networks and cost flexibility. Automated workflow deployment reduced relocation processing timelines by 27% for leading providers, while cloud-based compliance systems improved assignment visibility by 31%. Competition increasingly centers on ecosystem partnerships involving HR software vendors, immigration consultants, and temporary housing operators. Consolidation pressure is rising as enterprises reduce vendor fragmentation and prioritize scalable mobility platforms. High entry barriers include regulatory complexity, multinational compliance infrastructure, and integrated service-network requirements. Winning requires operational scalability, digital mobility orchestration, and strong enterprise retention capabilities.

Cartus Corporation

Graebel Companies Inc.

SIRVA Worldwide Relocation & Moving

Aires

Altair Global

Crown Worldwide Group

NEI Global Relocation

Weichert Workforce Mobility

Sterling Lexicon

BGRS

XONEX Relocation

Relocity

MoveCenter

Santa Fe Relocation

AI-driven mobility orchestration platforms are transforming relocation management through automated workflow coordination, predictive assignment tracking, and integrated compliance processing. By 2026, nearly 58% of multinational enterprises are expected to deploy cloud-based relocation ecosystems connected with HR, payroll, and immigration systems. AI-enabled document verification tools are reducing manual processing workloads by 34% while improving relocation case accuracy by 27%. Compared with legacy spreadsheet-based coordination systems, integrated mobility platforms improve assignment visibility by nearly 40% and significantly reduce onboarding delays. Large global mobility providers are scaling API-driven infrastructure to strengthen enterprise retention and operational responsiveness.

Emerging technologies including predictive mobility analytics, digital destination intelligence, and automated housing optimization are accelerating enterprise deployment efficiency. More than 43% of relocation providers are integrating machine-learning algorithms to forecast assignment risks, temporary housing demand, and employee transition timelines. Smart relocation dashboards are reducing vendor coordination delays by 22%, particularly across the United States, Germany, and Singapore. Companies with advanced digital mobility infrastructure are gaining competitive advantage through faster deployment cycles, centralized compliance execution, and improved workforce continuity across high-volume international assignments.

Disruptive innovation between 2026 and 2028 will center on AI-assisted immigration management, blockchain-enabled document authentication, and sustainability-linked mobility optimization. Relocation providers deploying real-time workforce analytics and low-emission travel coordination systems are expected to reduce relocation-related operational costs by 18%. Enterprises delaying modernization risk slower deployment execution, fragmented compliance management, and weaker employee mobility scalability.

April 2026 – Graebel launched Catalyst, an executive transition platform developed with Ten Lifestyle Group, targeting faster leadership integration during the first six-to-nine months of relocation operations, strengthening enterprise readiness and employee retention outcomes.

February 2026 – Graebel partnered with Yembo to deploy AI-powered visual claims technology, digitally linking pre-move surveys with relocation claims workflows, accelerating claims verification speed and reducing manual documentation friction for mobile employees. Source: Graebel Insights

January 2026 – Cartus became the first major global talent mobility company with SBTi-validated net-zero targets, committing to reduce scope 1 and 2 emissions 63% by 2035 while strengthening ESG-linked relocation operations. Source: StockTitan

March 2026 – Graebel centralized housing coordination for a global hospitality enterprise, eliminating employee out-of-pocket accommodation expenses while streamlining relocation billing workflows and improving scalable workforce mobility deployment across multiple operational regions. Source: Graebel Case Studies

The report provides comprehensive analysis of relocation management services across Domestic Relocation, International Relocation, Employee Relocation, Office Relocation, and Mobility Consulting segments, with detailed evaluation of Workforce Mobility, Corporate Transfers, Immigration Support, Logistics Coordination, Temporary Housing, and Household Relocation applications. More than 52% of enterprise demand concentration is analyzed across multinational corporate mobility operations, while emerging deployment trends in healthcare, IT infrastructure, and financial services are assessed through operational and technology adoption indicators. The study covers North America, Europe, Asia-Pacific, South America, and Middle East & Africa with country-level industrial and workforce mobility insights.

The report further examines AI-enabled relocation platforms, digital immigration processing, predictive mobility analytics, and cloud-based workforce coordination technologies shaping operational modernization between 2026 and 2033. Strategic assessment includes enterprise deployment models, compliance infrastructure evolution, vendor consolidation activity, sustainability-linked mobility programs, and competitive positioning across high-volume mobility ecosystems. The analysis supports investment prioritization, regional expansion planning, partnership evaluation, operational scalability assessment, and long-term workforce mobility strategy development for enterprises and relocation service providers.

| Report Attribute/Metric | Report Details |

|---|---|

|

Market Revenue in 2025 |

USD 9370 Million |

|

Market Revenue in 2033 |

USD 15047.44 Million |

|

CAGR (2026 - 2033) |

6.1% |

|

Base Year |

2025 |

|

Forecast Period |

2026 - 2033 |

|

Historic Period |

2021 - 2025 |

|

Segments Covered |

By Type

By Application

By End-User

|

|

Key Report Deliverable |

Revenue Forecast, Growth Trends, Market Dynamics, Segmental Overview, Regional and Country-wise Analysis, Competition Landscape |

|

Region Covered |

North America, Europe, Asia-Pacific, South America, Middle East, Africa |

|

Key Players Analyzed |

Cartus Corporation, Graebel Companies Inc., SIRVA Worldwide Relocation & Moving, Aires, Altair Global, Crown Worldwide Group, NEI Global Relocation, Weichert Workforce Mobility, Sterling Lexicon, BGRS, XONEX Relocation, Relocity, MoveCenter, Santa Fe Relocation |

|

Customization & Pricing |

Available on Request (10% Customization is Free) |