Reports

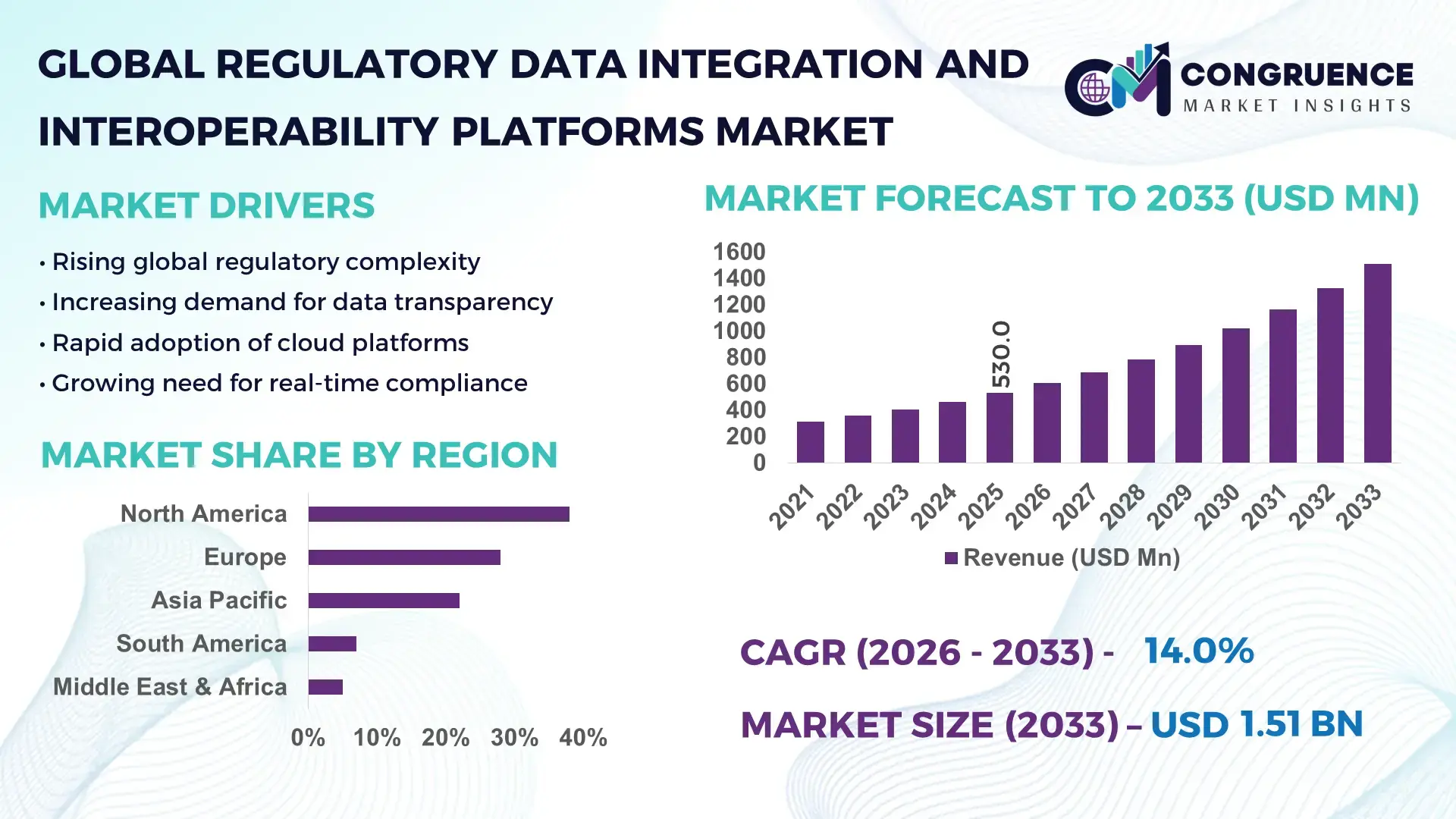

The Global Regulatory Data Integration and Interoperability Platforms Market was valued at USD 530.0 Million in 2025 and is anticipated to reach a value of USD 1,511.9 Million by 2033 expanding at a CAGR of 14.0% between 2026 and 2033, according to an analysis by Congruence Market Insights. The growth is primarily driven by increasing regulatory complexity and cross-border data standardization requirements across industries.

The United States leads the Regulatory Data Integration and Interoperability Platforms Market with strong enterprise-scale deployments and regulatory-driven innovation. Over 68% of large financial institutions in the U.S. have implemented interoperable compliance platforms to streamline reporting across multiple jurisdictions. The healthcare sector accounts for nearly 32% of platform deployments, driven by interoperability mandates such as electronic health record integration. Additionally, federal investments in digital infrastructure exceeded USD 80 billion between 2021 and 2025, supporting advanced API-based data exchange systems. The country also hosts over 45% of global RegTech startups focused on compliance automation and regulatory data harmonization.

Market Size & Growth: USD 530.0 Million in 2025, projected to reach USD 1,511.9 Million by 2033, expanding at 14.0% CAGR, driven by regulatory digitization mandates.

Top Growth Drivers: 65% enterprises adopting compliance automation, 48% improvement in reporting efficiency, 52% rise in API-based integrations.

Short-Term Forecast: By 2028, operational compliance costs expected to reduce by 28% through automation.

Emerging Technologies: AI-driven compliance analytics, blockchain-based audit trails, and API-first interoperability frameworks.

Regional Leaders: North America (~USD 620 Million by 2033) driven by BFSI digitization; Europe (~USD 410 Million) driven by GDPR compliance; Asia-Pacific (~USD 360 Million) driven by fintech expansion.

Consumer/End-User Trends: BFSI and healthcare sectors account for over 58% of platform usage, with rising adoption among government agencies.

Pilot or Case Example: In 2025, a European bank achieved 35% faster regulatory reporting using AI-integrated interoperability systems.

Competitive Landscape: Market leader holds ~18% share, followed by major players including IBM, Oracle, SAP, and Informatica.

Regulatory & ESG Impact: Over 70% firms aligning with ESG compliance reporting frameworks, boosting adoption.

Investment & Funding Patterns: Over USD 2.3 Billion invested globally in RegTech and interoperability platforms between 2023–2025.

Innovation & Future Outlook: Increasing integration of AI, cloud-native platforms, and real-time data validation systems.

The Regulatory Data Integration and Interoperability Platforms Market is shaped by BFSI contributing nearly 38% of demand, followed by healthcare at 26% and government at 18%. Cloud-native platforms account for over 55% of deployments, while API-based integration adoption exceeds 60%. Regulatory frameworks and digital transformation policies continue to accelerate adoption globally, with Asia-Pacific witnessing over 40% increase in enterprise onboarding. Emerging trends include AI-powered compliance monitoring and real-time cross-border data validation systems.

The Regulatory Data Integration and Interoperability Platforms Market plays a critical role in enabling organizations to manage increasingly complex regulatory ecosystems while ensuring seamless data exchange across systems and jurisdictions. These platforms are strategically vital for industries such as banking, healthcare, insurance, and government, where compliance requirements are expanding rapidly. Organizations leveraging AI-driven regulatory platforms report up to 42% improvement in compliance accuracy and a 35% reduction in manual reporting efforts.

Modern interoperability technologies such as API-first architectures deliver 40% faster data exchange compared to legacy batch-processing systems, significantly improving real-time compliance monitoring. North America dominates in volume due to high enterprise digital maturity, while Europe leads in adoption with over 62% of enterprises implementing interoperability frameworks aligned with GDPR and data governance mandates. This regional contrast highlights the importance of regulatory frameworks in shaping adoption trends.

By 2028, AI-enabled regulatory analytics is expected to improve audit efficiency by 45%, enabling predictive compliance and automated risk detection. Firms are also committing to ESG-related data transparency, targeting up to 30% improvement in sustainability reporting accuracy by 2030. In 2025, a U.S.-based financial institution achieved a 38% reduction in compliance processing time through implementation of machine learning-driven regulatory data integration platforms.

As organizations prioritize digital transformation, the Regulatory Data Integration and Interoperability Platforms Market is positioned as a foundational pillar supporting resilience, compliance, and sustainable growth across global industries.

The Regulatory Data Integration and Interoperability Platforms Market is influenced by a combination of regulatory expansion, digital transformation initiatives, and the growing need for real-time data exchange across complex ecosystems. Increasing regulatory mandates across industries such as BFSI, healthcare, and government are driving demand for platforms that enable seamless integration and standardized data reporting. Over 72% of enterprises globally are investing in interoperability solutions to enhance compliance efficiency and reduce operational complexity. Additionally, the rise of cloud computing and API-driven architectures has accelerated adoption, enabling organizations to integrate disparate systems with improved scalability and flexibility. The market is also witnessing growing demand for AI-powered analytics tools that can automate compliance monitoring and risk assessment processes. However, challenges such as data security concerns, integration complexities, and lack of standardized frameworks across regions continue to impact adoption. Overall, the market dynamics reflect a strong shift toward digital compliance ecosystems and real-time regulatory intelligence.

The rapid expansion of global regulatory frameworks is a major driver for the Regulatory Data Integration and Interoperability Platforms Market. Financial institutions alone face over 300 regulatory updates annually, requiring advanced systems for efficient compliance management. Approximately 67% of organizations report challenges in managing multi-jurisdictional compliance requirements, increasing reliance on automated integration platforms. These platforms enable real-time data sharing across departments, reducing reporting errors by nearly 40%. In the healthcare sector, interoperability mandates have led to over 55% of hospitals adopting integrated data systems for compliance reporting. Additionally, governments worldwide are enforcing stricter data governance policies, with over 70 countries implementing data protection regulations. This growing complexity necessitates scalable and intelligent interoperability platforms capable of managing large volumes of structured and unstructured regulatory data efficiently.

Despite strong demand, the complexity associated with implementing regulatory data integration platforms acts as a significant restraint. Around 48% of enterprises report difficulties in integrating legacy systems with modern interoperability frameworks. The lack of standardized data formats across regions further complicates implementation, with over 60% of organizations experiencing delays in deployment timelines. Additionally, high initial setup costs and the need for specialized expertise hinder adoption among small and medium enterprises. Data security concerns also play a critical role, as nearly 52% of organizations cite risks related to data breaches and compliance violations during integration processes. These challenges increase operational risks and slow down decision-making, limiting the pace of market expansion despite growing regulatory pressures.

AI-driven compliance automation presents significant opportunities for market growth by enhancing efficiency and accuracy in regulatory reporting. Organizations adopting AI-based interoperability platforms report up to 45% improvement in data validation processes and a 30% reduction in compliance-related errors. The increasing adoption of machine learning algorithms enables predictive analytics, allowing companies to identify potential compliance risks proactively. In the banking sector, over 50% of institutions are exploring AI-powered solutions for real-time regulatory monitoring. Additionally, the integration of blockchain technology offers opportunities for secure and transparent audit trails, improving trust and accountability. Emerging markets are also witnessing increased adoption, with enterprise digital transformation initiatives growing by over 35%, creating new opportunities for platform providers.

Data standardization remains a critical challenge impacting the Regulatory Data Integration and Interoperability Platforms Market. Approximately 58% of organizations struggle with inconsistent data formats across different regulatory jurisdictions, leading to inefficiencies in reporting processes. The absence of globally unified standards results in duplication of efforts and increased operational costs. In industries such as healthcare, over 45% of data exchange errors are attributed to incompatible data structures. Additionally, frequent updates in regulatory requirements necessitate continuous system upgrades, increasing maintenance complexity. Organizations must also manage large volumes of unstructured data, with over 65% of compliance data requiring transformation before integration. These challenges highlight the need for standardized frameworks and advanced data harmonization tools to ensure seamless interoperability.

AI-driven compliance automation improving efficiency by 40%: Organizations are increasingly deploying AI-powered regulatory platforms, with over 62% of enterprises integrating machine learning models to automate compliance monitoring. These systems reduce manual intervention by 45% and enhance reporting accuracy by 38%, particularly in BFSI and healthcare sectors where data complexity is high.

API-first interoperability adoption exceeding 65% globally: API-based integration frameworks now account for more than 65% of deployments, enabling real-time data exchange across multiple regulatory systems. Enterprises report up to 50% faster data synchronization and 30% reduction in system downtime due to improved interoperability capabilities.

Cloud-native platforms driving 55% of deployments: Cloud-based regulatory data platforms represent over 55% of implementations, offering scalability and cost efficiency. Organizations adopting cloud-native solutions report 35% improvement in operational agility and 28% reduction in infrastructure costs.

Blockchain integration enhancing audit transparency by 33%: The use of blockchain for regulatory audit trails has increased by 27%, enabling secure and tamper-proof data records. Enterprises leveraging blockchain report a 33% improvement in audit transparency and a 25% reduction in compliance-related disputes.

The Regulatory Data Integration and Interoperability Platforms Market is segmented based on type, application, and end-user, each contributing uniquely to overall adoption patterns. Platform-based solutions dominate due to their scalability and ability to handle complex regulatory datasets, while services such as consulting and system integration support implementation across industries. Applications span across compliance reporting, risk management, and data governance, with compliance reporting emerging as a key use case due to stringent regulations. End-users include BFSI, healthcare, government, and manufacturing sectors, with BFSI leading adoption due to high regulatory exposure. Increasing digital transformation and regulatory mandates continue to shape segmentation trends, with growing emphasis on AI-enabled platforms and cloud-based deployment models across industries.

Platform solutions account for approximately 62% of adoption due to their ability to provide end-to-end regulatory data management capabilities. These platforms enable seamless integration, real-time data validation, and automated compliance reporting, making them essential for large enterprises. Services, including consulting and system integration, represent around 38% of the market, supporting implementation and customization requirements. Cloud-based platforms are the fastest-growing segment, expanding at an estimated CAGR of 16.5%, driven by scalability, cost efficiency, and ease of deployment. On-premise solutions continue to serve organizations with strict data security requirements, particularly in government and defense sectors. Hybrid models are also gaining traction, offering flexibility for enterprises managing sensitive and non-sensitive data simultaneously. Other niche types, including blockchain-enabled platforms and AI-driven compliance tools, collectively contribute to around 22% of the market, reflecting growing interest in advanced technologies for regulatory data management.

In 2025, a leading global bank implemented AI-powered interoperability platforms, improving compliance processing efficiency for over 12 million transactions annually.

Compliance reporting dominates with a 44% share, driven by increasing regulatory mandates across industries. Risk management applications account for 28%, while data governance contributes 18%. However, real-time regulatory monitoring is the fastest-growing segment, expected to grow at a CAGR of 17.2% due to demand for proactive compliance strategies. Other applications, including audit management and fraud detection, collectively hold a 30% share, supporting broader regulatory requirements. In 2025, over 41% of enterprises globally reported adopting interoperability platforms for compliance reporting, while 36% implemented solutions for risk management. Additionally, 58% of financial institutions are investing in real-time monitoring systems to enhance regulatory responsiveness.

In 2025, over 200 global financial institutions deployed automated compliance platforms, enabling faster regulatory reporting and improved data accuracy.

The BFSI sector leads with a 46% share due to high regulatory requirements and complex data ecosystems. Healthcare follows with 27%, driven by interoperability mandates and digital health initiatives. Government agencies account for 15%, focusing on data transparency and regulatory enforcement. The fastest-growing segment is healthcare, expanding at a CAGR of 15.8%, supported by increasing adoption of electronic health records and data-sharing standards. Manufacturing and energy sectors contribute a combined 12%, leveraging interoperability platforms for regulatory compliance and reporting. In 2025, over 63% of large enterprises globally adopted regulatory data platforms, while 48% of SMEs initiated pilot programs. Additionally, 54% of healthcare providers are investing in interoperability solutions to improve patient data integration.

In 2025, a national healthcare system implemented interoperability platforms across 120 hospitals, improving patient data accessibility for over 8 million individuals.

North America accounted for the largest market share at 38% in 2025 however, Asia-Pacific is expected to register the fastest growth, expanding at a CAGR of 16.2% between 2026 and 2033.

North America benefits from high digital maturity and regulatory compliance requirements, with over 70% of enterprises adopting interoperability platforms. Europe holds approximately 28% share, driven by strict data protection regulations and increasing enterprise adoption. Asia-Pacific accounts for around 22%, with rapid digital transformation across China, India, and Japan. South America and the Middle East & Africa collectively contribute 12%, with growing investments in digital infrastructure. Increasing government initiatives and enterprise adoption across regions are driving global market expansion.

North America holds approximately 38% market share, driven by strong adoption across BFSI, healthcare, and government sectors. The region benefits from advanced regulatory frameworks and high enterprise IT spending. Over 72% of financial institutions have implemented interoperability platforms to streamline compliance processes. Regulatory initiatives focusing on data transparency and cybersecurity are accelerating adoption. Companies such as IBM are investing in AI-driven compliance solutions, enhancing automation capabilities. Consumer behavior indicates higher adoption among large enterprises, particularly in healthcare and finance, where real-time data integration is critical for compliance and operational efficiency.

Europe accounts for around 28% market share, with key markets including Germany, the UK, and France. The region is characterized by strong regulatory frameworks such as GDPR, driving demand for compliant data integration solutions. Over 62% of enterprises have adopted interoperability platforms to ensure regulatory compliance. Technological advancements in AI and blockchain are further supporting adoption. Companies like SAP are developing advanced compliance solutions tailored to European regulations. Consumer behavior reflects high demand for transparent and explainable systems due to regulatory pressure.

Asia-Pacific holds approximately 22% market share and is the fastest-growing region. China, India, and Japan are key contributors, driven by rapid digitalization and fintech expansion. Over 48% of enterprises in the region are investing in interoperability platforms to support regulatory compliance. Governments are investing heavily in digital infrastructure, accelerating adoption. Companies like Tata Consultancy Services are expanding interoperability solutions across industries. Consumer behavior shows increased adoption driven by mobile-first technologies and digital platforms.

South America accounts for approximately 7% market share, with Brazil and Argentina leading adoption. The region is witnessing increased investment in digital infrastructure and regulatory modernization. Over 35% of enterprises are adopting interoperability platforms to enhance compliance capabilities. Government initiatives aimed at improving data governance are supporting market growth. Regional companies are focusing on developing cost-effective solutions to address local regulatory requirements. Consumer behavior indicates growing demand for localized compliance solutions.

Middle East & Africa holds around 5% market share, with UAE and South Africa as key markets. The region is experiencing increased demand for interoperability platforms in sectors such as oil & gas and government. Over 30% of enterprises are investing in digital transformation initiatives. Governments are implementing policies to enhance data governance and regulatory compliance. Local players are focusing on cloud-based solutions to improve scalability. Consumer behavior reflects increasing adoption driven by digital modernization efforts.

United States – 34% Market share: Strong regulatory frameworks and high enterprise adoption of compliance technologies.

Germany – 12% Market share: Stringent data protection regulations and advanced industrial digitalization initiatives.

The Regulatory Data Integration and Interoperability Platforms Market is moderately fragmented, with over 120 active global and regional players competing across platform development, integration services, and compliance automation solutions. The top five companies collectively account for approximately 42% of the market, indicating a competitive yet consolidated structure among leading players. Major companies are focusing on strategic partnerships, mergers, and product innovations to strengthen their market position. For instance, AI integration and cloud-based platform expansion are key strategic initiatives adopted by leading players to enhance scalability and efficiency.

Innovation remains a critical differentiator, with over 58% of companies investing in AI-driven compliance solutions and advanced analytics capabilities. Additionally, approximately 47% of market participants are expanding their product portfolios to include blockchain-based audit systems and real-time data integration tools. The competitive landscape is also characterized by increasing collaborations between technology providers and regulatory bodies to develop standardized frameworks. Regional players are focusing on niche markets and customized solutions, intensifying competition across segments. Overall, the market is evolving with a strong emphasis on technological innovation and strategic expansion.

Oracle

SAP

Informatica

SAS Institute

TIBCO Software

Microsoft

Salesforce

FIS Global

NICE Actimize

Wolters Kluwer

Thomson Reuters

Qlik

Talend

The Regulatory Data Integration and Interoperability Platforms Market is undergoing rapid technological transformation driven by advancements in artificial intelligence, cloud computing, and data standardization frameworks. AI-powered analytics tools are increasingly used to automate compliance monitoring, with over 60% of enterprises deploying machine learning models to detect anomalies and predict regulatory risks. These systems enhance data accuracy by approximately 35% and reduce manual intervention significantly.

Cloud-native architectures are becoming the backbone of interoperability platforms, accounting for over 55% of deployments. These platforms enable scalable and flexible integration across multiple systems, allowing organizations to manage complex regulatory requirements efficiently. API-driven integration is another key technological trend, with over 65% of platforms utilizing APIs to enable real-time data exchange. This approach improves data synchronization speed by up to 50% and enhances system interoperability.

Blockchain technology is also gaining traction, particularly for audit trails and data integrity verification. Around 28% of organizations are experimenting with blockchain-based compliance systems to ensure secure and tamper-proof records. Additionally, data standardization frameworks such as FHIR in healthcare and open banking APIs are facilitating seamless data exchange across industries. The integration of advanced technologies continues to drive innovation, enabling organizations to achieve higher levels of compliance efficiency and operational transparency.

• In May 2025, IBMin collaboration with EY launched EY.ai for Tax built with watsonx, enabling automated regulatory data integration across 36+ enterprise data sources. The solution is designed to automate up to 80% of foreign tax compliance processes and significantly reduce manual reporting workloads. Source: www.ibm.com

• In June 2025, IBMintroduced an industry-first integration between watsonx.governance and Guardium AI Security, allowing enterprises to validate compliance against 12+ regulatory frameworks including EU AI Act. The platform enables automated governance workflows and real-time risk visibility across AI-driven data environments.

• In October 2025, IBMpartnered with Groq to enhance watsonx Orchestratewith high-speed AI inference capabilities, enabling faster execution of compliance and regulatory workflows. The integration supports enterprise-scale interoperability by accelerating AI-driven data processing across regulated environments.

• In January 2026, IBMcollaborated with e& to deploy agentic AI within governance and compliance systems, enabling real-time regulatory data interpretation and automated decision workflows. The solution integrates over 500 tools and supports enterprise-wide regulatory intelligence with traceable outputs.

The Regulatory Data Integration and Interoperability Platforms Market Report provides a comprehensive analysis of the industry across multiple dimensions, including technology, application, end-user industries, and geographic regions. The report covers platform types such as cloud-based, on-premise, and hybrid solutions, along with integration services that support implementation and customization. It examines key application areas including compliance reporting, risk management, data governance, audit management, and real-time regulatory monitoring.

The report also provides detailed insights into end-user industries such as BFSI, healthcare, government, manufacturing, and energy, highlighting their adoption patterns and operational requirements. BFSI accounts for the largest adoption due to high regulatory complexity, while healthcare is rapidly expanding due to interoperability mandates and digital health initiatives. Additionally, the report analyzes regional markets including North America, Europe, Asia-Pacific, South America, and the Middle East & Africa, offering insights into regional adoption trends, infrastructure development, and regulatory frameworks.

Technological coverage includes AI-driven analytics, API-based integration, cloud-native platforms, and blockchain-enabled compliance systems. The report further explores emerging trends such as real-time data validation, predictive compliance analytics, and ESG-driven reporting requirements. With over 15 key segments analyzed and more than 100 data points included, the report provides a holistic view of the market, enabling stakeholders to make informed strategic decisions and identify growth opportunities across the global landscape.

| Report Attribute / Metric | Details |

|---|---|

| Market Revenue (2025) | USD 530.0 Million |

| Market Revenue (2033) | USD 1,511.9 Million |

| CAGR (2026–2033) | 14.0% |

| Base Year | 2025 |

| Forecast Period | 2026–2033 |

| Historic Period | 2021–2025 |

| Segments Covered |

By Type

By Application

By End-User Insights

|

| Key Report Deliverables | Revenue Forecast; Market Trends; Growth Drivers & Restraints; Technology Insights; Segmentation Analysis; Regional Insights; Competitive Landscape; Regulatory & ESG Overview; Recent Developments |

| Regions Covered | North America; Europe; Asia-Pacific; South America; Middle East & Africa |

| Key Players Analyzed | IBM; Oracle; SAP; Informatica; SAS Institute; TIBCO Software; Microsoft; Salesforce; FIS Global; NICE Actimize; Wolters Kluwer; Thomson Reuters; Qlik; Talend |

| Customization & Pricing | Available on Request (10% Customization Free) |