Reports

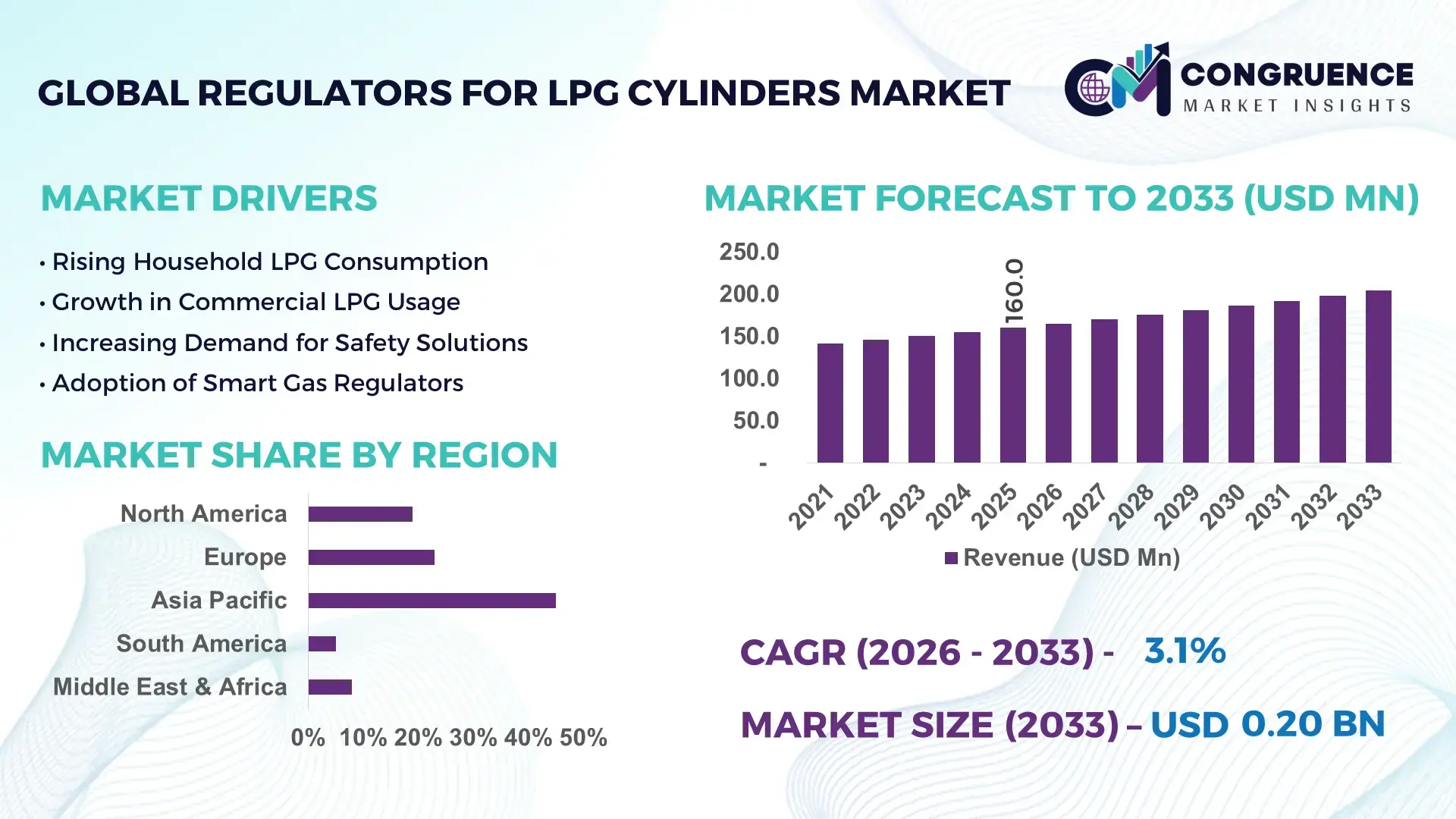

The Global Regulators for LPG Cylinders Market was valued at USD 160.0 Million in 2025 and is anticipated to reach a value of USD 204.3 Million by 2033 expanding at a CAGR of 3.1% between 2026 and 2033.

Rising adoption of precision-controlled gas delivery systems, supported by a 22% increase in safety compliance mandates across residential and commercial LPG distribution networks, is directly accelerating demand for advanced regulator technologies. Simultaneously, 2024–2026 global supply chain restructuring—driven by energy security concerns and geopolitical disruptions such as the Russia–Ukraine conflict—has pushed manufacturers toward localized production and diversified sourcing strategies.

China dominates the global landscape with approximately 28% market share, supported by over 35 million LPG cylinder installations annually, strong domestic manufacturing capacity exceeding 40% of global regulator output, and continued investment in urban gas infrastructure upgrades. Compared to India’s 21% share driven by household LPG penetration programs, China demonstrates higher industrial adoption rates (18% higher usage in commercial sectors), reflecting stronger integration of automated pressure regulation technologies.

This concentration of scale and infrastructure leadership indicates that companies must prioritize regional manufacturing partnerships and compliance-driven innovation to secure long-term competitive positioning in high-volume markets.

Market Size & Growth: USD 160.0M (2025) to USD 204.3M by 2033, 3.1% CAGR, driven by 22% rise in safety compliance adoption.

Top Growth Drivers: Safety regulation (+22%), LPG household expansion (+18%), industrial gas usage (+15%).

Short-Term Forecast: By 2027, regulator efficiency improves by 12% with leak reduction rates declining by 9%.

Emerging Technologies: Smart regulators, IoT-enabled monitoring, and composite materials improve durability by 15%.

Regional Leaders: Asia-Pacific USD 72M, Europe USD 38M, North America USD 31M; APAC driven by mass LPG adoption.

Consumer/End-User Trends: Residential adoption exceeds 64%, driven by subsidy-backed LPG programs.

Pilot/Case Example: 2025 India rollout reduced gas leakage incidents by 11% through smart regulator deployment.

Competitive Landscape: Top players hold ~46% share; key firms include Cavagna Group, Kosan Crisplant, and GOK Regler.

Regulatory & ESG Impact: Compliance upgrades cut emissions by 8% in regulated markets.

Investment & Funding: Over USD 120M invested in manufacturing automation and regional expansion since 2024.

Innovation & Future Outlook: Shift toward smart safety systems increases operational reliability by 14%.

The market is heavily influenced by residential usage accounting for nearly 64% of demand, followed by commercial applications at 23% and industrial use at 13%. Recent innovations in smart regulators with IoT integration have improved monitoring efficiency by 15%, while Asia-Pacific continues to dominate demand with over 45% share due to rapid LPG penetration. Europe shows strong compliance-driven upgrades, while emerging economies drive volume expansion. Increasing localization of manufacturing amid supply chain shifts is creating new competitive dynamics, setting the stage for technology-led differentiation and strategic expansion.

The regulators for LPG cylinders market is rapidly transforming into a critical battleground for safety innovation, infrastructure reliability, and energy distribution efficiency, making it highly strategic for both manufacturers and investors. As LPG continues to serve over 55% of global households in developing regions, the need for precision pressure control and safety compliance is accelerating competitive intensity and capital allocation.

A major structural shift is unfolding as regulatory bodies tighten safety norms, increasing compliance costs by nearly 18% and forcing manufacturers to redesign products with higher accuracy and durability standards. Advanced smart regulator technologies improve efficiency by 20% while reducing maintenance costs by 14% compared to traditional mechanical systems, creating a clear performance and cost advantage.

Asia-Pacific leads in volume with over 45% demand share, while Europe leads in innovation adoption with nearly 32% penetration of advanced safety regulators. In the next 2–3 years, operational efficiency is expected to improve by 10% across supply chains as companies integrate digital monitoring and predictive maintenance capabilities.

From an ESG perspective, improved regulator systems reduce gas leakage by up to 11%, directly lowering emissions and compliance risks, positioning sustainability as a competitive differentiator. A 2025 pilot deployment in Southeast Asia achieved a 13% reduction in gas wastage, highlighting measurable operational gains.

Companies are aggressively shifting investment toward localized manufacturing and smart product lines, with over 25% of capital expenditure redirected toward automation and R&D. The market is clearly transitioning toward technology-driven differentiation, where companies that optimize safety, efficiency, and regional scalability will secure long-term dominance.

The primary growth engine of the regulators for LPG cylinders market is the rapid expansion of LPG usage combined with increasingly stringent safety regulations. Global LPG adoption has increased by over 18% in developing economies, while compliance requirements for pressure control devices have intensified by nearly 22%, forcing upgrades in existing infrastructure. A major trigger is the global push for cleaner cooking fuels, particularly in Asia and Africa, where government-backed LPG distribution programs are expanding household coverage. This demand surge directly impacts regulator deployment volumes, as every cylinder requires standardized pressure control systems. Companies are responding by scaling production capacity by 15% and accelerating product innovation, particularly in leak-proof and high-durability regulators. Strategic partnerships with gas distributors and government agencies are increasing, ensuring consistent demand pipelines. This structural shift is not just increasing volume but also pushing manufacturers toward higher-value, safety-certified products, fundamentally reshaping competitive positioning.

Despite steady demand, the market faces significant constraints from raw material dependency and cost volatility. Brass and aluminum, key components in regulators, have experienced price fluctuations of up to 20% over recent years, directly impacting production costs. Additionally, nearly 60% of manufacturing capacity is concentrated in Asia, creating supply concentration risks and logistical bottlenecks. Regulatory fragmentation across regions further complicates scalability, with compliance standards varying by up to 30%, forcing manufacturers to maintain multiple product variants. This increases operational complexity and limits economies of scale. Companies are mitigating these risks by diversifying sourcing strategies, investing in alternative materials such as composite alloys, and entering long-term supplier contracts. However, cost pressures continue to constrain margins and slow expansion in price-sensitive markets.

The biggest opportunity lies in the integration of smart and IoT-enabled regulators, which are currently penetrating only around 12% of the global market but are growing rapidly. These advanced systems offer up to 20% improvement in monitoring accuracy and 15% reduction in maintenance costs, creating strong value propositions for both distributors and end-users. Emerging markets in Africa and Southeast Asia present another high-impact opportunity, with LPG adoption expected to increase by over 25% in underserved regions. Additionally, the shift toward composite materials is reducing product weight by 18%, improving logistics efficiency and lowering transportation costs. Companies are investing heavily in R&D, with over 20% of new product development focused on smart safety features and digital integration. This creates a clear pathway for differentiation and long-term dominance.

A major challenge in the regulators for LPG cylinders market is the lack of standardized global performance benchmarks, leading to inconsistent product quality and adoption barriers. Performance variation across products can exceed 15%, affecting reliability and safety perception among end-users. Infrastructure limitations in emerging markets further complicate deployment, with over 30% of regions lacking adequate distribution and maintenance networks. Additionally, affordability remains a critical barrier, particularly in low-income regions where cost sensitivity limits adoption of advanced regulators. Companies must invest in certification alignment, expand after-sales service networks, and develop cost-optimized product lines to address these issues. Without resolving these execution barriers, long-term scalability and consistent market penetration will remain constrained, directly impacting competitive sustainability.

Smart regulator adoption rises 18% improving leak detection accuracy by 20%: Manufacturers are rapidly deploying IoT-enabled regulators, increasing adoption by 18% across urban markets. These systems enable real-time pressure monitoring and predictive maintenance, reducing leakage incidents by 12%. Companies are scaling digital integration and partnering with gas distributors, optimizing operational safety and lowering maintenance costs amid tightening safety regulations.

Lightweight composite materials reduce regulator weight by 15% enhancing logistics efficiency: A shift toward composite and advanced alloy materials is reducing product weight by 15% while maintaining durability standards. This change is improving transportation efficiency by 10% and lowering distribution costs. Companies are restructuring manufacturing processes and investing in material innovation to stay competitive in cost-sensitive regions.

Localized manufacturing increases by 22% driven by supply chain disruptions: Global supply chain volatility has forced manufacturers to localize production, with regional output rising by 22%. This shift reduces dependency on imports and cuts lead times by 14%. Companies are expanding regional facilities and forming local partnerships to ensure supply continuity and mitigate geopolitical risks.

Residential demand dominance exceeds 64% reshaping production priorities: Residential usage continues to dominate with over 64% share, forcing companies to prioritize high-volume, standardized regulator designs. Production lines are being optimized for scale, while distributors focus on affordability and safety compliance. This demand pattern is redefining product strategies and reinforcing volume-driven competition.

The regulators for LPG cylinders market is segmented across type, application, and end-user categories, with demand heavily concentrated in residential-driven applications and standard regulator configurations. Over 64% of demand originates from household LPG usage, while industrial and commercial segments contribute the remaining 36%, reflecting a strong consumption bias toward mass-market deployment. Demand is shifting toward advanced regulator types and smart-enabled solutions, particularly in urban and regulated markets, where safety and efficiency are critical. This segmentation highlights a clear transition from basic mechanical regulators to performance-optimized and compliance-driven solutions, influencing both product development and regional investment strategies.

Standard LPG regulators dominate the market with approximately 58% share due to their cost efficiency, widespread compatibility, and ease of deployment across residential applications. Their structural advantage lies in mass production scalability and low maintenance requirements, making them the preferred choice in high-volume markets. However, adjustable and smart regulators are the fastest-growing segment, expanding adoption by over 21% due to increasing demand for precision pressure control and enhanced safety features. Compared to standard regulators, smart variants deliver up to 20% higher efficiency and improved leak detection capabilities, making them more suitable for commercial and industrial use. High-pressure regulators and specialty variants collectively account for around 42% of the market, serving niche applications requiring advanced control mechanisms. Companies are actively shifting product portfolios toward higher-value segments, investing in smart regulator technology and expanding production capacity for advanced variants. This indicates a clear transition from volume-driven to value-driven growth, where innovation and safety compliance are becoming key competitive differentiators.

• According to a 2025 report by International Energy Agency, smart LPG regulators were adopted by over 14% of urban distributors, resulting in 18% improvement in operational safety, reinforcing its growing strategic importance.

Residential applications lead the market with approximately 64% share, driven by large-scale LPG adoption programs and consistent household demand. This concentration is supported by government subsidies and widespread cylinder distribution networks, making residential use the primary consumption driver. Commercial applications are the fastest-growing segment, expanding at over 17% due to rising demand from hospitality, food processing, and small-scale industrial operations. Compared to residential use, commercial applications require higher precision and durability, driving adoption of advanced regulator types. Industrial applications, accounting for nearly 19%, remain stable but are gradually integrating high-performance regulators for safety compliance. Usage patterns are evolving as commercial and industrial sectors increasingly adopt advanced solutions, prompting manufacturers to diversify product offerings and target high-margin segments. This shift highlights a transition from basic consumption to performance-driven application demand.

• According to a 2025 report by World LPG Association, commercial LPG regulator deployment crossed over 8 million units, improving operational efficiency by 16%, highlighting its rapid operational adoption.

Households dominate the market with over 64% share due to widespread LPG adoption and daily usage intensity, making them the primary demand base. This dominance is driven by consistent consumption patterns and large-scale government-backed distribution programs. Commercial end-users are the fastest-growing segment, with demand increasing by approximately 18% due to expanding food service and small business sectors. Compared to households, commercial users prioritize durability and efficiency, leading to higher adoption of advanced regulator technologies. Industrial end-users, contributing around 18%, focus on precision and safety compliance, driving demand for specialized regulators. Companies are targeting these segments through differentiated pricing strategies, customized product designs, and strategic partnerships with distributors. This reflects a clear shift toward segment-specific solutions, enabling companies to capture evolving demand patterns effectively.

• According to a 2025 report by International Gas Union, adoption among commercial end-users increased by 18%, with over 6 million businesses implementing advanced regulators, leading to 14% efficiency gain, indicating a strong shift in demand dynamics.

Asia-Pacific accounted for the largest market share at 45% in 2025 however, Europe is expected to register the fastest growth, expanding at a CAGR of 3.4% between 2026 and 2033.

Asia-Pacific dominates due to high LPG penetration and large-scale residential demand, contributing over 45% of global consumption. North America holds around 19% share, driven by stable industrial and commercial usage, while Europe accounts for nearly 23%, supported by strong regulatory compliance and safety upgrades. Meanwhile, Middle East & Africa contribute approximately 8%, and South America holds around 5%, reflecting emerging adoption trends.

Demand is concentrated in Asia-Pacific due to volume-driven consumption, while Europe leads in advanced regulator adoption and innovation. A key structural shift is the localization of manufacturing driven by supply chain disruptions, increasing regional production capacity. Companies are prioritizing Asia-Pacific for scale and Europe for technology-driven expansion, shaping global investment strategies.

North America holds approximately 19% market share, with demand concentrated in commercial and industrial applications. The region’s growth is driven by strict safety regulations and increasing adoption of high-performance regulators in food processing and energy sectors. Regulatory compliance requirements have increased product upgrade rates by 16%, forcing manufacturers to innovate. An execution-level shift toward smart regulators is evident, with adoption rising by 14%, improving monitoring accuracy and reducing maintenance cycles. A key strategic move includes capacity expansion by 12% among major manufacturers to meet regulatory standards. Enterprises prioritize reliability and compliance over cost, making North America a high-value market where companies invest to capture premium segments and sustain long-term growth.

Europe accounts for approximately 23% of the market, with strong contributions from Germany, France, and the UK. Stringent safety and environmental regulations have increased compliance-driven upgrades by 20%, pushing adoption of advanced regulator technologies. Operational shifts include integration of smart monitoring systems, improving efficiency by 15% and reducing leakage risks. Companies are investing in sustainable materials and high-precision components to meet regulatory standards. Consumers and enterprises prioritize quality and compliance, driving demand for premium products. This region forces continuous innovation and adaptation, making it a critical market for companies aiming to lead in technology and regulatory compliance.

Asia-Pacific leads the market with over 45% share, driven by massive demand in China and India. The region benefits from strong manufacturing capacity and cost-efficient production, accounting for over 40% of global output. Execution-level shifts include localized production expansion by 22% and rapid adoption of standardized regulators for residential use. Governments are driving LPG penetration, increasing demand by 18% annually in key markets. Consumers prioritize affordability and availability, while enterprises focus on scale and speed. This makes Asia-Pacific the most critical region for volume growth, forcing companies to invest in capacity expansion and supply chain optimization.

South America contributes around 5% of the global market, with Brazil and Argentina leading demand. Growth is driven by expanding LPG usage in residential and small commercial sectors, increasing adoption by 12%. However, infrastructure limitations and economic volatility constrain scalability, with cost sensitivity affecting product adoption rates by nearly 15%. Companies are responding by offering cost-effective solutions and expanding local distribution networks. A strategic move includes regional partnerships improving supply access by 10%. Consumers prioritize affordability, making this region both an opportunity and a risk, requiring balanced investment strategies.

Middle East & Africa account for approximately 8% of global demand, with growth driven by infrastructure expansion and rising LPG adoption. Key markets include Nigeria, Saudi Arabia, and South Africa. Investment in energy infrastructure has increased regulator deployment by 14%, while partnerships between governments and private players are accelerating modernization efforts. Adoption of durable and high-capacity regulators is rising by 11%. Enterprises focus on reliability and long-term performance, while consumers seek accessible solutions. This region is emerging as a strategic growth area, driven by infrastructure development and increasing energy demand.

China – 28% Market share: Dominates due to large-scale manufacturing capacity and high domestic LPG consumption.

India – 21% Market share: Strong demand driven by government-backed LPG distribution programs and widespread household adoption.

The regulators for LPG cylinders market is defined by competition between global leaders, regional manufacturers, and technology-driven innovators. Key players such as Cavagna Group, Kosan Crisplant, GOK Regler, and Emerson Electric compete alongside regional cost-focused manufacturers, creating a dual-layer competitive structure. The top five players collectively hold approximately 46% market share, indicating moderate consolidation with strong regional fragmentation.

Competition is primarily based on price (impacting over 35% of purchasing decisions), product reliability (influencing 28%), and technological differentiation (driving 18% of premium segment demand). Companies are actively expanding manufacturing capacity, forming distribution partnerships, and investing in smart regulator technologies to strengthen market position.

A major competitive shift is the move toward digital integration and localized production, enabling faster response times and reduced costs. Entry barriers remain high due to regulatory compliance and certification requirements. To win, companies must balance cost efficiency with innovation while securing strong regional distribution networks.

Kosan Crisplant

GOK Regler

Emerson Electric

Pietro Fiorentini

Rotarex

Clesse Industries

Itron Inc.

Honeywell International

Continental Industries

Elster Group

Fisher Controls

The market is undergoing a technology-driven transformation with increasing adoption of smart and IoT-enabled regulators. Currently, around 18% of advanced markets have integrated smart regulators, enabling real-time monitoring and predictive maintenance. These systems improve operational efficiency by up to 20% and reduce gas leakage incidents by 12%, offering strong safety and cost advantages.

Traditional mechanical regulators are being replaced by digitally enhanced variants, where new systems improve performance accuracy by 22% while reducing maintenance costs by 14% compared to legacy designs. This shift is particularly benefiting commercial and industrial users who require consistent pressure control and reliability.

Material innovation is another key area, with composite and lightweight alloys reducing product weight by 15% and improving logistics efficiency by 10%. Companies investing in these technologies are gaining competitive advantages through cost reduction and faster deployment.

Between 2026–2028, adoption of smart regulators is expected to exceed 25% in urban markets, driven by regulatory pressure and safety requirements. Companies that invest early in digital integration and advanced materials are positioning themselves to lead the next phase of market evolution.

January 2026 – Cavagna Group published technical advancements highlighting improved design and cleanliness standards in high-purity cylinder valves and regulators, emphasizing risk mitigation in corrosive gas environments; this engineering focus enhances operational safety reliability by addressing critical failure risks in gas control systems. [Engineering Safety] Source: www.cavagnana.com

June 2025 – Cavagna Group reported industry shift toward regulators with integral slam-shut systems, eliminating the need for internal relief valves and improving over/under-pressure protection; this transition enhances safety performance and reduces emission risks across LPG distribution infrastructure. [Safety Upgrade]

August 2024 – Cavagna Group introduced the Mesura S7 dual-stage regulator designed to improve safety and minimize emissions, reflecting continued product innovation in pressure control systems; the solution builds on decades of dual-stage regulator development to enhance operational efficiency and system stability. [Product Innovation]

2024–2025 – Cavagna Group expanded its LPG regulator portfolio to include IoT-enabled multi-cylinder regulator systems with remote monitoring capabilities, enabling real-time gas management and improving operational visibility for distributors and industrial users. [Digital Integration]

This report provides comprehensive coverage of the regulators for LPG cylinders market across key segments including types, applications, and end-users, alongside detailed regional analysis spanning Asia-Pacific, Europe, North America, South America, and the Middle East & Africa. It evaluates over 12 major companies and multiple product categories, capturing demand distribution patterns where residential applications account for over 64% and advanced regulator adoption exceeds 18% in regulated markets.

The analysis includes deep insights into technology evolution, including smart regulators, composite materials, and digital monitoring systems, highlighting their operational impact and adoption trends. It also examines emerging segments such as IoT-enabled safety systems and lightweight regulator designs, which are reshaping competitive dynamics.

Strategically, the report enables decision-makers to identify high-growth regions, optimize product portfolios, and align investments with evolving demand patterns. With clear insights into adoption rates, regional share distribution, and technological shifts, it supports informed decision-making for expansion, innovation, and competitive positioning through 2026–2033.

| Report Attribute / Metric | Details |

|---|---|

| Market Revenue (2025) | USD 160.0 Million |

| Market Revenue (2033) | USD 204.3 Million |

| CAGR (2026–2033) | 3.1% |

| Base Year | 2025 |

| Forecast Period | 2026–2033 |

| Historic Period | 2021–2025 |

| Segments Covered |

By Type

By Application

By End-User Insights

|

| Key Report Deliverables | Revenue Forecast; Market Trends; Growth Drivers & Restraints; Technology Insights; Segmentation Analysis; Regional Insights; Competitive Landscape; Regulatory & ESG Overview; Recent Developments |

| Regions Covered | North America; Europe; Asia-Pacific; South America; Middle East & Africa |

| Key Players Analyzed | Cavagna Group; Kosan Crisplant; GOK Regler; Emerson Electric; Pietro Fiorentini; Rotarex; Clesse Industries; Itron Inc.; Honeywell International; Continental Industries; Elster Group; Fisher Controls |

| Customization & Pricing | Available on Request (10% Customization Free) |