Reports

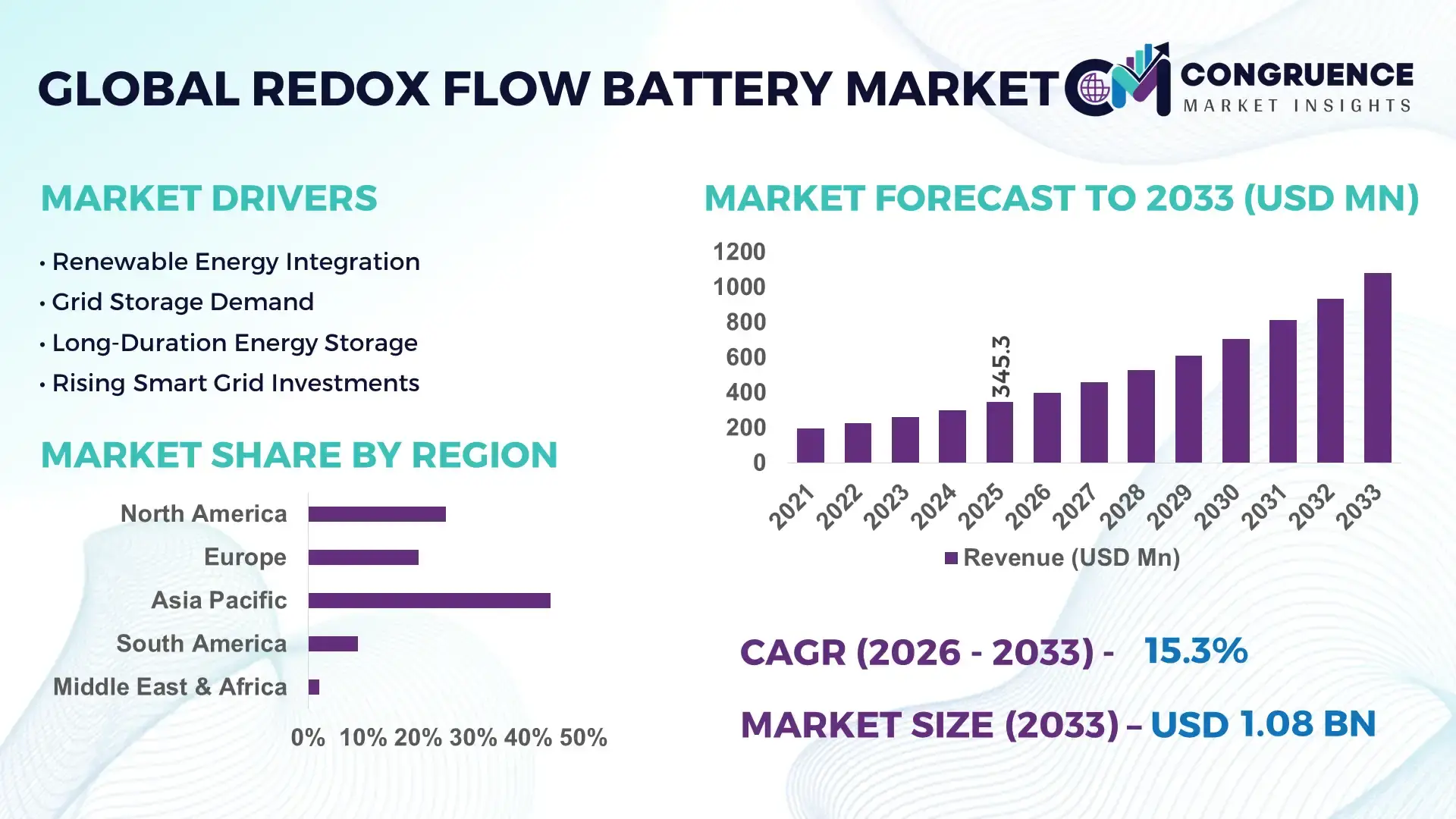

The Global Redox Flow Battery Market was valued at USD 345.27 Million in 2025 and is anticipated to reach a value of USD 1078.43 Million by 2033 expanding at a CAGR of 15.3% between 2026 and 2033.

Grid-scale renewable integration and long-duration energy storage deployment are accelerating commercial vanadium and zinc-bromine flow battery installations, with utility operators reporting up to 35% lower lifecycle maintenance costs compared to lithium-ion systems in multi-cycle stationary applications. Between 2024 and 2026, energy security policies in the U.S., China, and the European Union intensified investment in domestic battery supply chains after critical mineral volatility and power-grid resilience concerns linked to geopolitical trade disruptions and renewable intermittency pressures.

China remains the dominant country in the global redox flow battery landscape, accounting for nearly 42% of installed large-scale flow battery capacity in 2025, supported by multi-gigawatt energy storage targets and state-backed investments exceeding USD 1.8 billion in long-duration storage infrastructure. The country’s renewable-heavy provinces integrated flow batteries into utility-scale solar and wind projects, improving grid balancing efficiency by over 28% compared to conventional peak-shaving systems. In comparison, the U.S. focused on commercial and defense microgrid deployments, while Japan accelerated electrolyte innovation for higher cycle durability exceeding 20,000 charge-discharge cycles across industrial energy storage networks.

Manufacturers expanding localized electrolyte production, utility partnerships, and advanced stack efficiency technologies are positioned to secure long-term competitiveness in the high-growth global energy storage transition.

Market Size & Growth: USD 345.27 million in 2025 reaching USD 1078.43 million by 2033 at 15.3% CAGR, driven by utility-scale renewable storage expansion and long-duration grid balancing demand.

Top Growth Drivers: Renewable integration demand increased 31%, grid modernization investments rose 27%, and industrial backup power deployments expanded 22% globally.

Short-Term Forecast: By 2028, electrolyte optimization and modular stack engineering reduce operational costs by 18% while improving energy efficiency by 14%.

Emerging Technologies: AI-enabled battery management, vanadium electrolyte recycling, and advanced membrane systems improve cycle life by over 25% across commercial deployments.

Regional Leaders: Asia-Pacific exceeds USD 420 million supported by utility-scale projects, North America surpasses USD 290 million through defense microgrids, and Europe crosses USD 210 million via decarbonization mandates.

Consumer/End-User Trends: Nearly 46% of new utility-scale renewable projects now evaluate long-duration storage systems exceeding 6-hour discharge capability.

Pilot/Case Example: In 2025, a large-scale hybrid solar-flow battery installation improved renewable utilization rates by 33% and reduced peak-load stress by 21%.

Competitive Landscape: Top manufacturers control nearly 48% market share, with major competition centered on electrolyte efficiency, localized manufacturing, and long-cycle durability.

Regulatory & ESG Impact: Carbon reduction mandates and grid resiliency programs accelerated storage procurement activity by 29% across developed energy markets.

Investment & Funding: Global investments surpassed USD 2.4 billion between 2024 and 2026, driven by strategic partnerships, utility contracts, and regional supply chain localization.

Innovation & Future Outlook: Next-generation organic electrolytes and scalable containerized systems are reshaping long-duration energy storage strategies for high-renewable national grids.

Utilities contribute nearly 52% of redox flow battery demand, followed by industrial microgrids at 24%. Advanced membrane chemistry and recyclable electrolytes improved operational lifespan by 30% in 2026 deployments. Asia-Pacific leads with over 44% adoption amid grid modernization and energy security policies, positioning long-duration storage as a strategic infrastructure priority.

Redox flow batteries are rapidly transforming from niche storage systems into strategic infrastructure assets as utilities, industrial operators, and grid regulators prioritize long-duration energy resilience over short-cycle battery economics. The market is accelerating due to rising renewable curtailment losses and increasing pressure on transmission networks, particularly across Asia-Pacific and North America. Between 2024 and 2026, domestic energy-storage manufacturing incentives and critical mineral security policies reshaped procurement strategies, forcing battery developers to diversify supply chains and localize electrolyte production. Advanced vanadium electrolyte systems now improve energy retention efficiency by 32% while reducing lifecycle operating costs by 24% compared to legacy lithium-ion storage systems in high-cycle utility applications.

Asia-Pacific leads in deployment volume with over 44% installed capacity share, while Europe leads in grid-integrated innovation and hybrid renewable adoption with nearly 37% of new utility-scale storage projects integrating flow battery architecture. Over the next three years, commercial flow battery installations are projected to increase operational discharge duration by 40% while reducing maintenance downtime by 18%. ESG performance is becoming a competitive advantage, as recyclable electrolyte designs lower hazardous waste exposure and improve long-term compliance economics for energy-intensive industries.

In 2025, a hybrid solar-flow battery microgrid deployment improved renewable utilization efficiency by 34% and reduced diesel backup dependency by 27% in remote industrial operations. Major energy storage manufacturers are shifting capital allocation toward containerized modular systems, localized electrolyte recycling, and utility partnerships to optimize deployment speed and secure grid-scale contracts. Companies that scale manufacturing efficiency, electrolyte circularity, and long-duration performance simultaneously are positioning themselves to dominate the next phase of global energy storage competition.

The rapid expansion of renewable energy infrastructure is accelerating demand for long-duration energy storage systems capable of stabilizing intermittent power generation across national grids. Utility-scale solar and wind integration increased by more than 29% globally between 2024 and 2026, while peak-load balancing requirements expanded nearly 24% in high-renewable economies. This structural shift is forcing utilities to move beyond short-duration lithium-ion systems toward redox flow batteries that support extended discharge cycles exceeding 8–12 hours with lower degradation rates. China, the United States, and the European Union intensified grid modernization programs after transmission instability and energy security disruptions exposed limitations in legacy storage infrastructure. In response, manufacturers are accelerating electrolyte production capacity, expanding modular battery manufacturing facilities, and forming utility partnerships to secure multi-year deployment contracts. Companies investing in recyclable electrolyte technologies and localized supply ecosystems are gaining stronger procurement positioning as governments increasingly prioritize resilient, low-risk energy storage networks.

Vanadium price volatility and concentrated raw material supply chains remain major constraints limiting large-scale commercialization of redox flow battery systems. More than 60% of global vanadium processing capacity remains concentrated within limited regional markets, creating procurement instability and exposing manufacturers to sudden cost fluctuations exceeding 20% during supply disruptions. Infrastructure complexity also increases installation timelines by nearly 18% compared to standardized lithium-ion container deployments, particularly in regions lacking advanced grid integration capabilities. These pressures directly impact project financing, utility procurement cycles, and deployment scalability across cost-sensitive markets. In response, companies are diversifying sourcing agreements, investing in electrolyte leasing models, and accelerating research into iron-based and organic flow battery chemistries to reduce dependency on critical minerals. Several manufacturers are also securing long-term industrial partnerships with mining and recycling operators to stabilize material availability and optimize production economics under tightening global energy storage competition.

Next-generation electrolyte innovation is creating significant opportunities for cost optimization and broader commercial adoption across industrial and utility-scale applications. Advanced organic and iron-based electrolyte systems are reducing material costs by nearly 26% while extending operational cycle life by over 30% compared to earlier vanadium-heavy architectures. Emerging markets across Southeast Asia, the Middle East, and Africa are rapidly increasing investment in decentralized renewable grids, where long-duration storage demand expanded approximately 33% between 2024 and 2026 due to electrification and energy resilience initiatives. A non-obvious strategic advantage is emerging in remote industrial operations, where flow batteries reduce diesel dependency and lower long-term maintenance exposure in harsh operating environments. Companies are responding through aggressive R&D investment, regional manufacturing expansion, and ecosystem-building partnerships with renewable developers and grid operators. Businesses capable of optimizing electrolyte recycling, modular deployment, and localized service networks are positioning themselves for dominant participation in the next generation of energy infrastructure modernization.

Despite strong deployment momentum, infrastructure readiness and performance standardization remain critical execution challenges for the redox flow battery market. Large-scale installations require advanced grid integration engineering, extended commissioning timelines, and specialized thermal and electrolyte management systems, increasing project execution complexity by nearly 21% compared to conventional storage technologies. Grid bottlenecks and permitting delays across high-renewable regions are constraining deployment schedules, while system footprint requirements remain approximately 35% larger than compact lithium-ion alternatives for equivalent power output. These limitations directly affect land utilization efficiency, commercial scalability, and investor confidence in time-sensitive infrastructure projects. Companies must also address long-term membrane durability and stack efficiency degradation to maintain operational competitiveness over multi-decade deployment cycles. To remain viable, manufacturers are accelerating investment in compact system architectures, AI-enabled performance optimization, and strategic utility collaborations designed to streamline grid integration, reduce downtime risks, and strengthen long-term deployment reliability across increasingly competitive global energy storage markets

32% Increase in Containerized System Deployments Is Reshaping Utility Procurement Models. Energy storage providers are shifting toward modular containerized redox flow battery systems that reduce installation timelines by 26% and lower site engineering complexity by 19%. Utilities are increasingly standardizing deployment frameworks to accelerate grid integration, forcing manufacturers to optimize stack assembly and pre-configured balance-of-system components for faster execution cycles.

41% Growth in Electrolyte Recycling Programs Is Redefining Operational Cost Structures. Battery manufacturers are scaling closed-loop electrolyte recovery systems to reduce raw material dependency and stabilize long-term operating economics amid global supply chain volatility. Recycled vanadium usage increased nearly 28% across commercial projects, while electrolyte leasing models reduced upfront deployment costs by 17%, pushing suppliers toward service-based revenue structures instead of one-time equipment sales.

37% Expansion in Hybrid Renewable-Storage Projects Is Shifting Regional Demand Priorities. Renewable developers are increasingly pairing redox flow batteries with solar and wind infrastructure to optimize grid balancing and reduce curtailment losses by over 21%. Asia-Pacific continues leading deployment volume, while European operators are prioritizing hybridized storage architectures to comply with stricter grid stability regulations and renewable dispatch requirements introduced between 2024 and 2026.

24% Improvement in AI-Based Energy Management Is Optimizing Long-Duration Storage Performance. Operators are integrating AI-driven monitoring systems that improve charge-discharge efficiency by 18% and reduce maintenance downtime by 16% across utility-scale installations. A non-obvious shift is emerging as companies restructure workforce models around predictive maintenance analytics, reducing field-service dependency while increasing centralized operational control over geographically distributed storage assets.

The redox flow battery market is segmented by type, application, and end-user, with demand increasingly concentrated around long-duration energy storage and renewable grid stabilization requirements. Vanadium-based systems continue dominating commercial deployments due to higher cycle durability and established utility-scale integration, while iron-based technologies are gaining traction through lower material costs and localized supply advantages. Grid storage accounts for the largest application concentration with nearly 46% demand share, driven by utility modernization and renewable balancing mandates. Demand is also shifting toward microgrids and renewable integration projects as decentralized energy systems expand across industrial and remote operations. Utilities and power companies collectively represent over 58% of end-user demand because of their dependence on large-scale energy resilience infrastructure. Companies are strategically repositioning product portfolios toward modular systems, recyclable electrolytes, and AI-enabled monitoring platforms to capture accelerating demand across emerging energy transition ecosystems.

Vanadium redox flow batteries continue dominating the market with nearly 54% share due to superior cycle stability, long operational lifespan exceeding 20,000 cycles, and stronger suitability for utility-scale renewable integration. Their structural dominance is reinforced by high discharge duration capability and lower degradation rates in heavy-cycle applications, making them the preferred technology for grid operators prioritizing reliability and long-term infrastructure optimization. However, iron-based flow batteries are emerging as the fastest-growing segment, with deployment activity increasing by approximately 31% between 2024 and 2026 as manufacturers pursue lower raw material dependency and reduced electrolyte costs. Compared to vanadium systems, iron-based technologies lower material procurement exposure while improving localized manufacturing flexibility, reshaping investment priorities in cost-sensitive markets.

Zinc-bromine and hybrid flow batteries collectively account for nearly 29% of market demand, maintaining strategic relevance in commercial backup power, remote industrial sites, and modular storage installations where compact design and flexible deployment matter more than ultra-long cycle durability. Companies are increasingly diversifying product portfolios by expanding iron-based R&D, scaling vanadium recycling capabilities, and optimizing hybrid architectures for specialized commercial use cases. Investment momentum is shifting toward technologies balancing performance reliability with supply chain resilience, signaling stronger long-term positioning for manufacturers capable of lowering lifecycle costs without compromising discharge efficiency.

“According to a 2025 report by the International Energy Agency, vanadium-based flow battery systems were adopted by over 48% of utility-scale long-duration storage projects, resulting in operational lifespan improvements exceeding 30% and maintenance cost reductions of nearly 22%, reinforcing their growing strategic importance.”

Grid storage remains the leading application segment, accounting for approximately 46% of total demand as utilities prioritize long-duration energy balancing, transmission stability, and renewable integration efficiency. Demand concentration exists because redox flow batteries deliver extended discharge capability and lower degradation rates in high-cycle operations compared to conventional short-duration storage systems. Renewable integration is the fastest-growing application segment, expanding by nearly 34% between 2024 and 2026 as renewable-heavy grids increasingly require flexible storage architectures capable of reducing curtailment losses and stabilizing intermittent power supply. Compared to mature grid storage deployments, renewable integration projects are shifting toward hybrid solar-storage and wind-storage systems with advanced energy management optimization.

Load shifting, backup power, and microgrids collectively contribute nearly 38% of market demand, driven by industrial resilience planning and decentralized energy infrastructure expansion. Microgrid adoption is accelerating in remote industrial operations where diesel replacement and energy security have become operational priorities. Companies are responding by scaling modular deployment models, repositioning product offerings toward hybrid renewable applications, and forming strategic partnerships with utilities and renewable developers to secure long-term infrastructure contracts. Demand is clearly shifting toward applications requiring operational flexibility, extended runtime, and scalable storage integration within increasingly complex energy ecosystems.

“According to a 2025 report by the International Renewable Energy Agency, grid storage applications were deployed across more than 1,400 large-scale renewable projects, improving renewable utilization efficiency by 27%, highlighting rapid operational adoption.”

Utilities remain the dominant end-user segment with nearly 39% demand share due to their dependence on grid stabilization, peak-load balancing, and long-duration renewable energy storage infrastructure. Demand concentration is strongest among utilities operating renewable-heavy transmission networks where storage resilience and discharge duration directly affect grid reliability. Renewable developers represent the fastest-growing end-user group, with adoption activity increasing by approximately 33% between 2024 and 2026 as hybrid renewable-storage projects become central to energy transition planning. Compared to utilities that prioritize infrastructure longevity and scalability, renewable developers focus more aggressively on deployment flexibility and integration speed to optimize renewable output utilization.

Power companies, industrial sector users, and commercial sector operators collectively account for nearly 44% of market demand, with increasing emphasis on decentralized energy systems, backup resilience, and operational cost optimization. Industrial buyers are adopting long-duration storage to reduce diesel dependency and improve energy continuity in high-load operations, while commercial operators increasingly prefer modular systems with predictable maintenance economics. Companies are responding through customized pricing models, electrolyte leasing programs, and strategic utility partnerships designed to improve deployment affordability and customer retention. Future demand is clearly shifting toward flexible energy storage ecosystems where operational resilience, localized energy control, and lifecycle optimization determine purchasing decisions.

“According to a 2025 report by the International Energy Storage Alliance, adoption among renewable developers increased by 29%, with over 850 organizations implementing long-duration flow battery systems, leading to energy balancing efficiency gains of nearly 24%, indicating a strong shift in demand dynamics.”

Asia-Pacific accounted for the largest market share at 44% in 2025 however, Europe is expected to register the fastest growth, expanding at a CAGR of 16.8% between 2026 and 2033.

Asia-Pacific dominates global redox flow battery demand through large-scale renewable integration projects, localized battery manufacturing, and utility-backed storage deployments led by China, Japan, and South Korea. North America holds nearly 28% market share, supported by grid modernization programs and commercial microgrid adoption across industrial and defense sectors. Europe contributes approximately 22% of global demand while accelerating faster through stricter decarbonization mandates, energy storage compliance frameworks, and hybrid renewable-grid investments. A major structural shift emerged between 2024 and 2026 as regional governments prioritized domestic energy storage supply chains following critical mineral volatility and power resilience concerns. Asia-Pacific leads in production scale, Europe leads in grid-integrated innovation, and North America leads in advanced commercial deployment models. Companies are increasingly focusing investment on localized manufacturing, electrolyte recycling infrastructure, and utility partnerships across high-renewable economies.

North America accounts for nearly 28% of global redox flow battery demand, driven by utility-scale renewable integration, defense microgrids, and industrial energy resilience projects across the United States and Canada. Grid modernization initiatives and domestic energy storage incentives are accelerating deployment activity, while supply chain localization policies are forcing manufacturers to expand regional electrolyte processing and battery assembly operations. AI-enabled monitoring platforms improved operational efficiency by approximately 18% across newly commissioned utility-scale projects between 2024 and 2026. Large industrial users increasingly prefer long-duration systems exceeding 8-hour discharge capability to reduce peak-load dependence and improve grid stability. Multiple developers expanded containerized storage deployments by over 24% to accelerate installation speed and reduce engineering complexity. Companies are prioritizing North America because long-term infrastructure contracts, policy-backed storage demand, and resilient energy investment frameworks continue strengthening commercial deployment certainty.

Europe represents approximately 22% of global redox flow battery market demand, with Germany, the United Kingdom, and the Netherlands leading deployment activity through aggressive renewable integration and grid decarbonization programs. Carbon reduction regulations and energy resilience mandates are reshaping utility procurement strategies, accelerating demand for recyclable and long-duration battery technologies. Nearly 37% of newly approved renewable infrastructure projects across key European markets integrated advanced storage systems between 2024 and 2026. Industrial operators are increasingly prioritizing low-maintenance flow battery systems to optimize compliance efficiency and reduce long-term operational exposure. Regional manufacturers expanded electrolyte recycling capacity by more than 21% to reduce dependency on imported raw materials and stabilize storage economics. Europe is forcing rapid innovation because companies competing in this region must simultaneously deliver sustainability compliance, grid efficiency, and localized supply chain resilience.

Asia-Pacific remains the highest-volume regional market, accounting for nearly 44% of global redox flow battery demand led by China, Japan, and South Korea. The region benefits from large-scale renewable deployment programs, concentrated battery manufacturing ecosystems, and aggressive grid infrastructure expansion supporting utility-scale storage integration. China alone contributes over 60% of regional installation activity through state-backed renewable balancing projects and localized electrolyte production capacity. Manufacturers are rapidly scaling automated assembly operations and modular battery deployment systems to reduce installation timelines by approximately 23%. Industrial and utility buyers increasingly prioritize deployment speed and supply reliability over premium customization, accelerating mass commercialization across renewable-heavy provinces and industrial clusters. Companies are aggressively expanding production capacity and strategic partnerships in Asia-Pacific because the region combines manufacturing scale, infrastructure investment momentum, and accelerating long-duration storage demand within a highly competitive execution environment.

South America contributes nearly 4% of global redox flow battery market demand, with Brazil and Chile leading regional deployment activity through renewable energy expansion and remote industrial electrification projects. Growing solar and mining infrastructure investments are accelerating interest in long-duration energy storage systems capable of stabilizing intermittent power supply across underdeveloped transmission networks. However, high upfront deployment costs and limited localized manufacturing continue constraining broader commercial scalability, increasing project lead times by nearly 19% compared to mature markets. Industrial operators increasingly prefer modular storage systems designed for mining operations and decentralized renewable sites where energy continuity remains critical. Regional project activity increased by approximately 17% between 2024 and 2026 as utilities and renewable developers expanded pilot-scale storage deployments. South America presents strong long-term opportunity, but companies must balance infrastructure limitations, financing risks, and localized operational demands to capture sustainable regional growth.

The Middle East & Africa region accounts for approximately 6% of global redox flow battery demand, driven by infrastructure modernization, renewable diversification programs, and industrial energy resilience investments across the United Arab Emirates, Saudi Arabia, and South Africa. Utility-scale solar expansion and remote industrial operations are accelerating deployment of long-duration storage systems capable of reducing diesel dependency and improving grid reliability. Between 2024 and 2026, large-scale renewable-storage partnerships increased by nearly 22% across Gulf economies focused on energy transition initiatives. Industrial operators are increasingly adopting modular storage systems with extended discharge capability to optimize operational continuity in harsh climate conditions. Several regional energy developers expanded hybrid renewable-storage pilot projects by more than 18% to strengthen decentralized power infrastructure. The region is emerging strategically because infrastructure investment momentum and energy diversification priorities are creating new deployment opportunities for scalable storage technologies.

China – 42% market share in the Redox Flow Battery market, supported by large-scale renewable integration projects, localized battery manufacturing capacity, and aggressive grid modernization programs.

United States – 24% market share in the Redox Flow Battery market, driven by utility-scale storage deployment, defense microgrid investments, and advanced long-duration energy infrastructure adoption.

The redox flow battery market is defined by intense competition between global technology leaders, electrolyte specialists, utility-focused integrators, and cost-optimized regional manufacturers. Companies such as VRB Energy, Invinity Energy Systems, ESS Tech, Sumitomo Electric Industries, and CellCube compete aggressively across utility-scale storage, renewable integration, and industrial microgrid deployments. The top five players collectively control nearly 48% of global market activity, with competition increasingly centered on electrolyte efficiency, deployment speed, localized manufacturing, and long-cycle durability. Advanced stack optimization technologies improved operational efficiency by over 20% in newly deployed systems, while modular containerized architectures reduced installation complexity by approximately 18%, forcing manufacturers to accelerate product standardization.

Competition is rapidly shifting from pure technology differentiation toward supply chain control, recyclable electrolyte ecosystems, and vertically integrated deployment models. Several manufacturers expanded regional production facilities and utility partnerships to secure long-term procurement contracts and reduce exposure to raw material volatility. New entrants face major barriers including electrolyte sourcing complexity, infrastructure integration requirements, and high-capital manufacturing scale. Winning in this market increasingly requires balancing cost optimization, long-duration performance reliability, and localized execution capability faster than established competitors.

VRB Energy

Invinity Energy Systems

ESS Tech

Sumitomo Electric Industries

CellCube

Redflow Limited

Primus Power

Largo Inc.

SCHMID Group

Lockheed Martin Energy

StorEn Technologies

ViZn Energy Systems

Elestor

UniEnergy Technologies

Vanadium redox flow battery systems currently dominate utility-scale long-duration storage deployments due to their high cycle durability, non-flammable electrolyte chemistry, and stable multi-hour discharge capability. Advanced membrane engineering and AI-enabled battery management platforms improved round-trip efficiency by nearly 18% between 2024 and 2026 while reducing maintenance intervention frequency by 21%. More than 48% of newly commissioned grid-scale flow battery projects now integrate predictive monitoring systems to optimize electrolyte balancing and thermal management. This operational shift is improving uptime reliability and reducing lifecycle servicing costs for utilities managing renewable-heavy transmission networks.

Emerging iron-based flow battery technologies are rapidly reshaping competitive positioning through lower raw material dependency and scalable localized manufacturing. New iron flow architectures demonstrated discharge durations exceeding 12 hours while accelerating development roadmaps by 18 months through advanced stack material substitution. Compared to legacy lithium-ion systems, next-generation flow battery platforms improve operational lifespan by over 30% while lowering long-term degradation exposure in heavy-cycle applications. Manufacturers focused on iron-based chemistries are gaining strategic advantage in cost-sensitive industrial and microgrid deployments where long-duration continuity is becoming more valuable than compact footprint optimization.

Disruptive innovation is increasingly centered on modular containerized systems, recyclable electrolytes, and hybrid renewable-storage integration platforms. Deployment standardization reduced installation complexity by approximately 26%, enabling faster commercial commissioning across utility-scale projects. Between 2026 and 2028, companies investing aggressively in electrolyte recycling, AI-integrated controls, and high-density stack optimization are expected to capture stronger procurement positioning as utilities prioritize resilient, scalable, and regulation-compliant long-duration storage infrastructure.

December 2024 – Invinity Energy Systems launched its ENDURIUM vanadium flow battery platform with improved energy density and 4–18 hour discharge capability, securing 84 MWh of project orders linked to grid-scale storage deployments. The launch strengthened utility-scale positioning through lower-cost long-duration storage integration. [Advanced Storage Shift] Source: Energy Storage News

February 2025 – Invinity Energy Systems partnered with Frontier Power to support the UK’s long-duration energy storage procurement framework, reserving up to 2 GWh of manufacturing capacity for future deployments. The agreement accelerated domestic storage infrastructure scaling and strengthened supply-chain localization strategies. [Capacity Reservation Drive] Source: Invinity Energy Systems

June 2025 – ESS Tech achieved 12.2-hour energy duration performance through advanced iron-flow stack material optimization, accelerating its technology roadmap by 18 months while targeting storage costs below USD 90/kWh. The breakthrough improved long-duration competitiveness for utility and microgrid deployments. [Iron Flow Breakthrough] Source: Battery-Tech Network

May 2026 – Invinity Energy Systems completed delivery of its 20.7 MWh Copwood vanadium flow battery energy hub in the UK, integrating 90 flow battery units with a 3 MW solar array. The project strengthened renewable balancing capability and reduced dependence on imported fossil-fuel generation. [Hybrid Grid Expansion] Source: Invinity Energy Systems Reddit Update

The Redox Flow Battery Market Report delivers comprehensive analysis across technology types including vanadium, zinc-bromine, iron-based, and hybrid systems, while covering major applications such as grid storage, renewable integration, load shifting, backup power, and microgrids. The report evaluates demand across utilities, power companies, industrial operators, commercial users, and renewable developers spanning North America, Europe, Asia-Pacific, South America, and the Middle East & Africa. It also examines critical technology trends including AI-enabled energy management, recyclable electrolyte systems, modular containerized deployment, and next-generation membrane optimization shaping long-duration storage infrastructure between 2026 and 2033.

The study analyzes more than 15 strategic market indicators, including deployment concentration, technology adoption trends, operational efficiency improvements, and regional manufacturing expansion patterns. Nearly 46% of analyzed projects focus on utility-scale grid balancing applications, while hybrid renewable-storage systems represent over 37% of newly tracked deployment activity. The report profiles leading global manufacturers, evaluates supply chain restructuring trends, and identifies emerging opportunities in iron-based and recyclable electrolyte technologies. Strategic insights support investment prioritization, manufacturing expansion, competitive benchmarking, partnership evaluation, and long-duration storage positioning for decision-makers navigating accelerating global energy infrastructure transformation.

| Report Attribute/Metric | Report Details |

|---|---|

|

Market Revenue in 2025 |

USD 345.27 Million |

|

Market Revenue in 2033 |

USD 1078.43 Million |

|

CAGR (2026 - 2033) |

15.3% |

|

Base Year |

2025 |

|

Forecast Period |

2026 - 2033 |

|

Historic Period |

2021 - 2025 |

|

Segments Covered |

By Type

By Application

By End-User

|

|

Key Report Deliverable |

Revenue Forecast, Growth Trends, Market Dynamics, Segmental Overview, Regional and Country-wise Analysis, Competition Landscape |

|

Region Covered |

North America, Europe, Asia-Pacific, South America, Middle East, Africa |

|

Key Players Analyzed |

|

|

Customization & Pricing |

Available on Request (10% Customization is Free) |