Reports

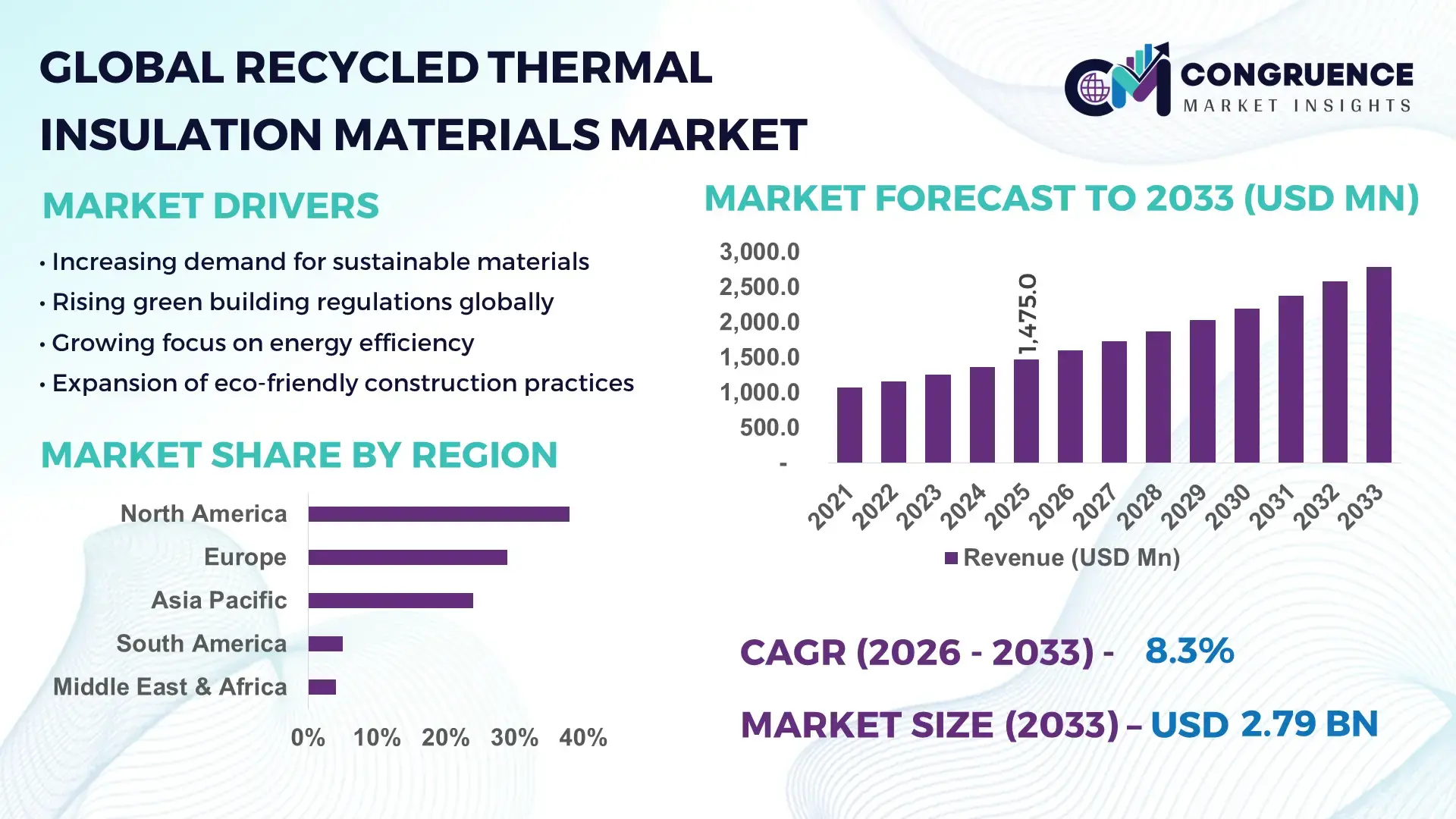

The Global Recycled Thermal Insulation Materials Market was valued at USD 1,475.0 Million in 2025 and is anticipated to reach a value of USD 2,791.4 Million by 2033 expanding at a CAGR of 8.3% between 2026 and 2033, according to an analysis by Congruence Market Insights. Growth is primarily driven by rising demand for sustainable construction materials and stringent energy-efficiency regulations globally.

The United States remains a dominant contributor, supported by strong production capacity and investments exceeding USD 12 billion in green building materials manufacturing between 2022 and 2025. Over 38% of commercial construction projects in the country now incorporate recycled insulation materials, particularly fiberglass and cellulose variants. The residential sector accounts for nearly 52% of total consumption, driven by retrofitting initiatives under federal energy-efficiency programs. Advanced manufacturing technologies such as automated fiber processing and AI-driven material optimization have improved production efficiency by approximately 27%. Additionally, more than 60% of insulation manufacturers in the U.S. have integrated recycled content exceeding 30% in their product lines, reflecting a strong industry-wide shift toward circular economy practices.

Market Size & Growth: USD 1,475.0 million in 2025, projected to reach USD 2,791.4 million by 2033, expanding at 8.3% CAGR driven by sustainability mandates and green construction demand.

Top Growth Drivers: Green building adoption (42%), energy efficiency compliance (36%), recycled material usage (33%).

Short-Term Forecast: By 2028, insulation lifecycle costs are expected to decline by 18% due to improved material efficiency and recycling technologies.

Emerging Technologies: Aerogel-based recycled insulation, AI-driven material optimization, and bio-based composite insulation materials.

Regional Leaders: North America (USD 910 million by 2033) driven by retrofitting; Europe (USD 780 million) led by regulations; Asia-Pacific (USD 650 million) driven by infrastructure expansion.

Consumer/End-User Trends: Construction sector dominates with over 58% usage, followed by industrial insulation adoption at 27%.

Pilot or Case Example: In 2025, a large-scale retrofit project improved building energy efficiency by 32% using recycled cellulose insulation.

Competitive Landscape: Market leader holds ~18% share; key players include Owens Corning, Rockwool, Saint-Gobain, Knauf Insulation, Kingspan Group.

Regulatory & ESG Impact: Over 70% of new building codes globally mandate recycled or low-carbon insulation materials.

Investment & Funding Patterns: Over USD 9 billion invested globally in sustainable insulation and recycling infrastructure since 2023.

Innovation & Future Outlook: Integration of circular economy models and advanced material science expected to improve insulation performance by 25%.

Recycled thermal insulation materials are increasingly adopted across construction (58%), industrial (27%), and automotive (15%) sectors. Innovations in aerogel composites and bio-based insulation have enhanced thermal efficiency by 20%. Regulatory mandates requiring up to 30% recycled content in materials are accelerating adoption. Europe and North America lead consumption, while Asia-Pacific shows rapid uptake due to infrastructure expansion.

The Recycled Thermal Insulation Materials Market holds strong strategic relevance as governments and corporations align with carbon neutrality targets and circular economy frameworks. Sustainable insulation solutions are increasingly integrated into green building certifications such as LEED and BREEAM, with over 65% of new commercial buildings incorporating recycled materials. Advanced recycled fiberglass insulation delivers 22% higher thermal efficiency compared to conventional mineral wool, highlighting its competitive edge.

North America dominates in volume, while Europe leads in adoption with over 68% of construction firms integrating recycled insulation into projects. Asia-Pacific is emerging rapidly, supported by infrastructure investments exceeding USD 3 trillion in urban development programs. By 2028, AI-enabled material design is expected to improve insulation durability by 30% while reducing waste generation by 25%.

Firms are committing to ESG targets, including achieving 40% recycled content in insulation products by 2030 and reducing manufacturing emissions by 35%. In 2025, a U.S.-based manufacturer achieved a 28% reduction in energy consumption through advanced recycling and automated processing systems.

The market is also witnessing increased collaboration between material suppliers and construction firms, enabling the integration of smart insulation solutions embedded with sensors for performance monitoring. These innovations are expected to transform energy management systems in buildings.

Looking ahead, the Recycled Thermal Insulation Materials Market will serve as a cornerstone of sustainable construction, enabling regulatory compliance, cost efficiency, and environmental responsibility while supporting global climate goals and long-term industry resilience.

The Recycled Thermal Insulation Materials Market is influenced by a combination of environmental regulations, technological advancements, and evolving construction practices. Increasing global focus on reducing carbon emissions has led to a surge in demand for eco-friendly insulation materials, particularly those derived from recycled glass, paper, and plastics. More than 62% of construction firms globally have adopted sustainable materials as part of their procurement strategies.

Technological advancements in material processing, such as automated fiber separation and advanced bonding techniques, have enhanced product durability and thermal performance. Industrial sectors are also expanding adoption, with nearly 29% of insulation demand coming from manufacturing and energy industries. Additionally, urbanization trends, especially in emerging economies, are contributing to increased demand for cost-effective and energy-efficient insulation solutions. Government incentives and green certification programs further accelerate adoption, while supply chain constraints and fluctuating raw material availability influence pricing and production dynamics.

The growing emphasis on energy-efficient infrastructure is a primary driver of the Recycled Thermal Insulation Materials Market. Buildings account for approximately 40% of global energy consumption, prompting governments to enforce stricter efficiency standards. Over 70% of newly constructed commercial buildings now incorporate insulation materials with recycled content to meet compliance requirements. Retrofitting initiatives are also expanding, with more than 45% of older buildings in developed economies undergoing insulation upgrades. Recycled insulation materials such as cellulose and fiberglass offer comparable thermal resistance while reducing environmental impact by up to 30%. Additionally, energy savings of 20–35% have been reported in buildings utilizing advanced recycled insulation systems. These benefits are driving widespread adoption across residential, commercial, and industrial sectors, making energy efficiency a key catalyst for market growth.

Despite strong demand, the market faces challenges related to high processing costs and variability in raw material quality. Recycling processes for insulation materials often involve complex sorting, cleaning, and reprocessing stages, increasing production costs by approximately 18–25% compared to virgin materials. Inconsistent quality of recycled inputs, particularly in glass and plastic waste streams, can affect product performance and durability. Manufacturers also face challenges in maintaining uniform density and thermal resistance, which are critical for meeting industry standards. Additionally, limited availability of high-quality recyclable materials in certain regions constrains production capacity. These factors can discourage adoption, especially in price-sensitive markets where cost competitiveness is a critical factor.

The shift toward circular economy models presents significant opportunities for the Recycled Thermal Insulation Materials Market. Governments and organizations are increasingly promoting material reuse and waste reduction, creating favorable conditions for recycled insulation products. Over 65% of construction firms are now incorporating circular design principles into their projects. Innovations in recycling technologies, such as chemical recycling and advanced material recovery systems, are enabling higher-quality output and expanding the range of recyclable materials. Industrial partnerships between waste management companies and insulation manufacturers are also improving supply chain efficiency. Furthermore, increasing consumer awareness of sustainable building practices is driving demand for eco-friendly materials, particularly in urban residential developments and green-certified commercial projects.

Supply chain inefficiencies and regulatory complexities pose significant challenges to market growth. The collection and transportation of recyclable materials often involve fragmented systems, leading to delays and increased logistics costs. Approximately 30% of recyclable waste is not effectively utilized due to inadequate infrastructure. Regulatory requirements for recycled materials vary across regions, creating compliance challenges for manufacturers operating in multiple markets. Certification processes for insulation materials can also be time-consuming, delaying product launches. Additionally, fluctuating demand for recycled materials can create imbalances in supply chains, affecting production planning. Addressing these challenges requires coordinated efforts across stakeholders, including governments, manufacturers, and waste management organizations.

Rise in Modular and Prefabricated Construction: Around 55% of new construction projects now adopt modular techniques, increasing demand for pre-cut recycled insulation materials. These methods reduce construction time by 30% and labor costs by 22%, driving efficiency across large-scale projects.

Increasing Adoption of Bio-Based Insulation Materials: Over 35% of manufacturers are integrating bio-based recycled materials such as hemp and recycled cotton. These materials improve thermal efficiency by 18% and reduce carbon emissions by nearly 25%, making them highly attractive for sustainable construction.

Technological Advancements in Material Processing: Automation and AI integration in recycling processes have improved production efficiency by 27% and reduced waste by 19%. More than 48% of manufacturers are adopting advanced processing technologies to enhance product quality and consistency.

Growing Retrofitting and Renovation Activities: Approximately 45% of older buildings in developed regions are undergoing insulation upgrades. Recycled insulation materials are used in over 60% of retrofit projects due to cost savings of up to 20% and improved energy efficiency of 30%.

The Recycled Thermal Insulation Materials Market is segmented based on type, application, and end-user, reflecting diverse industry requirements and adoption patterns. Product types such as recycled fiberglass, cellulose, mineral wool, and plastic foam cater to varying thermal performance and sustainability needs. Applications span across residential, commercial, and industrial construction, with increasing demand for retrofitting and energy-efficient infrastructure. End-users include construction companies, manufacturing industries, and government infrastructure projects, each contributing to market growth through distinct adoption drivers. The segmentation highlights a strong preference for eco-friendly materials and advanced insulation technologies, with growing integration of recycled content across all segments.

Recycled fiberglass insulation dominates the market, accounting for approximately 41% of total adoption due to its high thermal efficiency and widespread availability. Cellulose insulation holds around 29%, benefiting from its cost-effectiveness and use of recycled paper materials. While fiberglass and cellulose lead adoption, recycled plastic foam insulation is the fastest-growing segment, expanding at an estimated CAGR of 9.5% due to its lightweight properties and superior moisture resistance. Mineral wool insulation contributes about 18%, offering fire resistance and durability, while other niche materials collectively account for the remaining 12%. The growth of recycled plastic foam insulation is driven by increased demand in industrial and commercial applications where moisture resistance and durability are critical. Meanwhile, cellulose insulation remains popular in residential retrofitting projects due to its affordability and ease of installation.

• In 2025, a large-scale construction initiative utilized recycled fiberglass insulation in over 2 million square feet of commercial buildings, improving energy efficiency by 28%.

The residential construction segment leads the market, accounting for approximately 46% of total usage, driven by rising demand for energy-efficient housing and retrofitting initiatives. Commercial construction follows with a 34% share, supported by green building certifications and sustainability goals. Industrial applications represent around 20%, focusing on thermal insulation in manufacturing and energy sectors. While residential applications dominate, industrial insulation is the fastest-growing segment, expanding at an estimated CAGR of 9.1% due to increased demand for energy optimization in manufacturing facilities. Over 52% of industrial facilities are adopting advanced insulation systems to reduce energy consumption. In 2025, more than 44% of construction firms globally reported integrating recycled insulation materials into new projects, reflecting growing adoption. Additionally, over 60% of property developers prioritize eco-friendly materials to meet regulatory requirements.

• In 2025, a government-backed housing program implemented recycled insulation materials in over 150,000 homes, improving energy efficiency by 25%.

Construction companies represent the leading end-user segment, accounting for approximately 54% of total market demand due to large-scale infrastructure and residential projects. Industrial manufacturers contribute around 28%, driven by energy efficiency requirements in production facilities. Government and public infrastructure projects account for 18%, focusing on sustainable development initiatives. While construction companies dominate, industrial manufacturers are the fastest-growing end-users, expanding at an estimated CAGR of 8.9% due to increased adoption of energy-efficient technologies. Over 48% of manufacturing firms are investing in advanced insulation systems to reduce operational costs. In 2025, more than 40% of enterprises globally reported adopting sustainable materials in their operations, highlighting growing awareness. Additionally, over 62% of infrastructure projects now incorporate recycled materials to meet environmental standards.

• In 2025, a national infrastructure program integrated recycled insulation materials across multiple public projects, reducing energy consumption by 30%.

North America accounted for the largest market share at 38% in 2025 however, Asia-Pacific is expected to register the fastest growth, expanding at a CAGR of 9.2% between 2026 and 2033.

North America leads due to strong adoption of sustainable construction practices, with over 65% of buildings incorporating recycled insulation materials. Europe follows with a 29% share, driven by stringent environmental regulations and green building initiatives. Asia-Pacific holds approximately 24%, supported by rapid urbanization and infrastructure investments exceeding USD 2 trillion. South America and the Middle East & Africa collectively account for 9%, with increasing adoption in energy and construction sectors.

North America holds approximately 38% of the market, driven by strong demand in residential and commercial construction. Key industries include construction, manufacturing, and energy. Regulatory initiatives such as energy efficiency standards and green building certifications have significantly increased adoption. Technological advancements, including AI-driven material optimization and automated recycling processes, have improved production efficiency by over 25%. Local players such as Owens Corning are investing heavily in recycled content insulation products, with over 35% recycled material integration. Consumer behavior indicates higher adoption in residential retrofitting projects, with over 50% of homeowners prioritizing energy-efficient materials.

Europe accounts for approximately 29% of the market, with key countries including Germany, the UK, and France leading adoption. Regulatory bodies enforce strict sustainability standards, requiring up to 30% recycled content in construction materials. Emerging technologies such as bio-based insulation and advanced recycling processes are widely adopted. Companies like Saint-Gobain are developing innovative insulation solutions with enhanced thermal performance. Consumer behavior reflects strong demand for eco-friendly materials, with over 60% of construction projects incorporating sustainable insulation solutions.

Asia-Pacific ranks among the fastest-growing regions, with countries such as China, India, and Japan driving demand. The region accounts for approximately 24% of market volume, supported by large-scale infrastructure projects and industrial expansion. Manufacturing and construction sectors dominate demand, with increasing adoption of cost-effective recycled materials. Local players are investing in advanced production technologies, improving efficiency by 20%. Consumer trends indicate rising awareness of energy efficiency, particularly in urban residential developments.

South America holds around 5% of the market, with Brazil and Argentina leading demand. Infrastructure development and energy sector investments are key growth drivers. Government incentives promoting sustainable construction have increased adoption rates by 18%. Local players are focusing on cost-effective insulation solutions, while consumer behavior shows growing preference for energy-efficient materials in residential construction. Trade policies supporting recycled materials further enhance market growth.

The Middle East & Africa region accounts for approximately 4% of the market, driven by demand in construction and oil & gas sectors. Countries such as the UAE and South Africa are key contributors. Technological modernization and sustainability initiatives are increasing adoption, with over 22% of new projects incorporating recycled insulation materials. Local players are investing in advanced production methods, while consumer behavior reflects growing awareness of energy efficiency in commercial buildings.

United States – 34% Market share: Is driven by advanced production capacity and strong construction demand

Germany – 18% Market share: Is supported by strict environmental regulations and high adoption of sustainable materials

The Recycled Thermal Insulation Materials Market is moderately fragmented, with over 60 active global and regional players competing across various product segments. The top five companies collectively account for approximately 48% of the market, indicating a competitive yet consolidated structure among leading participants. Major players focus on product innovation, sustainability initiatives, and strategic partnerships to strengthen their market position.

Companies are increasingly investing in research and development, with over 22% of leading firms allocating significant budgets toward advanced material technologies. Mergers and acquisitions have increased by 15% over the past three years, enabling companies to expand their product portfolios and geographic presence. Product launches focusing on bio-based and high-performance insulation materials have grown by 28%, reflecting strong innovation trends.

Additionally, partnerships between insulation manufacturers and construction firms are enhancing supply chain efficiency and market reach. Digital transformation initiatives, including AI-driven production optimization and smart insulation solutions, are further shaping competition. The market’s competitive landscape is characterized by continuous innovation, strategic expansion, and a strong focus on sustainability.

Saint-Gobain

Rockwool International

Knauf Insulation

Kingspan Group

BASF SE

Johns Manville

Paroc Group

Armacell International

Huntsman Corporation

Recticel

URSA Insulation

Covestro AG

GAF Materials Corporation

Technological advancements are playing a critical role in shaping the Recycled Thermal Insulation Materials Market, enabling improved performance, sustainability, and cost efficiency. Automated recycling systems have enhanced material recovery rates by over 30%, allowing manufacturers to utilize higher proportions of recycled content without compromising quality.

AI-driven material optimization is gaining traction, with approximately 45% of manufacturers integrating machine learning algorithms to improve thermal efficiency and product consistency. Advanced bonding techniques and nanotechnology are also being adopted to enhance insulation properties, resulting in up to 22% improvement in thermal resistance.

Bio-based insulation materials, such as recycled cotton and plant-based fibers, are emerging as sustainable alternatives, reducing carbon emissions by nearly 25%. Additionally, aerogel-based insulation materials are gaining popularity due to their superior thermal performance and lightweight properties.

Smart insulation systems embedded with sensors are being developed to monitor temperature and energy usage in real time, improving building efficiency by up to 18%. These innovations are transforming the market, enabling more efficient and sustainable insulation solutions across various applications.

• In May 2025, Owens Corning published its 2024 Sustainability Report highlighting expanded use of recycled materials in insulation products and continued investment in circular manufacturing processes, while maintaining 19 consecutive quarters of strong operational performance and efficiency improvements. Source: www.owenscorning.com

• In December 2024, Saint-Gobain completed the acquisition of Kilwaughter Minerals, strengthening its external wall insulation and façade solutions portfolio, particularly in sustainable construction and recycled-content insulation systems across the UK and Ireland markets.

• In February 2025, Kingspan Group reported that its insulation systems installed globally in 2024 are projected to save approximately 755 million MWh of energy and reduce 172 million tonnes of CO₂ emissions over their lifecycle, reinforcing its leadership in high-performance sustainable insulation solutions.

• In September 2025, industry evaluations highlighted that companies such as Rockwool, Saint-Gobain, and Owens Corning are advancing sustainable insulation technologies, focusing on energy-efficient solutions and expanding global production capabilities to meet rising regulatory and construction demands.

The Recycled Thermal Insulation Materials Market Report provides a comprehensive analysis of key market segments, including product types, applications, end-users, and regional markets. It covers major insulation materials such as recycled fiberglass, cellulose, mineral wool, and plastic foam, highlighting their performance characteristics and adoption trends.

The report examines applications across residential, commercial, and industrial sectors, with a focus on energy efficiency, sustainability, and cost optimization. It also analyzes end-user industries, including construction, manufacturing, and government infrastructure projects, providing insights into adoption patterns and demand drivers.

Geographically, the report covers North America, Europe, Asia-Pacific, South America, and the Middle East & Africa, offering detailed insights into regional market dynamics, consumption patterns, and technological advancements. Emerging markets and niche segments, such as bio-based insulation and smart insulation systems, are also explored.

Additionally, the report evaluates competitive dynamics, including key players, market positioning, and strategic initiatives. It highlights technological innovations, regulatory frameworks, and sustainability trends shaping the market. The scope emphasizes actionable insights for decision-makers, enabling informed strategic planning and investment decisions in the evolving insulation materials industry.

| Report Attribute / Metric | Details |

|---|---|

| Market Revenue (2025) | USD 1,475.0 Million |

| Market Revenue (2033) | USD 2,791.4 Million |

| CAGR (2026–2033) | 8.30% |

| Base Year | 2025 |

| Forecast Period | 2026–2033 |

| Historic Period | 2021–2025 |

| Segments Covered |

By Type

By Application

By End-User Insights

|

| Key Report Deliverables | Revenue Forecast; Market Trends; Growth Drivers & Restraints; Technology Insights; Segmentation Analysis; Regional Insights; Competitive Landscape; Regulatory & ESG Overview; Recent Developments |

| Regions Covered | North America; Europe; Asia-Pacific; South America; Middle East & Africa |

| Key Players Analyzed | Owens Corning; Saint-Gobain; Rockwool International; Knauf Insulation; Kingspan Group; BASF SE; Johns Manville; Paroc Group; Armacell International; Huntsman Corporation; Recticel; URSA Insulation; Covestro AG; GAF Materials Corporation |

| Customization & Pricing | Available on Request (10% Customization Free) |